Key Insights

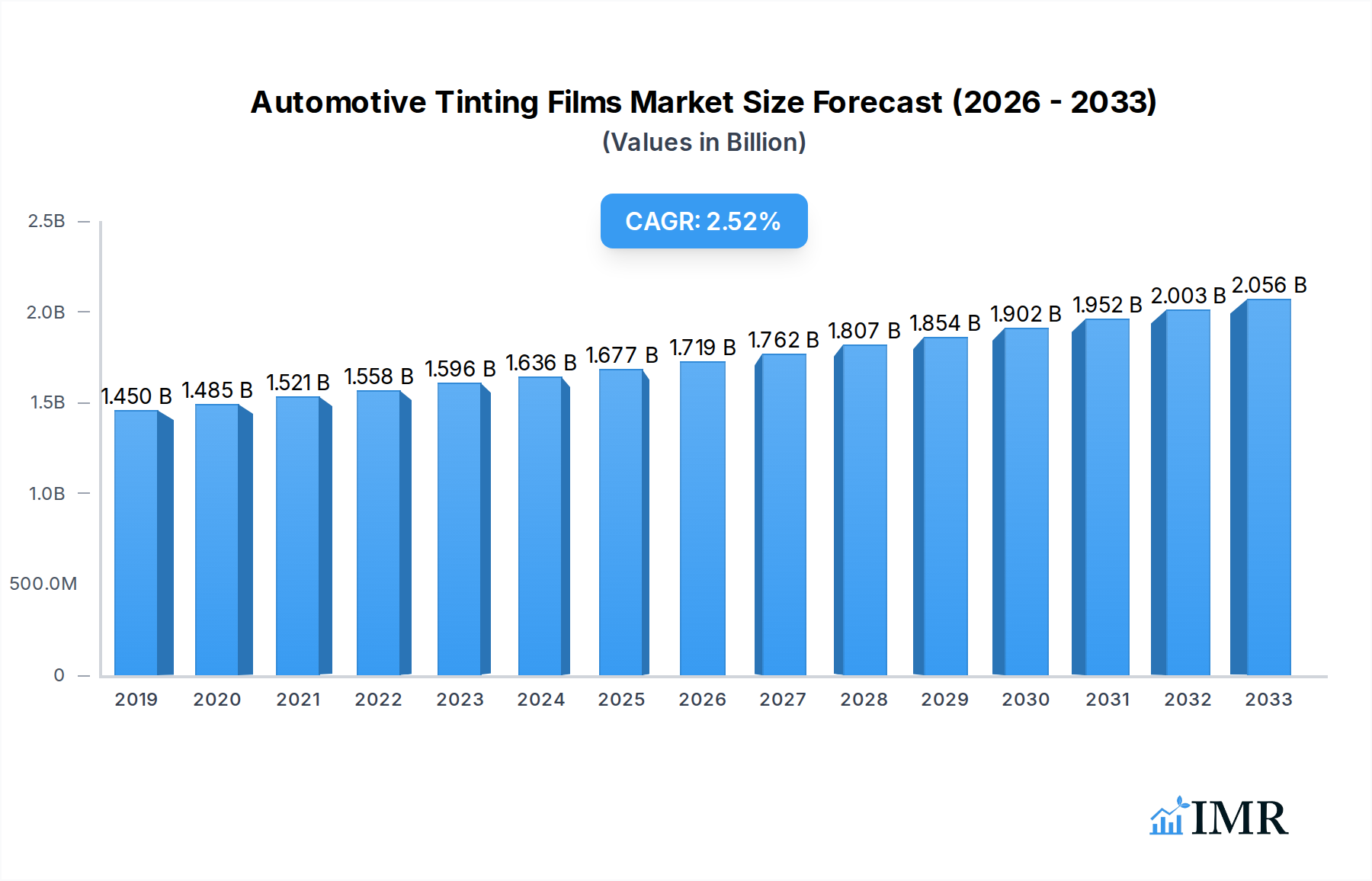

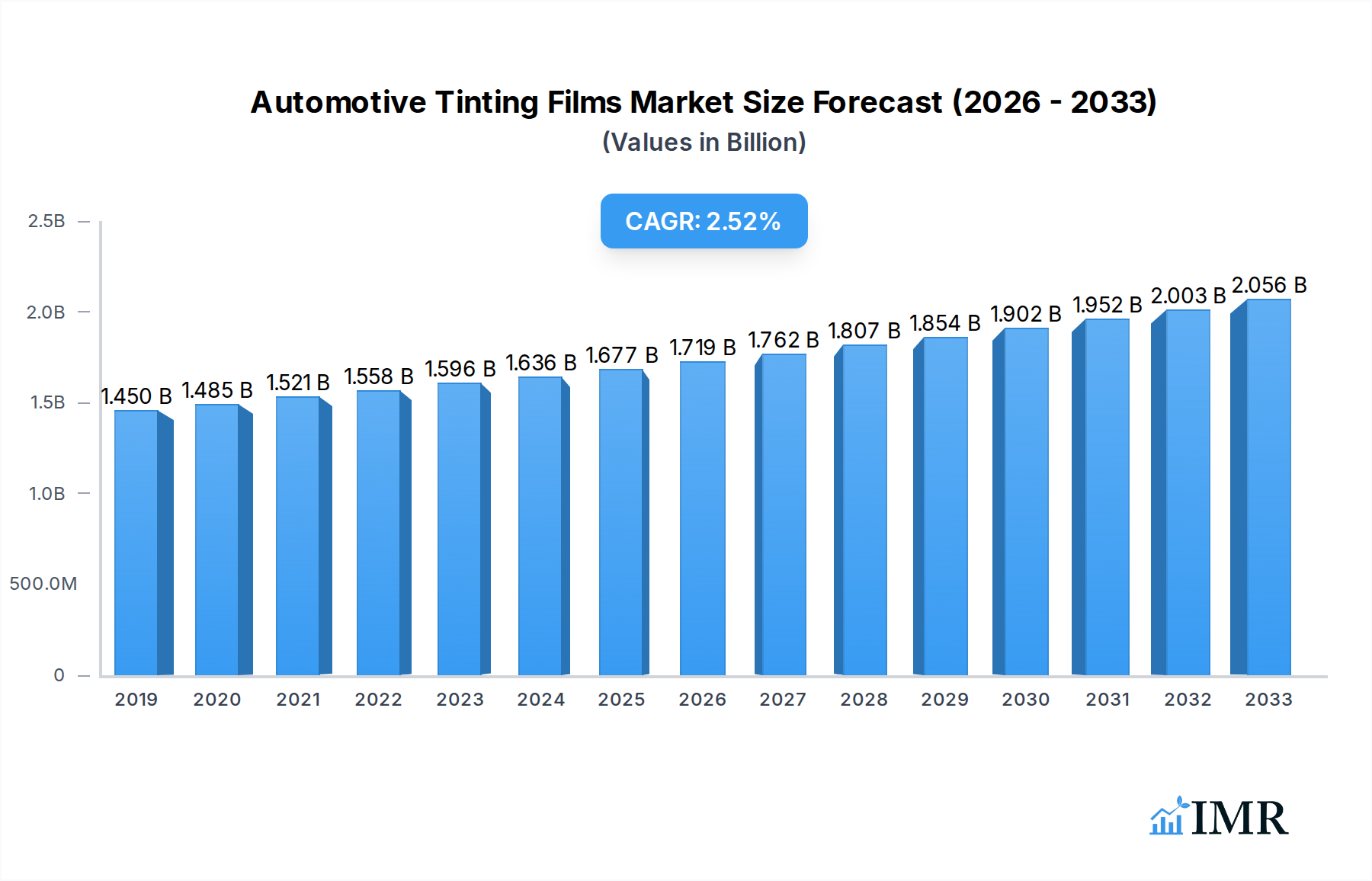

The global automotive tinting films market is poised for steady growth, projected to reach $1450.1 million in 2019 and expand at a CAGR of 3.8% throughout the forecast period of 2025-2033. This growth is propelled by a confluence of factors, primarily driven by increasing consumer demand for enhanced vehicle aesthetics, UV protection, and improved passenger comfort. As vehicle ownership continues to rise globally, so does the adoption of aftermarket accessories like tinting films. Furthermore, stringent automotive safety regulations and the growing awareness of the detrimental effects of UV radiation are further bolstering market expansion. The market's trajectory also benefits from advancements in film technology, leading to more durable, energy-efficient, and visually appealing products. Regions like Europe, with a strong automotive manufacturing base and a discerning consumer market, are expected to play a significant role in this growth.

Automotive Tinting Films Market Size (In Billion)

The automotive tinting films market is characterized by a competitive landscape featuring a broad spectrum of established players and emerging innovators. Key trends shaping the industry include the development of advanced nano-ceramic and carbon-based films, offering superior heat rejection and signal clarity. The increasing focus on sustainability and eco-friendly manufacturing processes is also a notable trend. However, the market faces certain restraints, including fluctuating raw material prices and the potential for regulatory changes concerning tint levels in different regions. Despite these challenges, the persistent demand for personalized and functional vehicle upgrades, coupled with ongoing innovation in product offerings, ensures a robust outlook for the automotive tinting films market. The market's segmentation across various applications, such as passenger cars, commercial vehicles, and SUVs, along with diverse product types, caters to a wide array of consumer needs and preferences.

Automotive Tinting Films Company Market Share

This in-depth report provides a panoramic view of the global automotive tinting films market, encompassing a detailed analysis of its structure, growth trajectory, regional dominance, product innovations, key drivers, emerging opportunities, and the pivotal companies shaping its future. Covering the historical period from 2019–2024, the base year of 2025, and a robust forecast period extending to 2033, this report leverages the latest industry data and expert insights to deliver actionable intelligence for stakeholders.

Automotive Tinting Films Market Dynamics & Structure

The global automotive tinting films market is characterized by a moderately fragmented structure, with a mix of established multinational corporations and a significant number of regional and specialized players. Key companies like Llumar, Solar Gard, SunTek, 3M, and Saint-Gobain Solar Gard hold substantial market shares, driven by their extensive product portfolios, robust distribution networks, and consistent innovation. The market concentration is influenced by technological advancements, particularly in material science and manufacturing processes, which act as significant drivers for innovation. Regulatory frameworks, varying by region, also play a crucial role in shaping market access and product development, with stringent safety and performance standards in some territories. Competitive product substitutes, such as aftermarket coatings and advanced automotive glass technologies, present a challenge, though tinting films continue to offer a compelling balance of aesthetics, performance, and cost-effectiveness. End-user demographics are evolving, with a growing demand from younger demographics for aesthetic customization and from a broader consumer base for enhanced comfort, UV protection, and energy efficiency in vehicles. Mergers and acquisitions (M&A) trends are notable, with larger entities acquiring smaller, innovative companies to expand their market reach and technological capabilities. For instance, recent years have seen an estimated 5-8 significant M&A deals annually within the broader window film industry, indicating a consolidation drive. Innovation barriers, such as the high cost of R&D for advanced materials and the lengthy product development cycles, are present, but offset by the continuous pursuit of enhanced performance metrics like heat rejection, durability, and glare reduction.

- Market Concentration: Moderately fragmented with a presence of both global leaders and niche players.

- Technological Innovation Drivers: Advancements in nano-technology, polymer science, and manufacturing efficiencies.

- Regulatory Frameworks: Influencing product standards, safety regulations, and market entry barriers across different regions.

- Competitive Product Substitutes: Advanced automotive glass, ceramic coatings, and aftermarket paint protection films.

- End-User Demographics: Increasing demand from millennials for customization, and a broad appeal for comfort, safety, and energy savings.

- M&A Trends: Ongoing consolidation through strategic acquisitions to gain market share and technology.

- Innovation Barriers: High R&D costs for next-generation films, and lengthy approval processes.

Automotive Tinting Films Growth Trends & Insights

The global automotive tinting films market is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 6.5% from 2025 to 2033. This growth is underpinned by a confluence of factors including increasing automotive production globally, a rising awareness among consumers regarding the benefits of vehicle window films, and continuous technological advancements leading to superior product offerings. The market size, estimated at over USD 4,500 million in the base year 2025, is expected to reach over USD 7,500 million by 2033. Adoption rates for automotive tinting films are steadily increasing across both developed and emerging economies, driven by both aesthetic preferences and functional advantages. Consumers are increasingly recognizing the value proposition of tinting films in enhancing vehicle comfort by reducing interior heat buildup, protecting occupants from harmful UV radiation, and improving fuel efficiency through reduced air conditioning load. Technological disruptions are playing a pivotal role, with the development of advanced nano-ceramic films offering superior heat rejection without compromising signal transmission, and hybrid films combining the benefits of different technologies. Consumer behavior shifts are also evident, with a growing preference for premium films that offer enhanced durability, scratch resistance, and sophisticated aesthetics. The aftermarket segment continues to dominate, accounting for approximately 80% of the total market revenue, though original equipment manufacturer (OEM) installations are projected to witness a higher growth rate as automotive manufacturers integrate these films as standard features. The rising disposable incomes in emerging markets, coupled with a burgeoning middle class that aspires to own and customize vehicles, will further fuel market penetration. The demand for specialized films, such as those offering privacy, security, and aesthetic customization, is also on an upward trajectory, contributing to the overall market expansion.

Dominant Regions, Countries, or Segments in Automotive Tinting Films

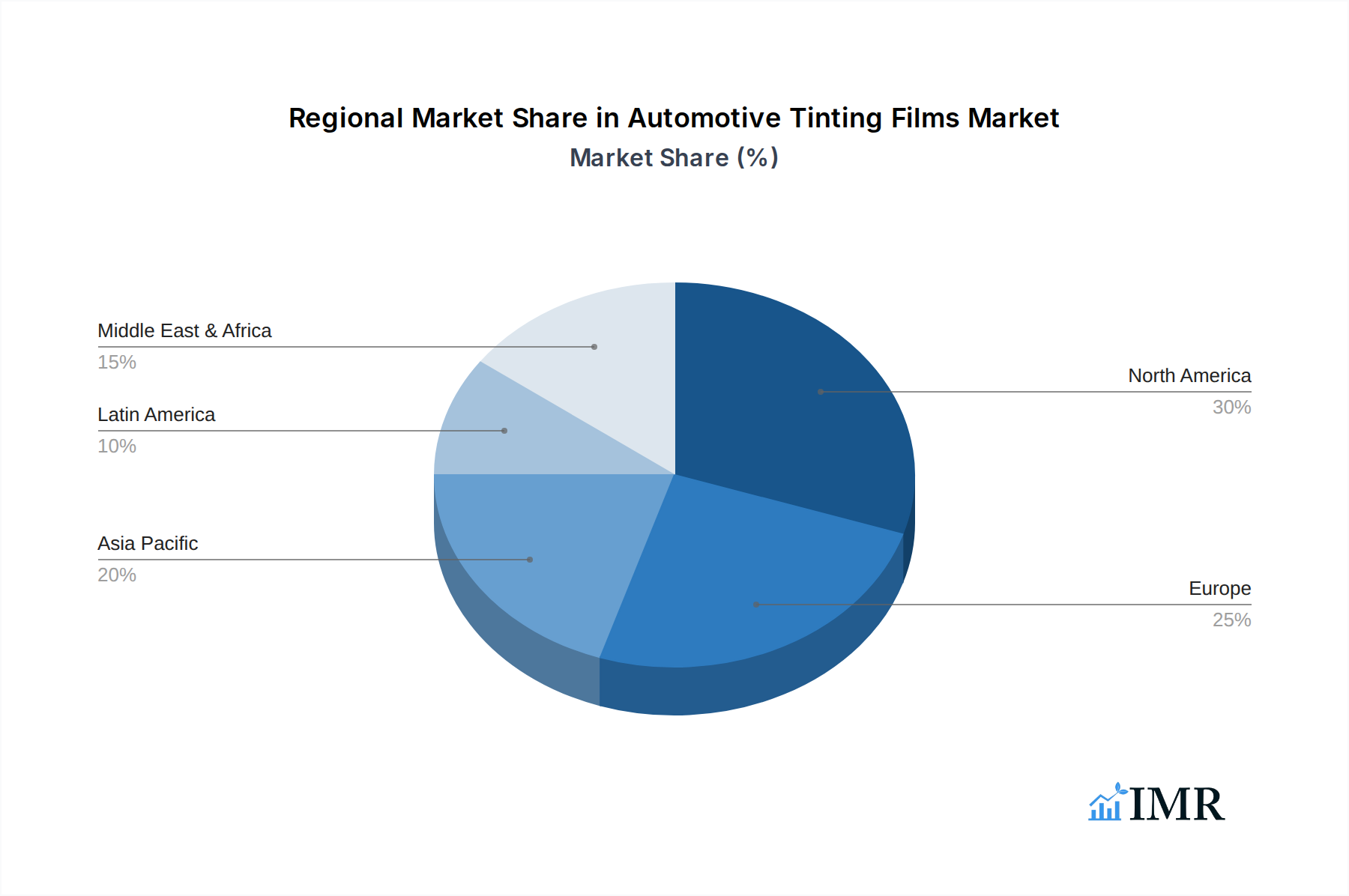

The Asia-Pacific region stands out as the dominant force in the global automotive tinting films market, driven by its colossal automotive manufacturing base and rapidly expanding consumer market. Countries like China, India, and South Korea are at the forefront, contributing significantly to both production and consumption. The sheer volume of new vehicle sales in these nations, coupled with a growing middle class with increasing disposable incomes and a desire for vehicle customization and comfort, fuels the demand for automotive tinting films. Economic policies that favor automotive manufacturing and consumer spending, coupled with substantial investments in infrastructure, further bolster the market's growth in this region.

Within the Application segment, the aftermarket application continues to hold the lion's share, estimated at approximately 80% of the total market revenue. This dominance is attributed to the vast number of existing vehicles on the road that can be retrofitted with tinting films to enhance their features and aesthetics. However, the OEM (Original Equipment Manufacturer) segment is exhibiting a higher growth rate, projected at a CAGR of around 7.2%, as more automotive manufacturers integrate tinting films as a factory-installed option, recognizing their consumer appeal and functional benefits.

In terms of Types, dyed films have historically held a significant market share due to their affordability and basic aesthetic appeal. However, the market is witnessing a pronounced shift towards nano-ceramic films and hybrid films. Nano-ceramic films, in particular, are experiencing robust growth, estimated at a CAGR of approximately 8%, owing to their superior performance in heat rejection, UV protection, and signal permeability without compromising clarity. Hybrid films, which combine the benefits of various technologies, are also gaining traction, offering a balance of performance and cost-effectiveness.

Dominant Region: Asia-Pacific, driven by China, India, and South Korea.

- Key Drivers: High automotive production, increasing disposable incomes, consumer aspiration for vehicle customization, supportive economic policies.

- Market Share: Estimated to hold over 35% of the global market revenue.

- Growth Potential: Continued expansion fueled by urbanization and a growing automotive fleet.

Dominant Application Segment: Aftermarket.

- Market Share: Approximately 80% of the total market.

- Growth Drivers: Large existing vehicle parc, ease of retrofitting, consumer desire for upgrades.

- Growth Potential: Steady growth, but with a slower CAGR compared to OEM.

Emerging Dominant Type: Nano-ceramic films.

- Growth Rate: Projected CAGR of around 8%.

- Performance Advantages: Superior heat rejection, UV blockage, signal clarity.

- Consumer Preference: Growing demand for high-performance, non-metallized options.

Automotive Tinting Films Product Landscape

The automotive tinting films product landscape is characterized by continuous innovation focused on enhancing performance, durability, and user experience. Advanced materials and manufacturing techniques are yielding films with superior heat rejection capabilities, blocking up to 90% of solar infrared radiation, and providing excellent UV protection, safeguarding interiors and occupants from harmful rays. Innovations in nano-ceramic technology have led to films that are non-metallized, preventing signal interference with electronic devices like GPS and mobile phones, a significant unique selling proposition. Furthermore, advancements in scratch-resistant coatings and adhesive technologies ensure longevity and ease of application, reducing installation time and enhancing the final aesthetic. The development of privacy films, security films offering enhanced shatter resistance, and decorative films catering to aesthetic customization further diversifies the product offerings.

Key Drivers, Barriers & Challenges in Automotive Tinting Films

Key Drivers:

- Enhanced Comfort and Energy Efficiency: Films significantly reduce interior cabin temperatures, leading to lower air conditioning usage and improved fuel economy.

- UV Protection: Crucial for protecting vehicle occupants and interior materials from harmful ultraviolet radiation, preventing fading and degradation.

- Aesthetic Customization: Provides vehicle owners with options for enhancing the appearance and privacy of their vehicles.

- Technological Advancements: Development of nano-ceramic and hybrid films with superior performance characteristics.

- Growing Automotive Production: Increased vehicle sales globally directly translate to a larger market for tinting films.

Barriers & Challenges:

- Regulatory Hurdles: Varying tinting regulations across different regions can limit product adoption and market access. For instance, some regions have strict limitations on the darkness of window tinting.

- Counterfeit Products: The presence of low-quality counterfeit films can damage brand reputation and consumer trust.

- Skilled Labor Shortage: The need for professional and skilled installers can be a bottleneck for market growth in certain areas.

- Material Costs: Fluctuations in the cost of raw materials like PET and specialized polymers can impact manufacturing costs and profitability.

- Competition from Advanced Glass: Increasing adoption of factory-tinted or privacy glass in new vehicles presents a competitive challenge.

Emerging Opportunities in Automotive Tinting Films

Emerging opportunities in the automotive tinting films sector lie in the development of smart films with dynamic tinting capabilities, responding to light conditions or user preferences. The increasing demand for electric vehicles (EVs) presents a unique opportunity, as EVs can benefit significantly from advanced thermal management films to optimize battery performance and cabin comfort, thereby extending range. Furthermore, the integration of antimicrobial or self-cleaning properties into tinting films could cater to evolving consumer preferences for hygiene and low-maintenance solutions. Untapped markets in developing economies, coupled with a growing awareness of the benefits of automotive window films, offer substantial growth potential. The expansion of tinting services into adjacent sectors, such as commercial vehicle fleets and recreational vehicles, also represents a promising avenue for market diversification.

Growth Accelerators in the Automotive Tinting Films Industry

Several catalysts are accelerating the growth of the automotive tinting films industry. Technological breakthroughs in material science, particularly in the development of advanced polymers and nano-coatings, are continuously enhancing film performance, driving demand for premium products. Strategic partnerships between film manufacturers and automotive OEMs are crucial for integrating these films at the production stage, thereby increasing market penetration. Furthermore, aggressive marketing and educational campaigns aimed at highlighting the multifaceted benefits of automotive tinting films are vital in driving consumer awareness and adoption. The increasing focus on sustainability within the automotive sector also presents an opportunity for tinting films that contribute to energy efficiency and reduced carbon footprints.

Key Players Shaping the Automotive Tinting Films Market

- Llumar

- Solar Gard

- SunTek

- Global Window Films

- Madico

- Johnson Window Films

- Hüper Optik

- 3M

- Armolan

- Hexis

- Garware Suncontrol

- ASWF (American Standard Window Film)

- Aegis Films

- Saint-Gobain Solar Gard

- Avery Dennison

- Filtra Automotive

- Hanita Coatings

- Klingshield

- Suntrol

- V-KOOL

- Sun-X

- Gila

- Express Window Films

- Solamatrix

- Opalux Window Films

- SolarScreen

- Tintfit Window Films

- Contra Vision

- Apex Window Films

- Bekaert Specialty Films

- Reflectiv Window Films

- Brume Ltd

- Purlfrost Window Film

Notable Milestones in Automotive Tinting Films Sector

- 2019: Introduction of next-generation nano-ceramic films offering enhanced infrared rejection and signal clarity.

- 2020: Increased focus on sustainable manufacturing practices and the development of eco-friendly tinting solutions.

- 2021: Significant surge in demand for privacy and security-enhancing window films due to global events.

- 2022: Major players invest heavily in R&D for films with self-healing and antimicrobial properties.

- 2023: Growing adoption of heat-rejecting films in electric vehicles to optimize battery performance and range.

- 2024: Expansion of tinting services into commercial fleet management and a rise in DIY film kits.

In-Depth Automotive Tinting Films Market Outlook

The future outlook for the automotive tinting films market is exceptionally positive, driven by sustained demand for enhanced vehicle comfort, protection, and aesthetics. Growth accelerators such as ongoing technological innovation, particularly in the realm of smart and sustainable films, will continue to propel the industry forward. Strategic collaborations between film manufacturers and automotive giants will further integrate these films as standard features, expanding their reach. The increasing global automotive production, coupled with the rising disposable incomes in emerging economies, presents a vast untapped market potential. Opportunities in specialized applications, like those tailored for electric vehicles and advanced driver-assistance systems (ADAS) integration, will shape future product development. The market is expected to witness continued growth at a healthy CAGR, solidifying its position as an indispensable component of the modern automotive experience.

Automotive Tinting Films Segmentation

- 1. Application

- 2. Types

Automotive Tinting Films Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Automotive Tinting Films Regional Market Share

Geographic Coverage of Automotive Tinting Films

Automotive Tinting Films REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 6. Automotive Tinting Films Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.2. Market Analysis, Insights and Forecast - by Types

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Llumar

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Solar Gard

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 SunTek

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Global Window Films

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Madico

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Johnson Window Films

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Hüper Optik

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 3M

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Armolan

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Hexis

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Garware Suncontrol

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 ASWF (American Standard Window Film)

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Aegis Films

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Saint-Gobain Solar Gard

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Avery Dennison

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 Filtra Automotive

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.17 Hanita Coatings

- 7.1.17.1. Company Overview

- 7.1.17.2. Products

- 7.1.17.3. Company Financials

- 7.1.17.4. SWOT Analysis

- 7.1.18 Klingshield

- 7.1.18.1. Company Overview

- 7.1.18.2. Products

- 7.1.18.3. Company Financials

- 7.1.18.4. SWOT Analysis

- 7.1.19 Suntrol

- 7.1.19.1. Company Overview

- 7.1.19.2. Products

- 7.1.19.3. Company Financials

- 7.1.19.4. SWOT Analysis

- 7.1.20 V-KOOL

- 7.1.20.1. Company Overview

- 7.1.20.2. Products

- 7.1.20.3. Company Financials

- 7.1.20.4. SWOT Analysis

- 7.1.21 Sun-X

- 7.1.21.1. Company Overview

- 7.1.21.2. Products

- 7.1.21.3. Company Financials

- 7.1.21.4. SWOT Analysis

- 7.1.22 Gila

- 7.1.22.1. Company Overview

- 7.1.22.2. Products

- 7.1.22.3. Company Financials

- 7.1.22.4. SWOT Analysis

- 7.1.23 Express Window Films

- 7.1.23.1. Company Overview

- 7.1.23.2. Products

- 7.1.23.3. Company Financials

- 7.1.23.4. SWOT Analysis

- 7.1.24 Solamatrix

- 7.1.24.1. Company Overview

- 7.1.24.2. Products

- 7.1.24.3. Company Financials

- 7.1.24.4. SWOT Analysis

- 7.1.25 Opalux Window Films

- 7.1.25.1. Company Overview

- 7.1.25.2. Products

- 7.1.25.3. Company Financials

- 7.1.25.4. SWOT Analysis

- 7.1.26 SolarScreen

- 7.1.26.1. Company Overview

- 7.1.26.2. Products

- 7.1.26.3. Company Financials

- 7.1.26.4. SWOT Analysis

- 7.1.27 Tintfit Window Films

- 7.1.27.1. Company Overview

- 7.1.27.2. Products

- 7.1.27.3. Company Financials

- 7.1.27.4. SWOT Analysis

- 7.1.28 Contra Vision

- 7.1.28.1. Company Overview

- 7.1.28.2. Products

- 7.1.28.3. Company Financials

- 7.1.28.4. SWOT Analysis

- 7.1.29 Apex Window Films

- 7.1.29.1. Company Overview

- 7.1.29.2. Products

- 7.1.29.3. Company Financials

- 7.1.29.4. SWOT Analysis

- 7.1.30 Bekaert Specialty Films

- 7.1.30.1. Company Overview

- 7.1.30.2. Products

- 7.1.30.3. Company Financials

- 7.1.30.4. SWOT Analysis

- 7.1.31 Reflectiv Window Films

- 7.1.31.1. Company Overview

- 7.1.31.2. Products

- 7.1.31.3. Company Financials

- 7.1.31.4. SWOT Analysis

- 7.1.32 Brume Ltd

- 7.1.32.1. Company Overview

- 7.1.32.2. Products

- 7.1.32.3. Company Financials

- 7.1.32.4. SWOT Analysis

- 7.1.33 Purlfrost Window Film

- 7.1.33.1. Company Overview

- 7.1.33.2. Products

- 7.1.33.3. Company Financials

- 7.1.33.4. SWOT Analysis

- 7.1.1 Llumar

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Automotive Tinting Films Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: Automotive Tinting Films Share (%) by Company 2025

List of Tables

- Table 1: Automotive Tinting Films Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Automotive Tinting Films Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Automotive Tinting Films Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Automotive Tinting Films Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Automotive Tinting Films Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Automotive Tinting Films Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United Kingdom Automotive Tinting Films Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Germany Automotive Tinting Films Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: France Automotive Tinting Films Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Italy Automotive Tinting Films Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 11: Spain Automotive Tinting Films Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 12: Netherlands Automotive Tinting Films Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 13: Belgium Automotive Tinting Films Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Sweden Automotive Tinting Films Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Norway Automotive Tinting Films Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Poland Automotive Tinting Films Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 17: Denmark Automotive Tinting Films Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Tinting Films?

The projected CAGR is approximately 3.8%.

2. Which companies are prominent players in the Automotive Tinting Films?

Key companies in the market include Llumar, Solar Gard, SunTek, Global Window Films, Madico, Johnson Window Films, Hüper Optik, 3M, Armolan, Hexis, Garware Suncontrol, ASWF (American Standard Window Film), Aegis Films, Saint-Gobain Solar Gard, Avery Dennison, Filtra Automotive, Hanita Coatings, Klingshield, Suntrol, V-KOOL, Sun-X, Gila, Express Window Films, Solamatrix, Opalux Window Films, SolarScreen, Tintfit Window Films, Contra Vision, Apex Window Films, Bekaert Specialty Films, Reflectiv Window Films, Brume Ltd, Purlfrost Window Film.

3. What are the main segments of the Automotive Tinting Films?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3900.00, USD 5850.00, and USD 7800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Tinting Films," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Tinting Films report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Tinting Films?

To stay informed about further developments, trends, and reports in the Automotive Tinting Films, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence