Key Insights

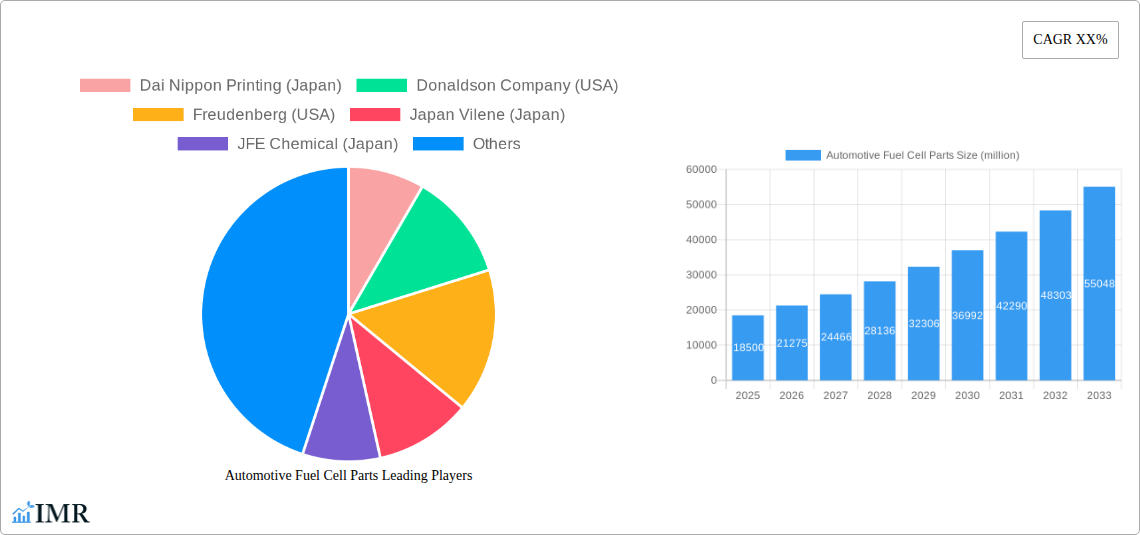

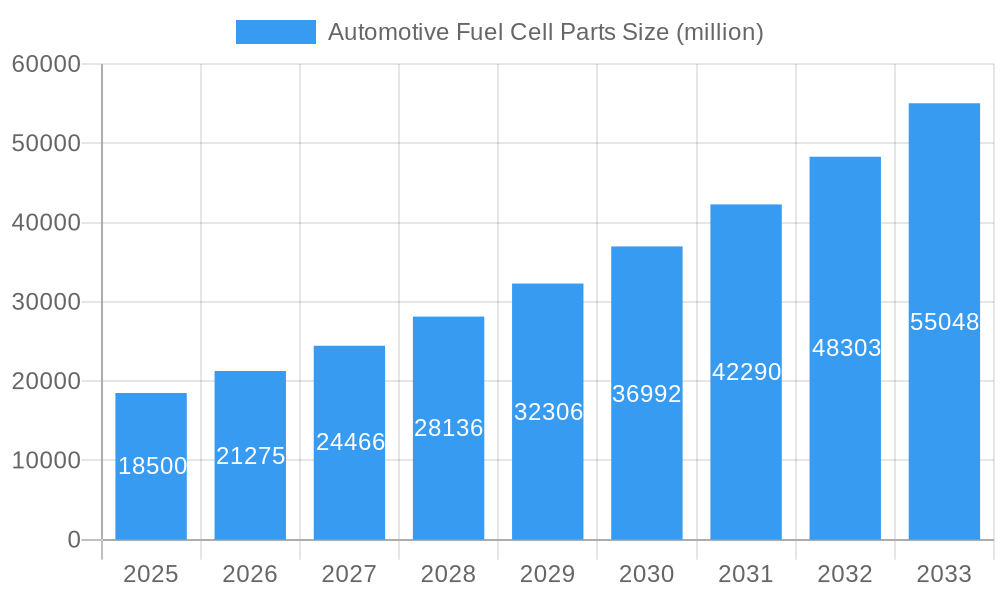

The global Automotive Fuel Cell Parts market is poised for significant expansion, projected to reach a substantial market size of approximately \$18,500 million by 2025, with an estimated Compound Annual Growth Rate (CAGR) of around 15% through 2033. This robust growth is fueled by the accelerating adoption of fuel cell electric vehicles (FCEVs) across both passenger car and commercial vehicle segments. The increasing demand for zero-emission transportation solutions, driven by stringent environmental regulations and a growing consumer preference for sustainable mobility, serves as a primary catalyst. Key components such as Membrane Electrode Assemblies (MEAs) and Fuel Cell Stack Installation Parts are experiencing heightened demand as manufacturers scale up FCEV production and optimize fuel cell performance and durability. Investments in hydrogen infrastructure and advancements in fuel cell technology, leading to improved efficiency and reduced costs, further bolster market confidence and investment.

Automotive Fuel Cell Parts Market Size (In Billion)

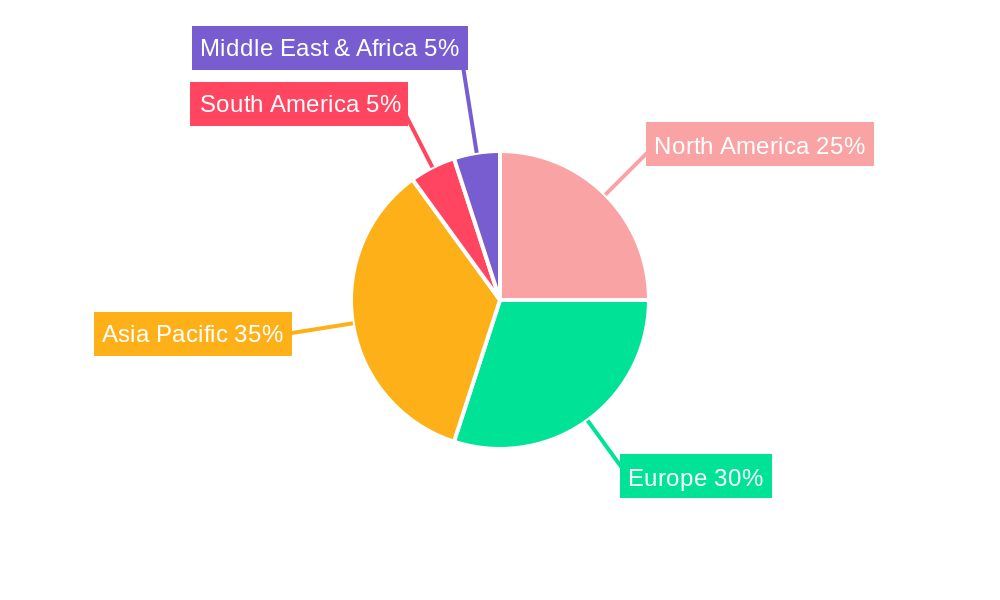

The market is characterized by a dynamic landscape with several key trends shaping its trajectory. The development of more efficient and cost-effective MEAs, crucial for the core function of fuel cells, is a major focus for R&D efforts. Furthermore, the integration of advanced materials and manufacturing techniques for fuel cell stack components is enhancing durability and reducing the overall cost of FCEVs. While the market demonstrates immense potential, certain restraints, such as the high initial cost of FCEVs and the ongoing challenges in establishing a widespread hydrogen refueling infrastructure, need to be addressed for mass market penetration. However, ongoing technological innovations and strategic collaborations among leading companies like Dai Nippon Printing, Donaldson Company, and Toray Industries are actively working to overcome these hurdles, positioning the Automotive Fuel Cell Parts market for sustained and dynamic growth across key regions including Asia Pacific, Europe, and North America.

Automotive Fuel Cell Parts Company Market Share

Automotive Fuel Cell Parts Market Analysis: Driving the Future of Sustainable Mobility

This comprehensive report offers an in-depth analysis of the global Automotive Fuel Cell Parts market, providing critical insights for stakeholders navigating the rapidly evolving landscape of hydrogen-powered vehicles. With a detailed study period spanning from 2019 to 2033, including a base year of 2025 and a forecast period from 2025 to 2033, this report equips you with the intelligence needed to capitalize on emerging opportunities and mitigate potential risks. Leveraging high-traffic keywords like "automotive fuel cell components," "hydrogen fuel cell parts," "MEA market," "fuel cell stack materials," and "FCV parts," this report ensures maximum search engine visibility and engagement within the industry.

Automotive Fuel Cell Parts Market Dynamics & Structure

The Automotive Fuel Cell Parts market, while nascent, is characterized by a dynamic interplay of technological innovation, stringent regulatory frameworks, and increasing environmental consciousness. Market concentration is currently moderate, with a few key players dominating specific segments, but the vast growth potential is attracting new entrants.

- Technological Innovation Drivers: Advancements in Membrane Electrode Assemblies (MEAs), fuel cell stack materials, and balance-of-plant components are crucial for enhancing efficiency, durability, and cost-effectiveness. Research into novel catalyst materials and improved membrane technologies are key innovation frontiers.

- Regulatory Frameworks: Government mandates for emission reduction and incentives for Fuel Cell Electric Vehicle (FCV) adoption are significant drivers. International standards for fuel cell performance and safety are also shaping product development.

- Competitive Product Substitutes: While fuel cells offer a zero-emission alternative, they face competition from Battery Electric Vehicles (BEVs). However, the longer range and faster refueling capabilities of FCVs position them as strong contenders for specific applications, particularly commercial vehicles.

- End-User Demographics: The adoption of FCVs is influenced by consumer awareness of environmental issues, government subsidies, and the availability of hydrogen refueling infrastructure. Fleet operators, especially in the commercial vehicle segment, are showing increasing interest due to operational cost advantages and reduced downtime.

- M&A Trends: The market is witnessing strategic alliances and acquisitions as established automotive suppliers and specialized fuel cell component manufacturers seek to expand their portfolios and gain a competitive edge. The volume of M&A deals is expected to rise as the market matures.

Automotive Fuel Cell Parts Growth Trends & Insights

The Automotive Fuel Cell Parts market is poised for remarkable growth, driven by a confluence of factors including escalating demand for sustainable transportation solutions, supportive government policies, and significant technological advancements. The market size is projected to expand at an impressive Compound Annual Growth Rate (CAGR) of XX% during the forecast period, reaching an estimated value of XXX million units by 2033. This robust growth trajectory is underpinned by increasing adoption rates of Fuel Cell Electric Vehicles (FCVs) across both passenger car and commercial vehicle segments.

Technological disruptions are at the forefront of this evolution. Innovations in Membrane Electrode Assemblies (MEAs) are continuously improving their durability, performance, and cost-effectiveness, making them a more viable option for mass production. Similarly, advancements in Fuel Cell Stack Installation Parts are contributing to lighter, more compact, and highly efficient fuel cell systems. The development of advanced materials and manufacturing processes for these critical components is a key differentiator for market players.

Consumer behavior is also shifting. As awareness of climate change intensifies and governments implement stricter emission regulations, consumers are increasingly seeking cleaner mobility alternatives. The superior range and rapid refueling capabilities of FCVs, compared to their battery-electric counterparts, are becoming more attractive, particularly for long-haul transportation and commercial applications. This shift in preference is a significant catalyst for market penetration.

The global push towards decarbonization, exemplified by international agreements and national emission reduction targets, provides a strong policy tailwind for the fuel cell industry. Governments worldwide are offering substantial incentives, subsidies, and tax credits for FCV purchases and hydrogen infrastructure development, further accelerating adoption. The expanding hydrogen refueling network, though still in its nascent stages in many regions, is crucial for alleviating range anxiety and fostering consumer confidence.

Furthermore, the evolving energy landscape, with a growing emphasis on renewable hydrogen production, is enhancing the sustainability credentials of fuel cell technology. The integration of fuel cells with renewable energy sources creates a truly green powertrain solution, appealing to environmentally conscious consumers and corporations alike. The report projects the market penetration of FCVs to reach XX% by 2033, a testament to the growing acceptance and viability of this technology.

Dominant Regions, Countries, or Segments in Automotive Fuel Cell Parts

The global Automotive Fuel Cell Parts market is experiencing significant growth, with distinct regions, countries, and product segments emerging as dominant forces. This dominance is shaped by a combination of supportive government policies, robust infrastructure development, strong research and development capabilities, and burgeoning end-user demand.

Dominant Segment: Passenger Cars

While commercial vehicles are a crucial growth area for fuel cell technology due to their operational advantages, the Passenger Cars segment is projected to lead the market in terms of volume and overall market share in the near to medium term. This leadership is driven by several key factors:

- Government Mandates and Incentives: Many leading automotive nations have implemented ambitious targets for reducing tailpipe emissions and promoting zero-emission vehicles. These mandates are often coupled with substantial purchase incentives, tax credits, and registration benefits for FCVs, making them more accessible and attractive to individual consumers. For instance, countries like Japan and South Korea have been pioneers in supporting FCV development and adoption.

- Infrastructure Development: Significant investments are being channeled into building a comprehensive hydrogen refueling infrastructure, particularly in densely populated urban areas and along major transportation corridors. The increasing availability of refueling stations directly addresses consumer concerns about range anxiety and makes FCV ownership more practical.

- Automotive Manufacturer Investment: Major global automotive manufacturers are heavily investing in the research, development, and production of FCV passenger cars. This commitment signifies a belief in the long-term viability of fuel cell technology for personal mobility and translates into a wider range of available models and improved vehicle performance. Companies like Toyota with its Mirai, and Hyundai with its Nexo, are leading this charge, showcasing advancements in Membrane Electrode Assemblies (MEAs) and Fuel Cell Stack Installation Parts.

- Technological Advancements and Cost Reduction: Continuous innovation in fuel cell components, particularly MEAs and stack materials, is leading to improved efficiency, durability, and a reduction in the overall cost of fuel cell systems. As these costs decline, FCVs become more price-competitive with traditional internal combustion engine vehicles and battery-electric vehicles.

- Consumer Awareness and Perception: Growing public awareness of environmental issues and the benefits of zero-emission transportation is influencing purchasing decisions. FCVs, with their fast refueling times and longer range compared to some BEVs, are appealing to a segment of consumers seeking convenience and performance without compromising on sustainability.

Key Drivers Shaping Passenger Car Dominance:

- Economic Policies: Favorable tax structures, subsidies for FCV purchases, and investment in hydrogen infrastructure development create a conducive market environment.

- Infrastructure: The strategic expansion of hydrogen refueling stations in urban centers and along key travel routes is paramount for consumer adoption.

- R&D Investment: Significant funding for research into more efficient and cost-effective fuel cell technologies, including advancements in MEAs and stack components, fuels innovation.

- Consumer Demand: Growing environmental consciousness and the desire for a premium, sustainable driving experience are influencing purchasing behavior.

While Commercial Vehicles represent a significant growth opportunity driven by operational efficiency and emissions regulations in logistics and public transport, the sheer volume of the global passenger car market, coupled with early adoption initiatives and manufacturer commitment, positions passenger cars as the dominant segment in the near term. The evolution of Fuel Cell Stack Installation Parts and the cost-effectiveness of Membrane Electrode Assemblies (MEAs) will be critical in solidifying this dominance and expanding market reach.

Automotive Fuel Cell Parts Product Landscape

The Automotive Fuel Cell Parts sector is defined by continuous innovation in critical components essential for the efficient operation of hydrogen fuel cell systems. Leading the charge are Membrane Electrode Assemblies (MEAs), which are the heart of the fuel cell, facilitating the electrochemical reaction. Advancements focus on enhancing durability, reducing platinum catalyst loading, and improving power density. Fuel Cell Stack Installation Parts, including bipolar plates, gaskets, and end plates, are also undergoing significant evolution. These components are optimized for weight reduction, improved thermal management, and enhanced sealing to ensure the longevity and performance of the entire fuel cell stack. Manufacturers are also focusing on the development of specialized materials that can withstand harsh operating conditions, contributing to a more robust and cost-effective fuel cell ecosystem.

Key Drivers, Barriers & Challenges in Automotive Fuel Cell Parts

Key Drivers:

- Stringent Emission Regulations: Global mandates to reduce greenhouse gas emissions are a primary catalyst for the adoption of zero-emission technologies like fuel cells.

- Government Incentives and Subsidies: Financial support for FCV purchase, manufacturing, and hydrogen infrastructure development significantly accelerates market growth.

- Technological Advancements: Continuous improvements in Membrane Electrode Assemblies (MEAs) and Fuel Cell Stack Installation Parts are enhancing performance, durability, and cost-effectiveness.

- Demand for Extended Range and Faster Refueling: Fuel cell vehicles offer advantages in range and refueling time over battery-electric vehicles, making them attractive for certain applications.

- Growing Environmental Awareness: Increasing consumer and corporate demand for sustainable transportation solutions fuels the market.

Barriers & Challenges:

- High Cost of Fuel Cell Systems: The current manufacturing costs of fuel cell components, particularly platinum catalysts and advanced membranes, remain a significant barrier to widespread adoption.

- Limited Hydrogen Refueling Infrastructure: The scarcity and uneven distribution of hydrogen refueling stations pose a major challenge for consumer acceptance and operational feasibility.

- Hydrogen Production and Distribution Costs: The cost and carbon intensity of producing and distributing hydrogen can impact the overall environmental and economic viability of FCVs.

- Durability and Longevity Concerns: While improving, the long-term durability and lifespan of fuel cell components still require further validation and enhancement.

- Competition from Battery Electric Vehicles (BEVs): BEVs benefit from established charging infrastructure and rapidly falling battery costs, presenting strong competition.

- Supply Chain Development: Establishing a robust and scalable supply chain for specialized fuel cell components is crucial for mass production.

- Regulatory Harmonization: Variations in international regulations and standards for fuel cells and hydrogen can create complexities for global manufacturers.

Emerging Opportunities in Automotive Fuel Cell Parts

The Automotive Fuel Cell Parts industry is ripe with emerging opportunities, particularly in the development of next-generation Membrane Electrode Assemblies (MEAs) with reduced reliance on precious metals and enhanced durability. The expansion of hydrogen refueling infrastructure presents a significant opportunity for companies involved in the production of associated components, such as high-pressure tanks and dispensing systems. Furthermore, the increasing focus on circular economy principles within the automotive sector is driving opportunities in the recycling and refurbishment of fuel cell components, including stacks and MEAs. The growing demand for heavy-duty commercial vehicles, long-haul trucking, and specialized industrial applications (e.g., forklifts, buses) also represents a substantial untapped market for fuel cell technology.

Growth Accelerators in the Automotive Fuel Cell Parts Industry

Several key factors are acting as growth accelerators for the Automotive Fuel Cell Parts industry. Significant investments in research and development by both established automotive manufacturers and specialized component suppliers are continuously pushing the boundaries of technological innovation. Strategic partnerships and collaborations between these entities are crucial for sharing expertise, mitigating risks, and accelerating the commercialization of new products and technologies. The expansion of hydrogen refueling infrastructure, driven by government initiatives and private sector investment, is directly reducing adoption barriers for fuel cell vehicles. Moreover, the increasing commitment of major automotive original equipment manufacturers (OEMs) to develop and launch a wider range of fuel cell electric vehicles is a powerful signal to the market, stimulating demand for the underlying components and fostering a more robust ecosystem.

Key Players Shaping the Automotive Fuel Cell Parts Market

- Dai Nippon Printing

- Donaldson Company

- Freudenberg

- Japan Vilene

- JFE Chemical

- NICHIAS

- Nisshin Seiko

- NOK

- Sumitomo

- Toray Industries

Notable Milestones in Automotive Fuel Cell Parts Sector

- 2019/01: Toyota announces plans for significant investment in fuel cell technology, signaling continued commitment.

- 2020/07: Hyundai launches the all-new Nexo fuel cell SUV, showcasing advancements in performance and durability.

- 2021/03: The European Union revises its hydrogen strategy, emphasizing the role of fuel cells in transport.

- 2022/05: Major automotive suppliers announce partnerships to develop next-generation Membrane Electrode Assemblies (MEAs).

- 2022/11: Governments worldwide pledge increased funding for hydrogen refueling infrastructure development.

- 2023/02: Development of novel catalyst materials for Membrane Electrode Assemblies (MEAs) with significantly reduced platinum content announced.

- 2023/08: First large-scale commercial truck fleet powered by fuel cells begins operations in North America.

- 2024/01: Toray Industries announces expansion of its Membrane Electrode Assembly (MEA) production capacity.

- 2024/06: New government regulations in China mandate increased adoption of zero-emission vehicles, including FCVs.

In-Depth Automotive Fuel Cell Parts Market Outlook

The Automotive Fuel Cell Parts market is poised for sustained and significant growth, fueled by a global imperative for decarbonization and the inherent advantages of fuel cell technology in specific automotive applications. The continued acceleration of technological advancements, particularly in the efficiency and cost reduction of Membrane Electrode Assemblies (MEAs) and Fuel Cell Stack Installation Parts, will be pivotal in expanding market penetration. Strategic investments in hydrogen infrastructure, coupled with supportive government policies, will further de-risk adoption for both consumers and manufacturers. The growing commitment from leading automotive players to integrate fuel cell technology into their product portfolios creates substantial demand, fostering a positive feedback loop for innovation and market expansion. This outlook suggests a future where fuel cells play an increasingly critical role in achieving cleaner and more sustainable mobility.

Automotive Fuel Cell Parts Segmentation

-

1. Application

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

-

2. Types

- 2.1. Membrane Electrode Assemblies

- 2.2. Fuel Cell Stack Installation Parts

- 2.3. Others

Automotive Fuel Cell Parts Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Fuel Cell Parts Regional Market Share

Geographic Coverage of Automotive Fuel Cell Parts

Automotive Fuel Cell Parts REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.78% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Membrane Electrode Assemblies

- 5.2.2. Fuel Cell Stack Installation Parts

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Automotive Fuel Cell Parts Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Cars

- 6.1.2. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Membrane Electrode Assemblies

- 6.2.2. Fuel Cell Stack Installation Parts

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Automotive Fuel Cell Parts Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Cars

- 7.1.2. Commercial Vehicles

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Membrane Electrode Assemblies

- 7.2.2. Fuel Cell Stack Installation Parts

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Automotive Fuel Cell Parts Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Cars

- 8.1.2. Commercial Vehicles

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Membrane Electrode Assemblies

- 8.2.2. Fuel Cell Stack Installation Parts

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Automotive Fuel Cell Parts Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Cars

- 9.1.2. Commercial Vehicles

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Membrane Electrode Assemblies

- 9.2.2. Fuel Cell Stack Installation Parts

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Automotive Fuel Cell Parts Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Cars

- 10.1.2. Commercial Vehicles

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Membrane Electrode Assemblies

- 10.2.2. Fuel Cell Stack Installation Parts

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Automotive Fuel Cell Parts Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Passenger Cars

- 11.1.2. Commercial Vehicles

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Membrane Electrode Assemblies

- 11.2.2. Fuel Cell Stack Installation Parts

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Dai Nippon Printing (Japan)

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Donaldson Company (USA)

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Freudenberg (USA)

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Japan Vilene (Japan)

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 JFE Chemical (Japan)

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 NICHIAS (Japan)

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Nisshin Seiko (Japan)

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 NOK (Japan)

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Sumitomo (Japan)

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Toray Industries (Japan)

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Dai Nippon Printing (Japan)

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Automotive Fuel Cell Parts Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Automotive Fuel Cell Parts Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Automotive Fuel Cell Parts Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Fuel Cell Parts Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Automotive Fuel Cell Parts Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive Fuel Cell Parts Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Automotive Fuel Cell Parts Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Fuel Cell Parts Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Automotive Fuel Cell Parts Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Fuel Cell Parts Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Automotive Fuel Cell Parts Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive Fuel Cell Parts Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Automotive Fuel Cell Parts Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Fuel Cell Parts Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Automotive Fuel Cell Parts Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Fuel Cell Parts Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Automotive Fuel Cell Parts Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive Fuel Cell Parts Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Automotive Fuel Cell Parts Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Fuel Cell Parts Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Fuel Cell Parts Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Fuel Cell Parts Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive Fuel Cell Parts Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive Fuel Cell Parts Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Fuel Cell Parts Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Fuel Cell Parts Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Fuel Cell Parts Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Fuel Cell Parts Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive Fuel Cell Parts Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive Fuel Cell Parts Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Fuel Cell Parts Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Fuel Cell Parts Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Fuel Cell Parts Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Automotive Fuel Cell Parts Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Fuel Cell Parts Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Fuel Cell Parts Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Automotive Fuel Cell Parts Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Fuel Cell Parts Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Fuel Cell Parts Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Automotive Fuel Cell Parts Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Fuel Cell Parts Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Fuel Cell Parts Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Automotive Fuel Cell Parts Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Fuel Cell Parts Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Fuel Cell Parts Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Automotive Fuel Cell Parts Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Fuel Cell Parts Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Fuel Cell Parts Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Automotive Fuel Cell Parts Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Fuel Cell Parts Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Fuel Cell Parts?

The projected CAGR is approximately 13.78%.

2. Which companies are prominent players in the Automotive Fuel Cell Parts?

Key companies in the market include Dai Nippon Printing (Japan), Donaldson Company (USA), Freudenberg (USA), Japan Vilene (Japan), JFE Chemical (Japan), NICHIAS (Japan), Nisshin Seiko (Japan), NOK (Japan), Sumitomo (Japan), Toray Industries (Japan).

3. What are the main segments of the Automotive Fuel Cell Parts?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Fuel Cell Parts," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Fuel Cell Parts report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Fuel Cell Parts?

To stay informed about further developments, trends, and reports in the Automotive Fuel Cell Parts, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence