Key Insights

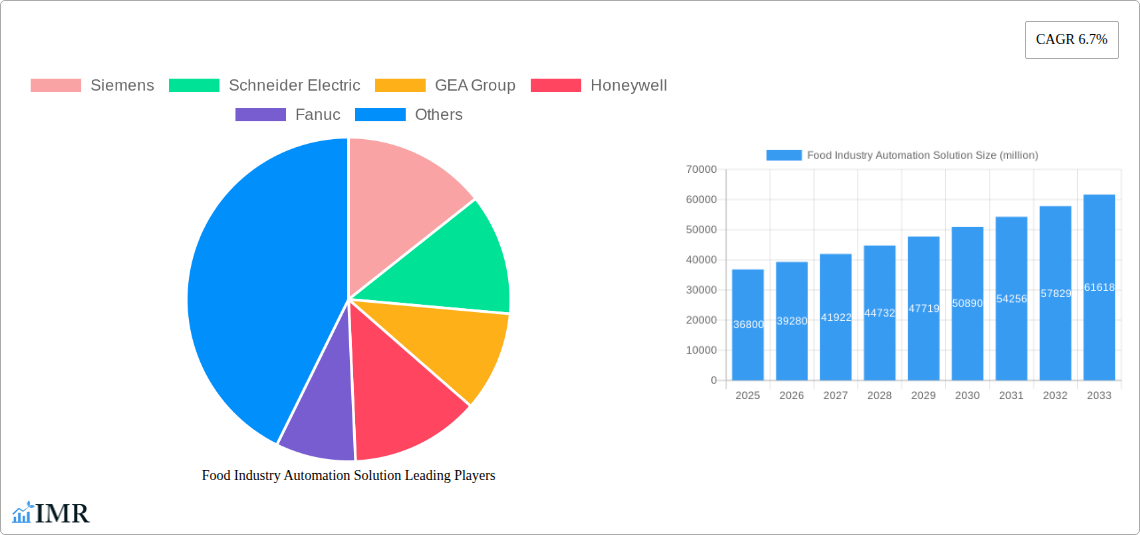

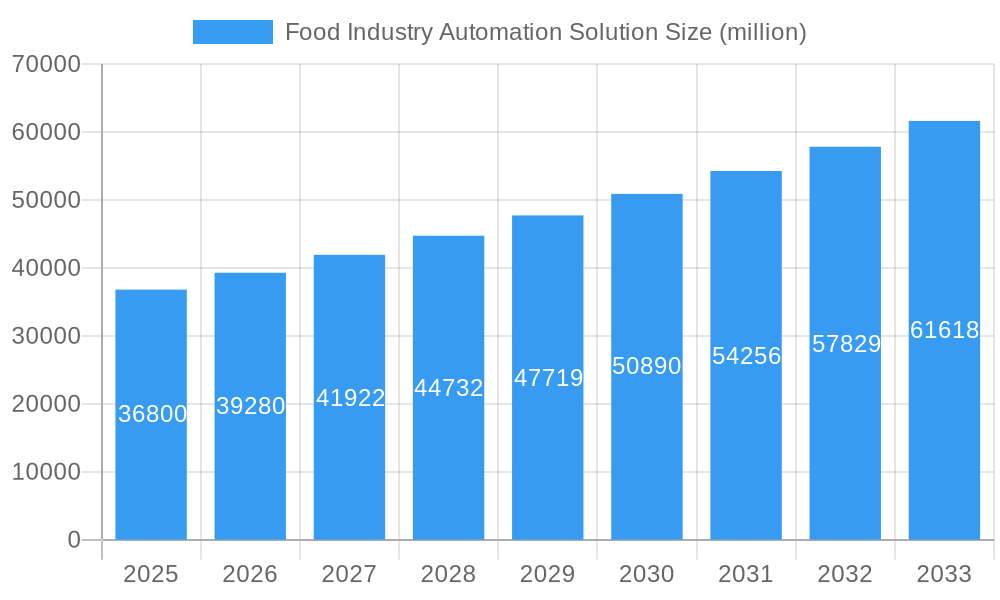

The global Food Industry Automation Solution market is projected for robust expansion, estimated at USD 36,800 million in 2025, and is expected to grow at a compelling Compound Annual Growth Rate (CAGR) of 6.7% through 2033. This significant growth is propelled by several key drivers. Increasing consumer demand for consistently high-quality food products, coupled with the need for enhanced food safety and traceability, is a primary catalyst. Automation solutions address these by improving process control, reducing human error, and ensuring compliance with stringent regulatory standards. Furthermore, the ongoing labor shortage across the food processing sector, particularly for repetitive or hazardous tasks, is pushing companies to invest in automated systems for improved efficiency and operational resilience. The drive for cost optimization through reduced waste, energy consumption, and increased throughput also plays a crucial role. Trends such as the adoption of advanced robotics, AI-powered quality inspection, and IoT-enabled smart factories are further shaping the market, enabling greater flexibility and data-driven decision-making.

Food Industry Automation Solution Market Size (In Billion)

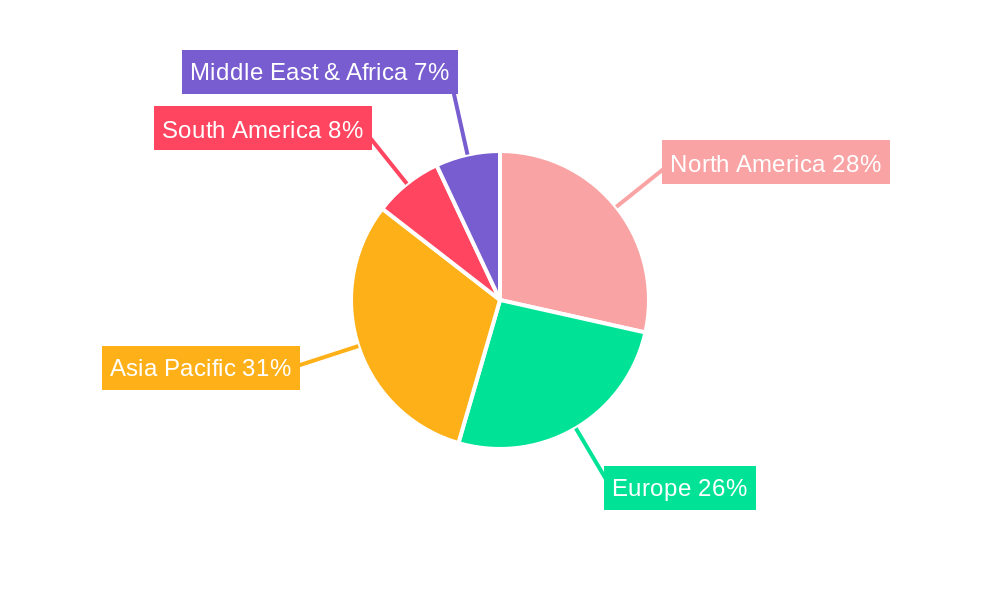

The market is segmented across various applications including Beverages, Dairy, Bakery, Fruits and Vegetables, Meat, Poultry and Seafood, and others, reflecting the pervasive nature of automation across the entire food value chain. By type, solutions encompass Production and Processing, Packaging, Quality Control, Sorting and Grading, and others, highlighting a comprehensive approach to optimizing food operations. While the market demonstrates strong growth potential, certain restraints, such as the high initial investment cost for advanced automation systems and the need for skilled labor to operate and maintain these technologies, need to be addressed. However, the long-term benefits of increased productivity, improved product consistency, and enhanced food safety are expected to outweigh these challenges. Key players like Siemens, Schneider Electric, GEA Group, Honeywell, and Fanuc are actively innovating and expanding their offerings to cater to the evolving needs of the food industry. The Asia Pacific region is anticipated to witness the fastest growth, driven by rapid industrialization and a growing food processing sector, while North America and Europe will continue to be significant markets.

Food Industry Automation Solution Company Market Share

Report Description: Global Food Industry Automation Solution Market: Trends, Opportunities, and Forecast (2019-2033)

This comprehensive report provides an in-depth analysis of the global Food Industry Automation Solution market, covering the study period from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033. This report is meticulously designed for industry professionals seeking to understand the current market landscape, identify growth opportunities, and strategize for future expansion. We delve into the intricate dynamics of the food and beverage sector's adoption of advanced automation technologies, including robotic systems, AI-powered quality control, and smart packaging solutions. The report offers critical insights into the evolving needs of the parent market – the broader food and beverage manufacturing industry – and its direct impact on the child market – the food industry automation solution sector. Our analysis is segmented by key applications such as Beverages, Dairy, Bakery, Fruits and Vegetables, and Meat, Poultry and Seafood, and by technology types including Production and Processing, Packaging, Quality Control, and Sorting and Grading.

Food Industry Automation Solution Market Dynamics & Structure

The Food Industry Automation Solution market is characterized by a moderately concentrated structure, with a few key players like Siemens, Schneider Electric, GEA Group, Honeywell, and ABB holding significant market shares. Technological innovation is a primary driver, fueled by advancements in robotics, artificial intelligence (AI), machine learning (ML), and the Industrial Internet of Things (IIoT). These technologies are crucial for enhancing efficiency, improving product quality, and ensuring food safety. Regulatory frameworks, particularly those related to food hygiene, traceability, and worker safety, also play a pivotal role in shaping automation adoption. For instance, stringent regulations in North America and Europe push manufacturers towards automated solutions for compliance. Competitive product substitutes, such as semi-automated systems or manual labor, are becoming less viable as the cost-effectiveness and efficiency benefits of full automation become more apparent. End-user demographics are shifting, with a growing demand for processed and packaged food products, necessitating higher production volumes and greater precision, thus accelerating automation demand. Mergers and acquisitions (M&A) trends indicate a strategic consolidation within the industry, with larger players acquiring innovative startups to expand their product portfolios and market reach. In 2023, there were an estimated 15 significant M&A deals valued at over $50 million each, aimed at strengthening technological capabilities and market presence. The barriers to innovation, such as the high initial investment costs and the need for skilled labor to operate and maintain complex automated systems, are being addressed through advancements in user-friendly interfaces and cloud-based support services.

- Market Concentration: Moderately concentrated, with leading players holding a combined market share of approximately 45%.

- Technological Innovation Drivers: AI, ML, Robotics, IIoT for enhanced efficiency and quality.

- Regulatory Frameworks: Stringent food safety and traceability regulations in developed economies.

- Competitive Product Substitutes: Semi-automated systems and manual labor are increasingly being outpaced.

- End-User Demographics: Growing demand for processed foods drives automation needs for higher output.

- M&A Trends: Strategic acquisitions to bolster technological capabilities and market expansion.

- Estimated 15 significant M&A deals in 2023, exceeding $50 million each.

- Innovation Barriers: High initial investment and need for skilled workforce.

Food Industry Automation Solution Growth Trends & Insights

The global Food Industry Automation Solution market is experiencing robust growth, projected to expand significantly over the forecast period. This expansion is underpinned by several critical trends including escalating labor costs, increasing demand for higher food safety standards, and the relentless pursuit of operational efficiency within the food and beverage sector. The market size, which stood at an estimated $32,500 million in 2024, is anticipated to reach an impressive $68,200 million by 2033, demonstrating a compound annual growth rate (CAGR) of approximately 8.5%. Adoption rates of automation technologies are on an upward trajectory, driven by the demonstrable return on investment through reduced waste, improved throughput, and enhanced product consistency. Technological disruptions, such as the integration of advanced robotics for intricate tasks like picking and packing, and the deployment of AI-powered vision systems for real-time quality control, are revolutionizing production lines. Consumer behavior shifts, including a preference for sustainably produced and traceable food products, are further compelling manufacturers to invest in automation solutions that can ensure transparency and reduce environmental impact. For instance, automation plays a crucial role in optimizing resource utilization in the bakery segment, leading to reduced energy consumption and ingredient wastage. Market penetration of advanced automation in emerging economies is expected to witness a significant surge, driven by government initiatives promoting industrial modernization and increasing disposable incomes. The increasing adoption of collaborative robots (cobots) in smaller food processing units is a notable trend, making automation more accessible and flexible. Furthermore, the growing focus on personalized nutrition and specialized dietary products necessitates flexible and adaptable automation systems, further fueling market growth. The integration of predictive maintenance algorithms powered by AI is also reducing downtime and optimizing the lifespan of automated machinery, contributing to overall cost savings and operational continuity. The demand for automated solutions in the meat, poultry, and seafood segment is particularly strong due to hygiene concerns and the need for high-volume processing. The report will analyze these dynamics in detail, providing quantitative metrics such as market penetration rates and CAGR projections for various sub-segments, enabling stakeholders to identify lucrative investment avenues.

Dominant Regions, Countries, or Segments in Food Industry Automation Solution

The North America region stands as a dominant force in the global Food Industry Automation Solution market, driven by a confluence of factors including strong economic policies supporting technological adoption, highly developed industrial infrastructure, and a consumer base with a high demand for processed and conveniently packaged food products. Within North America, the United States spearheads this dominance, boasting a significant market share attributed to its large food processing industry and continuous investment in research and development for automation technologies. The Beverages segment, within the Application category, emerges as a particularly strong growth driver across many regions due to the high volume production requirements and the need for precise filling, capping, and packaging operations. The Production and Processing segment, under the Type category, consistently holds the largest market share globally, as this is where the core efficiency gains from automation are realized, impacting every stage from raw material handling to final product preparation.

Key drivers for this dominance include:

- Economic Policies: Government incentives and tax breaks for manufacturing automation and technological upgrades in the US and Canada.

- Infrastructure: Advanced logistics and robust supply chains facilitating the deployment and maintenance of automation systems.

- Consumer Demand: High per capita consumption of processed foods and beverages, requiring large-scale, efficient production.

- Technological Advancement: Proactive adoption of cutting-edge automation technologies by leading food manufacturers.

- Labor Costs: Rising labor wages incentivize investment in robotic and automated solutions to maintain competitive pricing.

- Food Safety Regulations: Strict adherence to safety and quality standards necessitates precise and consistent automated processes.

The market share of the Production and Processing segment is estimated to be around 40% of the total food industry automation market, reflecting its foundational importance. The Beverages segment contributes significantly with an estimated 25% market share within the applications. The growth potential within these dominant segments is substantial, driven by the ongoing need for greater throughput, reduced waste, and enhanced product quality to meet evolving consumer expectations and competitive pressures. Emerging economies in Asia-Pacific are also showing rapid growth, but North America's established infrastructure and continuous innovation currently solidify its leading position. The adoption of Industry 4.0 principles, including AI and IoT, further propels the dominance of these key segments and regions.

Food Industry Automation Solution Product Landscape

The product landscape for Food Industry Automation Solutions is characterized by rapid innovation focused on enhancing efficiency, precision, and safety. Robotic systems, including articulated robots and collaborative robots (cobots), are increasingly being deployed for intricate tasks such as high-speed pick-and-place, palletizing, and intricate assembly in bakery and confectionery lines. AI-powered vision inspection systems are revolutionizing quality control, enabling real-time defect detection and sorting with unparalleled accuracy, reducing product recalls and improving consistency. Smart sensors and IIoT devices are integrating seamlessly with existing machinery, providing real-time data for process optimization, predictive maintenance, and enhanced traceability. Automated packaging solutions, such as intelligent filling machines and advanced pallet wrappers, are crucial for meeting the growing demand for customized and sustainable packaging. Unique selling propositions lie in solutions that offer flexibility, scalability, and seamless integration with enterprise resource planning (ERP) systems. For example, advanced robotic arms designed for high-speed dairy packaging can achieve over 120 cycles per minute, while AI vision systems can identify minute imperfections in fruits and vegetables with a success rate of 99.8%.

Key Drivers, Barriers & Challenges in Food Industry Automation Solution

Key Drivers:

The food industry automation solution market is propelled by several significant drivers. Rising labor costs are a primary catalyst, compelling manufacturers to seek automated alternatives for enhanced cost-effectiveness. Increasing demand for food safety and quality is paramount; automation ensures consistent processes and reduces human error, thereby minimizing contamination risks. Growing consumer demand for processed and convenience foods necessitates higher production volumes and faster turnaround times, which automation effectively addresses. Furthermore, technological advancements in robotics, AI, and IoT are continuously offering more sophisticated and affordable solutions, making automation accessible to a wider range of food businesses. Government initiatives promoting industrial modernization and smart manufacturing also act as strong accelerators.

Key Barriers & Challenges:

Despite the growth, several challenges impede market expansion. The high initial investment cost associated with advanced automation systems remains a significant barrier, particularly for small and medium-sized enterprises (SMEs). The need for skilled labor to operate, maintain, and program complex automation machinery presents a talent gap challenge. Integration complexities with existing legacy systems can also pose technical hurdles. Supply chain disruptions, as experienced in recent years, can impact the availability of automation components. Regulatory hurdles and evolving food safety standards require continuous adaptation of automation solutions. Competitive pressures from lower-cost regions or alternative production methods also present ongoing challenges, impacting the speed of adoption. The quantified impact of labor shortages in the US food processing sector alone is estimated to cost the industry over $1 billion annually, highlighting the economic imperative for automation.

Emerging Opportunities in Food Industry Automation Solution

Emerging opportunities in the Food Industry Automation Solution sector are largely driven by evolving consumer preferences and technological breakthroughs. The growing demand for personalized nutrition and specialized dietary products creates a market for highly flexible and adaptable automation systems capable of handling smaller batch sizes and diverse ingredient combinations, particularly in the bakery and dairy segments. Sustainable and eco-friendly packaging automation presents a significant growth area, with increased adoption of solutions that minimize waste and utilize recyclable materials. The application of AI and ML in predictive maintenance and process optimization offers substantial opportunities for reducing downtime and enhancing operational efficiency across all food segments. Furthermore, the expansion of automation solutions for the "farm-to-fork" traceability and safety monitoring, leveraging blockchain and IoT technologies, is gaining traction. Untapped markets in developing regions offer immense potential as these economies increasingly focus on modernizing their food processing capabilities.

Growth Accelerators in the Food Industry Automation Solution Industry

Several key catalysts are accelerating the growth of the Food Industry Automation Solution industry. Technological breakthroughs in areas such as advanced robotics, including dexterous manipulation and human-robot collaboration, are enabling automation of previously impossible tasks. Strategic partnerships between automation providers and food manufacturers, as well as collaborations with research institutions, foster innovation and accelerate the development and deployment of new solutions. Market expansion strategies, particularly targeting emerging economies with growing food processing needs, are opening up new revenue streams. The increasing focus on data analytics and AI-driven insights is transforming automation from simple task execution to intelligent process management, leading to significant operational improvements and driving further investment. The drive for increased shelf-life and reduced spoilage through precisely controlled automated environments also acts as a significant growth accelerator, particularly for fruits and vegetables and meat, poultry, and seafood.

Key Players Shaping the Food Industry Automation Solution Market

- Siemens

- Schneider Electric

- GEA Group

- Honeywell

- Fanuc

- JBT

- Yaskawa Electric

- Kawasaki Heavy Industries

- Emerson Electric

- ABB

- Rockwell Automation

- Mitsubishi Electric

- Rheon Automatic Machinery

- JR Automation

- Omron Corporation

- KUKA AG

- Yokogawa Electric

- Staubli International AG

Notable Milestones in Food Industry Automation Solution Sector

- 2019: Introduction of advanced AI-powered quality control systems capable of real-time defect detection with over 99% accuracy, significantly reducing product waste in the fruits and vegetables segment.

- 2020: Increased adoption of collaborative robots (cobots) in bakery and confectionery lines, enabling smaller food manufacturers to automate intricate tasks with enhanced safety and flexibility.

- 2021: Major automation providers launch integrated IIoT platforms, facilitating seamless data exchange and remote monitoring for enhanced operational efficiency across the food production chain.

- 2022: Significant advancements in robotic palletizing and depalletizing solutions for the meat, poultry, and seafood industry, addressing labor shortages and improving hygiene standards.

- 2023: Expansion of automated packaging solutions, including sustainable and smart packaging technologies, driven by increasing consumer demand for eco-friendly and traceable products.

- 2024: Emergence of digital twin technologies for simulating and optimizing food production lines, leading to reduced development times and improved process performance.

- Early 2025: Introduction of new generation of vision systems with enhanced spectral analysis capabilities for deeper quality assessment in dairy and beverage production.

In-Depth Food Industry Automation Solution Market Outlook

The future outlook for the Food Industry Automation Solution market is exceptionally robust, driven by an unwavering commitment to efficiency, quality, and safety. Growth accelerators, including ongoing technological breakthroughs in AI, robotics, and the IIoT, will continue to fuel innovation and create new application possibilities. Strategic partnerships and collaborations will remain vital for bringing advanced solutions to market swiftly. The expansion into emerging economies, coupled with a focus on smart manufacturing and Industry 4.0 principles, presents significant untapped potential. The market is poised for sustained expansion as food manufacturers globally recognize automation not just as a cost-saving measure, but as a critical enabler of competitiveness, sustainability, and consumer satisfaction in an ever-evolving food landscape. Future strategic opportunities lie in developing highly customized, scalable, and data-driven automation solutions tailored to specific segment needs and regulatory environments.

Food Industry Automation Solution Segmentation

-

1. Application

- 1.1. Beverages

- 1.2. Dairy

- 1.3. Bakery

- 1.4. Fruits and Vegetables

- 1.5. Meat, Poultry and Seafood

- 1.6. Others

-

2. Type

- 2.1. Production and Processing

- 2.2. Packaging

- 2.3. Quality Control

- 2.4. Sorting and Grading

- 2.5. Others

Food Industry Automation Solution Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Food Industry Automation Solution Regional Market Share

Geographic Coverage of Food Industry Automation Solution

Food Industry Automation Solution REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Food Industry Automation Solution Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Beverages

- 5.1.2. Dairy

- 5.1.3. Bakery

- 5.1.4. Fruits and Vegetables

- 5.1.5. Meat, Poultry and Seafood

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Production and Processing

- 5.2.2. Packaging

- 5.2.3. Quality Control

- 5.2.4. Sorting and Grading

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Food Industry Automation Solution Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Beverages

- 6.1.2. Dairy

- 6.1.3. Bakery

- 6.1.4. Fruits and Vegetables

- 6.1.5. Meat, Poultry and Seafood

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Production and Processing

- 6.2.2. Packaging

- 6.2.3. Quality Control

- 6.2.4. Sorting and Grading

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Food Industry Automation Solution Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Beverages

- 7.1.2. Dairy

- 7.1.3. Bakery

- 7.1.4. Fruits and Vegetables

- 7.1.5. Meat, Poultry and Seafood

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Production and Processing

- 7.2.2. Packaging

- 7.2.3. Quality Control

- 7.2.4. Sorting and Grading

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Food Industry Automation Solution Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Beverages

- 8.1.2. Dairy

- 8.1.3. Bakery

- 8.1.4. Fruits and Vegetables

- 8.1.5. Meat, Poultry and Seafood

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Production and Processing

- 8.2.2. Packaging

- 8.2.3. Quality Control

- 8.2.4. Sorting and Grading

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Food Industry Automation Solution Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Beverages

- 9.1.2. Dairy

- 9.1.3. Bakery

- 9.1.4. Fruits and Vegetables

- 9.1.5. Meat, Poultry and Seafood

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Production and Processing

- 9.2.2. Packaging

- 9.2.3. Quality Control

- 9.2.4. Sorting and Grading

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Food Industry Automation Solution Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Beverages

- 10.1.2. Dairy

- 10.1.3. Bakery

- 10.1.4. Fruits and Vegetables

- 10.1.5. Meat, Poultry and Seafood

- 10.1.6. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Production and Processing

- 10.2.2. Packaging

- 10.2.3. Quality Control

- 10.2.4. Sorting and Grading

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Siemens

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Schneider Electric

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 GEA Group

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Honeywell

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Fanuc

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 JBT

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Yaskawa Electric

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Kawasaki Heavy Industries

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Emerson Electric

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 ABB

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Rockwell Automation

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Mitsubishi Electric

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Rheon Automatic Machinery

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 JR Automation

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Omron Corporation

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 KUKA AG

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Yokogawa Electric

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Staubli International AG

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.1 Siemens

List of Figures

- Figure 1: Global Food Industry Automation Solution Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Food Industry Automation Solution Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Food Industry Automation Solution Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Food Industry Automation Solution Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Food Industry Automation Solution Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Food Industry Automation Solution Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Food Industry Automation Solution Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Food Industry Automation Solution Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Food Industry Automation Solution Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Food Industry Automation Solution Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Food Industry Automation Solution Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Food Industry Automation Solution Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Food Industry Automation Solution Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Food Industry Automation Solution Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Food Industry Automation Solution Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Food Industry Automation Solution Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Food Industry Automation Solution Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Food Industry Automation Solution Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Food Industry Automation Solution Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Food Industry Automation Solution Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Food Industry Automation Solution Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Food Industry Automation Solution Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Food Industry Automation Solution Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Food Industry Automation Solution Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Food Industry Automation Solution Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Food Industry Automation Solution Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Food Industry Automation Solution Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Food Industry Automation Solution Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Food Industry Automation Solution Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Food Industry Automation Solution Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Food Industry Automation Solution Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Food Industry Automation Solution Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Food Industry Automation Solution Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Food Industry Automation Solution Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Food Industry Automation Solution Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Food Industry Automation Solution Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Food Industry Automation Solution Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Food Industry Automation Solution Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Food Industry Automation Solution Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Food Industry Automation Solution Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Food Industry Automation Solution Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Food Industry Automation Solution Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Food Industry Automation Solution Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Food Industry Automation Solution Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Food Industry Automation Solution Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Food Industry Automation Solution Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Food Industry Automation Solution Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Food Industry Automation Solution Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Food Industry Automation Solution Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Food Industry Automation Solution Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Food Industry Automation Solution?

The projected CAGR is approximately 7.4%.

2. Which companies are prominent players in the Food Industry Automation Solution?

Key companies in the market include Siemens, Schneider Electric, GEA Group, Honeywell, Fanuc, JBT, Yaskawa Electric, Kawasaki Heavy Industries, Emerson Electric, ABB, Rockwell Automation, Mitsubishi Electric, Rheon Automatic Machinery, JR Automation, Omron Corporation, KUKA AG, Yokogawa Electric, Staubli International AG.

3. What are the main segments of the Food Industry Automation Solution?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Food Industry Automation Solution," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Food Industry Automation Solution report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Food Industry Automation Solution?

To stay informed about further developments, trends, and reports in the Food Industry Automation Solution, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence