Key Insights

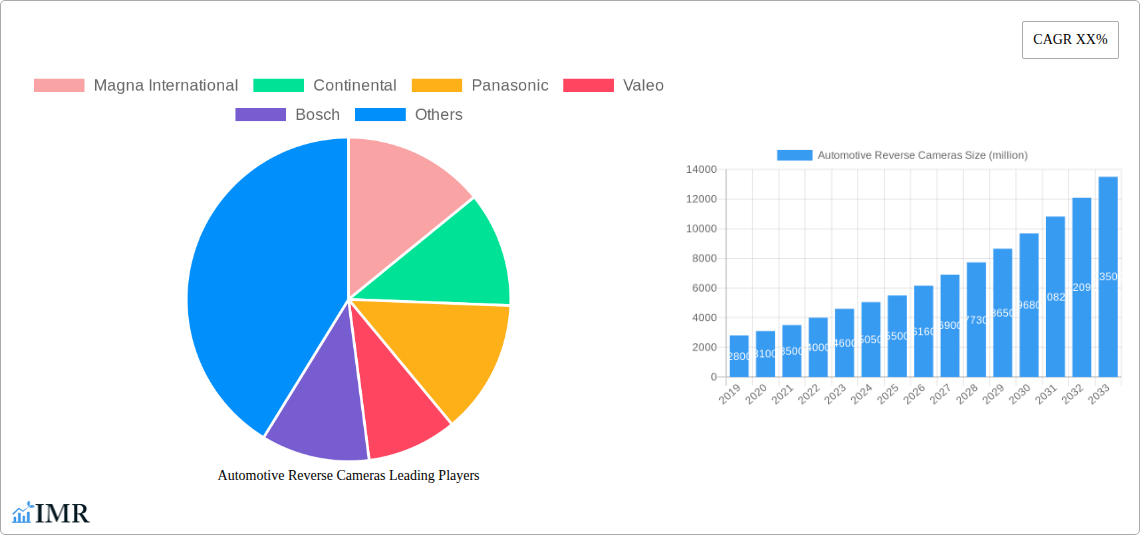

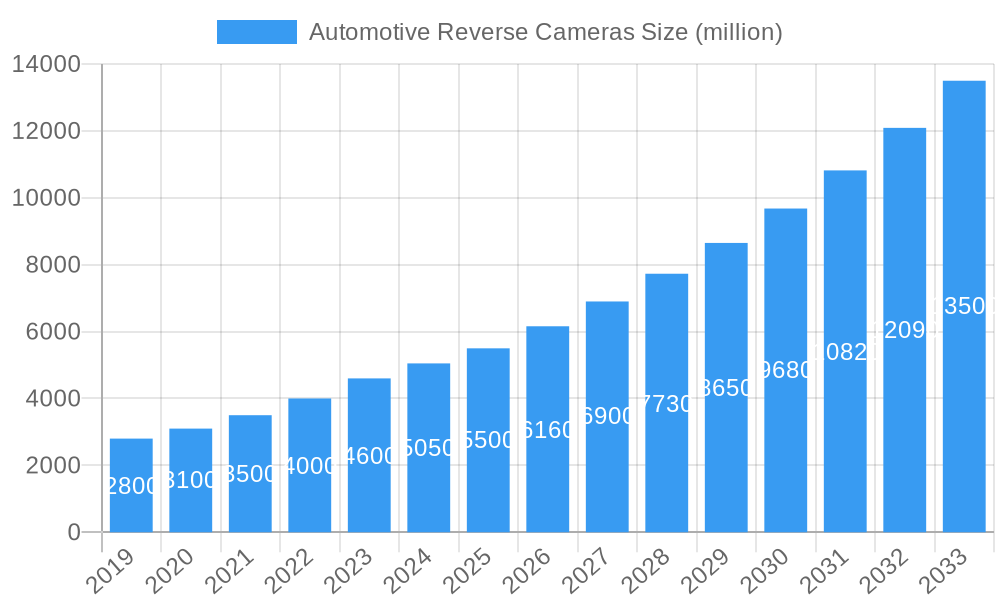

The global Automotive Reverse Camera market is experiencing robust expansion, projected to reach approximately USD 5,500 million in 2025. This growth is fueled by a Compound Annual Growth Rate (CAGR) of around 12%, indicating a dynamic and evolving sector. The increasing integration of advanced driver-assistance systems (ADAS) and the growing consumer demand for enhanced vehicle safety are primary drivers. Regulatory mandates in various regions, pushing for greater visibility and collision avoidance in vehicles, further propel market adoption. The market is segmented into applications spanning both private cars and commercial vehicles, with private cars currently dominating due to higher production volumes and rising consumer awareness. In terms of technology, both CCD and CMOS cameras hold significant market share, with CMOS cameras gaining traction due to their cost-effectiveness and superior performance in various lighting conditions.

Automotive Reverse Cameras Market Size (In Billion)

Key trends shaping the Automotive Reverse Camera market include the miniaturization of camera components, enabling sleeker integration into vehicle designs, and the increasing adoption of higher resolution and wider field-of-view cameras for improved situational awareness. The development of AI-powered image processing and object recognition capabilities within reverse camera systems is also a significant trend, moving beyond simple rearview imaging to offer predictive safety features. However, the market faces certain restraints, including the initial cost of advanced camera systems, which can impact adoption in budget-conscious segments, and concerns regarding data privacy and cybersecurity as camera systems become more interconnected. Despite these challenges, the sustained focus on automotive safety, coupled with technological advancements, positions the Automotive Reverse Camera market for continued strong growth in the forecast period.

Automotive Reverse Cameras Company Market Share

Automotive Reverse Cameras Market Dynamics & Structure

The global automotive reverse camera market exhibits a moderately concentrated structure, driven by significant technological advancements and stringent regulatory mandates. The increasing focus on vehicle safety and the adoption of Advanced Driver-Assistance Systems (ADAS) are primary innovation drivers. Regulatory frameworks worldwide are progressively making rear-view cameras a standard safety feature, particularly in new vehicle registrations, pushing demand. Competitive product substitutes, while present in the form of parking sensors, are largely complementary rather than direct replacements, as cameras offer superior visual information. End-user demographics show a growing preference for vehicles equipped with these safety features across both private car and commercial vehicle segments, with an increasing emphasis from fleet operators prioritizing driver safety and operational efficiency. Mergers and Acquisitions (M&A) trends are active, as major Tier-1 automotive suppliers consolidate their offerings and expand their ADAS portfolios. For instance, in 2023, there were an estimated 15 significant M&A deals focused on ADAS technologies, including camera systems. Innovation barriers are primarily related to high R&D costs for advanced imaging and processing technologies, as well as the need for robust integration into complex vehicle architectures.

- Market Concentration: Moderately concentrated, with key players holding substantial market share.

- Technological Innovation Drivers: ADAS integration, AI-powered object recognition, low-light performance enhancements, and miniaturization of camera modules.

- Regulatory Frameworks: Mandates in North America and Europe for mandatory rear-view camera installation are significant demand drivers.

- Competitive Product Substitutes: Parking sensors, while complementary, do not offer the same level of visual data.

- End-User Demographics: Growing consumer demand for safety features, increased adoption in commercial fleets for enhanced safety and liability reduction.

- M&A Trends: Consolidation among Tier-1 suppliers to enhance ADAS offerings and technological capabilities. Estimated 15 significant M&A deals in 2023 related to ADAS.

Automotive Reverse Cameras Growth Trends & Insights

The automotive reverse camera market is poised for robust expansion, propelled by an ever-increasing emphasis on vehicle safety and the broader integration of intelligent driving technologies. The global market size for automotive reverse cameras is projected to reach approximately $12.5 billion in 2025, with an anticipated Compound Annual Growth Rate (CAGR) of around 8.7% during the forecast period of 2025–2033. This significant growth is fueled by escalating consumer awareness regarding road safety and the proactive adoption of advanced driver-assistance systems (ADAS) by automakers. Regulatory mandates, such as those requiring rear-view cameras in new vehicles in major markets like the United States, continue to be a foundational driver, ensuring a baseline demand.

Technological disruptions are further accelerating adoption. The shift from traditional CCD cameras to advanced CMOS sensors, offering enhanced image quality, lower power consumption, and superior low-light performance, is a key trend. The integration of artificial intelligence (AI) and machine learning algorithms within camera systems is enabling more sophisticated functionalities, such as pedestrian and obstacle detection, cross-traffic alerts, and even basic autonomous parking capabilities. This evolution transforms reverse cameras from simple aids into integral components of a vehicle's intelligent sensing suite.

Consumer behavior is also undergoing a discernible shift. As drivers become more accustomed to the safety benefits provided by these systems, there's a growing expectation for them to be standard equipment, even in entry-level vehicle segments. The increasing prevalence of infotainment systems with large displays further enhances the user experience of reverse camera systems, making them more intuitive and appealing. For the parent market of automotive cameras, the reverse camera segment is a substantial contributor, accounting for an estimated 35% of the total automotive camera market revenue in 2025, projected to grow to $35.7 billion by 2033. The child market for high-definition automotive cameras within the reverse camera segment is experiencing an even faster CAGR of 9.2%.

- Market Size Evolution: Projected to reach $12.5 billion in 2025, with significant growth anticipated.

- Adoption Rates: Steadily increasing due to regulatory mandates and consumer demand. Estimated market penetration of 78% in new passenger vehicles by 2025.

- Technological Disruptions: Transition to CMOS sensors, AI integration for advanced detection, and improved imaging capabilities.

- Consumer Behavior Shifts: Growing expectation for standard safety features, enhanced user experience with integrated displays.

- CAGR: Approximately 8.7% for the automotive reverse camera market during 2025–2033.

- Parent Market Contribution: Automotive reverse cameras to represent 35% of the total automotive camera market revenue in 2025.

- Child Market Growth: High-definition automotive cameras within the reverse camera segment showing a CAGR of 9.2%.

Dominant Regions, Countries, or Segments in Automotive Reverse Cameras

The Private Cars segment stands out as the dominant force driving growth within the global automotive reverse camera market. In 2025, this segment is estimated to account for approximately 85% of the total market revenue, projected to reach $10.6 billion. This dominance is largely attributed to the sheer volume of passenger vehicle production worldwide and the increasing standardization of reverse cameras as a crucial safety feature by major automotive manufacturers. The increasing disposable income in emerging economies and a heightened consumer awareness regarding vehicle safety further bolster demand for private cars equipped with these systems.

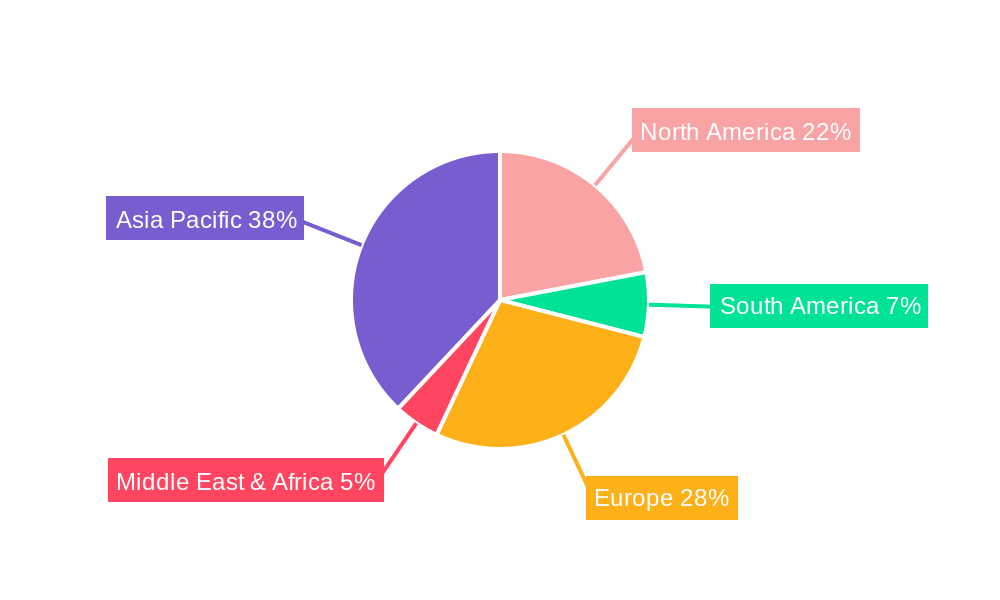

North America and Europe currently lead in terms of market penetration and revenue due to stringent safety regulations and a mature automotive market. The United States, in particular, has mandated the inclusion of rear-view camera systems in all new vehicles since May 2018, creating a substantial and consistent demand. European countries are also progressively aligning with these safety standards, further consolidating the region's leadership. In 2025, North America is expected to hold an estimated 30% market share, followed closely by Europe with 28%.

The CMOS Cameras type segment is rapidly gaining traction and is poised to surpass CCD cameras in market share by 2026. In 2025, CMOS cameras are expected to capture around 60% of the market, valued at $7.5 billion. Their superior image quality, lower power consumption, and cost-effectiveness compared to CCD technology make them the preferred choice for modern automotive applications. The continuous advancements in CMOS sensor technology, enabling higher resolution, better dynamic range, and improved low-light performance, are key drivers for this shift.

- Dominant Segment (Application): Private Cars, accounting for an estimated 85% of market revenue in 2025, projected to reach $10.6 billion.

- Leading Regions: North America (30% market share in 2025) and Europe (28% market share in 2025) due to regulatory mandates and market maturity.

- Dominant Segment (Type): CMOS Cameras, projected to capture 60% market share in 2025, valued at $7.5 billion, due to superior performance and cost-effectiveness.

- Key Drivers for Private Cars: High production volumes, increasing consumer demand for safety, regulatory mandates, and rising disposable incomes.

- Key Drivers for CMOS Cameras: Technological advancements, cost efficiency, enhanced image quality, and lower power consumption.

- Growth Potential in Emerging Markets: Significant untapped potential in Asia-Pacific and Latin America as automotive production and safety awareness grow.

Automotive Reverse Cameras Product Landscape

The automotive reverse camera landscape is characterized by continuous innovation focused on enhancing imaging capabilities, miniaturization, and integration with advanced vehicle systems. Modern systems offer high-definition video output (e.g., 1080p resolution) for crystal-clear visuals, significantly improving driver awareness. Features such as dynamic trajectory lines, which adjust based on steering wheel input, provide intuitive guidance for parking maneuvers. Advanced low-light performance and wide-angle lenses are becoming standard, ensuring visibility in various lighting conditions and blind spots. Integration with AI-powered object detection algorithms is a key technological advancement, enabling the identification of pedestrians, cyclists, and other vehicles. The increasing trend towards surround-view camera systems, combining multiple cameras for a 360-degree view, further elevates the product offering and safety proposition.

Key Drivers, Barriers & Challenges in Automotive Reverse Cameras

The automotive reverse camera market is propelled by several key drivers. Regulatory Mandates from governments worldwide, requiring the installation of rear-view cameras in new vehicles, form a foundational demand. The growing consumer emphasis on Vehicle Safety and the increasing adoption of ADAS features by OEMs are also significant motivators. Technological advancements, such as improved image sensors and AI integration, are making these systems more effective and desirable.

However, the market faces certain barriers and challenges. High R&D Costs associated with developing sophisticated imaging and processing technologies can be a hurdle for smaller players. Supply Chain Disruptions, as evidenced by recent global events, can impact the availability and cost of critical components like image sensors. Integration Complexity within vehicle electronics architectures requires significant engineering effort and standardization. Intense Competitive Pressures from established Tier-1 suppliers and emerging technology companies also pose a challenge, driving down prices and demanding continuous innovation.

Emerging Opportunities in Automotive Reverse Cameras

Emerging opportunities in the automotive reverse camera sector lie in the increasing demand for enhanced functionalities beyond basic rear-view imaging. The integration of AI-powered analytics for real-time threat detection and driver assistance is a significant growth avenue. The expansion of these camera systems into commercial vehicle fleets, where safety and operational efficiency are paramount, presents a vast untapped market. Furthermore, the development of cost-effective, high-resolution camera solutions tailored for emerging economies will unlock new consumer segments. The growing trend of smart city integration and vehicle-to-infrastructure (V2I) communication could also see reverse cameras playing a role in broader traffic management systems.

Growth Accelerators in the Automotive Reverse Cameras Industry

Several factors are accelerating growth in the automotive reverse cameras industry. The relentless pace of technological breakthroughs in sensor technology, image processing, and AI is continuously improving system performance and enabling new features. Strategic partnerships between camera manufacturers, semiconductor suppliers, and automotive OEMs are streamlining development and market penetration. The increasing adoption of ADAS packages as a whole, where reverse cameras are an integral component, further bolsters their deployment. Furthermore, proactive market expansion strategies targeting regions with developing automotive markets and increasing safety awareness are driving volume growth.

Key Players Shaping the Automotive Reverse Cameras Market

- Magna International

- Continental

- Panasonic

- Valeo

- Bosch

- ZF Friedrichshafen

- Denso

- Sony

- MCNEX

- LG Innotek

- Aptiv

- Veoneer

- Samsung Electro Mechanics (SEMCO)

- HELLA GmbH

- TungThih Electronic

- OFILM

- Suzhou Invo Automotive Electronics

- Desay SV

Notable Milestones in Automotive Reverse Cameras Sector

- May 2018: US mandates rear-view camera systems for all new vehicles.

- 2020: Introduction of AI-powered pedestrian and cyclist detection in commercial reverse camera systems.

- 2021: Widespread adoption of dynamic trajectory lines in mid-range passenger vehicles.

- 2022: Significant advancements in low-light CMOS sensor technology enabling clearer night-time visibility.

- 2023: Increased integration of reverse cameras with other ADAS sensors for enhanced situational awareness.

- 2024: Introduction of surround-view camera systems becoming more accessible in non-premium vehicle segments.

In-Depth Automotive Reverse Cameras Market Outlook

The future outlook for the automotive reverse camera market is exceptionally strong, driven by an ongoing commitment to vehicle safety and the accelerating integration of intelligent automotive technologies. Growth accelerators, including continuous technological innovation in AI and imaging, strategic collaborations between industry giants, and the expansion of ADAS feature suites, will fuel sustained demand. The increasing penetration of these systems into the commercial vehicle sector and emerging markets presents significant untapped potential. As automotive manufacturers continue to prioritize safety and driver assistance, reverse cameras will remain a critical component, evolving into more sophisticated sensing modules that contribute to the broader ecosystem of autonomous and connected vehicles. This trajectory promises robust market expansion and continued innovation.

Automotive Reverse Cameras Segmentation

-

1. Application

- 1.1. Private Cars

- 1.2. Commercial Vehicles

-

2. Types

- 2.1. CCD Cameras

- 2.2. CMOS Cameras

Automotive Reverse Cameras Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Reverse Cameras Regional Market Share

Geographic Coverage of Automotive Reverse Cameras

Automotive Reverse Cameras REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Private Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. CCD Cameras

- 5.2.2. CMOS Cameras

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Automotive Reverse Cameras Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Private Cars

- 6.1.2. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. CCD Cameras

- 6.2.2. CMOS Cameras

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Automotive Reverse Cameras Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Private Cars

- 7.1.2. Commercial Vehicles

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. CCD Cameras

- 7.2.2. CMOS Cameras

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Automotive Reverse Cameras Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Private Cars

- 8.1.2. Commercial Vehicles

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. CCD Cameras

- 8.2.2. CMOS Cameras

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Automotive Reverse Cameras Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Private Cars

- 9.1.2. Commercial Vehicles

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. CCD Cameras

- 9.2.2. CMOS Cameras

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Automotive Reverse Cameras Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Private Cars

- 10.1.2. Commercial Vehicles

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. CCD Cameras

- 10.2.2. CMOS Cameras

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Automotive Reverse Cameras Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Private Cars

- 11.1.2. Commercial Vehicles

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. CCD Cameras

- 11.2.2. CMOS Cameras

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Magna International

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Continental

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Panasonic

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Valeo

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Bosch

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 ZF Friedrichshafen

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Denso

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Sony

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 MCNEX

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 LG Innotek

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Aptiv

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Veoneer

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Samsung Electro Mechanics (SEMCO)

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 HELLA GmbH

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 TungThih Electronic

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 OFILM

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Suzhou Invo Automotive Electronics

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Desay SV

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.1 Magna International

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Automotive Reverse Cameras Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Reverse Cameras Revenue (million), by Application 2025 & 2033

- Figure 3: North America Automotive Reverse Cameras Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Reverse Cameras Revenue (million), by Types 2025 & 2033

- Figure 5: North America Automotive Reverse Cameras Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive Reverse Cameras Revenue (million), by Country 2025 & 2033

- Figure 7: North America Automotive Reverse Cameras Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Reverse Cameras Revenue (million), by Application 2025 & 2033

- Figure 9: South America Automotive Reverse Cameras Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Reverse Cameras Revenue (million), by Types 2025 & 2033

- Figure 11: South America Automotive Reverse Cameras Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive Reverse Cameras Revenue (million), by Country 2025 & 2033

- Figure 13: South America Automotive Reverse Cameras Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Reverse Cameras Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Automotive Reverse Cameras Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Reverse Cameras Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Automotive Reverse Cameras Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive Reverse Cameras Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Automotive Reverse Cameras Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Reverse Cameras Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Reverse Cameras Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Reverse Cameras Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive Reverse Cameras Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive Reverse Cameras Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Reverse Cameras Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Reverse Cameras Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Reverse Cameras Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Reverse Cameras Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive Reverse Cameras Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive Reverse Cameras Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Reverse Cameras Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Reverse Cameras Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Reverse Cameras Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Automotive Reverse Cameras Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Reverse Cameras Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Reverse Cameras Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Automotive Reverse Cameras Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Reverse Cameras Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Reverse Cameras Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Automotive Reverse Cameras Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Reverse Cameras Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Reverse Cameras Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Automotive Reverse Cameras Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Reverse Cameras Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Reverse Cameras Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Automotive Reverse Cameras Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Reverse Cameras Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Reverse Cameras Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Automotive Reverse Cameras Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Reverse Cameras Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Reverse Cameras?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Automotive Reverse Cameras?

Key companies in the market include Magna International, Continental, Panasonic, Valeo, Bosch, ZF Friedrichshafen, Denso, Sony, MCNEX, LG Innotek, Aptiv, Veoneer, Samsung Electro Mechanics (SEMCO), HELLA GmbH, TungThih Electronic, OFILM, Suzhou Invo Automotive Electronics, Desay SV.

3. What are the main segments of the Automotive Reverse Cameras?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Reverse Cameras," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Reverse Cameras report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Reverse Cameras?

To stay informed about further developments, trends, and reports in the Automotive Reverse Cameras, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence