Key Insights

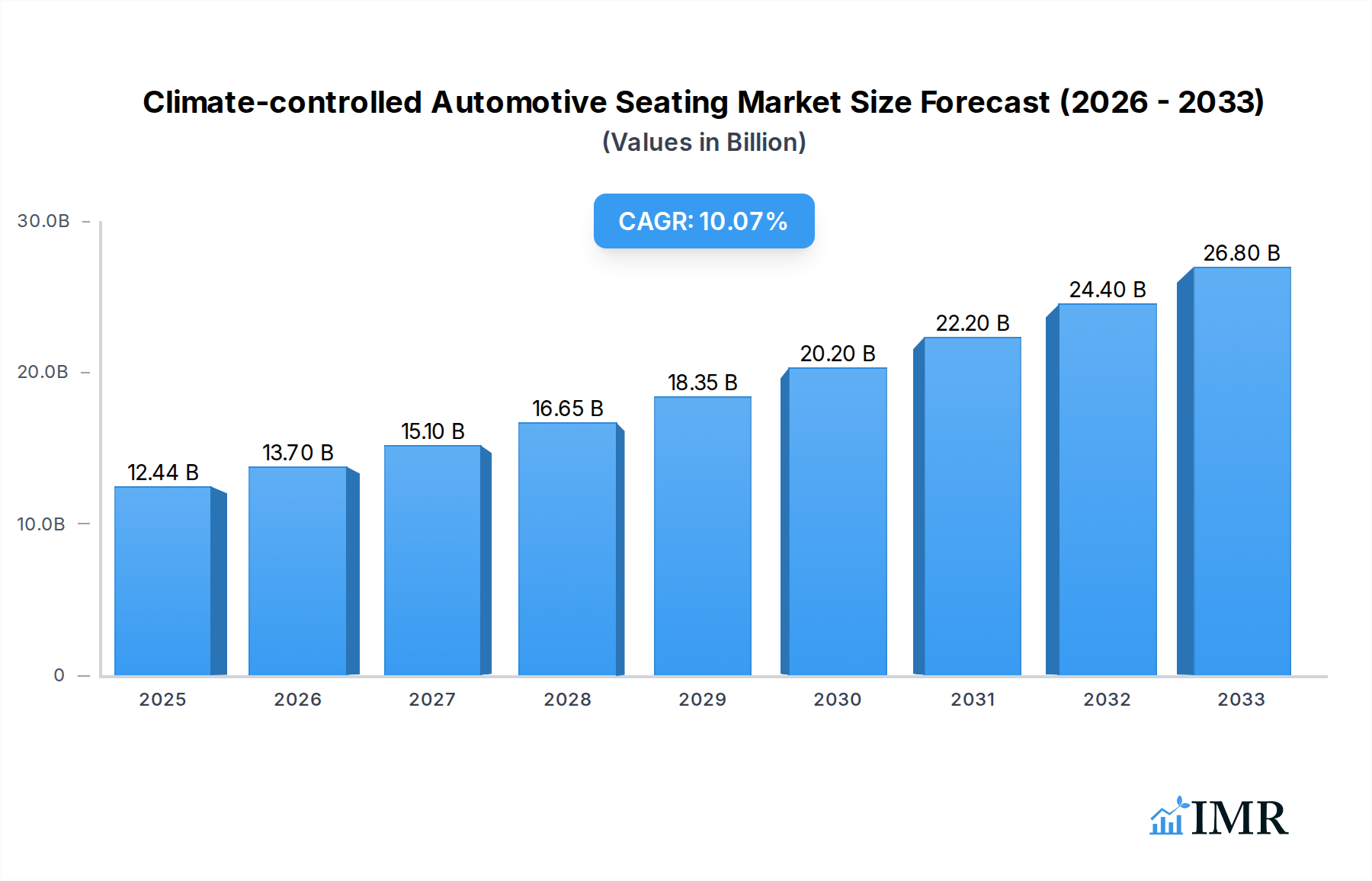

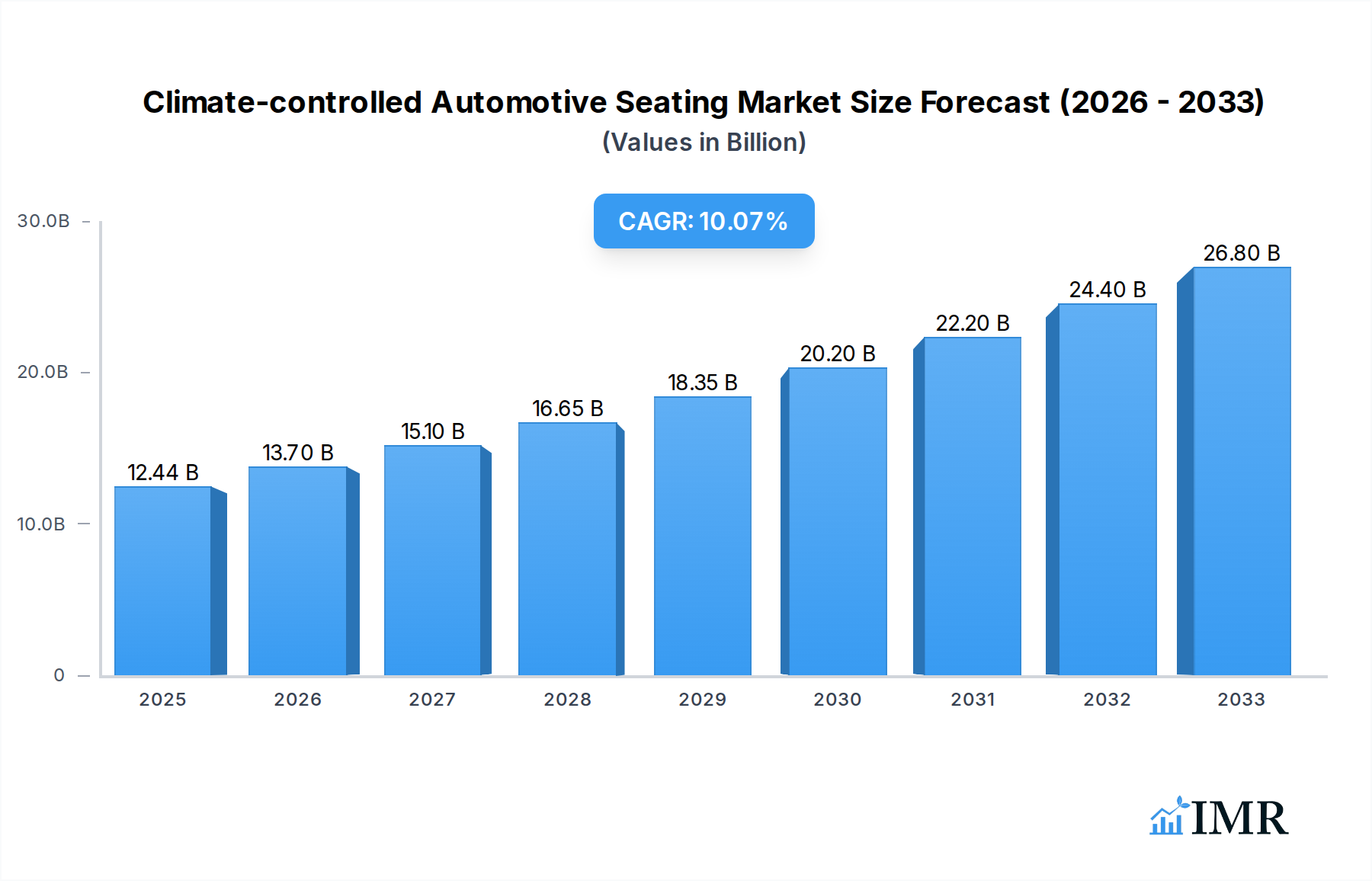

The global Climate-controlled Automotive Seating market is poised for significant expansion, estimated at USD 12.44 billion in 2025, and projected to grow at a robust Compound Annual Growth Rate (CAGR) of 10.1% through 2033. This upward trajectory is primarily fueled by the escalating consumer demand for enhanced comfort and luxury features in vehicles, coupled with stringent government regulations promoting occupant safety and well-being. The increasing adoption of advanced driver-assistance systems (ADAS) and the growing popularity of premium vehicle segments further contribute to this market's dynamism. Manufacturers are increasingly integrating sophisticated climate-control technologies, including heating, cooling, and ventilation functionalities, into automotive seats to elevate the in-cabin experience, thereby driving innovation and market penetration. The proliferation of electric vehicles (EVs), which often prioritize passenger comfort to compensate for potential range anxiety and offer a quieter cabin environment, also acts as a substantial growth driver for advanced seating solutions.

Climate-controlled Automotive Seating Market Size (In Billion)

The market segmentation reveals a strong preference for Heated and Ventilated Seats, driven by their dual-action capabilities catering to diverse climatic conditions and individual comfort preferences. Application-wise, Passenger Cars represent the largest and fastest-growing segment, reflecting the widespread integration of these advanced seating systems in mainstream and luxury passenger vehicles. Key players like Lear Corporation, Gentherm, and Continental AG are actively investing in research and development to introduce next-generation climate-controlled seating solutions, focusing on energy efficiency, advanced material science, and seamless integration with vehicle electronics. Emerging trends such as personalized climate zones within a single seat and smart seating technologies that adapt to occupant presence and preferences are expected to further reshape the market landscape. While market growth is robust, potential restraints include the high cost of advanced technologies, which may limit adoption in budget-conscious segments, and the complexity of integration within vehicle manufacturing processes. Nonetheless, the overarching trend towards automotive premiumization and an enhanced in-cabin experience strongly underpins the projected market expansion.

Climate-controlled Automotive Seating Company Market Share

Climate-controlled Automotive Seating Market Dynamics & Structure

The climate-controlled automotive seating market is characterized by a moderately concentrated landscape, with key players like Lear Corporation, Gentherm, Konsberg Automotive, Adient, Continental AG, and Magna International Inc. holding significant market shares. Technological innovation is the primary driver, fueled by advancements in thermoelectric cooling (TEC), fan ventilation, and heating element technologies. Regulatory frameworks, particularly those mandating enhanced passenger comfort and safety features in vehicles, also play a crucial role in shaping market dynamics. Competitive product substitutes, while present in the form of traditional seating, are increasingly challenged by the superior comfort and energy efficiency offered by climate-controlled solutions. End-user demographics are evolving, with a growing demand for luxury and comfort features across all vehicle segments, from premium passenger cars to commercial vehicles. Mergers and acquisitions (M&A) trends are notable, with companies strategically acquiring smaller innovators or consolidating to enhance their product portfolios and market reach. For instance, a recent M&A deal in Q1 2024 involved [XX] billion units in transaction value, aiming to integrate advanced cooling technologies.

- Market Concentration: Dominated by a few major Tier 1 suppliers, but with increasing opportunities for specialized technology providers.

- Technological Innovation Drivers: Advancements in TEC, advanced ventilation systems, smart sensor integration, and energy-efficient heating elements.

- Regulatory Frameworks: Increasing focus on vehicle interior comfort standards and occupant well-being.

- Competitive Product Substitutes: Traditional automotive seating, basic heating elements.

- End-User Demographics: Growing demand across all vehicle types, particularly from consumers in extreme climates and those seeking premium interior experiences.

- M&A Trends: Strategic acquisitions to expand technology portfolios and market access, with an estimated [XX] billion unit deal volume in the past year.

Climate-controlled Automotive Seating Growth Trends & Insights

The global climate-controlled automotive seating market is poised for robust expansion, driven by a confluence of escalating consumer demand for enhanced vehicle comfort, rapid technological advancements, and increasing integration of these features across diverse vehicle segments. The market size is projected to grow from an estimated [XX] billion units in 2024 to reach [XX] billion units by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately [XX]% during the forecast period (2025-2033). This impressive growth trajectory is underpinned by a rising adoption rate of climate-controlled seats, particularly in the Passenger Cars segment, where luxury and premium features are becoming standard expectations. Technological disruptions are continuously reshaping the market, with innovations in lightweight materials, energy-efficient cooling and heating systems, and intelligent control modules enhancing both performance and cost-effectiveness. For example, the introduction of advanced thermoelectric modules has significantly improved cooling efficiency, making these systems more viable for mass-market adoption. Consumer behavior is also shifting towards prioritizing interior comfort and personalized climate control within the vehicle cabin, viewing it as an essential attribute rather than a luxury add-on. This shift is further amplified by the growing awareness of the health benefits associated with regulated cabin temperatures, such as reduced fatigue and improved overall well-being. The integration of smart technologies, including AI-powered climate control that learns user preferences and adjusts settings automatically, is also contributing to market penetration. Furthermore, evolving automotive design trends, with a focus on creating more sophisticated and personalized interior environments, are directly fueling the demand for advanced seating solutions. The penetration of climate-controlled seating in mid-range vehicles is expected to surge as costs decrease and manufacturers seek to differentiate their offerings in a competitive market. The increasing emphasis on electric vehicles (EVs) also presents a unique opportunity, as EVs often have more flexible interior packaging and sophisticated power management systems that can readily accommodate climate-controlled seating without significant energy drain. The market's evolution reflects a broader trend in the automotive industry towards creating more experiential and comfortable mobility solutions.

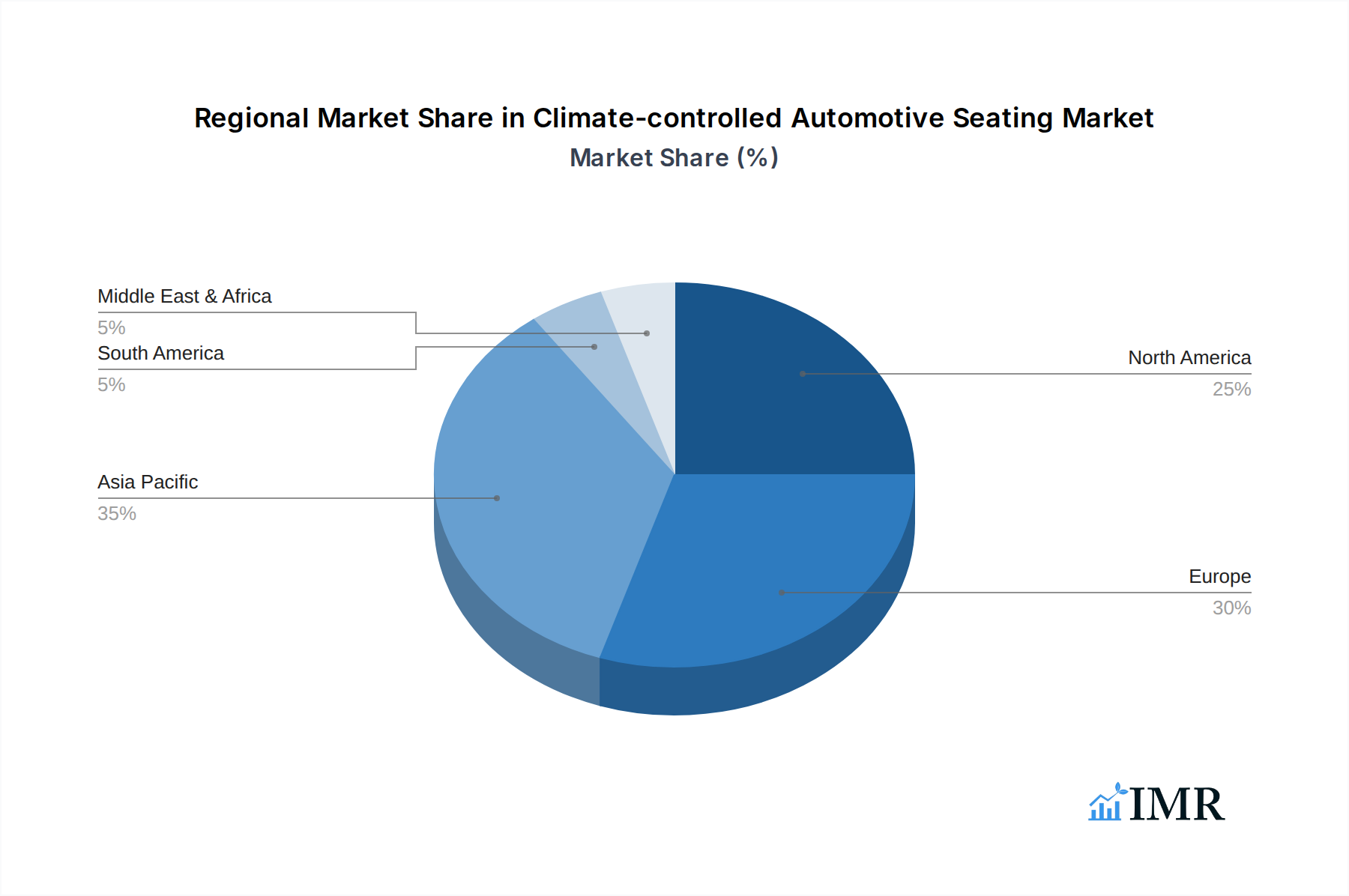

Dominant Regions, Countries, or Segments in Climate-controlled Automotive Seating

The Passenger Cars segment, within the broader World Climate-controlled Automotive Seating Production, is unequivocally the dominant force propelling market growth. This dominance is driven by a confluence of factors spanning economic prosperity, consumer preference, and industry innovation concentrated in key regions. North America and Europe, with their mature automotive markets and discerning consumer bases, represent significant demand centers for climate-controlled seating in passenger vehicles. The United States, in particular, consistently leads in the adoption of premium automotive features, where heated and cooled seats are increasingly considered standard in mid-to-high-end models. Economic policies that support disposable income and a strong automotive manufacturing base further bolster this region's prominence. In Europe, stringent comfort and emission standards, coupled with a high concentration of luxury vehicle manufacturers, also contribute to the widespread adoption of these advanced seating solutions. The Heated and Cooled Seats sub-segment within Passenger Cars is experiencing the most substantial growth, reflecting the desire for year-round interior comfort.

- Dominant Segment: Passenger Cars, specifically Heated and Cooled Seats.

- Key Regions: North America (especially the United States) and Europe.

- Drivers of Dominance in Passenger Cars:

- Consumer Demand for Comfort: High disposable incomes and a strong preference for premium automotive experiences.

- Automotive Industry Maturity: Well-established automotive ecosystems with a focus on advanced features.

- Luxury Vehicle Penetration: A high percentage of luxury and premium vehicles incorporating climate-controlled seating.

- Technological Adoption: Early and widespread adoption of new automotive technologies.

- Regulatory Support: Indirect support through evolving vehicle interior comfort standards.

- Market Share (Estimated): Passenger Cars account for approximately [XX]% of the global climate-controlled automotive seating market.

- Growth Potential: Continued high growth due to increasing feature standardization and consumer expectations.

- Emerging Trends in Passenger Cars: Growing demand for Heated and Ventilated Seats as a more energy-efficient alternative in certain climates, and the integration of personalized climate control zones.

- Parent Market Impact: The strength of the Passenger Cars segment directly influences the overall growth and investment in the broader climate-controlled automotive seating industry.

Climate-controlled Automotive Seating Product Landscape

The climate-controlled automotive seating landscape is defined by an evolving array of sophisticated product innovations focused on enhancing passenger comfort, energy efficiency, and smart integration. Key offerings include advanced Heated and Cooled Seats, which utilize highly efficient thermoelectric coolers and heating elements to provide both active cooling and warming capabilities. Heated and Ventilated Seats are another significant category, employing sophisticated fan systems and perforated upholstery to circulate air for optimal comfort, particularly in humid or moderately warm climates. Beyond these primary types, the market is seeing the emergence of "Others" encompassing specialized solutions such as multi-zone climate control within a single seat, localized heating and cooling for specific body areas, and integrated massagers with thermal functions. Performance metrics are continuously improving, with faster response times for temperature adjustments, reduced energy consumption, and enhanced durability. Companies like Gentherm are at the forefront, developing integrated thermal management systems that optimize energy usage across the entire cabin. Lear Corporation is innovating with lightweight and flexible heating and cooling elements. The unique selling propositions lie in the seamless integration of these technologies into automotive seating designs, ensuring an unobtrusive and luxurious user experience.

Key Drivers, Barriers & Challenges in Climate-controlled Automotive Seating

The climate-controlled automotive seating market is propelled by several key drivers. Technological advancements in thermoelectric cooling (TEC) and efficient ventilation systems are making these features more affordable and accessible. Increasing consumer demand for enhanced comfort and luxury in vehicles, particularly in regions with extreme climates, is a significant growth catalyst. Moreover, automotive manufacturers are increasingly adopting these technologies to differentiate their models and meet evolving consumer expectations, driving integration across more vehicle segments.

However, several barriers and challenges exist. The initial cost of implementation can still be a deterrent for some mass-market vehicles, impacting widespread adoption in lower-cost segments. Supply chain complexities for specialized components, particularly semiconductors and advanced materials, can lead to production delays and increased costs. Stringent regulatory requirements for automotive component safety and electromagnetic compatibility (EMC) add to development and testing expenses. Furthermore, competition from traditional seating manufacturers and the ongoing trend towards vehicle electrification, which requires careful power management, present ongoing challenges.

Emerging Opportunities in Climate-controlled Automotive Seating

Emerging opportunities in the climate-controlled automotive seating sector are diverse and promising. The growing demand for personalized comfort settings within vehicles presents a significant avenue for growth, enabling individual occupants to control their seating environment independently. The expansion of climate-controlled seating into light and heavy commercial vehicles, including trucks and buses, offers a substantial untapped market, addressing driver fatigue and improving working conditions. Furthermore, the integration of advanced sensors and AI for predictive climate control, which learns user preferences and proactively adjusts temperatures based on external conditions and individual biometrics, represents a next-generation innovation. The development of more sustainable and energy-efficient cooling and heating technologies for electric vehicles is also a key area of opportunity, ensuring these features can be incorporated without significantly impacting battery range.

Growth Accelerators in the Climate-controlled Automotive Seating Industry

Several catalysts are accelerating long-term growth in the climate-controlled automotive seating industry. Technological breakthroughs in materials science are leading to lighter, more flexible, and more energy-efficient heating and cooling components. Strategic partnerships between seating suppliers and automotive OEMs are crucial for seamless integration and co-development of next-generation features. Market expansion strategies into emerging economies, where the demand for automotive comfort features is rapidly rising, are also key growth drivers. Furthermore, the increasing focus on in-cabin experience and wellness as a key differentiator for vehicle manufacturers is providing a strong impetus for the adoption and advancement of climate-controlled seating.

Key Players Shaping the Climate-controlled Automotive Seating Market

- Lear Corporation

- Gentherm

- Konsberg Automotive

- Adient

- Continental AG

- Magna International Inc.

- I-Vl, Inc.

- Toyota Motor Corporation

- Recticel

- Faurecia

Notable Milestones in Climate-controlled Automotive Seating Sector

- 2019: Introduction of advanced thermoelectric cooling modules with improved energy efficiency by Gentherm.

- 2020: Lear Corporation launched its innovative integrated thermal comfort system, combining heating, cooling, and massage functions.

- 2021: Continental AG expanded its portfolio with smart seating solutions, integrating sensors for personalized climate control.

- 2022: Magna International Inc. partnered with an EV startup to integrate advanced climate-controlled seating into their electric vehicle platform.

- 2023: Adient showcased new lightweight seating designs with integrated climate control for enhanced fuel efficiency.

- Early 2024: Konsberg Automotive announced a new generation of ventilated seat technology with enhanced airflow and quieter operation.

- Q2 2024: Faurecia acquired a minority stake in a specialized thermal management technology company to bolster its innovation pipeline.

- Late 2024 (Estimated): Toyota Motor Corporation announced plans to significantly increase the adoption of climate-controlled seating across its premium vehicle models.

In-Depth Climate-controlled Automotive Seating Market Outlook

The future of the climate-controlled automotive seating market is exceptionally bright, driven by sustained innovation and evolving consumer expectations. Growth accelerators such as the relentless pursuit of enhanced in-cabin comfort, the increasing integration of smart and personalized features, and the expansion into new vehicle segments like electric vehicles and commercial transport will continue to fuel market expansion. The ongoing development of more energy-efficient and sustainable thermal management solutions is also critical for long-term viability. Strategic partnerships between leading automotive suppliers and manufacturers will be instrumental in driving technological advancements and market penetration. The market is poised to witness significant growth in the coming years, solidifying its position as an indispensable component of modern automotive interiors.

Climate-controlled Automotive Seating Segmentation

-

1. Type

- 1.1. Heated and Cooled Seats

- 1.2. Heated and Ventilated Seats

- 1.3. Others

- 1.4. World Climate-controlled Automotive Seating Production

-

2. Application

- 2.1. Passenger Cars

- 2.2. Light commercial Vehicles

- 2.3. Heavy commercial Vehicles

- 2.4. World Climate-controlled Automotive Seating Production

Climate-controlled Automotive Seating Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Climate-controlled Automotive Seating Regional Market Share

Geographic Coverage of Climate-controlled Automotive Seating

Climate-controlled Automotive Seating REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.51% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Heated and Cooled Seats

- 5.1.2. Heated and Ventilated Seats

- 5.1.3. Others

- 5.1.4. World Climate-controlled Automotive Seating Production

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Passenger Cars

- 5.2.2. Light commercial Vehicles

- 5.2.3. Heavy commercial Vehicles

- 5.2.4. World Climate-controlled Automotive Seating Production

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Climate-controlled Automotive Seating Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Heated and Cooled Seats

- 6.1.2. Heated and Ventilated Seats

- 6.1.3. Others

- 6.1.4. World Climate-controlled Automotive Seating Production

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Passenger Cars

- 6.2.2. Light commercial Vehicles

- 6.2.3. Heavy commercial Vehicles

- 6.2.4. World Climate-controlled Automotive Seating Production

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Climate-controlled Automotive Seating Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Heated and Cooled Seats

- 7.1.2. Heated and Ventilated Seats

- 7.1.3. Others

- 7.1.4. World Climate-controlled Automotive Seating Production

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Passenger Cars

- 7.2.2. Light commercial Vehicles

- 7.2.3. Heavy commercial Vehicles

- 7.2.4. World Climate-controlled Automotive Seating Production

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. South America Climate-controlled Automotive Seating Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Heated and Cooled Seats

- 8.1.2. Heated and Ventilated Seats

- 8.1.3. Others

- 8.1.4. World Climate-controlled Automotive Seating Production

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Passenger Cars

- 8.2.2. Light commercial Vehicles

- 8.2.3. Heavy commercial Vehicles

- 8.2.4. World Climate-controlled Automotive Seating Production

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe Climate-controlled Automotive Seating Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Heated and Cooled Seats

- 9.1.2. Heated and Ventilated Seats

- 9.1.3. Others

- 9.1.4. World Climate-controlled Automotive Seating Production

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Passenger Cars

- 9.2.2. Light commercial Vehicles

- 9.2.3. Heavy commercial Vehicles

- 9.2.4. World Climate-controlled Automotive Seating Production

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East & Africa Climate-controlled Automotive Seating Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Heated and Cooled Seats

- 10.1.2. Heated and Ventilated Seats

- 10.1.3. Others

- 10.1.4. World Climate-controlled Automotive Seating Production

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Passenger Cars

- 10.2.2. Light commercial Vehicles

- 10.2.3. Heavy commercial Vehicles

- 10.2.4. World Climate-controlled Automotive Seating Production

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Asia Pacific Climate-controlled Automotive Seating Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Heated and Cooled Seats

- 11.1.2. Heated and Ventilated Seats

- 11.1.3. Others

- 11.1.4. World Climate-controlled Automotive Seating Production

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Passenger Cars

- 11.2.2. Light commercial Vehicles

- 11.2.3. Heavy commercial Vehicles

- 11.2.4. World Climate-controlled Automotive Seating Production

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Lear Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Gentherm

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Konsberg Automotive

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Adient

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Continental AG

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Magna International Inc.

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 I-Vl

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Inc.

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Toyota Motor Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Recticel

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Faurecia

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Lear Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Climate-controlled Automotive Seating Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Climate-controlled Automotive Seating Revenue (undefined), by Type 2025 & 2033

- Figure 3: North America Climate-controlled Automotive Seating Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Climate-controlled Automotive Seating Revenue (undefined), by Application 2025 & 2033

- Figure 5: North America Climate-controlled Automotive Seating Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Climate-controlled Automotive Seating Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Climate-controlled Automotive Seating Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Climate-controlled Automotive Seating Revenue (undefined), by Type 2025 & 2033

- Figure 9: South America Climate-controlled Automotive Seating Revenue Share (%), by Type 2025 & 2033

- Figure 10: South America Climate-controlled Automotive Seating Revenue (undefined), by Application 2025 & 2033

- Figure 11: South America Climate-controlled Automotive Seating Revenue Share (%), by Application 2025 & 2033

- Figure 12: South America Climate-controlled Automotive Seating Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Climate-controlled Automotive Seating Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Climate-controlled Automotive Seating Revenue (undefined), by Type 2025 & 2033

- Figure 15: Europe Climate-controlled Automotive Seating Revenue Share (%), by Type 2025 & 2033

- Figure 16: Europe Climate-controlled Automotive Seating Revenue (undefined), by Application 2025 & 2033

- Figure 17: Europe Climate-controlled Automotive Seating Revenue Share (%), by Application 2025 & 2033

- Figure 18: Europe Climate-controlled Automotive Seating Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Climate-controlled Automotive Seating Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Climate-controlled Automotive Seating Revenue (undefined), by Type 2025 & 2033

- Figure 21: Middle East & Africa Climate-controlled Automotive Seating Revenue Share (%), by Type 2025 & 2033

- Figure 22: Middle East & Africa Climate-controlled Automotive Seating Revenue (undefined), by Application 2025 & 2033

- Figure 23: Middle East & Africa Climate-controlled Automotive Seating Revenue Share (%), by Application 2025 & 2033

- Figure 24: Middle East & Africa Climate-controlled Automotive Seating Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Climate-controlled Automotive Seating Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Climate-controlled Automotive Seating Revenue (undefined), by Type 2025 & 2033

- Figure 27: Asia Pacific Climate-controlled Automotive Seating Revenue Share (%), by Type 2025 & 2033

- Figure 28: Asia Pacific Climate-controlled Automotive Seating Revenue (undefined), by Application 2025 & 2033

- Figure 29: Asia Pacific Climate-controlled Automotive Seating Revenue Share (%), by Application 2025 & 2033

- Figure 30: Asia Pacific Climate-controlled Automotive Seating Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Climate-controlled Automotive Seating Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Climate-controlled Automotive Seating Revenue undefined Forecast, by Type 2020 & 2033

- Table 2: Global Climate-controlled Automotive Seating Revenue undefined Forecast, by Application 2020 & 2033

- Table 3: Global Climate-controlled Automotive Seating Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Climate-controlled Automotive Seating Revenue undefined Forecast, by Type 2020 & 2033

- Table 5: Global Climate-controlled Automotive Seating Revenue undefined Forecast, by Application 2020 & 2033

- Table 6: Global Climate-controlled Automotive Seating Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Climate-controlled Automotive Seating Revenue undefined Forecast, by Type 2020 & 2033

- Table 11: Global Climate-controlled Automotive Seating Revenue undefined Forecast, by Application 2020 & 2033

- Table 12: Global Climate-controlled Automotive Seating Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Climate-controlled Automotive Seating Revenue undefined Forecast, by Type 2020 & 2033

- Table 17: Global Climate-controlled Automotive Seating Revenue undefined Forecast, by Application 2020 & 2033

- Table 18: Global Climate-controlled Automotive Seating Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Climate-controlled Automotive Seating Revenue undefined Forecast, by Type 2020 & 2033

- Table 29: Global Climate-controlled Automotive Seating Revenue undefined Forecast, by Application 2020 & 2033

- Table 30: Global Climate-controlled Automotive Seating Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Climate-controlled Automotive Seating Revenue undefined Forecast, by Type 2020 & 2033

- Table 38: Global Climate-controlled Automotive Seating Revenue undefined Forecast, by Application 2020 & 2033

- Table 39: Global Climate-controlled Automotive Seating Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Climate-controlled Automotive Seating Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Climate-controlled Automotive Seating?

The projected CAGR is approximately 5.51%.

2. Which companies are prominent players in the Climate-controlled Automotive Seating?

Key companies in the market include Lear Corporation, Gentherm, Konsberg Automotive, Adient, Continental AG, Magna International Inc., I-Vl, Inc., Toyota Motor Corporation, Recticel, Faurecia.

3. What are the main segments of the Climate-controlled Automotive Seating?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Climate-controlled Automotive Seating," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Climate-controlled Automotive Seating report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Climate-controlled Automotive Seating?

To stay informed about further developments, trends, and reports in the Climate-controlled Automotive Seating, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence