Key Insights

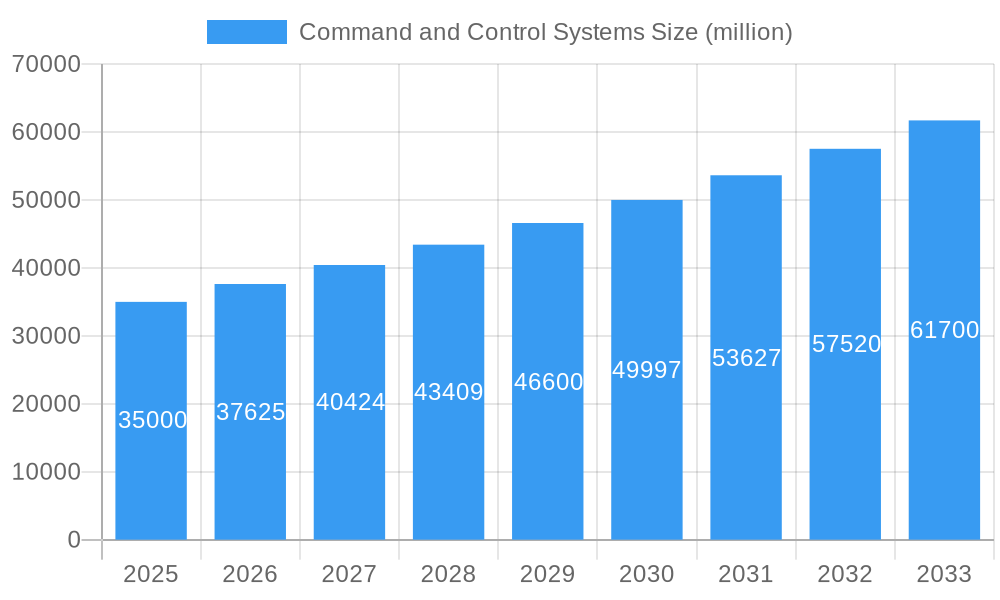

The global Command and Control (C2) Systems market is poised for significant expansion, driven by increasing geopolitical complexities and the imperative for enhanced situational awareness and operational effectiveness across defense, public safety, and other critical sectors. With an estimated market size of approximately $35 billion in 2025, and projected to grow at a Compound Annual Growth Rate (CAGR) of around 7.5% through 2033, the market is expected to reach over $60 billion by the end of the forecast period. Key growth drivers include the escalating need for integrated C2 solutions capable of managing diverse sensor inputs, complex communication networks, and autonomous systems. Nations worldwide are heavily investing in modernizing their military capabilities and bolstering internal security infrastructure, directly fueling demand for advanced C2 platforms. The "Others" application segment, encompassing civilian infrastructure protection, emergency response, and industrial automation, is also demonstrating robust growth as C2 principles are increasingly applied beyond traditional military contexts.

Command and Control Systems Market Size (In Billion)

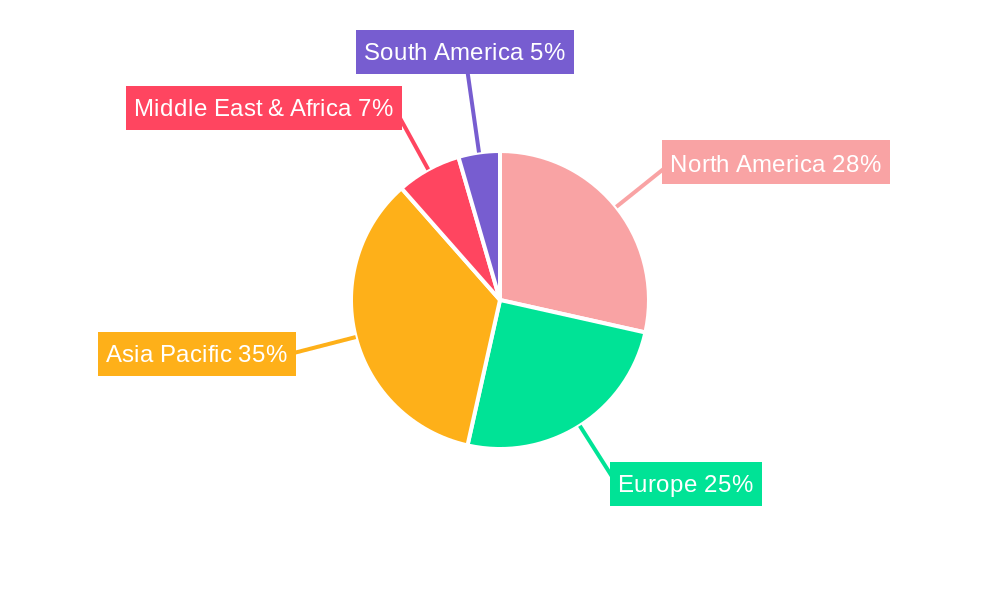

The market is characterized by a strong focus on technological advancements, including artificial intelligence (AI) and machine learning (ML) for intelligent data processing and decision support, cloud-based C2 solutions for scalability and accessibility, and the integration of advanced networking technologies for seamless data exchange. However, the market faces certain restraints, such as the high cost of implementation and integration for legacy systems, stringent cybersecurity concerns and evolving threat landscapes, and the complexity of interoperability between different C2 platforms and national defense systems. The 'Land' segment currently holds the largest market share due to extensive battlefield requirements, followed closely by 'Naval' and 'Air' applications. Asia Pacific, led by China and India's substantial defense modernization efforts, is emerging as a dominant region, with North America and Europe also presenting substantial market opportunities due to ongoing technological upgrades and regional security challenges.

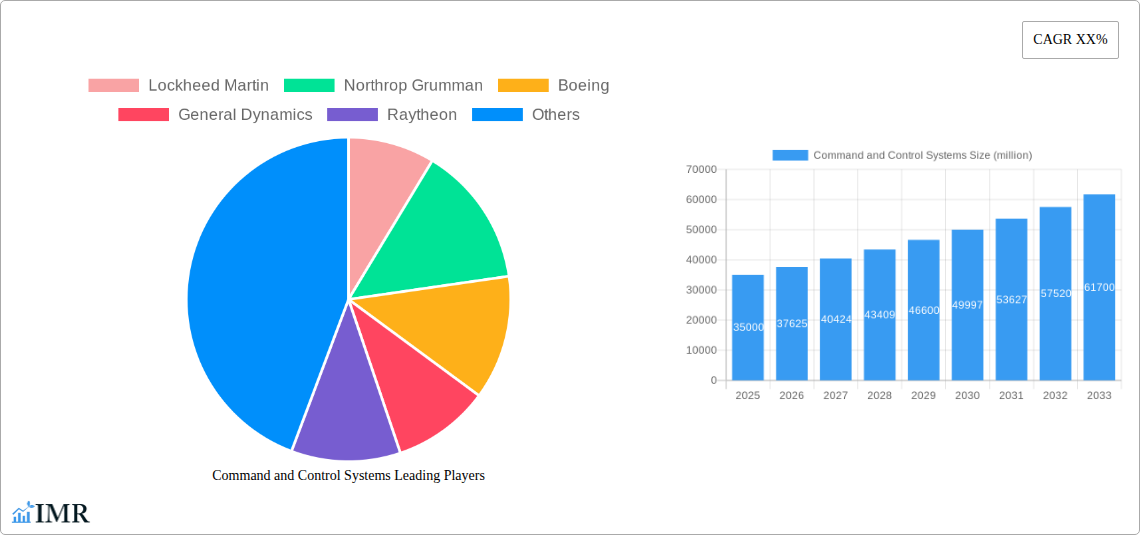

Command and Control Systems Company Market Share

Absolutely! Here is the SEO-optimized report description for Command and Control Systems, incorporating your specified requirements and high-traffic keywords.

Command and Control Systems Market Dynamics & Structure

The global Command and Control (C2) systems market is characterized by a dynamic and evolving landscape, driven by escalating geopolitical tensions, increasing homeland security concerns, and the relentless pursuit of technological superiority. This report delves into the intricate market structure, analyzing key aspects such as market concentration, technological innovation drivers, and regulatory frameworks that shape the industry. We examine the competitive product substitutes, understanding how advancements in AI, IoT, and cybersecurity are creating both opportunities and challenges. End-user demographics are critically assessed, with a focus on defense forces, public safety agencies, and critical infrastructure operators demanding increasingly sophisticated C2 capabilities. Mergers and Acquisitions (M&A) trends are a significant indicator of market consolidation and strategic positioning, with major players like Lockheed Martin, Northrop Grumman, and Boeing actively engaged in acquiring complementary technologies and expanding their portfolios.

- Market Concentration: Highly concentrated with a few dominant players holding significant market share.

- Technological Innovation Drivers: AI/ML integration, IoT connectivity, advanced sensor fusion, edge computing, cybersecurity advancements.

- Regulatory Frameworks: Stringent export controls, national security mandates, data privacy regulations impacting deployment and interoperability.

- Competitive Product Substitutes: Evolving C2 solutions, commercial off-the-shelf (COTS) integration, open architecture designs challenging proprietary systems.

- End-User Demographics: Primarily government entities (defense and public safety), critical infrastructure operators, and international organizations.

- M&A Trends: Strategic acquisitions focused on AI, cyber, and integrated C2 solutions. Notable deal volumes are anticipated to increase, driven by the need for comprehensive capabilities.

Command and Control Systems Growth Trends & Insights

The Command and Control (C2) systems market is poised for significant expansion, projected to grow from an estimated $25,500 million in 2025 to $35,800 million by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of approximately 4.5% during the forecast period (2025–2033). This growth is propelled by a confluence of factors, including the increasing sophistication of global security threats, the imperative for enhanced situational awareness, and the widespread adoption of digital transformation across defense and public safety sectors. Market penetration is deepening, particularly within advanced defense capabilities and homeland security operations, where C2 systems are becoming indispensable for effective decision-making and operational efficiency. Technological disruptions, such as the integration of artificial intelligence (AI) and machine learning (ML) for predictive analytics and automated response, are revolutionizing C2 capabilities. The evolution of AI in C2 systems is leading to more intelligent and autonomous operations, enhancing threat detection and response times.

Consumer behavior shifts are evident, with end-users demanding more agile, scalable, and interoperable C2 platforms that can seamlessly integrate data from diverse sources. The historical period (2019–2024) has witnessed a steady upward trajectory, laying the groundwork for accelerated growth in the coming years. The adoption of cloud-based C2 solutions and the increasing demand for secure, resilient communication networks are further fueling market expansion. The estimated market size for 2025 is $25,500 million, reflecting a strong foundation for future growth. Innovations in data fusion, intelligent automation, and cyber resilience are critical enablers for this expansion. The market is witnessing a sustained demand for C2 systems that can provide real-time, multi-domain awareness, enabling joint operational effectiveness across land, naval, and air domains. The increasing complexity of modern warfare and the rise of asymmetric threats necessitate C2 systems that can process vast amounts of data and facilitate rapid, informed decision-making. Furthermore, the global emphasis on cybersecurity and data protection is driving investments in highly secure and resilient C2 infrastructures, ensuring the integrity and confidentiality of critical information.

Dominant Regions, Countries, or Segments in Command and Control Systems

The Defense application segment, historically and consistently, is the primary driver of the global Command and Control (C2) systems market, accounting for an estimated 75% of the total market share in 2025. This dominance stems from significant government investments in national security, advanced military modernization programs, and the escalating need for superior battlefield awareness and strategic coordination. Within the Defense segment, the Air type, with an estimated 35% market share, and Naval types, with an estimated 30% market share, are particularly prominent due to the complexity of modern aerial and maritime warfare, requiring sophisticated integrated C2 solutions for command and control of fleets and air forces. The North American region, particularly the United States, continues to be the largest market for C2 systems, representing an estimated 40% of the global market share in 2025. This leadership is attributed to substantial defense budgets, ongoing military research and development, and the country's pivotal role in global security initiatives.

Key drivers for this regional dominance include government procurement policies, technological innovation driven by leading defense contractors like Lockheed Martin and Northrop Grumman, and the continuous deployment of advanced C2 systems in various operational theaters. The Public Safety application segment is also exhibiting robust growth, driven by increasing concerns over terrorism, natural disasters, and urban security. Countries are investing in integrated C2 platforms to enhance emergency response coordination, disaster management, and law enforcement effectiveness. Countries like Germany and the United Kingdom within Europe, and Japan and South Korea in Asia, are significantly contributing to the growth of the Public Safety C2 market. The growth potential in emerging economies, particularly in the Asia-Pacific region, is substantial, driven by their increasing defense spending and efforts to enhance national security and public safety infrastructure. The strategic importance of interoperability between different C2 systems, both within and across allied nations, is a critical factor influencing market adoption and growth across all segments. Economic policies that favor defense modernization and public safety upgrades, coupled with the deployment of advanced communication and sensor technologies, are further bolstering the market's expansion. The "Others" category within Application and Types, while smaller, includes critical infrastructure protection and civilian aviation control, areas that are also witnessing increased investment in sophisticated C2 capabilities.

Command and Control Systems Product Landscape

The Command and Control (C2) systems product landscape is defined by a rapid evolution towards integrated, intelligent, and multi-domain solutions. Innovations are centered on enhancing situational awareness, enabling seamless data fusion from disparate sensors, and providing intuitive interfaces for operators. Key product advancements include AI-powered decision support systems, secure cloud-based C2 platforms, and edge computing capabilities for real-time data processing. Performance metrics are increasingly focused on reduced latency, improved data accuracy, enhanced cybersecurity resilience, and greater interoperability across different platforms and domains. Unique selling propositions often lie in the ability to provide a unified operational picture, facilitate collaborative planning, and automate routine tasks, thereby reducing cognitive load on operators.

Key Drivers, Barriers & Challenges in Command and Control Systems

Key Drivers:

- Technological Advancements: Integration of AI, ML, IoT, and advanced analytics for enhanced situational awareness and decision-making.

- Geopolitical Instability: Rising global security threats and the need for modern defense and public safety capabilities.

- Modernization Programs: Government investments in upgrading legacy defense and security infrastructure with advanced C2 systems.

- Interoperability Demands: Increasing need for seamless communication and data sharing across different services and allied nations.

Barriers & Challenges:

- High Development & Procurement Costs: Significant financial investment required for R&D, system integration, and deployment.

- Regulatory Hurdles & Export Controls: Complex and stringent regulations, particularly for defense-related C2 systems, can impede global market access.

- Cybersecurity Threats: The persistent and evolving nature of cyberattacks poses a continuous risk to the integrity and security of C2 systems.

- Supply Chain Disruptions: Reliance on global supply chains for critical components can lead to vulnerabilities and delays, impacting timely delivery and operational readiness. Quantifiable impacts include project delays up to 15% and cost escalations of up to 10% due to unforeseen supply chain issues.

Emerging Opportunities in Command and Control Systems

Emerging opportunities in the Command and Control (C2) systems market lie in the expansion of AI-driven autonomous operations, the integration of space-based C2 capabilities, and the development of resilient cyber-physical systems. The increasing demand for secure and scalable cloud-based C2 solutions presents a significant untapped market. Furthermore, the application of C2 principles to civilian sectors like smart city management and critical infrastructure protection offers substantial growth potential. The growing emphasis on human-machine teaming and cognitive augmentation within C2 environments also represents a promising area for innovation and market penetration.

Growth Accelerators in the Command and Control Systems Industry

Technological breakthroughs in areas such as quantum computing for enhanced encryption and advanced AI algorithms for predictive threat analysis are significant growth accelerators. Strategic partnerships between traditional defense contractors and emerging technology firms are fostering innovation and expanding market reach. Market expansion strategies, including the adoption of open architecture C2 frameworks and the development of modular, scalable solutions, are driving widespread adoption. Furthermore, the increasing adoption of C2 systems in non-traditional security domains, such as critical infrastructure monitoring and public health crisis management, is a key growth accelerator.

Key Players Shaping the Command and Control Systems Market

- Lockheed Martin

- Northrop Grumman

- Boeing

- General Dynamics

- Raytheon

- L3Harris

- Leonardo

- Saab AB

- BAE Systems

- Thales Group

- Airbus

- Leidos

- Elbit Systems

- Atos

- ST Engineering

- Indra

- Havelsan Inc.

Notable Milestones in Command and Control Systems Sector

- 2019: Increased investment in AI-driven C2 solutions by major defense contractors.

- 2020: Launch of advanced multi-domain C2 platforms integrating cyber and electronic warfare capabilities.

- 2021: Significant M&A activity focused on acquiring companies with expertise in AI and data analytics for C2.

- 2022: Deployment of cloud-native C2 systems for enhanced flexibility and scalability in military operations.

- 2023: Growing emphasis on resilient C2 architectures to counter sophisticated cyber threats.

- 2024: Advancements in edge computing for real-time C2 decision-making at the tactical edge.

In-Depth Command and Control Systems Market Outlook

The future of the Command and Control (C2) systems market is characterized by continued innovation, strategic consolidation, and expanding applications. Growth accelerators such as the ubiquitous integration of AI and machine learning, the development of secure and resilient cyber-physical systems, and the increasing demand for multi-domain operational awareness will fuel market expansion. Strategic opportunities lie in addressing the evolving threat landscape with agile and adaptive C2 solutions, fostering greater interoperability across allied forces, and extending C2 capabilities to new civilian sectors. The market is poised for sustained growth, driven by a clear imperative for enhanced security, operational efficiency, and informed decision-making in an increasingly complex global environment.

Command and Control Systems Segmentation

-

1. Application

- 1.1. Defence

- 1.2. Public Safety and Others

-

2. Types

- 2.1. Land

- 2.2. Naval

- 2.3. Air

- 2.4. Others

Command and Control Systems Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Command and Control Systems Regional Market Share

Geographic Coverage of Command and Control Systems

Command and Control Systems REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Defence

- 5.1.2. Public Safety and Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Land

- 5.2.2. Naval

- 5.2.3. Air

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Command and Control Systems Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Defence

- 6.1.2. Public Safety and Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Land

- 6.2.2. Naval

- 6.2.3. Air

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Command and Control Systems Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Defence

- 7.1.2. Public Safety and Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Land

- 7.2.2. Naval

- 7.2.3. Air

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Command and Control Systems Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Defence

- 8.1.2. Public Safety and Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Land

- 8.2.2. Naval

- 8.2.3. Air

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Command and Control Systems Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Defence

- 9.1.2. Public Safety and Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Land

- 9.2.2. Naval

- 9.2.3. Air

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Command and Control Systems Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Defence

- 10.1.2. Public Safety and Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Land

- 10.2.2. Naval

- 10.2.3. Air

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Command and Control Systems Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Defence

- 11.1.2. Public Safety and Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Land

- 11.2.2. Naval

- 11.2.3. Air

- 11.2.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Lockheed Martin

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Northrop Grumman

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Boeing

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 General Dynamics

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Raytheon

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 L3Harris

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Leonardo

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Saab AB

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 BAE Systems

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Thales Group

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Airbus

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Leidos

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Elbit Systems

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Atos

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 ST Engineering

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Indra

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Havelsan Inc.

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.1 Lockheed Martin

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Command and Control Systems Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Command and Control Systems Revenue (million), by Application 2025 & 2033

- Figure 3: North America Command and Control Systems Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Command and Control Systems Revenue (million), by Types 2025 & 2033

- Figure 5: North America Command and Control Systems Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Command and Control Systems Revenue (million), by Country 2025 & 2033

- Figure 7: North America Command and Control Systems Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Command and Control Systems Revenue (million), by Application 2025 & 2033

- Figure 9: South America Command and Control Systems Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Command and Control Systems Revenue (million), by Types 2025 & 2033

- Figure 11: South America Command and Control Systems Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Command and Control Systems Revenue (million), by Country 2025 & 2033

- Figure 13: South America Command and Control Systems Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Command and Control Systems Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Command and Control Systems Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Command and Control Systems Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Command and Control Systems Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Command and Control Systems Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Command and Control Systems Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Command and Control Systems Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Command and Control Systems Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Command and Control Systems Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Command and Control Systems Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Command and Control Systems Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Command and Control Systems Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Command and Control Systems Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Command and Control Systems Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Command and Control Systems Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Command and Control Systems Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Command and Control Systems Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Command and Control Systems Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Command and Control Systems Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Command and Control Systems Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Command and Control Systems Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Command and Control Systems Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Command and Control Systems Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Command and Control Systems Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Command and Control Systems Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Command and Control Systems Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Command and Control Systems Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Command and Control Systems Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Command and Control Systems Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Command and Control Systems Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Command and Control Systems Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Command and Control Systems Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Command and Control Systems Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Command and Control Systems Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Command and Control Systems Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Command and Control Systems Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Command and Control Systems Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Command and Control Systems?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Command and Control Systems?

Key companies in the market include Lockheed Martin, Northrop Grumman, Boeing, General Dynamics, Raytheon, L3Harris, Leonardo, Saab AB, BAE Systems, Thales Group, Airbus, Leidos, Elbit Systems, Atos, ST Engineering, Indra, Havelsan Inc..

3. What are the main segments of the Command and Control Systems?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Command and Control Systems," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Command and Control Systems report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Command and Control Systems?

To stay informed about further developments, trends, and reports in the Command and Control Systems, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence