Key Insights

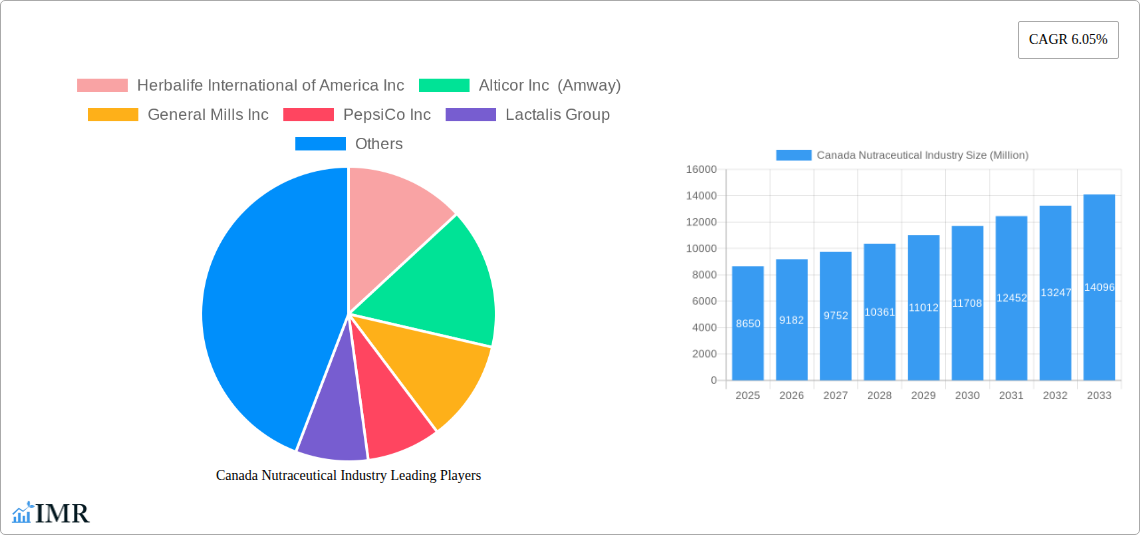

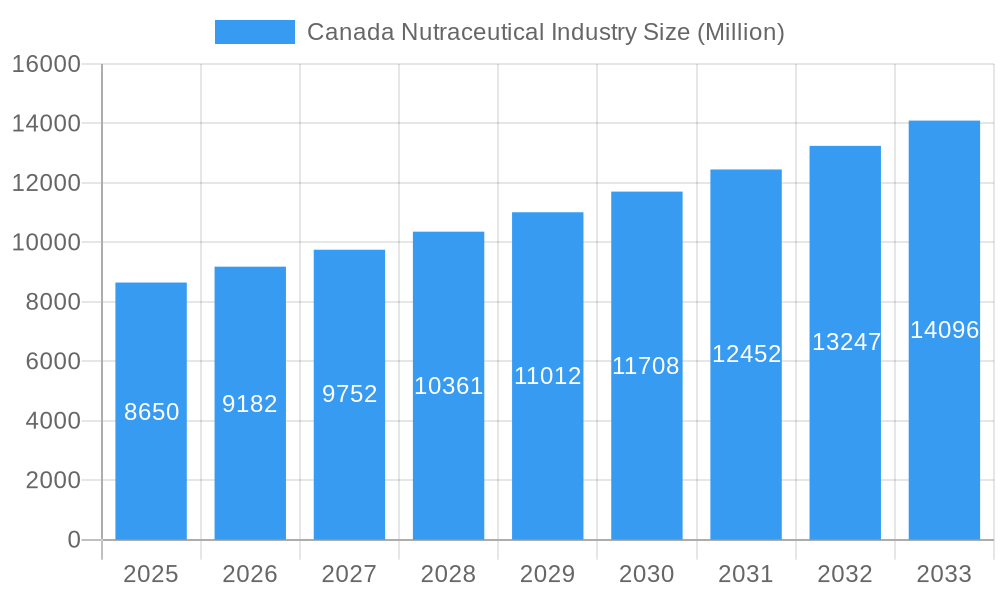

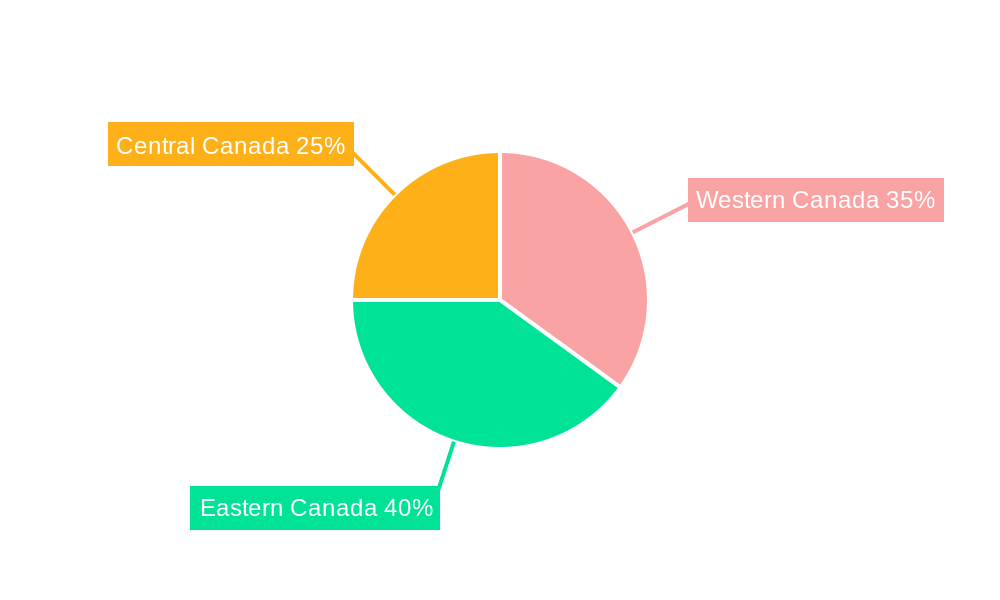

The Canadian nutraceutical market, valued at $8.65 billion in 2025, exhibits robust growth potential, projected to expand at a Compound Annual Growth Rate (CAGR) of 6.05% from 2025 to 2033. This growth is driven by several key factors. Increasing health consciousness among Canadians, coupled with rising disposable incomes, fuels demand for products promoting wellness and disease prevention. The aging population also contributes significantly, as older adults are more likely to utilize nutraceuticals for maintaining health and managing age-related conditions. Furthermore, the increasing prevalence of chronic diseases like cardiovascular disease and diabetes is driving the adoption of nutraceuticals as complementary therapies. The market segmentation reveals strong performance across various distribution channels, with online retail witnessing particularly rapid expansion. Functional foods and beverages, including dietary supplements, dominate the product landscape, reflecting a preference for incorporating health benefits into daily routines. Key players like Herbalife, Amway, and Nestlé leverage their brand recognition and established distribution networks to capture market share. Regional variations exist, with Western Canada potentially exhibiting faster growth due to higher per capita income and health consciousness. However, the Eastern and Central regions present substantial opportunities given their larger populations.

Canada Nutraceutical Industry Market Size (In Billion)

The Canadian nutraceutical industry is strategically positioned for continued success. Government initiatives promoting healthy lifestyles and preventative healthcare further enhance market prospects. However, regulatory complexities and the need for stringent quality control measures represent potential challenges. The industry's future growth hinges on innovation, with an increasing focus on personalized nutrition and the development of scientifically-backed products. Furthermore, effective marketing strategies that emphasize product efficacy and safety will be crucial in maintaining consumer confidence and driving sustained expansion. Competitive pricing strategies and the expansion of distribution networks into underserved areas will also contribute to market growth. Finally, addressing consumer concerns regarding product authenticity and transparency will be paramount in fostering trust and maintaining the industry's reputation for high-quality products.

Canada Nutraceutical Industry Company Market Share

Canada Nutraceutical Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Canadian nutraceutical industry, offering invaluable insights for industry professionals, investors, and strategic planners. Covering the period 2019-2033, with a base year of 2025, this report unveils the market dynamics, growth trends, and future potential of this rapidly evolving sector. The report leverages robust data and market intelligence to offer a clear and concise view of the Canadian nutraceutical landscape.

Canada Nutraceutical Industry Market Dynamics & Structure

The Canadian nutraceutical market is a dynamic landscape shaped by several key factors. Market concentration is moderate, with several large multinational corporations alongside smaller, specialized players. Technological innovation, particularly in product formulation and delivery systems (e.g., targeted delivery systems, personalized nutrition), is a significant driver. Stringent regulatory frameworks, overseen by Health Canada, influence product development and marketing claims. Competition from substitute products, such as conventional foods fortified with nutrients, poses a challenge. The end-user demographics are shifting, with growing demand from aging populations and health-conscious consumers. Mergers and acquisitions (M&A) activity is relatively frequent, reflecting industry consolidation and expansion strategies. The market size in 2024 was estimated at xx Million, and is predicted to reach xx Million by 2033.

- Market Concentration: Moderate, with a mix of large and small players.

- Technological Innovation: Driving development of functional foods and beverages with enhanced efficacy and delivery.

- Regulatory Framework: Health Canada's regulations impact product development and marketing.

- Competitive Substitutes: Fortified foods and conventional medicine present competition.

- End-User Demographics: Aging population and health-conscious consumers fuel demand.

- M&A Activity: Moderate to high, with strategic acquisitions driving market consolidation.

Canada Nutraceutical Industry Growth Trends & Insights

The Canadian nutraceutical market exhibits robust growth, fueled by several key trends. Market size has expanded significantly over the historical period (2019-2024), driven by increasing health awareness, rising disposable incomes, and the growing popularity of functional foods and dietary supplements. Adoption rates for specific product categories, such as probiotics and omega-3 supplements, are steadily increasing. Technological disruptions, including personalized nutrition and precision medicine, are reshaping the market, while consumer behavior shifts towards proactive health management and preventative care contribute to continued growth. The Compound Annual Growth Rate (CAGR) for the forecast period (2025-2033) is projected to be xx%, reflecting continued market expansion. Market penetration for key product categories is expected to increase by xx% by 2033.

Dominant Regions, Countries, or Segments in Canada Nutraceutical Industry

Within the Canadian nutraceutical market, several segments and distribution channels are leading growth.

Distribution Channels: Supermarkets/Hypermarkets hold the largest market share, owing to their wide reach and established distribution networks. Drug stores/pharmacies also represent a significant channel, leveraging their professional expertise in health and wellness. Online retail stores are experiencing rapid growth, reflecting increasing consumer preference for e-commerce.

Product Type: Functional foods constitute the largest market segment, followed by dietary supplements. Within functional foods, functional beverages are a rapidly growing sub-segment.

- Supermarkets/Hypermarkets: Wide reach, established distribution, driving high market share.

- Drug Stores/Pharmacies: Leverage professional expertise in health and wellness.

- Online Retail Stores: Rapid growth reflecting e-commerce adoption.

- Functional Foods: Largest market segment, driven by convenience and perceived health benefits.

- Dietary Supplements: Significant segment with growing demand for specialized products.

- Functional Beverages: Rapidly expanding sub-segment within functional foods.

Canada Nutraceutical Industry Product Landscape

The Canadian nutraceutical market showcases diverse product innovations, reflecting ongoing efforts to improve product efficacy, safety, and consumer appeal. Recent product launches include novel delivery systems, targeted formulations, and functional foods with enhanced nutrient profiles. Key product innovations are driven by technological advancements in areas such as encapsulation, microencapsulation, and targeted delivery systems. These innovations contribute to improved bioavailability and targeted health outcomes, enhancing the overall value proposition for consumers.

Key Drivers, Barriers & Challenges in Canada Nutraceutical Industry

Key Drivers:

- Increasing health awareness among Canadians

- Rising disposable incomes allowing higher spending on health and wellness

- Government initiatives promoting healthy lifestyles

- Technological advancements leading to more efficient and targeted products

Key Challenges:

- Stringent regulatory environment (Health Canada approval process) affecting speed to market

- Competition from substitute products such as fortified foods

- Maintaining supply chain stability and resilience given fluctuating raw material costs and global events. This leads to a predicted 5% reduction in market growth in 2027.

Emerging Opportunities in Canada Nutraceutical Industry

- Growing demand for personalized nutrition solutions

- Expansion into niche markets, such as sports nutrition and specialized dietary needs

- Increasing interest in plant-based and sustainably sourced ingredients

- Opportunities to develop innovative product formats (e.g., functional snacks) to enhance consumer acceptance.

Growth Accelerators in the Canada Nutraceutical Industry Industry

Strategic partnerships between nutraceutical companies and healthcare providers are emerging as a significant growth catalyst. These collaborations facilitate product development, market access, and consumer engagement. Technological breakthroughs in areas such as personalized nutrition and precision medicine will unlock significant opportunities for market expansion. Furthermore, expanding into underserved market segments and exploring new product applications, driven by evolving consumer preferences and unmet health needs, will fuel future growth.

Key Players Shaping the Canada Nutraceutical Industry Market

Notable Milestones in Canada Nutraceutical Industry Sector

- October 2022: Nestlé and Nature's Bounty launch VitaBeans, entering the Canadian vitamins and supplements market.

- June 2022: Kellogg Company announces a split into three companies, impacting its presence in the Canadian cereal and snack market.

- September 2021: Lactalis Canada introduces Astro PROTEIN & FIBRE Yogurt, expanding its offerings in the functional food category.

In-Depth Canada Nutraceutical Industry Market Outlook

The Canadian nutraceutical market is poised for sustained growth, driven by strong underlying trends and emerging opportunities. Continued innovation in product development, expanding distribution channels, and strategic collaborations will drive market expansion. The focus on personalized nutrition and preventative health will further accelerate market growth, presenting significant opportunities for established and emerging players alike. The market's future potential is considerable, with significant opportunities for both domestic and international companies.

Canada Nutraceutical Industry Segmentation

-

1. Type

-

1.1. Functional Food

- 1.1.1. Functional Cereal

- 1.1.2. Functional Bakery & Confectionary

- 1.1.3. Functional Dairy

- 1.1.4. Functional Snacks

- 1.1.5. Other Functional Foods

-

1.2. Functional Beverage

- 1.2.1. Energy Drink

- 1.2.2. Sports Drink

- 1.2.3. Fortified Juice

- 1.2.4. Dairy and Dairy Alternative Beverage

- 1.2.5. Other Functional Beverages

-

1.3. Dietary Supplement

- 1.3.1. Vitamin

- 1.3.2. Mineral

- 1.3.3. Botanical

- 1.3.4. Enzyme

- 1.3.5. Fatty Acid

- 1.3.6. Protein

- 1.3.7. Other Dietary Supplements

-

1.1. Functional Food

-

2. Distribution Channel

- 2.1. Specialty Stores

- 2.2. Supermarkets/Hypermarkets

- 2.3. Convenience Stores

- 2.4. Drug Stores/Pharmacies

- 2.5. Online Retail Stores

- 2.6. Other Distribution Channels

Canada Nutraceutical Industry Segmentation By Geography

- 1. Canada

Canada Nutraceutical Industry Regional Market Share

Geographic Coverage of Canada Nutraceutical Industry

Canada Nutraceutical Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.05% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Functional Food

- 5.1.1.1. Functional Cereal

- 5.1.1.2. Functional Bakery & Confectionary

- 5.1.1.3. Functional Dairy

- 5.1.1.4. Functional Snacks

- 5.1.1.5. Other Functional Foods

- 5.1.2. Functional Beverage

- 5.1.2.1. Energy Drink

- 5.1.2.2. Sports Drink

- 5.1.2.3. Fortified Juice

- 5.1.2.4. Dairy and Dairy Alternative Beverage

- 5.1.2.5. Other Functional Beverages

- 5.1.3. Dietary Supplement

- 5.1.3.1. Vitamin

- 5.1.3.2. Mineral

- 5.1.3.3. Botanical

- 5.1.3.4. Enzyme

- 5.1.3.5. Fatty Acid

- 5.1.3.6. Protein

- 5.1.3.7. Other Dietary Supplements

- 5.1.1. Functional Food

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Specialty Stores

- 5.2.2. Supermarkets/Hypermarkets

- 5.2.3. Convenience Stores

- 5.2.4. Drug Stores/Pharmacies

- 5.2.5. Online Retail Stores

- 5.2.6. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Canada Nutraceutical Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Functional Food

- 6.1.1.1. Functional Cereal

- 6.1.1.2. Functional Bakery & Confectionary

- 6.1.1.3. Functional Dairy

- 6.1.1.4. Functional Snacks

- 6.1.1.5. Other Functional Foods

- 6.1.2. Functional Beverage

- 6.1.2.1. Energy Drink

- 6.1.2.2. Sports Drink

- 6.1.2.3. Fortified Juice

- 6.1.2.4. Dairy and Dairy Alternative Beverage

- 6.1.2.5. Other Functional Beverages

- 6.1.3. Dietary Supplement

- 6.1.3.1. Vitamin

- 6.1.3.2. Mineral

- 6.1.3.3. Botanical

- 6.1.3.4. Enzyme

- 6.1.3.5. Fatty Acid

- 6.1.3.6. Protein

- 6.1.3.7. Other Dietary Supplements

- 6.1.1. Functional Food

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Specialty Stores

- 6.2.2. Supermarkets/Hypermarkets

- 6.2.3. Convenience Stores

- 6.2.4. Drug Stores/Pharmacies

- 6.2.5. Online Retail Stores

- 6.2.6. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Herbalife International of America Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Alticor Inc (Amway)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 General Mills Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 PepsiCo Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Lactalis Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Magnum Nutraceuticals*List Not Exhaustive

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Red Bull GmbH

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Danone S A

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Natural Factors Nutritional Products Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Kellogg Company

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Pfizer Inc

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Nestlé S A

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Herbalife International of America Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Canada Nutraceutical Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Canada Nutraceutical Industry Share (%) by Company 2025

List of Tables

- Table 1: Canada Nutraceutical Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Canada Nutraceutical Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 3: Canada Nutraceutical Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Canada Nutraceutical Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Canada Nutraceutical Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 6: Canada Nutraceutical Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Nutraceutical Industry?

The projected CAGR is approximately 6.05%.

2. Which companies are prominent players in the Canada Nutraceutical Industry?

Key companies in the market include Herbalife International of America Inc, Alticor Inc (Amway), General Mills Inc, PepsiCo Inc, Lactalis Group, Magnum Nutraceuticals*List Not Exhaustive, Red Bull GmbH, Danone S A, Natural Factors Nutritional Products Ltd, Kellogg Company, Pfizer Inc, Nestlé S A.

3. What are the main segments of the Canada Nutraceutical Industry?

The market segments include Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.65 Million as of 2022.

5. What are some drivers contributing to market growth?

Popularity of On-the-Go Snacking Options; Trend Of Clean Label and Plant-Based Bars.

6. What are the notable trends driving market growth?

Increasing Expenditure on Health and Wellness.

7. Are there any restraints impacting market growth?

Availability of Counterfeit Products.

8. Can you provide examples of recent developments in the market?

In October 2022, with the launch of the VitaBeans product line, Nestlé and Natures Bounty entered the Canadian vitamins and supplements market. Besides being vegetarian, the beans also contain no gluten or gelatin and no artificial colors or flavors.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Nutraceutical Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Nutraceutical Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Nutraceutical Industry?

To stay informed about further developments, trends, and reports in the Canada Nutraceutical Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence