Key Insights

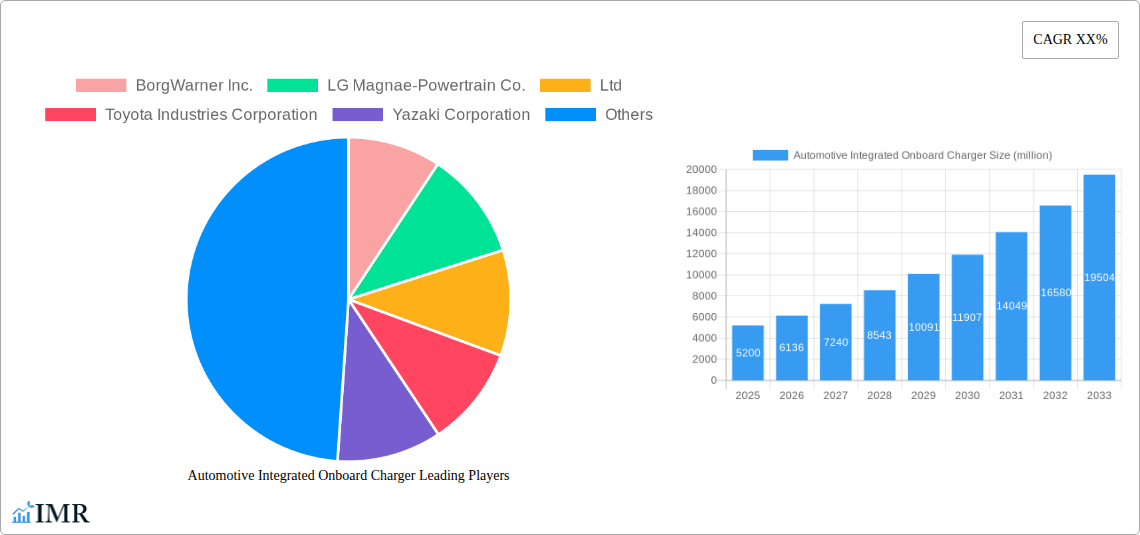

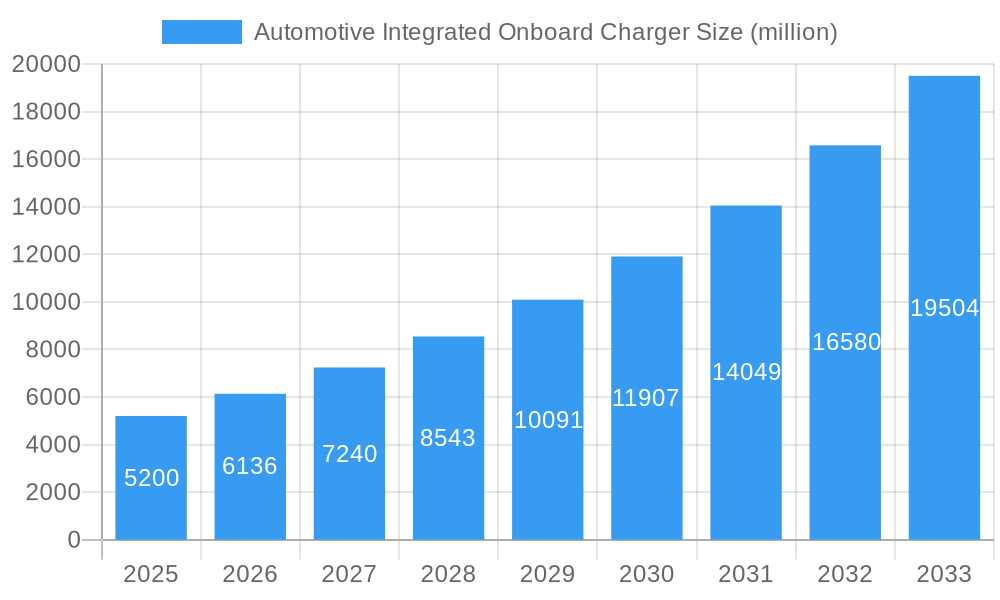

The global Automotive Integrated Onboard Charger market is projected for significant expansion, driven by the accelerating adoption of electric vehicles (EVs) and stringent emission regulations worldwide. With a substantial market size estimated at approximately $5,200 million in 2025, the sector is poised for robust growth, anticipating a Compound Annual Growth Rate (CAGR) of around 18% through 2033. This upward trajectory is primarily fueled by the increasing demand for cleaner transportation solutions, government incentives for EV purchases, and advancements in charging infrastructure technology. The integration of onboard chargers within EVs is becoming a critical feature, enhancing convenience and user experience by enabling charging directly from AC power sources. This integration streamlines the charging process, reducing the reliance on external charging stations for basic battery replenishment. The market's growth is further bolstered by the rising consumer awareness regarding environmental sustainability and the long-term cost benefits associated with EV ownership, making integrated onboard chargers an indispensable component.

Automotive Integrated Onboard Charger Market Size (In Billion)

The market dynamics are characterized by key drivers such as evolving automotive electrification strategies from major manufacturers and the continuous innovation in battery technology, which necessitates more efficient and compact charging solutions. The prevalence of both passenger cars and commercial vehicles transitioning to electric powertrains underscores the broad applicability of integrated onboard chargers. Key market restraints include the high initial cost of EVs and related charging infrastructure, as well as challenges in establishing a widespread and standardized charging network. However, ongoing technological advancements in areas like DC-DC converters and faster charging capabilities are expected to mitigate some of these limitations. The competitive landscape is dominated by established automotive suppliers and specialized electronics manufacturers, including BorgWarner Inc., LG Magna e-Powertrain Co., Ltd., Toyota Industries Corporation, and Robert Bosch GmbH, who are heavily investing in research and development to capture a larger market share in this rapidly expanding domain.

Automotive Integrated Onboard Charger Company Market Share

Here's a compelling and SEO-optimized report description for Automotive Integrated Onboard Chargers, designed for maximum industry visibility and engagement:

Report Title: Automotive Integrated Onboard Charger Market Analysis: Dynamics, Growth, and Future Outlook (2019-2033)

Report Description:

Unlock critical insights into the rapidly expanding Automotive Integrated Onboard Charger (IOC) market. This comprehensive report provides an in-depth analysis of market dynamics, growth trends, regional dominance, product innovations, key drivers, emerging opportunities, and the competitive landscape shaping the electric vehicle (EV) and hybrid electric vehicle (HEV) charging infrastructure. Delve into market segmentation by application (Passenger Cars, Commercial Vehicles) and type (On-board Charger, DC-DC Converter), gaining a granular understanding of segment-specific growth trajectories.

The Automotive Integrated Onboard Charger market is experiencing unprecedented growth, driven by the global shift towards sustainable mobility and stringent emission regulations. This report offers a forward-looking perspective, forecasting market evolution from 2025 to 2033, with a detailed look at the base year 2025 and historical data from 2019-2024. We examine the intricate interplay of technological advancements, evolving consumer preferences, and robust regulatory frameworks that are accelerating the adoption of advanced EV charging solutions.

This analysis is crucial for automotive manufacturers, Tier 1 suppliers, technology providers, investors, and policymakers seeking to capitalize on the burgeoning e-mobility sector. Understand the competitive strategies of key players like BorgWarner Inc., LG Magna e-Powertrain Co.,Ltd, Toyota Industries Corporation, Yazaki Corporation, Meta System S.P.A, Vitesco Technologies GmbH, Nichicon Corporation, Panasonic Corporation, Robert Bosch GmbH, and Texas Instruments, and identify potential collaborations and strategic partnerships.

Key Report Highlights:

This report is indispensable for stakeholders aiming to secure a competitive edge in the dynamic and high-growth Automotive Integrated Onboard Charger market.

- Market Size & CAGR: Detailed market size estimations in million units and projected Compound Annual Growth Rate (CAGR) for the forecast period.

- Segmentation Analysis: In-depth analysis of the Passenger Cars and Commercial Vehicles segments, and the On-board Charger and DC-DC Converter types.

- Regional Dominance: Identification and analysis of leading regions and countries driving market expansion.

- Technological Innovations: Exploration of cutting-edge technologies and product advancements.

- Parent & Child Markets: Understanding the influence of broader automotive and power electronics markets on the IOC sector, and the impact of IOCs on downstream EV component markets.

- Competitive Intelligence: Profiles of key market players and their strategic initiatives.

- Future Outlook: Strategic recommendations and insights for navigating the evolving automotive charging ecosystem.

Automotive Integrated Onboard Charger Market Dynamics & Structure

The Automotive Integrated Onboard Charger (IOC) market is characterized by a moderately concentrated structure, with a blend of established automotive suppliers and specialized power electronics manufacturers vying for market share. Technological innovation remains a primary driver, fueled by the relentless pursuit of higher charging efficiency, faster charging speeds, and enhanced vehicle integration. Regulatory frameworks, particularly those mandating EV adoption and emissions reductions globally, are profoundly influencing market dynamics, pushing manufacturers to invest heavily in advanced charging technologies. Competitive product substitutes, such as external charging stations and battery swapping solutions, present ongoing challenges, though the convenience and space-saving benefits of integrated onboard chargers are increasingly favored. End-user demographics are shifting, with a growing segment of environmentally conscious consumers and fleet operators demanding seamless and efficient EV charging experiences. Mergers and acquisitions (M&A) activity is notable, with larger players acquiring innovative startups to bolster their technological portfolios and expand market reach. For instance, M&A deal volumes are projected to reach approximately $XX billion in the forecast period, with innovation barriers such as the high cost of R&D and the need for extensive safety certifications acting as moderating factors.

- Market Concentration: Moderately concentrated with key players dominating, but opportunities for niche players exist.

- Technological Innovation Drivers: Increased EV adoption, demand for faster charging, miniaturization, and cost reduction.

- Regulatory Frameworks: Stringent emission standards, government incentives for EVs, and charging infrastructure mandates.

- Competitive Product Substitutes: External charging stations, battery swapping, and emerging wireless charging technologies.

- End-User Demographics: Growing demand from individual consumers, fleet operators, and public transportation sectors.

- M&A Trends: Strategic acquisitions to gain technological expertise and market share, with projected deal volumes of $XX billion.

Automotive Integrated Onboard Charger Growth Trends & Insights

The Automotive Integrated Onboard Charger (IOC) market is poised for significant expansion, driven by the accelerating global transition towards electric mobility. The market size is projected to grow from an estimated $XX billion in 2025 to $YY billion by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of XX% during the forecast period. This impressive growth trajectory is underpinned by increasing EV adoption rates worldwide, which are expected to reach approximately XX% of new vehicle sales by 2033. Technological disruptions are at the forefront of this evolution, with advancements in silicon carbide (SiC) and gallium nitride (GaN) power semiconductors leading to more efficient, compact, and lighter onboard chargers. These innovations are crucial for overcoming range anxiety and improving the overall user experience of electric vehicles.

Consumer behavior shifts are also playing a pivotal role. As the cost of EVs becomes more competitive and charging infrastructure more accessible, consumers are increasingly embracing electric vehicles for their daily commutes and long-distance travel. This burgeoning demand for EVs directly translates into a higher demand for integrated onboard charging solutions. The convenience of charging at home or at workplaces without the need for external charging equipment is a significant draw for consumers. Furthermore, the integration of bidirectional charging capabilities within onboard chargers is emerging as a key trend, allowing EVs to not only draw power but also to feed electricity back into the grid or a home energy system, thereby enhancing grid stability and offering new revenue streams for EV owners. The development of higher power onboard chargers, capable of supporting ultra-fast charging scenarios, is also a significant growth accelerator, reducing charging times and making EV ownership more practical for a wider audience.

The underlying parent market of automotive electronics and the burgeoning market for EV components are creating a fertile ground for IOC growth. As the complexity and functionality of EVs increase, the demand for sophisticated, integrated solutions like onboard chargers will only intensify. The market penetration of onboard chargers is directly correlated with the penetration of EVs, and as more consumers opt for electric powertrains, the demand for these essential components will naturally rise. The focus on sustainability and reduced carbon footprints is a universal theme, driving investments in EV technology and, consequently, in the critical infrastructure that supports them.

Dominant Regions, Countries, or Segments in Automotive Integrated Onboard Charger

The Automotive Integrated Onboard Charger (IOC) market exhibits a clear dominance in the Passenger Cars segment, which is expected to account for over XX% of the total market revenue by 2033. This segment's preeminence is driven by several factors, including the widespread consumer appeal of electric passenger vehicles, significant government incentives, and the rapid expansion of charging infrastructure in key automotive markets. The increasing number of EV models available in the passenger car category, coupled with declining battery costs, makes electric passenger vehicles a more accessible and attractive option for a broader consumer base.

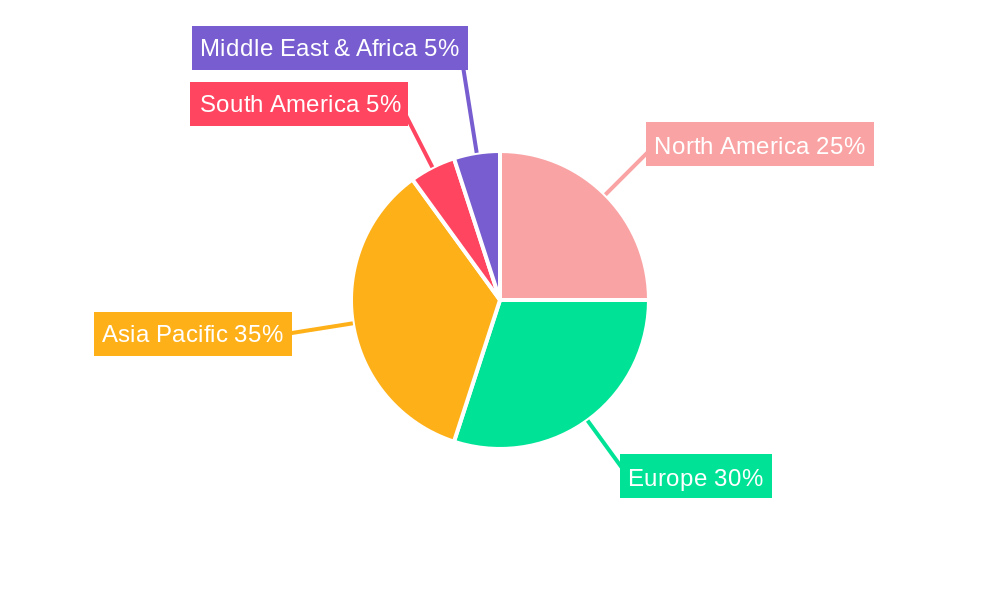

Geographically, Asia-Pacific is emerging as the dominant region in the Automotive Integrated Onboard Charger market, driven primarily by China, which is the world's largest EV market. China's robust government support for electric vehicle manufacturing and adoption, coupled with substantial investments in charging infrastructure, positions it as a leader. The region's dominance is further bolstered by the presence of major automotive manufacturers and a rapidly growing consumer base for electric vehicles. The market share for the Asia-Pacific region is projected to reach XX% by 2033, with countries like South Korea and Japan also contributing significantly to growth.

Within the Type segmentation, the On-board Charger segment is the primary growth driver, anticipated to capture over XX% of the market share by 2033. Onboard chargers are integral to the EV's powertrain, facilitating the conversion of AC electricity from charging stations into DC electricity required by the battery. The continuous innovation in charger power output, efficiency, and integration capabilities is fueling this segment's dominance. While DC-DC Converters are also crucial components in EV powertrains, managing voltage conversion for various vehicle systems, their market size is comparatively smaller than that of onboard chargers. The growth potential for DC-DC converters is still significant, however, as they play a vital role in optimizing power distribution and enhancing overall vehicle efficiency, especially in higher-voltage EV architectures.

Economic policies such as tax credits, subsidies for EV purchases, and investments in public charging infrastructure are critical enablers of market growth in dominant regions and countries. For example, the European Union's ambitious Green Deal and stringent CO2 emission targets for new vehicles are accelerating the shift towards EVs and, consequently, the demand for onboard chargers. The infrastructure development in countries like Germany, Norway, and the UK further supports this trend. North America, particularly the United States, is also witnessing substantial growth driven by federal and state-level incentives and the increasing product offerings from major automakers.

Automotive Integrated Onboard Charger Product Landscape

The Automotive Integrated Onboard Charger (IOC) product landscape is characterized by rapid advancements in power density, efficiency, and smart charging capabilities. Manufacturers are continuously innovating to deliver smaller, lighter, and more powerful chargers that seamlessly integrate into vehicle architectures. Key innovations include the adoption of wide-bandgap semiconductor technologies like Silicon Carbide (SiC) and Gallium Nitride (GaN), which significantly improve power conversion efficiency, reduce heat generation, and enable more compact designs. Performance metrics such as charging power (ranging from 3.7 kW to over 22 kW for AC charging) and charging efficiency (typically exceeding 90%) are crucial selling propositions. Furthermore, the trend towards bidirectional charging, enabling Vehicle-to-Grid (V2G) and Vehicle-to-Home (V2H) functionalities, is a significant technological advancement, offering added value to EV owners and supporting grid stability.

Key Drivers, Barriers & Challenges in Automotive Integrated Onboard Charger

Key Drivers: The Automotive Integrated Onboard Charger (IOC) market is propelled by several potent drivers. The accelerating global adoption of electric vehicles (EVs) and hybrid electric vehicles (HEVs) is the foremost catalyst, directly increasing the demand for these essential charging components. Stringent government regulations and mandates aimed at reducing carbon emissions, such as the EU's CO2 targets and CAFE standards in the US, are compelling automakers to electrify their fleets. Technological advancements in battery technology, leading to longer EV ranges and faster charging capabilities, further encourage consumer adoption and, consequently, the demand for sophisticated onboard chargers. Government incentives, including purchase subsidies and tax credits for EVs and charging infrastructure, also play a crucial role in making EVs more affordable and accessible.

Barriers & Challenges: Despite the robust growth, the Automotive Integrated Onboard Charger market faces several significant challenges. High manufacturing costs associated with advanced power electronics and rare earth materials can lead to higher vehicle prices, potentially hindering mass adoption. Supply chain disruptions, particularly for semiconductors and other critical electronic components, can impact production volumes and timelines. Evolving charging standards and interoperability issues across different charging networks and vehicle manufacturers can create confusion and inconvenience for consumers. Intense competition among established players and new entrants can lead to price pressures and necessitate continuous innovation to maintain market share. Regulatory hurdles and the need for extensive safety certifications for integrated electronic systems also add to the complexity and time-to-market for new products. The ongoing development and widespread availability of external charging infrastructure also present a competitive alternative, albeit with less integration convenience.

Emerging Opportunities in Automotive Integrated Onboard Charger

Emerging opportunities within the Automotive Integrated Onboard Charger (IOC) market are diverse and promising. The growing demand for higher power density and faster charging solutions for electric vehicles presents a significant avenue for innovation. Bidirectional charging capabilities, enabling Vehicle-to-Grid (V2G) and Vehicle-to-Home (V2H) applications, are becoming increasingly important, offering grid stabilization and potential revenue generation for EV owners. The integration of wireless charging technology within onboard chargers also represents a future growth area, offering enhanced convenience. Furthermore, the expansion of the EV market into developing economies presents untapped markets with significant growth potential as charging infrastructure and consumer awareness increase. The development of standardized, modular, and software-defined onboard charging systems that can be easily updated and adapted to future needs also offers a competitive advantage.

Growth Accelerators in the Automotive Integrated Onboard Charger Industry

Several key growth accelerators are shaping the future trajectory of the Automotive Integrated Onboard Charger (IOC) industry. The continuous advancements in power electronics, particularly the adoption of Silicon Carbide (SiC) and Gallium Nitride (GaN) semiconductors, are leading to higher efficiency, smaller form factors, and reduced costs for onboard chargers. Strategic partnerships and collaborations between automotive OEMs, Tier 1 suppliers, and technology providers are crucial for co-developing next-generation charging solutions and accelerating market penetration. The expanding global charging infrastructure, including fast-charging networks, is creating a more favorable ecosystem for EV adoption, directly benefiting the demand for onboard chargers. Furthermore, the increasing electrification of commercial vehicle fleets, such as buses and delivery vans, represents a significant untapped market segment with high growth potential. The development of robust and reliable charging solutions that can withstand diverse environmental conditions is also critical for long-term growth.

Key Players Shaping the Automotive Integrated Onboard Charger Market

- BorgWarner Inc.

- LG Magna e-Powertrain Co.,Ltd

- Toyota Industries Corporation

- Yazaki Corporation

- Meta System S.P.A

- Vitesco Technologies GmbH

- Nichicon Corporation

- Panasonic Corporation

- Robert Bosch GmbH

- Texas Instruments

Notable Milestones in Automotive Integrated Onboard Charger Sector

- 2019: Introduction of 11kW and 22kW onboard chargers by major Tier 1 suppliers, enabling faster AC charging.

- 2020: Increased adoption of SiC technology in onboard chargers by companies like Vitesco Technologies for improved efficiency.

- 2021: Launch of bidirectional charging capabilities in select premium EV models, signaling a new era for IOC functionality.

- 2022: Major automotive OEMs announce plans to integrate advanced onboard charging solutions across their EV portfolios, increasing market demand.

- 2023: Significant R&D investments by players like Bosch and Panasonic in next-generation, compact, and highly efficient onboard charger designs.

- 2024: Growing focus on smart charging features and connectivity integration within onboard chargers for optimized grid interaction and user experience.

In-Depth Automotive Integrated Onboard Charger Market Outlook

The future outlook for the Automotive Integrated Onboard Charger (IOC) market is exceptionally bright, propelled by the overarching trend of vehicle electrification. Growth accelerators such as advancements in wide-bandgap semiconductors, strategic collaborations among industry leaders, and the continuous expansion of EV charging infrastructure will fuel substantial market expansion. The increasing demand for higher charging speeds, bidirectional power flow capabilities (V2G/V2H), and enhanced vehicle integration will drive continuous innovation. Opportunities in the commercial vehicle sector and emerging markets present substantial untapped potential. Stakeholders who invest in R&D for more efficient, cost-effective, and feature-rich onboard charging solutions are well-positioned to capitalize on this rapidly evolving and high-growth industry. The integration of intelligent charging features and enhanced connectivity will further solidify the IOC's role as a critical component in the sustainable mobility ecosystem.

Automotive Integrated Onboard Charger Segmentation

-

1. Application

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

-

2. Types

- 2.1. On-board Charger

- 2.2. DC-DC Converter

Automotive Integrated Onboard Charger Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Integrated Onboard Charger Regional Market Share

Geographic Coverage of Automotive Integrated Onboard Charger

Automotive Integrated Onboard Charger REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. On-board Charger

- 5.2.2. DC-DC Converter

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Automotive Integrated Onboard Charger Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Cars

- 6.1.2. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. On-board Charger

- 6.2.2. DC-DC Converter

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Automotive Integrated Onboard Charger Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Cars

- 7.1.2. Commercial Vehicles

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. On-board Charger

- 7.2.2. DC-DC Converter

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Automotive Integrated Onboard Charger Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Cars

- 8.1.2. Commercial Vehicles

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. On-board Charger

- 8.2.2. DC-DC Converter

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Automotive Integrated Onboard Charger Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Cars

- 9.1.2. Commercial Vehicles

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. On-board Charger

- 9.2.2. DC-DC Converter

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Automotive Integrated Onboard Charger Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Cars

- 10.1.2. Commercial Vehicles

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. On-board Charger

- 10.2.2. DC-DC Converter

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Automotive Integrated Onboard Charger Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Passenger Cars

- 11.1.2. Commercial Vehicles

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. On-board Charger

- 11.2.2. DC-DC Converter

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 BorgWarner Inc.

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 LG Magnae-Powertrain Co.

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Ltd

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Toyota Industries Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Yazaki Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Meta System S.P.A

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Vitesco Technologies GmbH

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Nichicon Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Panasonic Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Robert Bosch GmbH

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Texas Instruments

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 BorgWarner Inc.

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Automotive Integrated Onboard Charger Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Integrated Onboard Charger Revenue (million), by Application 2025 & 2033

- Figure 3: North America Automotive Integrated Onboard Charger Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Integrated Onboard Charger Revenue (million), by Types 2025 & 2033

- Figure 5: North America Automotive Integrated Onboard Charger Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive Integrated Onboard Charger Revenue (million), by Country 2025 & 2033

- Figure 7: North America Automotive Integrated Onboard Charger Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Integrated Onboard Charger Revenue (million), by Application 2025 & 2033

- Figure 9: South America Automotive Integrated Onboard Charger Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Integrated Onboard Charger Revenue (million), by Types 2025 & 2033

- Figure 11: South America Automotive Integrated Onboard Charger Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive Integrated Onboard Charger Revenue (million), by Country 2025 & 2033

- Figure 13: South America Automotive Integrated Onboard Charger Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Integrated Onboard Charger Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Automotive Integrated Onboard Charger Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Integrated Onboard Charger Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Automotive Integrated Onboard Charger Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive Integrated Onboard Charger Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Automotive Integrated Onboard Charger Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Integrated Onboard Charger Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Integrated Onboard Charger Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Integrated Onboard Charger Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive Integrated Onboard Charger Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive Integrated Onboard Charger Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Integrated Onboard Charger Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Integrated Onboard Charger Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Integrated Onboard Charger Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Integrated Onboard Charger Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive Integrated Onboard Charger Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive Integrated Onboard Charger Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Integrated Onboard Charger Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Integrated Onboard Charger Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Integrated Onboard Charger Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Automotive Integrated Onboard Charger Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Integrated Onboard Charger Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Integrated Onboard Charger Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Automotive Integrated Onboard Charger Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Integrated Onboard Charger Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Integrated Onboard Charger Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Automotive Integrated Onboard Charger Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Integrated Onboard Charger Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Integrated Onboard Charger Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Automotive Integrated Onboard Charger Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Integrated Onboard Charger Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Integrated Onboard Charger Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Automotive Integrated Onboard Charger Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Integrated Onboard Charger Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Integrated Onboard Charger Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Automotive Integrated Onboard Charger Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Integrated Onboard Charger Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Integrated Onboard Charger?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Automotive Integrated Onboard Charger?

Key companies in the market include BorgWarner Inc., LG Magnae-Powertrain Co., Ltd, Toyota Industries Corporation, Yazaki Corporation, Meta System S.P.A, Vitesco Technologies GmbH, Nichicon Corporation, Panasonic Corporation, Robert Bosch GmbH, Texas Instruments.

3. What are the main segments of the Automotive Integrated Onboard Charger?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Integrated Onboard Charger," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Integrated Onboard Charger report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Integrated Onboard Charger?

To stay informed about further developments, trends, and reports in the Automotive Integrated Onboard Charger, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence