Key Insights

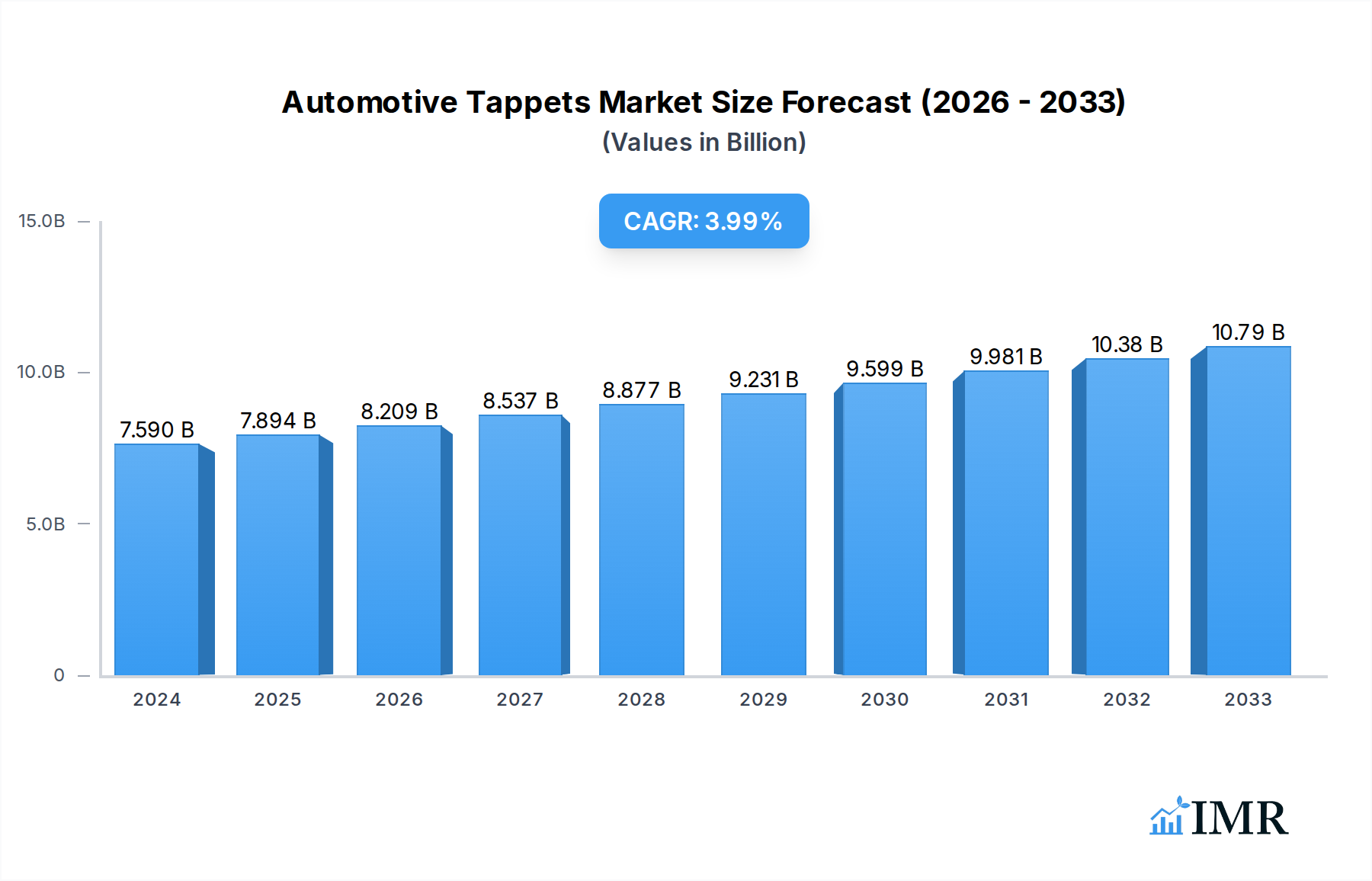

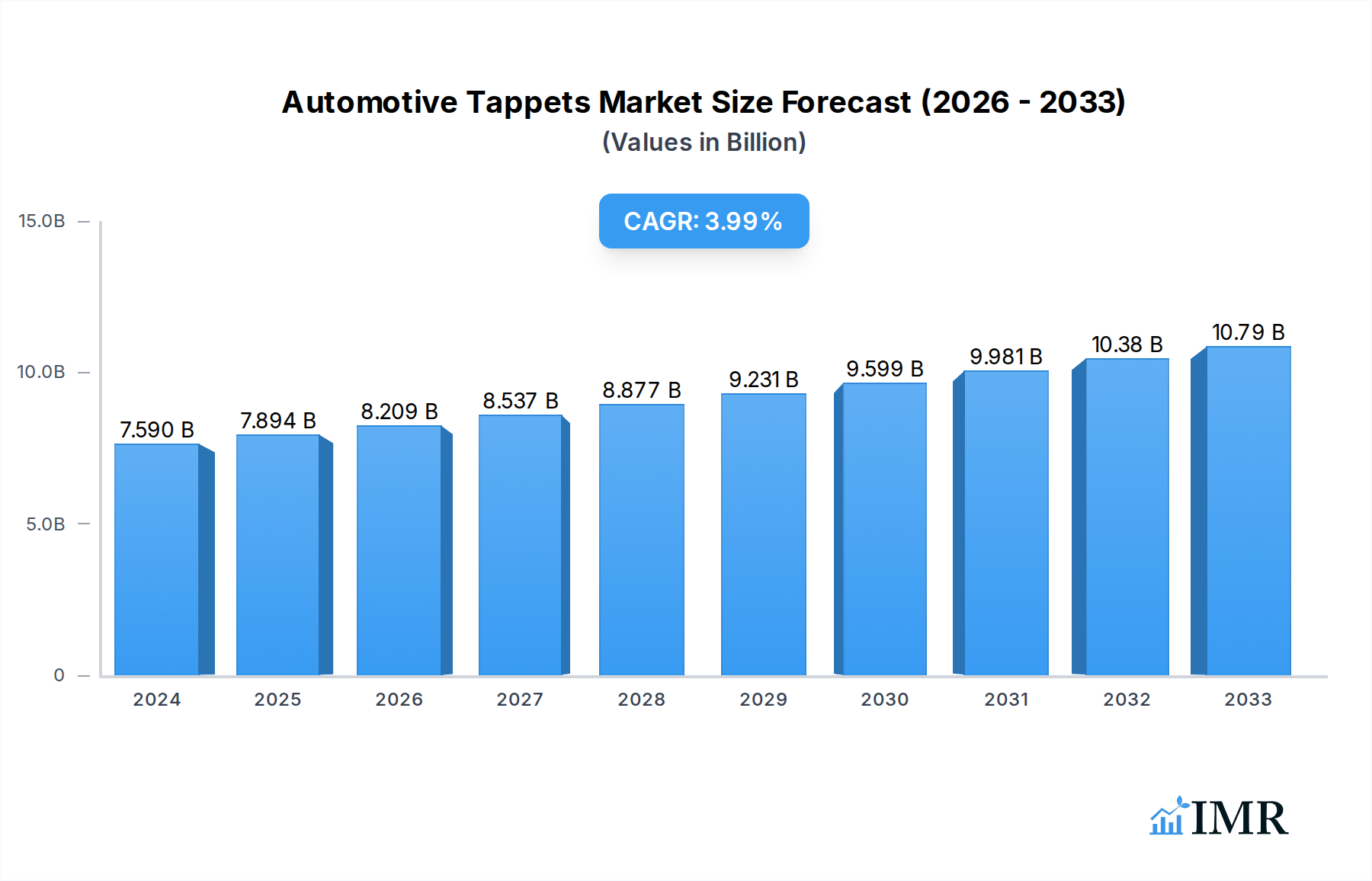

The global Automotive Tappets market is poised for steady expansion, reaching an estimated $7.59 billion in 2024. Driven by the continuous evolution of internal combustion engines (ICE) and the increasing demand for robust engine performance, the market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4% through 2033. While the automotive industry navigates the transition towards electric vehicles, the sheer volume of existing ICE vehicles and the ongoing production of new ones, particularly in emerging economies, ensures sustained demand for tappets. Furthermore, advancements in engine design, focusing on improved fuel efficiency and reduced emissions, necessitate the use of high-quality tappet components. The market's expansion is also supported by the aftermarket replacement segment, catering to the vast installed base of vehicles requiring regular maintenance and part replacements.

Automotive Tappets Market Size (In Billion)

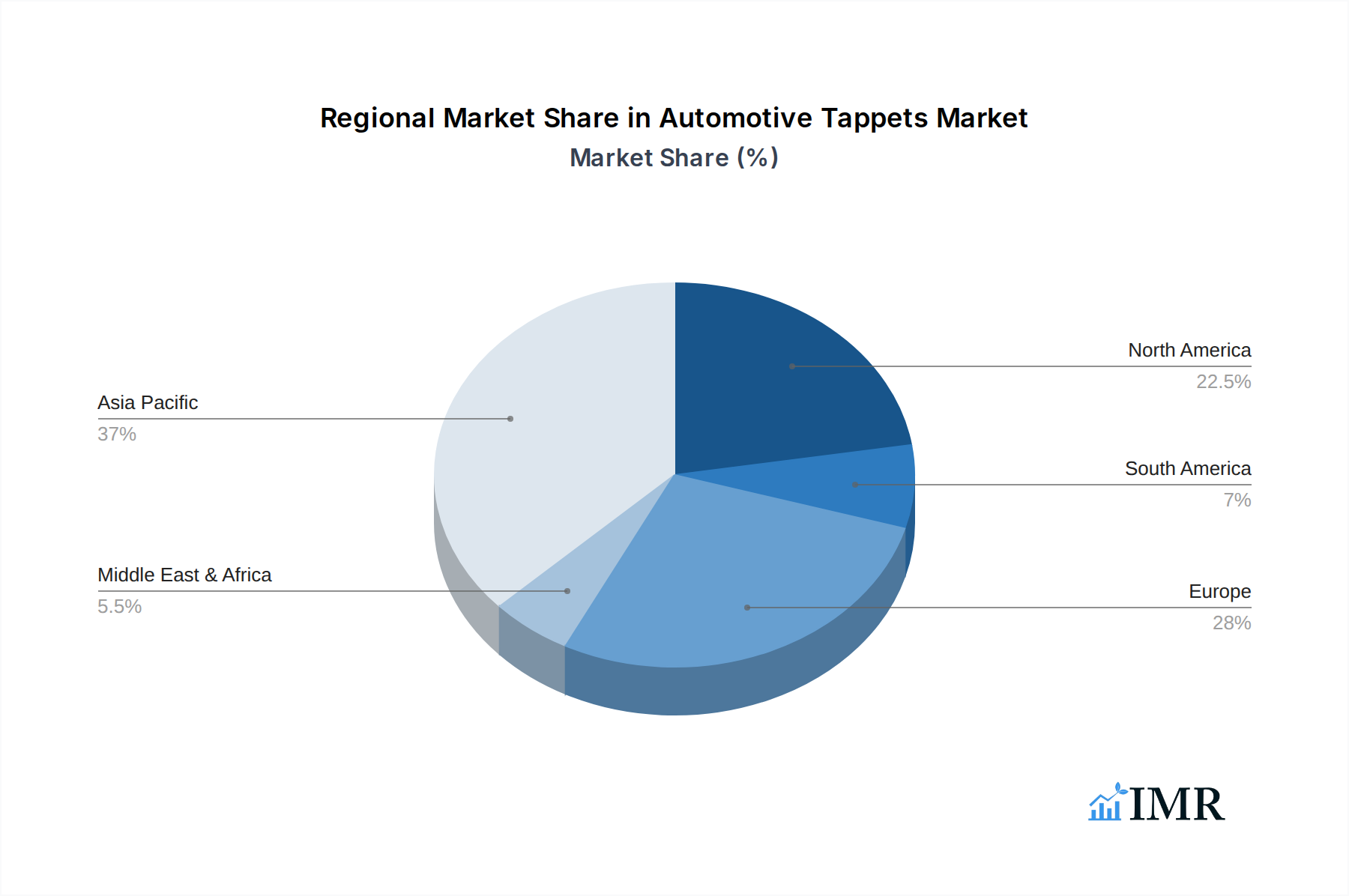

Key trends shaping the Automotive Tappets market include the increasing adoption of advanced materials for enhanced durability and reduced friction, such as specialized coatings and alloys. Innovations in tappet design, aimed at optimizing valve train dynamics and minimizing wear, are also significant drivers. The market is segmented into passenger cars and commercial vehicles, with both segments demonstrating consistent growth. Geographically, Asia Pacific, led by China and India, is expected to remain a dominant region due to its large automotive manufacturing base and burgeoning vehicle parc. North America and Europe continue to represent substantial markets, driven by stringent emission regulations and a strong aftermarket. Challenges, such as the gradual shift towards electric mobility, are being offset by the enduring relevance of ICE technology and the ongoing development of more efficient and cleaner combustion engines.

Automotive Tappets Company Market Share

Automotive Tappets Market Analysis & Forecast: Unveiling Growth Trajectories and Competitive Landscapes (2019-2033)

This comprehensive report offers an in-depth analysis of the global Automotive Tappets market, encompassing its intricate dynamics, growth trends, regional dominance, product innovations, and the strategic landscape shaped by key players. Covering the historical period from 2019 to 2024, with a base year of 2025 and a forecast period extending to 2033, this report provides critical insights for stakeholders across the automotive supply chain. Leveraging advanced analytical frameworks and proprietary data, we dissect the parent market's influence and the burgeoning child markets, offering a holistic view of opportunities and challenges. This report is an indispensable resource for manufacturers, suppliers, investors, and industry analysts seeking to navigate and capitalize on the evolving automotive tappets sector.

Automotive Tappets Market Dynamics & Structure

The global automotive tappets market exhibits a moderately concentrated structure, with a few key players holding significant market share, while a substantial number of smaller manufacturers cater to niche segments. Technological innovation remains a primary driver, fueled by the relentless pursuit of improved engine efficiency, reduced emissions, and enhanced durability. Developments in advanced materials, precision manufacturing, and surface treatments are continuously pushing the boundaries of tappet performance. Regulatory frameworks, particularly concerning vehicle emissions standards and fuel economy mandates, indirectly influence tappet design and material selection. Competitive product substitutes, though limited in direct replacement for tappets within traditional internal combustion engines, emerge from evolving powertrain technologies like electrification, which can lead to a decline in demand for certain tappet types. End-user demographics, characterized by a growing global middle class and increasing vehicle ownership in emerging economies, are contributing to sustained demand. Mergers and acquisitions (M&A) activity, while not as frenetic as in some other automotive sub-sectors, is present as larger entities seek to consolidate their market position and acquire specialized technological expertise.

- Market Concentration: Moderate, with leading global manufacturers dominating a substantial portion of the market.

- Technological Innovation Drivers: Enhanced fuel efficiency, stricter emission regulations, engine performance optimization, and lightweight material development.

- Regulatory Frameworks: Indirect impact through emission standards (e.g., Euro 7, EPA standards) and fuel economy mandates.

- Competitive Product Substitutes: Potential shift towards electric vehicle powertrains impacting demand for internal combustion engine components.

- End-User Demographics: Rising vehicle parc in emerging markets and increasing demand for high-performance vehicles.

- M&A Trends: Strategic acquisitions to expand product portfolios, gain technological advantages, and enhance global reach.

Automotive Tappets Growth Trends & Insights

The automotive tappets market is poised for steady growth, driven by the persistent demand for internal combustion engine (ICE) vehicles globally, even as the automotive industry transitions towards electrification. The parent market, encompassing the broader automotive component industry, continues to provide a stable foundation, while child markets focused on advanced tappet technologies for high-performance and specialized applications are exhibiting accelerated growth. This expansion is underpinned by consistent increases in global vehicle production, particularly in developing economies, where vehicle ownership is rising. Technological advancements in tappet design, such as the development of roller tappets with superior friction reduction capabilities and the incorporation of advanced coatings for enhanced wear resistance, are key growth enablers. Consumer behavior is increasingly influenced by a desire for greater fuel efficiency and reduced running costs, indirectly boosting the demand for components that contribute to these goals. Furthermore, the aftermarket segment, driven by vehicle maintenance and repair needs, represents a significant and stable revenue stream for tappet manufacturers. The overall market size is projected to reach an estimated $10.2 billion by 2025, with a Compound Annual Growth Rate (CAGR) of approximately 3.5% during the forecast period of 2025-2033. This growth trajectory is indicative of a maturing market that continues to benefit from ongoing innovation and sustained demand from both original equipment manufacturers (OEMs) and the aftermarket. Adoption rates for premium tappet technologies, such as those offering reduced friction and enhanced durability, are expected to climb as OEMs prioritize performance and lifecycle cost benefits.

Dominant Regions, Countries, or Segments in Automotive Tappets

Within the global automotive tappets market, Passenger Cars represent the dominant application segment, driving significant demand due to their sheer volume in global vehicle production. This dominance is fueled by several interconnected factors. Economically, the increasing disposable income in emerging economies, coupled with a growing preference for personal mobility, translates directly into higher passenger car sales. Policy-wise, governments worldwide are investing in improving road infrastructure, making personal transportation more accessible and attractive. Furthermore, the continuous evolution of passenger car technology, emphasizing improved fuel efficiency, enhanced performance, and reduced emissions, necessitates the adoption of advanced tappet designs. This includes a higher prevalence of roller tappets that offer better friction reduction compared to traditional flat tappets, contributing to overall engine efficiency. The market share for passenger cars in the tappet segment is estimated to be around 70% of the total market value.

- Dominant Segment: Passenger Cars. This segment accounts for the largest share of the automotive tappets market due to high production volumes and evolving technological demands for efficiency and performance.

- Key Drivers in Passenger Cars:

- Global Vehicle Production Volume: Asia-Pacific, North America, and Europe remain major hubs for passenger car manufacturing.

- Fuel Efficiency Regulations: Mandates pushing for lower emissions and better mileage favor advanced tappet designs.

- Technological Advancements: Integration of roller tappets and advanced materials for improved engine performance and longevity.

- Emerging Market Growth: Rising middle class and increasing demand for personal vehicles in regions like India, China, and Southeast Asia.

- Aftermarket Demand: Replacement and maintenance needs of the vast existing passenger car fleet.

The Asia-Pacific region, particularly China and India, is a leading geographical powerhouse for automotive tappets, mirroring its status as a global automotive manufacturing hub. Its dominance is attributed to a combination of robust economic policies fostering industrial growth, substantial investments in manufacturing capabilities, and a rapidly expanding domestic automotive market. The sheer volume of passenger car and commercial vehicle production in this region directly translates into significant demand for tappets.

- Dominant Region: Asia-Pacific. This region is the largest consumer and producer of automotive tappets due to its massive automotive manufacturing base and growing vehicle parc.

- Key Drivers in Asia-Pacific:

- Manufacturing Hub: Home to a significant number of automotive OEMs and component suppliers.

- Economic Growth & Urbanization: Increasing disposable incomes and a burgeoning middle class driving vehicle ownership.

- Government Initiatives: Support for domestic manufacturing and infrastructure development.

- Cost Competitiveness: Favorable manufacturing costs attracting global players and driving production volume.

- Rapidly Expanding Vehicle Parc: Continuous growth in both passenger and commercial vehicle sales.

Automotive Tappets Product Landscape

The automotive tappets product landscape is characterized by continuous innovation focused on improving engine efficiency, durability, and performance. Key developments include the widespread adoption of roller tappets, which significantly reduce friction compared to traditional flat tappets, leading to better fuel economy and reduced wear. Advanced materials such as hardened steel alloys and specialized coatings like DLC (Diamond-Like Carbon) are being employed to enhance wear resistance and extend the service life of tappets under extreme operating conditions. Furthermore, manufacturers are increasingly focusing on lightweight tappet designs to contribute to overall vehicle weight reduction, further enhancing fuel efficiency.

Key Drivers, Barriers & Challenges in Automotive Tappets

Key Drivers: The automotive tappets market is propelled by several key drivers. The increasing global vehicle parc, especially in emerging economies, directly fuels demand for both original equipment and aftermarket tappets. Stringent emission regulations and the ongoing pursuit of improved fuel efficiency by automotive manufacturers necessitate the use of advanced tappet designs that minimize friction and optimize engine performance. Technological advancements in engine design, leading to higher operating temperatures and pressures, also drive the need for more robust and durable tappet materials and manufacturing processes. The aftermarket sector, driven by vehicle maintenance and repair, provides a consistent and substantial demand stream.

- Growing Global Vehicle Production: Increased output of passenger cars and commercial vehicles.

- Emission Standards & Fuel Economy Mandates: Driving demand for efficient engine components.

- Technological Advancements in Engines: Requirement for more durable and high-performance tappets.

- Aftermarket Demand: Ongoing need for replacement parts in the vast existing vehicle fleet.

Key Challenges & Restraints: Despite positive growth prospects, the automotive tappets industry faces significant challenges. The ongoing shift towards vehicle electrification, particularly in developed markets, poses a long-term threat to the demand for internal combustion engine components like tappets. Fluctuations in raw material prices, such as steel and specialized alloys, can impact manufacturing costs and profitability. Intense competition within the market, with a large number of players, can lead to price pressures and compressed profit margins. Supply chain disruptions, as witnessed globally in recent years, can affect the availability of critical raw materials and components, impacting production schedules. Furthermore, the high capital investment required for advanced manufacturing technologies and precision tooling can be a barrier for smaller players.

- Electrification Trend: Long-term decline in demand for ICE components in some markets.

- Raw Material Price Volatility: Impact on manufacturing costs and profitability.

- Intense Market Competition: Price pressures and margin erosion.

- Supply Chain Disruptions: Affecting raw material availability and production schedules.

- High Capital Investment: For advanced manufacturing and tooling.

Emerging Opportunities in Automotive Tappets

Emerging opportunities in the automotive tappets sector lie in the development and application of tappets for specialized high-performance engines and niche automotive segments that will continue to utilize internal combustion engines for the foreseeable future. Innovations in advanced materials, such as ceramic or composite tappets offering exceptional wear resistance and reduced weight, present significant potential. Furthermore, the growing demand for hybrid powertrains, which still incorporate internal combustion engines, creates a sustained need for efficient tappet technologies. The aftermarket segment in emerging economies, with a rapidly expanding vehicle parc, offers a vast untapped market for tappet manufacturers. Developing customized tappet solutions for specific engine architectures and performance requirements can also unlock new revenue streams.

Growth Accelerators in the Automotive Tappets Industry

Several factors are accelerating growth in the automotive tappets industry. The continued development and adoption of advanced manufacturing techniques, such as precision grinding and surface finishing, are crucial for producing tappets that meet increasingly stringent performance and durability requirements. Strategic partnerships between tappet manufacturers and engine OEMs are vital for co-developing innovative tappet solutions that align with future engine designs and performance targets. Market expansion strategies focused on penetrating high-growth emerging economies, where demand for automotive components is robust, will also serve as significant growth accelerators. Investment in research and development to explore novel materials and designs that can further enhance engine efficiency and reduce emissions will be critical for sustained competitive advantage.

Key Players Shaping the Automotive Tappets Market

- Schaeffler

- Eaton

- Tenneco (Federal-Mogul)

- Rane Engine Valve

- NSK

- SKF

- Otics Corporation

- Riken

- Comp Cams

- SM Motorenteile

- Lunati

- Jinan Worldwide Auto-Accessory

- Yuhuan Huiyu

Notable Milestones in Automotive Tappets Sector

- 2019: Schaeffler introduces advanced lightweight tappet solutions for improved fuel efficiency.

- 2020: Eaton expands its portfolio of roller tappets, catering to the growing demand for performance engines.

- 2021: Tenneco (Federal-Mogul) announces significant investments in R&D for next-generation tappet technologies.

- 2022: Rane Engine Valve strengthens its manufacturing capabilities in India to meet rising regional demand.

- 2023: NSK and SKF collaborate on material innovations for enhanced tappet durability.

- 2024: Otics Corporation focuses on developing tappets with specialized coatings for extreme operating conditions.

- 2024: Riken enhances its production capacity for high-volume passenger car tappets.

In-Depth Automotive Tappets Market Outlook

The automotive tappets market is projected to exhibit a positive growth trajectory, driven by the sustained relevance of internal combustion engines in numerous global markets and the ongoing demand from the aftermarket. While the long-term impact of electrification presents a challenge, the immediate and medium-term outlook remains robust, particularly for advanced tappet technologies that contribute to fuel efficiency and emissions reduction. Strategic opportunities exist in focusing on high-performance engines, hybrid powertrains, and catering to the expanding vehicle parc in emerging economies. Continuous innovation in materials science and manufacturing processes will be crucial for maintaining a competitive edge and capitalizing on future market demands, ensuring a steady market size estimated to reach $13.1 billion by 2033.

Automotive Tappets Segmentation

-

1. Application

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

-

2. Types

- 2.1. Flat Tappet

- 2.2. Roller Tappet

Automotive Tappets Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Tappets Regional Market Share

Geographic Coverage of Automotive Tappets

Automotive Tappets REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Flat Tappet

- 5.2.2. Roller Tappet

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Automotive Tappets Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Cars

- 6.1.2. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Flat Tappet

- 6.2.2. Roller Tappet

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Automotive Tappets Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Cars

- 7.1.2. Commercial Vehicles

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Flat Tappet

- 7.2.2. Roller Tappet

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Automotive Tappets Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Cars

- 8.1.2. Commercial Vehicles

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Flat Tappet

- 8.2.2. Roller Tappet

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Automotive Tappets Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Cars

- 9.1.2. Commercial Vehicles

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Flat Tappet

- 9.2.2. Roller Tappet

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Automotive Tappets Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Cars

- 10.1.2. Commercial Vehicles

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Flat Tappet

- 10.2.2. Roller Tappet

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Automotive Tappets Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Passenger Cars

- 11.1.2. Commercial Vehicles

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Flat Tappet

- 11.2.2. Roller Tappet

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Schaeffler

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Eaton

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Tenneco(Federal-Mogul)

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Rane Engine Valve

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 NSK

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 SKF

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Otics Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Riken

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Comp Cams

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 SM Motorenteile

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Lunati

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Jinan Worldwide Auto-Accessory

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Yuhuan Huiyu

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 Schaeffler

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Automotive Tappets Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Automotive Tappets Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Automotive Tappets Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Tappets Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Automotive Tappets Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive Tappets Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Automotive Tappets Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Tappets Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Automotive Tappets Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Tappets Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Automotive Tappets Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive Tappets Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Automotive Tappets Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Tappets Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Automotive Tappets Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Tappets Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Automotive Tappets Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive Tappets Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Automotive Tappets Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Tappets Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Tappets Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Tappets Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive Tappets Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive Tappets Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Tappets Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Tappets Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Tappets Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Tappets Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive Tappets Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive Tappets Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Tappets Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Tappets Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Tappets Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Automotive Tappets Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Tappets Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Tappets Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Automotive Tappets Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Tappets Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Tappets Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Automotive Tappets Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Tappets Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Tappets Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Automotive Tappets Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Tappets Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Tappets Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Automotive Tappets Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Tappets Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Tappets Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Automotive Tappets Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Tappets Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Tappets?

The projected CAGR is approximately 4%.

2. Which companies are prominent players in the Automotive Tappets?

Key companies in the market include Schaeffler, Eaton, Tenneco(Federal-Mogul), Rane Engine Valve, NSK, SKF, Otics Corporation, Riken, Comp Cams, SM Motorenteile, Lunati, Jinan Worldwide Auto-Accessory, Yuhuan Huiyu.

3. What are the main segments of the Automotive Tappets?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Tappets," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Tappets report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Tappets?

To stay informed about further developments, trends, and reports in the Automotive Tappets, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence