Key Insights

The global market for Liquid Cooled DC Chargers is poised for substantial growth, projected to reach $13.95 billion by 2025, with a compelling Compound Annual Growth Rate (CAGR) of 13.23% through 2033. This expansion is driven by the accelerating adoption of electric vehicles (EVs), coupled with the increasing demand for rapid charging solutions. Supportive government initiatives and advancements in charging technology further bolster market momentum.

Liquid Cooled DC Charger Market Size (In Billion)

Key market players, including SINBON, Phoenix Contact, and Teison Energy, are actively innovating and collaborating. While fixed charging stations remain prevalent, mobile liquid-cooled DC chargers are emerging as a flexible alternative. Asia Pacific, led by China, is anticipated to dominate the market, followed by North America and Europe. Ongoing research and development are addressing challenges related to system costs and standardization.

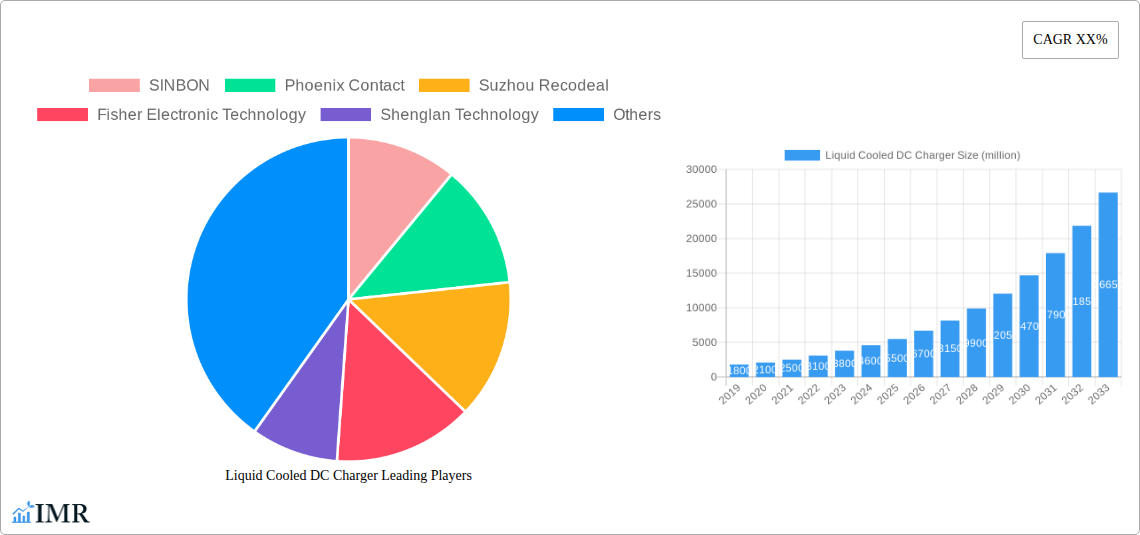

Liquid Cooled DC Charger Company Market Share

This report offers comprehensive analysis and forecasts for the Liquid Cooled DC Charger market from 2019 to 2033, with a base year of 2025. It targets EV charging infrastructure professionals, including manufacturers, suppliers, investors, and policymakers, utilizing high-traffic keywords for optimal search engine visibility.

The market analysis includes the Electric Vehicle Charging Infrastructure (parent market) and Liquid Cooled DC Chargers (child market). All quantitative data is presented in billions.

Liquid Cooled DC Charger Market Dynamics & Structure

The Liquid Cooled DC Charger market exhibits a moderately concentrated structure, with key players like SINBON, Phoenix Contact, and Suzhou Recodeal holding significant shares. Technological innovation is a primary driver, fueled by the increasing demand for faster charging solutions for Pure Electric Vehicles (PEVs) and Hybrid Electric Vehicles (HEVs). Emerging industry standards and government incentives for EV adoption are shaping regulatory frameworks, pushing for interoperability and safety. Competitive product substitutes, primarily air-cooled chargers, are gradually being overshadowed by liquid-cooled solutions due to their superior thermal management capabilities, enabling higher power output and reliability.

- Market Concentration: The top five players are estimated to hold approximately 55% of the market share by the end of 2025.

- Technological Innovation Drivers: Focus on higher power delivery (e.g., 350kW and above), improved efficiency, and enhanced cooling system reliability.

- Regulatory Frameworks: Increasing government mandates for charging infrastructure deployment and emission reduction targets directly influence market growth.

- Competitive Product Substitutes: Air-cooled chargers are still prevalent in lower power segments but face limitations in high-power applications.

- End-User Demographics: Growing adoption of PEVs and HEVs by both individual consumers and commercial fleets drives demand.

- M&A Trends: Expect an increase in strategic partnerships and acquisitions as larger players seek to consolidate their market positions and acquire advanced cooling technologies. For instance, the acquisition of specialized thermal management component suppliers by major charger manufacturers is anticipated.

Liquid Cooled DC Charger Growth Trends & Insights

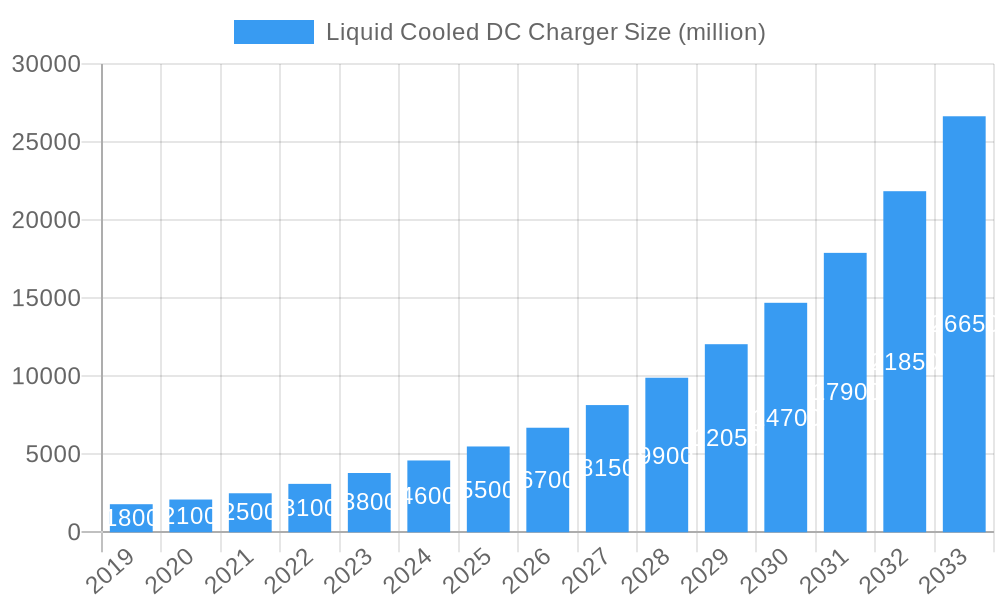

The Liquid Cooled DC Charger market is projected for substantial growth, driven by the accelerating global adoption of electric vehicles. By the end of 2025, the market size is estimated to reach approximately $5,500 million units, with a projected Compound Annual Growth Rate (CAGR) of around 28% during the forecast period of 2025–2033. This impressive growth is underpinned by a confluence of factors, including advancements in battery technology, the urgent need for sustainable transportation solutions, and significant investments in EV charging infrastructure by both public and private entities.

The adoption rate of liquid-cooled DC chargers is rapidly increasing, especially in regions with high EV penetration and stringent environmental regulations. These chargers are becoming the de facto standard for high-power charging stations, essential for reducing charging times for PEVs and HEVs, thereby alleviating range anxiety among consumers. Technological disruptions are at the forefront of this market evolution. Innovations in cooling fluids, pump systems, and connector designs are enhancing the efficiency, durability, and safety of liquid-cooled chargers. Furthermore, the integration of smart charging capabilities, V2G (Vehicle-to-Grid) technology, and advanced thermal management systems are setting new performance benchmarks.

Consumer behavior is also shifting towards faster and more convenient charging options. As EV ownership becomes more mainstream, drivers are seeking charging solutions that can replenish their batteries in a timeframe comparable to refueling a gasoline-powered vehicle. Liquid-cooled DC chargers are instrumental in meeting this demand. The increasing availability of electric vehicles with larger battery capacities further necessitates the deployment of high-power charging solutions, which liquid-cooled chargers are uniquely positioned to provide. The market penetration of liquid-cooled DC chargers in public charging stations is expected to exceed 70% by 2033, a testament to their technological superiority and market acceptance. The continuous refinement of charging protocols and the development of modular designs are also contributing to the ease of installation and maintenance, further accelerating adoption.

Dominant Regions, Countries, or Segments in Liquid Cooled DC Charger

The Pure Electric Vehicle (PEV) segment, specifically for charging, is currently the dominant force driving growth within the Liquid Cooled DC Charger market. This dominance is primarily attributed to the higher demand for rapid charging solutions from PEV owners who rely entirely on electric power for their daily commutes and longer journeys. By the end of 2025, PEVs are expected to account for an estimated 75% of the total market share for liquid-cooled DC charger applications. This segment's rapid expansion is closely linked to advancements in PEV battery technology, which increasingly supports higher charging rates, making liquid-cooled chargers a necessity rather than a luxury.

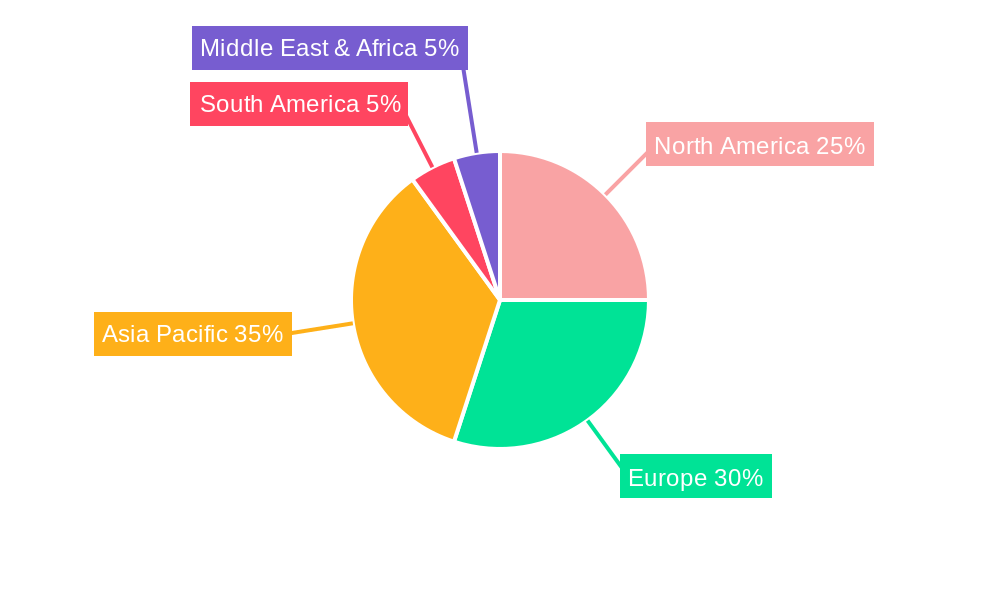

Geographically, Asia Pacific, particularly China, is emerging as the leading region for Liquid Cooled DC Charger adoption. China's proactive government policies, substantial investments in EV manufacturing and charging infrastructure, and a burgeoning EV market contribute to its leadership. By 2025, Asia Pacific is projected to hold over 45% of the global market share. The region's rapid urbanization and the increasing number of EV charging stations being deployed in public spaces, commercial complexes, and residential areas further bolster this dominance. Economic policies that offer subsidies for EV purchases and charging infrastructure development, coupled with aggressive mandates for emission reduction, create a highly conducive environment for the proliferation of liquid-cooled DC chargers.

The Type: Fixed liquid-cooled DC chargers are also significantly contributing to market dominance, especially in the development of large-scale public charging networks. These chargers, permanently installed at strategic locations, are designed for high-traffic areas such as highways, city centers, and dedicated EV charging hubs. Their robust construction and ability to deliver consistent high power outputs make them ideal for supporting the growing fleet of PEVs and HEVs. By 2025, the fixed charger segment is expected to capture approximately 70% of the total market revenue. The continuous build-out of charging infrastructure, driven by both government initiatives and private sector investments, ensures a sustained demand for these fixed charging solutions. The growth potential in this segment is further amplified by the increasing adoption of ultra-fast charging technologies, which are predominantly enabled by liquid-cooled systems to manage the immense heat generated during high-power charging sessions.

Liquid Cooled DC Charger Product Landscape

The Liquid Cooled DC Charger product landscape is characterized by rapid innovation focused on enhancing charging speed, efficiency, and reliability. Manufacturers are developing chargers capable of delivering power outputs exceeding 350 kW, significantly reducing charging times for Pure Electric Vehicles (PEVs) and Hybrid Electric Vehicles (HEVs). Key product innovations include advanced thermal management systems that utilize circulating cooling fluids to dissipate heat effectively, preventing component degradation and enabling sustained high-power charging. Connector designs are also evolving to ensure safe and robust connections under high current loads. Performance metrics are continuously being improved, with a focus on charging efficiency ratings above 95% and extended operational lifespans. Unique selling propositions include modular designs for easier maintenance and scalability, as well as integrated smart features for grid connectivity and remote diagnostics.

Key Drivers, Barriers & Challenges in Liquid Cooled DC Charger

Key Drivers:

- Accelerating EV Adoption: The rapid global uptake of PEVs and HEVs is the primary catalyst for demand in the liquid-cooled DC charger market.

- Demand for Faster Charging: Consumers and fleet operators require charging solutions that minimize downtime, driving the need for high-power liquid-cooled systems.

- Government Initiatives and Incentives: Policies promoting EV adoption and charging infrastructure development, including subsidies and tax credits, significantly boost market growth.

- Technological Advancements: Continuous improvements in battery technology and charger efficiency necessitate advanced cooling solutions.

Key Barriers & Challenges:

- High Initial Cost: Liquid-cooled DC chargers have a higher upfront cost compared to air-cooled alternatives, posing a barrier for some installations.

- Infrastructure Development: The need for substantial grid upgrades and the establishment of widespread charging networks can be a bottleneck.

- Standardization Issues: While improving, a lack of complete global standardization in charging protocols and connectors can create compatibility challenges.

- Maintenance Complexity: While designed for durability, the liquid cooling systems can be more complex to maintain than simpler air-cooled units, potentially requiring specialized technicians.

- Supply Chain Constraints: Disruptions in the supply chain for critical components can impact production volumes and lead times, affecting market availability.

Emerging Opportunities in Liquid Cooled DC Charger

Emerging opportunities lie in the integration of liquid-cooled DC chargers with smart grid technologies and renewable energy sources. The development of bidirectional charging capabilities, allowing EVs to feed power back into the grid (V2G), presents a significant avenue for growth and revenue generation. Furthermore, the expansion of charging infrastructure into new markets and underserved regions, such as rural areas and commercial fleet depots, offers untapped potential. Innovative applications, including charging solutions for heavy-duty electric vehicles (trucks and buses) and the potential for wireless liquid-cooled charging technologies, are also on the horizon. Evolving consumer preferences for integrated charging and mobility solutions will also drive demand for more advanced and user-friendly liquid-cooled charging experiences.

Growth Accelerators in the Liquid Cooled DC Charger Industry

Several factors are accelerating the growth of the Liquid Cooled DC Charger industry. Technological breakthroughs in thermal management, such as the development of more efficient cooling fluids and compact pump designs, are enabling higher power densities and smaller charger footprints. Strategic partnerships between charger manufacturers, EV automakers, and energy providers are crucial for developing seamless charging ecosystems and expanding market reach. Market expansion strategies, including the establishment of robust service and maintenance networks, are building consumer confidence. The increasing focus on sustainability and the circular economy is also driving innovation in charger design, emphasizing recyclability and energy efficiency.

Key Players Shaping the Liquid Cooled DC Charger Market

- SINBON

- Phoenix Contact

- Suzhou Recodeal

- Fisher Electronic Technology

- Shenglan Technology

- BULL

- Kaiye Xinneng Yuan

- kedesen

- Shenzhen Lilutong Electronic

- Weihai Honglin Electronic

- JAE

- Teison

- AG Electrical

- Teison Energy

- Shenzhen Woer Heat

- Jointlean Electrical Technology

Notable Milestones in Liquid Cooled DC Charger Sector

- 2019: Introduction of 350kW ultra-fast liquid-cooled chargers to the market, significantly reducing charging times for emerging EVs.

- 2020: Major automotive manufacturers begin to specify liquid-cooled DC charging as a standard for their high-performance electric vehicles.

- 2021: Increased investment in the development of advanced thermal management components, leading to improved efficiency and reliability of cooling systems.

- 2022: Rollout of new charging station networks featuring predominantly liquid-cooled DC chargers, driven by government infrastructure funding.

- 2023: Significant progress in the standardization of high-power charging connectors and communication protocols, enhancing interoperability.

- 2024: Enhanced focus on modular charger designs and predictive maintenance technologies for liquid-cooled systems.

- 2025 (Estimated): Widespread adoption of 500kW and above liquid-cooled charging solutions is anticipated, further accelerating EV adoption.

- 2027 (Projected): Integration of liquid-cooled chargers with grid management systems and V2G capabilities becomes more common.

- 2030 (Projected): Liquid-cooled DC chargers become the dominant technology for public fast-charging infrastructure globally.

- 2033 (Projected): Continuous innovation leads to even higher power outputs and increased integration with smart city infrastructure.

In-Depth Liquid Cooled DC Charger Market Outlook

The future of the Liquid Cooled DC Charger market is exceptionally bright, driven by the unstoppable momentum of global electrification. Growth accelerators such as rapid technological advancements in thermal management, the formation of strategic alliances across the EV ecosystem, and ambitious market expansion strategies will propel sustained expansion. The inherent advantages of liquid cooling—superior heat dissipation for higher power delivery and enhanced component longevity—will solidify its position as the preferred technology for fast-charging infrastructure. As EV penetration continues to soar and governments worldwide reinforce their commitment to decarbonization, the demand for efficient, reliable, and high-performance charging solutions will only intensify. This presents significant strategic opportunities for players to innovate, expand their global footprint, and capitalize on the transformative shift towards electric mobility.

Liquid Cooled DC Charger Segmentation

-

1. Application

- 1.1. Pure Electric Vehicle

- 1.2. Hybrid Electric Vehicle

-

2. Types

- 2.1. Fixed

- 2.2. Mobile

Liquid Cooled DC Charger Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Liquid Cooled DC Charger Regional Market Share

Geographic Coverage of Liquid Cooled DC Charger

Liquid Cooled DC Charger REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.23% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Pure Electric Vehicle

- 5.1.2. Hybrid Electric Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Fixed

- 5.2.2. Mobile

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Liquid Cooled DC Charger Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Pure Electric Vehicle

- 6.1.2. Hybrid Electric Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Fixed

- 6.2.2. Mobile

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Liquid Cooled DC Charger Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Pure Electric Vehicle

- 7.1.2. Hybrid Electric Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Fixed

- 7.2.2. Mobile

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Liquid Cooled DC Charger Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Pure Electric Vehicle

- 8.1.2. Hybrid Electric Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Fixed

- 8.2.2. Mobile

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Liquid Cooled DC Charger Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Pure Electric Vehicle

- 9.1.2. Hybrid Electric Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Fixed

- 9.2.2. Mobile

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Liquid Cooled DC Charger Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Pure Electric Vehicle

- 10.1.2. Hybrid Electric Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Fixed

- 10.2.2. Mobile

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Liquid Cooled DC Charger Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Pure Electric Vehicle

- 11.1.2. Hybrid Electric Vehicle

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Fixed

- 11.2.2. Mobile

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 SINBON

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Phoenix Contact

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Suzhou Recodeal

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Fisher Electronic Technology

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Shenglan Technology

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 BULL

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Kaiye Xinneng Yuan

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 kedesen

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Shenzhen Lilutong Electronic

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Weihai Honglin Electronic

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 JAE

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Teison

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 AG Electrical

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Teison Energy

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Shenzhen Woer Heat

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Jointlean Electrical Technology

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.1 SINBON

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Liquid Cooled DC Charger Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Liquid Cooled DC Charger Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Liquid Cooled DC Charger Revenue (billion), by Application 2025 & 2033

- Figure 4: North America Liquid Cooled DC Charger Volume (K), by Application 2025 & 2033

- Figure 5: North America Liquid Cooled DC Charger Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Liquid Cooled DC Charger Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Liquid Cooled DC Charger Revenue (billion), by Types 2025 & 2033

- Figure 8: North America Liquid Cooled DC Charger Volume (K), by Types 2025 & 2033

- Figure 9: North America Liquid Cooled DC Charger Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Liquid Cooled DC Charger Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Liquid Cooled DC Charger Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Liquid Cooled DC Charger Volume (K), by Country 2025 & 2033

- Figure 13: North America Liquid Cooled DC Charger Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Liquid Cooled DC Charger Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Liquid Cooled DC Charger Revenue (billion), by Application 2025 & 2033

- Figure 16: South America Liquid Cooled DC Charger Volume (K), by Application 2025 & 2033

- Figure 17: South America Liquid Cooled DC Charger Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Liquid Cooled DC Charger Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Liquid Cooled DC Charger Revenue (billion), by Types 2025 & 2033

- Figure 20: South America Liquid Cooled DC Charger Volume (K), by Types 2025 & 2033

- Figure 21: South America Liquid Cooled DC Charger Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Liquid Cooled DC Charger Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Liquid Cooled DC Charger Revenue (billion), by Country 2025 & 2033

- Figure 24: South America Liquid Cooled DC Charger Volume (K), by Country 2025 & 2033

- Figure 25: South America Liquid Cooled DC Charger Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Liquid Cooled DC Charger Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Liquid Cooled DC Charger Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Liquid Cooled DC Charger Volume (K), by Application 2025 & 2033

- Figure 29: Europe Liquid Cooled DC Charger Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Liquid Cooled DC Charger Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Liquid Cooled DC Charger Revenue (billion), by Types 2025 & 2033

- Figure 32: Europe Liquid Cooled DC Charger Volume (K), by Types 2025 & 2033

- Figure 33: Europe Liquid Cooled DC Charger Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Liquid Cooled DC Charger Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Liquid Cooled DC Charger Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Liquid Cooled DC Charger Volume (K), by Country 2025 & 2033

- Figure 37: Europe Liquid Cooled DC Charger Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Liquid Cooled DC Charger Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Liquid Cooled DC Charger Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa Liquid Cooled DC Charger Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Liquid Cooled DC Charger Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Liquid Cooled DC Charger Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Liquid Cooled DC Charger Revenue (billion), by Types 2025 & 2033

- Figure 44: Middle East & Africa Liquid Cooled DC Charger Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Liquid Cooled DC Charger Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Liquid Cooled DC Charger Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Liquid Cooled DC Charger Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa Liquid Cooled DC Charger Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Liquid Cooled DC Charger Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Liquid Cooled DC Charger Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Liquid Cooled DC Charger Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific Liquid Cooled DC Charger Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Liquid Cooled DC Charger Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Liquid Cooled DC Charger Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Liquid Cooled DC Charger Revenue (billion), by Types 2025 & 2033

- Figure 56: Asia Pacific Liquid Cooled DC Charger Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Liquid Cooled DC Charger Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Liquid Cooled DC Charger Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Liquid Cooled DC Charger Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific Liquid Cooled DC Charger Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Liquid Cooled DC Charger Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Liquid Cooled DC Charger Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Liquid Cooled DC Charger Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Liquid Cooled DC Charger Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Liquid Cooled DC Charger Revenue billion Forecast, by Types 2020 & 2033

- Table 4: Global Liquid Cooled DC Charger Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Liquid Cooled DC Charger Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Liquid Cooled DC Charger Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Liquid Cooled DC Charger Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Liquid Cooled DC Charger Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Liquid Cooled DC Charger Revenue billion Forecast, by Types 2020 & 2033

- Table 10: Global Liquid Cooled DC Charger Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Liquid Cooled DC Charger Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Liquid Cooled DC Charger Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Liquid Cooled DC Charger Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Liquid Cooled DC Charger Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Liquid Cooled DC Charger Revenue billion Forecast, by Types 2020 & 2033

- Table 22: Global Liquid Cooled DC Charger Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Liquid Cooled DC Charger Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Liquid Cooled DC Charger Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Liquid Cooled DC Charger Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Liquid Cooled DC Charger Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Liquid Cooled DC Charger Revenue billion Forecast, by Types 2020 & 2033

- Table 34: Global Liquid Cooled DC Charger Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Liquid Cooled DC Charger Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Liquid Cooled DC Charger Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Liquid Cooled DC Charger Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global Liquid Cooled DC Charger Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Liquid Cooled DC Charger Revenue billion Forecast, by Types 2020 & 2033

- Table 58: Global Liquid Cooled DC Charger Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Liquid Cooled DC Charger Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Liquid Cooled DC Charger Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Liquid Cooled DC Charger Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global Liquid Cooled DC Charger Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Liquid Cooled DC Charger Revenue billion Forecast, by Types 2020 & 2033

- Table 76: Global Liquid Cooled DC Charger Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Liquid Cooled DC Charger Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global Liquid Cooled DC Charger Volume K Forecast, by Country 2020 & 2033

- Table 79: China Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Liquid Cooled DC Charger Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Liquid Cooled DC Charger Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Liquid Cooled DC Charger?

The projected CAGR is approximately 13.23%.

2. Which companies are prominent players in the Liquid Cooled DC Charger?

Key companies in the market include SINBON, Phoenix Contact, Suzhou Recodeal, Fisher Electronic Technology, Shenglan Technology, BULL, Kaiye Xinneng Yuan, kedesen, Shenzhen Lilutong Electronic, Weihai Honglin Electronic, JAE, Teison, AG Electrical, Teison Energy, Shenzhen Woer Heat, Jointlean Electrical Technology.

3. What are the main segments of the Liquid Cooled DC Charger?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 13.95 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Liquid Cooled DC Charger," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Liquid Cooled DC Charger report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Liquid Cooled DC Charger?

To stay informed about further developments, trends, and reports in the Liquid Cooled DC Charger, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence