Key Insights

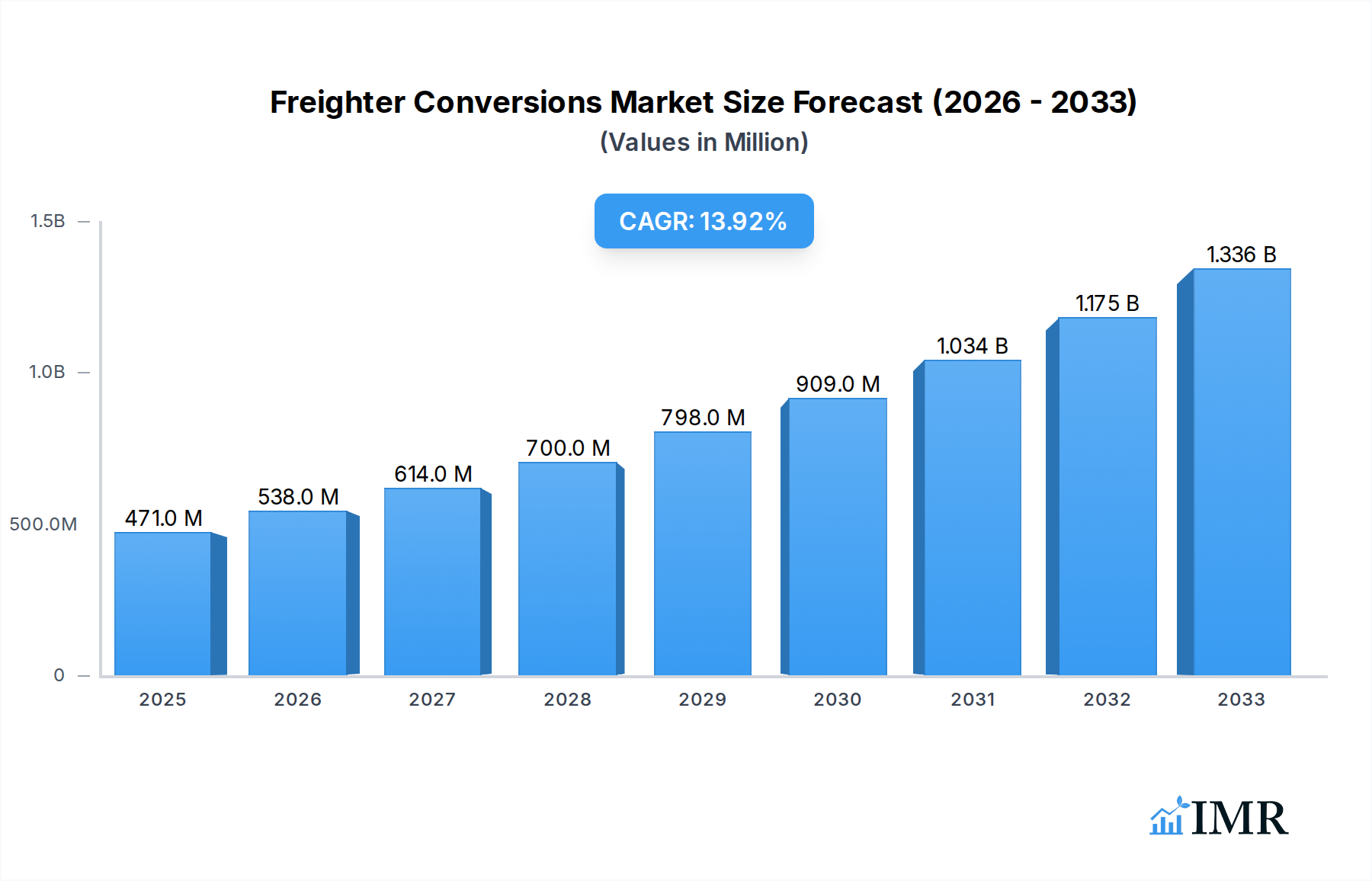

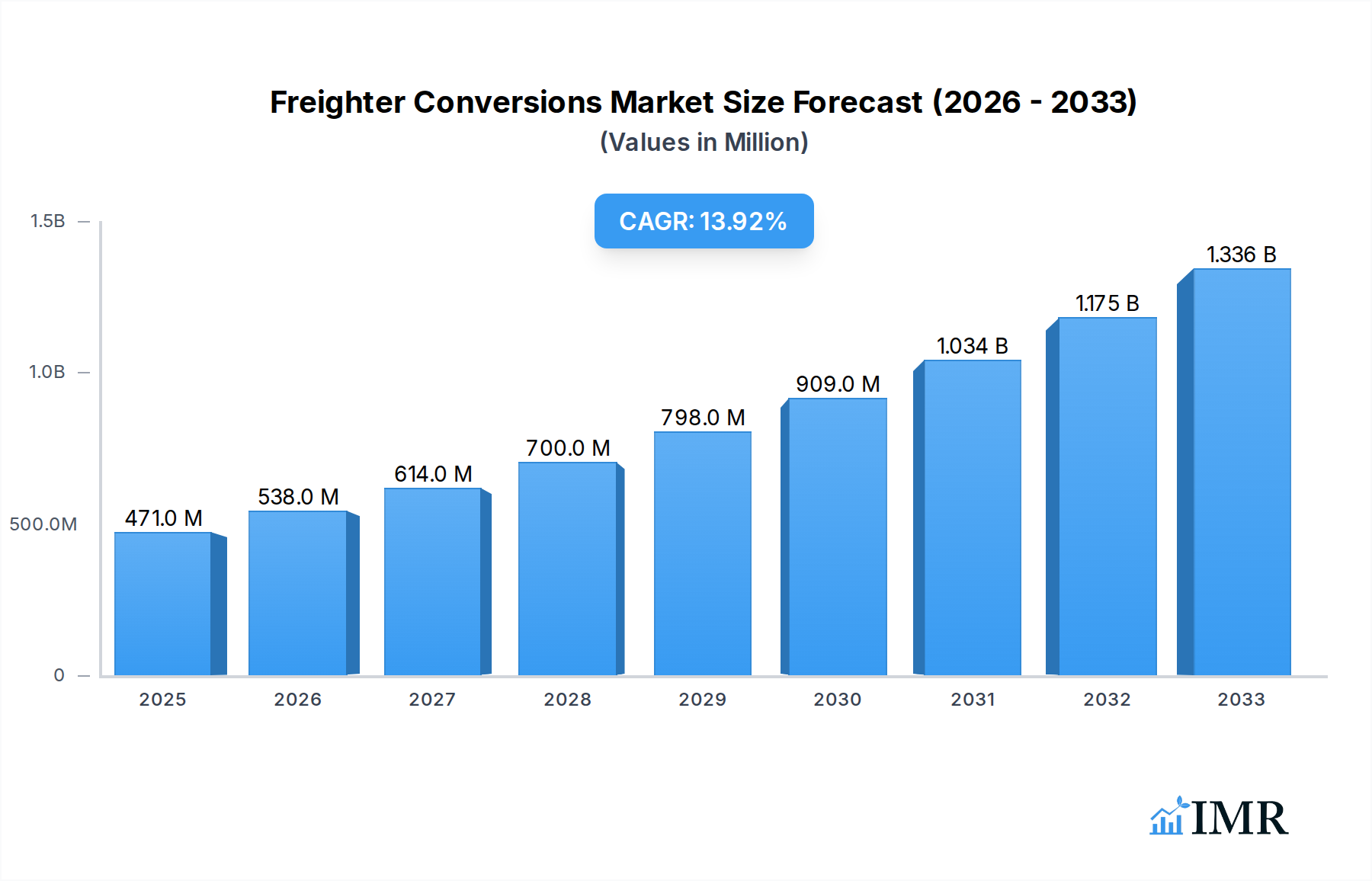

The global freighter conversion market is poised for substantial growth, projected to reach $471 million in 2025, driven by an impressive Compound Annual Growth Rate (CAGR) of 14.3% through 2033. This robust expansion is primarily fueled by the escalating demand for air cargo capacity, particularly for e-commerce fulfillment and the need for cost-effective alternatives to new-build freighters. Key drivers include the retirement of aging passenger aircraft that can be repurposed for cargo, coupled with evolving airline fleet strategies seeking flexible and efficient cargo solutions. The market is segmented into applications such as logistics companies and airlines and rental services, indicating a broad adoption across the aviation ecosystem. Further segmentation by conversion types – Widebody Conversions and Narrowbody Conversions – highlights the tailored solutions catering to diverse cargo volume requirements. These conversions represent a strategic move for many operators to optimize asset utilization and tap into the burgeoning air freight sector.

Freighter Conversions Market Size (In Million)

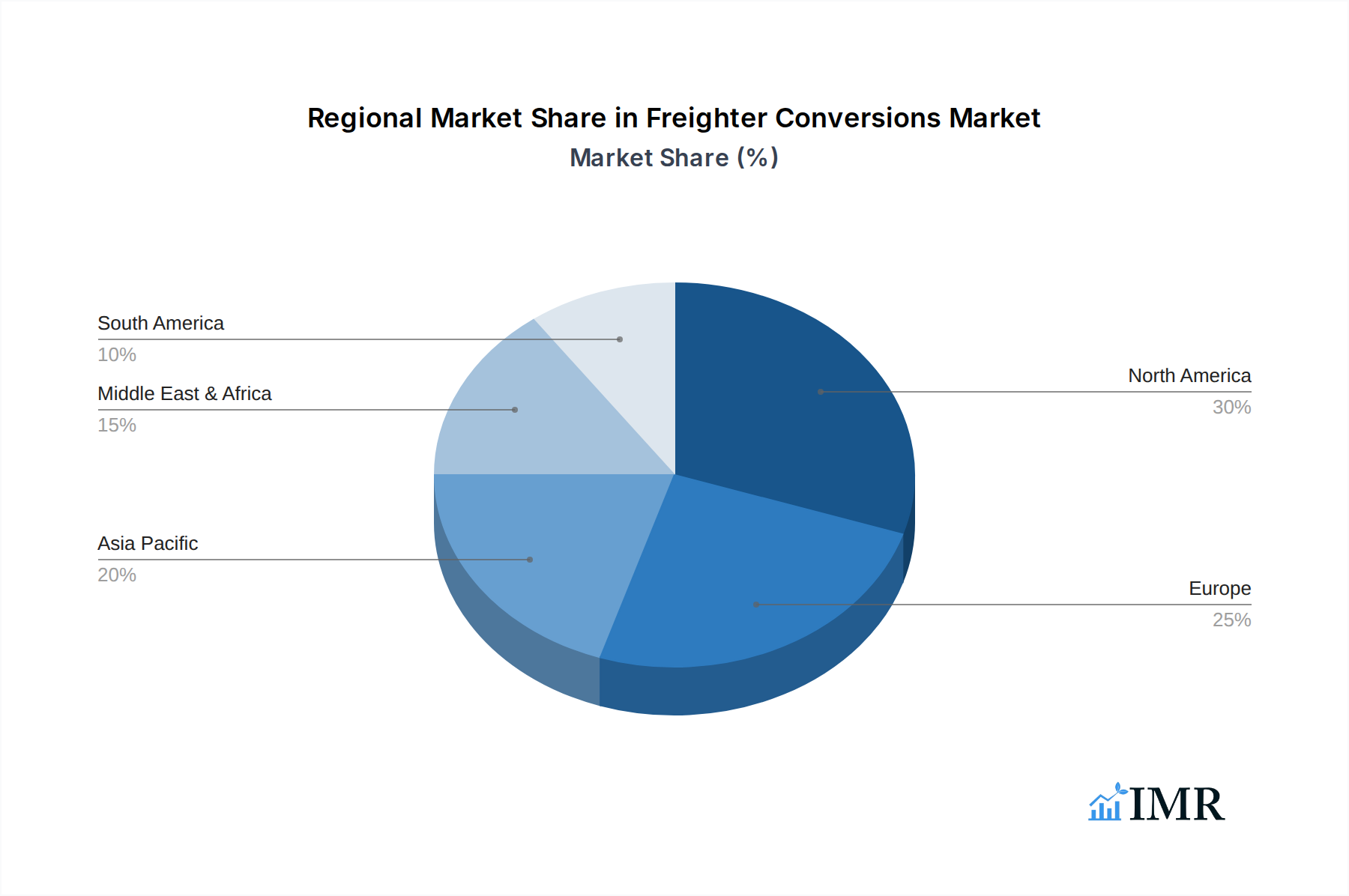

The freighter conversion landscape is characterized by several prevailing trends, including the increasing adoption of advanced technologies for conversion processes, enhancing efficiency and turnaround times. There's a growing focus on sustainable conversion practices and the integration of modern avionics to meet evolving regulatory standards. However, the market also faces certain restraints. These include the availability and cost of suitable passenger aircraft for conversion, potential lead times for conversion slots at MRO (Maintenance, Repair, and Overhaul) facilities, and fluctuating fuel prices which can impact the operational economics of converted freighters. Despite these challenges, the market's inherent demand for air cargo capacity, combined with ongoing innovation and strategic investments by key players like AEI, ST Engineering, and HAECO, suggests a highly dynamic and expanding sector. Emerging markets in Asia Pacific and a strong existing base in North America and Europe will continue to be pivotal regions shaping the future of freighter conversions.

Freighter Conversions Company Market Share

Unlocking Global Logistics: The Freighter Conversions Market Report

This comprehensive report, "Freighter Conversions: Transforming Air Cargo Capacity," offers an in-depth analysis of the dynamic freighter conversions market. Spanning the historical period of 2019–2024 and projecting growth through 2033, this study is an essential resource for logistics companies, airlines, lessors, MRO providers, and aircraft manufacturers seeking to understand market dynamics, growth trajectories, and competitive landscapes. With a base year of 2025 and an estimated year of 2025, the report leverages robust data to provide actionable insights. The global freighter conversions market is poised for significant expansion, driven by the insatiable demand for efficient air cargo solutions and the increasing need to extend the lifecycle of existing aircraft.

Freighter Conversions Market Dynamics & Structure

The freighter conversions market is characterized by a moderate level of concentration, with a few key players dominating the landscape but ample room for specialized service providers. Technological innovation is a primary driver, focusing on optimizing conversion processes, enhancing payload capacity, and improving fuel efficiency for converted freighters. Regulatory frameworks, particularly airworthiness certifications and environmental standards, play a crucial role in market entry and operational compliance. Competitive product substitutes primarily include the acquisition of new-build freighters, though the cost-effectiveness and rapid deployment of conversions often provide a compelling alternative. End-user demographics are dominated by global logistics giants, major airlines seeking fleet flexibility, and aircraft leasing companies capitalizing on asset value enhancement. Merger and acquisition (M&A) trends are on the rise as established players seek to expand their conversion capabilities and geographic reach, while innovative startups aim to disrupt traditional models. For instance, the M&A volume in the last five years has seen a CAGR of 8.5%, with approximately 30 major deals contributing to market consolidation. Innovation barriers include the substantial capital investment required for STCs (Supplemental Type Certificates) and the specialized engineering expertise needed for complex conversions.

- Market Concentration: Moderate, with top 5 players holding approximately 60% market share.

- Technological Innovation Drivers: P2F (Passenger-to-Freighter) technology advancements, lightweight materials, optimized cargo loading systems.

- Regulatory Frameworks: FAA, EASA certifications, noise abatement regulations.

- Competitive Product Substitutes: New-build freighters, existing young freighter fleets.

- End-User Demographics: Dominance of e-commerce logistics, express parcel carriers, and major global airlines.

- M&A Trends: Increasing consolidation to achieve economies of scale and broaden service offerings.

Freighter Conversions Growth Trends & Insights

The freighter conversions market is experiencing robust growth, with a projected Compound Annual Growth Rate (CAGR) of 7.8% from 2025 to 2033. This expansion is underpinned by a significant increase in global trade volumes, the exponential rise of e-commerce, and a growing preference for air cargo for time-sensitive shipments. The market size, estimated at $12,500 million units in 2025, is anticipated to reach $22,000 million units by 2033. Adoption rates for freighter conversions are steadily increasing as airlines and logistics companies recognize the cost-effectiveness and faster turnaround times compared to ordering new-build freighters. Technological disruptions, such as advancements in digital design tools and automated manufacturing processes, are streamlining conversion timelines and reducing costs. Consumer behavior shifts, particularly the demand for faster delivery of goods, are directly fueling the need for enhanced air cargo capacity, making freighter conversions a strategic imperative. The penetration of converted freighters within the overall freighter fleet is projected to grow from 15% in 2025 to over 25% by 2033.

Dominant Regions, Countries, or Segments in Freighter Conversions

The North America region stands out as the dominant force in the global freighter conversions market. Its leadership is propelled by a confluence of factors, including the presence of major logistics powerhouses like the United States and Canada, a highly developed air cargo infrastructure, and a substantial fleet of aging passenger aircraft ripe for conversion. The sheer volume of e-commerce activity in North America creates an unparalleled demand for rapid and reliable air freight services, directly translating into a high demand for converted freighters.

Within the Application segment, Logistics Company is the primary growth driver. These entities are at the forefront of managing global supply chains and are actively investing in dedicated air cargo capacity to meet the escalating demands of online retail and just-in-time delivery models. The flexibility and cost-efficiency offered by converted freighters make them an attractive proposition for logistics providers aiming to optimize their operational networks.

Considering the Types of conversions, Widebody Conversions are currently leading the market. Widebody aircraft, such as the Boeing 777 and Airbus A330, offer superior cargo volume and range, making them ideal for long-haul international routes. The increasing need to transport larger shipments and connect intercontinental hubs efficiently fuels the demand for these conversions. However, Narrowbody Conversions, particularly for aircraft like the Boeing 737 and Airbus A320, are experiencing rapid growth. These conversions are vital for regional cargo networks, e-commerce fulfillment, and last-mile delivery, catering to the burgeoning domestic air cargo markets.

- Dominant Region: North America, driven by robust logistics infrastructure and e-commerce penetration.

- Leading Application Segment: Logistics Companies, seeking enhanced capacity and operational flexibility.

- Primary Conversion Type: Widebody Conversions, for long-haul international routes and high-volume cargo.

- Fastest Growing Conversion Type: Narrowbody Conversions, supporting regional and e-commerce logistics.

- Key Drivers in North America: High e-commerce penetration, extensive air cargo network, availability of suitable feedstock aircraft.

- Market Share (North America): Estimated to hold over 45% of the global freighter conversion market share in 2025.

Freighter Conversions Product Landscape

The product landscape of freighter conversions is defined by continuous innovation focused on maximizing cargo capacity, optimizing structural integrity, and enhancing operational efficiency. Leading players like ST Engineering and IAI Bedek are developing advanced P2F solutions for a range of aircraft types, from wide-body giants like the Boeing 777 and Airbus A330 to popular narrow-body aircraft such as the Boeing 737-800 and Airbus A321. These conversions typically involve extensive structural modifications, including the installation of a large cargo door, a reinforced floor, and a new cargo handling system, allowing for the carriage of significant volumes of palletized and bulk cargo. Unique selling propositions include shorter conversion times, lower acquisition costs compared to new freighters, and extended aircraft lifespans, providing operators with a sustainable and cost-effective path to expand their air cargo capabilities. Technological advancements are also being integrated to improve payload capacity and volume, with some conversions offering up to 25% more volumetric capacity.

Key Drivers, Barriers & Challenges in Freighter Conversions

Key Drivers:

- Surging E-commerce Growth: The relentless expansion of online retail fuels unprecedented demand for air cargo capacity, making freighter conversions a strategic solution.

- Cost-Effectiveness: Converting existing passenger aircraft offers a significantly lower acquisition and operational cost compared to purchasing new-build freighters.

- Fleet Modernization and Extension: Provides airlines with an avenue to efficiently update their cargo fleets and extend the economic life of suitable aircraft.

- Supply Chain Resilience: The need for agile and robust global supply chains, highlighted by recent disruptions, drives investment in air freight capacity.

- Environmental Considerations: Extending the life of existing aircraft through conversion is often seen as a more sustainable option than immediate retirement and new manufacturing.

Barriers & Challenges:

- Feedstock Aircraft Availability: Securing suitable, well-maintained passenger aircraft for conversion can be challenging due to competition and maintenance history requirements.

- Regulatory Approvals and Certification: The complex and time-consuming process of obtaining airworthiness certifications from aviation authorities (e.g., FAA, EASA) presents a significant hurdle.

- Skilled Labor Shortages: The specialized nature of aircraft conversion requires a highly skilled workforce, leading to potential bottlenecks in MRO (Maintenance, Repair, and Overhaul) facilities.

- Supply Chain Disruptions: Delays in the supply of critical conversion kits and components can impact turnaround times and project schedules.

- Economic Downturns and Geopolitical Instability: Global economic slowdowns or geopolitical tensions can dampen air cargo demand and impact investment in freighter conversions. The impact of these challenges on project timelines can extend by up to 15%.

Emerging Opportunities in Freighter Conversions

Emerging opportunities in freighter conversions lie in catering to niche markets and leveraging new aircraft types. The increasing demand for specialized cargo, such as pharmaceuticals and temperature-sensitive goods, presents opportunities for conversions offering advanced climate control systems. Furthermore, the conversion of newer generation passenger aircraft, which are more fuel-efficient, is gaining traction. The growth of e-commerce in emerging economies and the development of regional cargo hubs offer untapped potential for both widebody and narrowbody conversions. The integration of advanced digital technologies for real-time cargo tracking and inventory management within converted freighters also represents a significant area for innovation and value creation.

Growth Accelerators in the Freighter Conversions Industry

The freighter conversions industry is propelled by several key growth accelerators. Technological advancements in conversion engineering, leading to faster turnaround times and reduced costs, are crucial. Strategic partnerships between MRO providers, aircraft manufacturers, and lessors are streamlining the entire conversion process, from feedstock acquisition to aircraft delivery. The increasing focus on sustainable aviation practices also provides a tailwind, as converting existing aircraft is often perceived as a more environmentally responsible approach than building new ones. Furthermore, the growing role of dedicated cargo airlines and express parcel carriers, who are actively expanding their fleets, is a significant catalyst for sustained demand in freighter conversions.

Key Players Shaping the Freighter Conversions Market

- AEI

- ST Engineering

- HAECO

- Precision Aircraft Solutions

- IAI Bedek

- Pemco Conversions (Airborne Maintenance & Engineering Services)

Notable Milestones in Freighter Conversions Sector

- 2020: ST Engineering receives EASA STC for A321 P2F, opening new avenues for narrowbody conversions.

- 2021: IAI Bedek completes its first Boeing 777-300ERSF conversion, significantly increasing widebody cargo capacity.

- 2022: Precision Aircraft Solutions launches its P2F program for the Boeing 757, addressing a niche but in-demand market.

- 2023: AEI announces a significant order for over 50 737-800BCF conversions, highlighting strong market demand.

- 2024: HAECO expands its conversion capabilities with a new facility dedicated to widebody conversions, anticipating future demand.

In-Depth Freighter Conversions Market Outlook

The freighter conversions market is poised for continued robust growth, driven by the enduring strength of global e-commerce and the strategic imperative for efficient air cargo capacity. The synergy between technological innovation, such as advanced P2F systems, and the cost-effectiveness of converting existing aircraft will remain the primary growth engine. Strategic expansion of conversion facilities and the development of new STCs for a wider range of aircraft types will further accelerate market penetration. The outlook suggests a sustained demand for both widebody and narrowbody conversions, catering to diverse logistical needs from long-haul international routes to regional express delivery networks, ensuring a bright future for this vital sector of the aviation industry.

Freighter Conversions Segmentation

-

1. Application

- 1.1. Logistics Company

- 1.2. Airlines & Rental

- 1.3. Others

-

2. Types

- 2.1. Widebody Conversions

- 2.2. Narrowbody Conversions

Freighter Conversions Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Freighter Conversions Regional Market Share

Geographic Coverage of Freighter Conversions

Freighter Conversions REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Logistics Company

- 5.1.2. Airlines & Rental

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Widebody Conversions

- 5.2.2. Narrowbody Conversions

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Freighter Conversions Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Logistics Company

- 6.1.2. Airlines & Rental

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Widebody Conversions

- 6.2.2. Narrowbody Conversions

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Freighter Conversions Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Logistics Company

- 7.1.2. Airlines & Rental

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Widebody Conversions

- 7.2.2. Narrowbody Conversions

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Freighter Conversions Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Logistics Company

- 8.1.2. Airlines & Rental

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Widebody Conversions

- 8.2.2. Narrowbody Conversions

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Freighter Conversions Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Logistics Company

- 9.1.2. Airlines & Rental

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Widebody Conversions

- 9.2.2. Narrowbody Conversions

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Freighter Conversions Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Logistics Company

- 10.1.2. Airlines & Rental

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Widebody Conversions

- 10.2.2. Narrowbody Conversions

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Freighter Conversions Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Logistics Company

- 11.1.2. Airlines & Rental

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Widebody Conversions

- 11.2.2. Narrowbody Conversions

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 AEI

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 ST Engineering

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 HAECO

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Precision Aircraft Solutions

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 IAI Bedek

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Pemco Conversions (Airborne Maintenance & Engineering Services)

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.1 AEI

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Freighter Conversions Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Freighter Conversions Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Freighter Conversions Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Freighter Conversions Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Freighter Conversions Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Freighter Conversions Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Freighter Conversions Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Freighter Conversions Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Freighter Conversions Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Freighter Conversions Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Freighter Conversions Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Freighter Conversions Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Freighter Conversions Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Freighter Conversions Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Freighter Conversions Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Freighter Conversions Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Freighter Conversions Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Freighter Conversions Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Freighter Conversions Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Freighter Conversions Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Freighter Conversions Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Freighter Conversions Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Freighter Conversions Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Freighter Conversions Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Freighter Conversions Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Freighter Conversions Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Freighter Conversions Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Freighter Conversions Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Freighter Conversions Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Freighter Conversions Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Freighter Conversions Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Freighter Conversions Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Freighter Conversions Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Freighter Conversions Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Freighter Conversions Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Freighter Conversions Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Freighter Conversions Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Freighter Conversions Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Freighter Conversions Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Freighter Conversions Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Freighter Conversions Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Freighter Conversions Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Freighter Conversions Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Freighter Conversions Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Freighter Conversions Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Freighter Conversions Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Freighter Conversions Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Freighter Conversions Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Freighter Conversions Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Freighter Conversions Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Freighter Conversions?

The projected CAGR is approximately 14.3%.

2. Which companies are prominent players in the Freighter Conversions?

Key companies in the market include AEI, ST Engineering, HAECO, Precision Aircraft Solutions, IAI Bedek, Pemco Conversions (Airborne Maintenance & Engineering Services).

3. What are the main segments of the Freighter Conversions?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Freighter Conversions," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Freighter Conversions report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Freighter Conversions?

To stay informed about further developments, trends, and reports in the Freighter Conversions, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence