Key Insights

The South American dairy alternatives market is set for substantial growth, projected to reach an estimated USD 896.04 million by 2025, with a Compound Annual Growth Rate (CAGR) of 8.2% anticipated through 2033. This expansion is driven by increasing consumer health awareness, a rise in lactose intolerance and dairy allergies, and growing ethical concerns for animal welfare and environmental sustainability. The surge in vegan and flexitarian diets across the region further fuels demand for plant-based beverages and foods. Key growth drivers include the expanding availability of nutritious and appealing dairy-free options, supported by strategic marketing from leading companies emphasizing health benefits and product versatility.

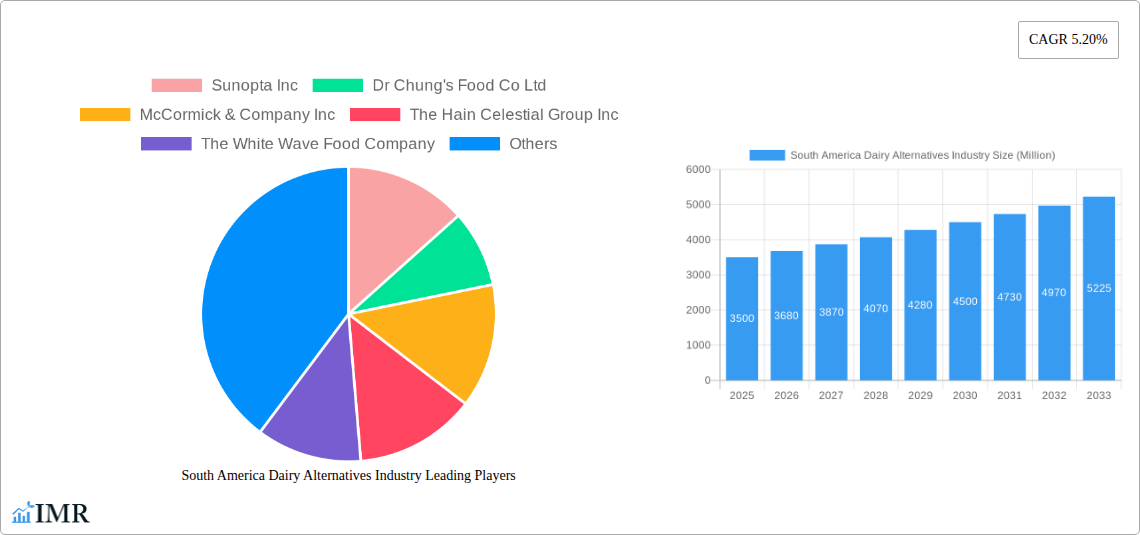

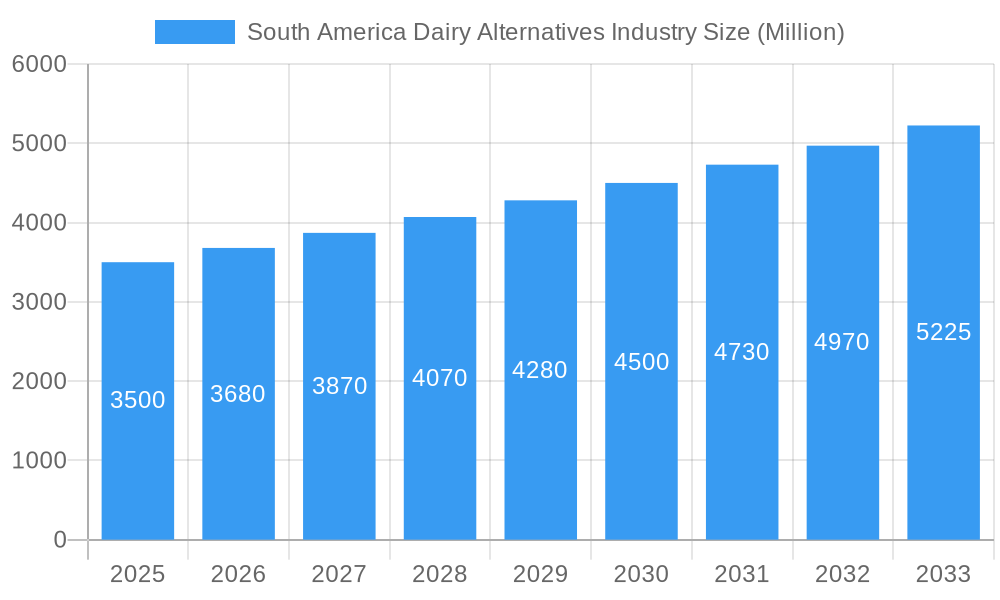

South America Dairy Alternatives Industry Market Size (In Million)

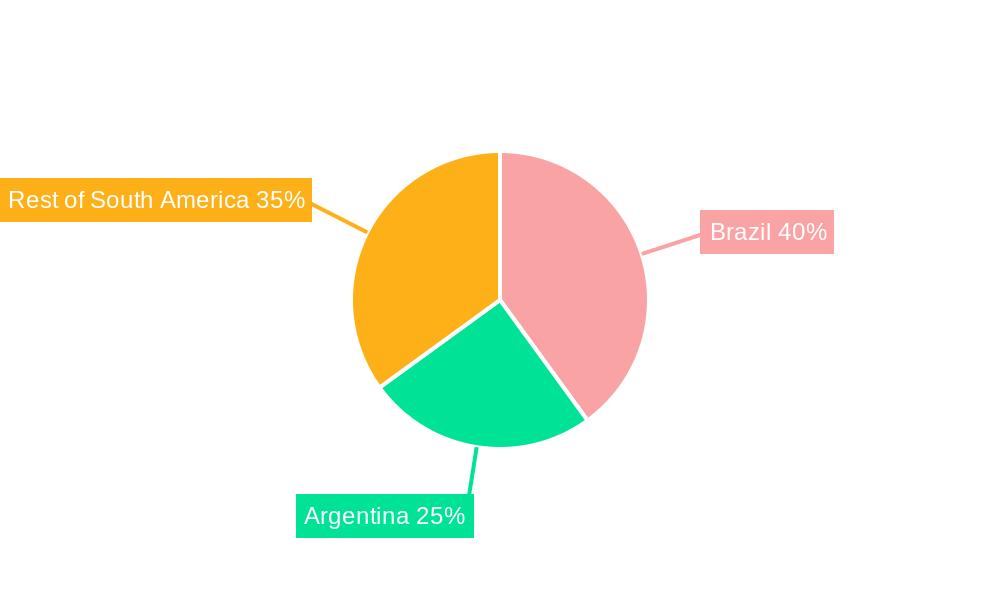

Consumer preferences are shifting, with soy and almond alternatives currently leading, though coconut and rice-based segments show significant future potential. Distribution channels are diversifying, with online sales rapidly growing alongside traditional retail, including hypermarkets, supermarkets, and health food stores. Brazil and Argentina are at the forefront of market penetration, with the "Rest of South America" segment also demonstrating promising expansion as awareness and product accessibility increase. Emerging trends focus on innovative dairy-free products like yogurts, cheeses, and ice creams, broadening market appeal beyond milk substitutes. Strategic focus is required to address challenges such as the price difference compared to conventional dairy and the need for enhanced consumer education on nutritional value and product benefits.

South America Dairy Alternatives Industry Company Market Share

South America Dairy Alternatives Industry Market Dynamics & Structure

The South America dairy alternatives market is characterized by a dynamic and evolving landscape, driven by increasing consumer awareness of health, environmental concerns, and ethical considerations. Market concentration is moderate, with a mix of established multinational corporations and agile local players vying for market share. Technological innovation is a significant driver, focusing on improving taste, texture, and nutritional profiles of plant-based beverages and foods. Key innovations include advancements in fermentation processes for enhanced flavor, the development of novel protein sources beyond traditional soy and almond, and improved emulsification techniques for smoother product consistency. Regulatory frameworks, while generally supportive of food safety standards, are still developing regarding labeling and marketing of dairy alternative products, presenting both opportunities and potential hurdles.

Competitive product substitutes are abundant, ranging from various plant-based milk alternatives (soy, almond, coconut, oat, rice) to vegan yogurts, cheeses, and even ice creams. The primary end-user demographics include lactose-intolerant individuals, vegans, vegetarians, health-conscious consumers seeking lower cholesterol and saturated fat options, and environmentally aware shoppers aiming to reduce their carbon footprint.

Mergers & Acquisitions (M&A) trends are active, with larger food conglomerates acquiring smaller, innovative startups to expand their plant-based portfolios and gain access to new technologies and consumer bases. For instance, acquisitions of artisanal vegan cheese producers and oat milk innovators are becoming more common.

- Market Concentration: Moderate, with increasing consolidation.

- Technological Innovation: Focus on taste, texture, nutrition, and novel protein sources.

- Regulatory Landscape: Evolving, with an emphasis on clarity and consumer protection.

- Competitive Landscape: Diverse plant-based substitutes, including soy, almond, coconut, and oat-based products.

- End-User Demographics: Lactose-intolerant, vegans, vegetarians, health-conscious, environmentally aware.

- M&A Trends: Strategic acquisitions by major food companies to bolster plant-based offerings.

South America Dairy Alternatives Industry Growth Trends & Insights

The South America dairy alternatives industry is experiencing robust growth, projected to expand significantly over the forecast period. The market size evolution is being shaped by a confluence of factors, including rising disposable incomes in key economies, a growing middle class with increased purchasing power, and a pervasive shift in dietary preferences. Adoption rates for dairy alternatives are accelerating, particularly among urban populations who have greater access to information and a wider variety of products. This surge in adoption is not merely a trend but a fundamental behavioral shift driven by a deeper understanding of the health benefits associated with plant-based diets. Consumers are actively seeking alternatives that are perceived as healthier, offering lower cholesterol, reduced saturated fat, and increased fiber content.

Technological disruptions are playing a crucial role in this expansion. Innovations in processing, ingredient sourcing, and product formulation are leading to dairy alternatives that more closely mimic the taste and texture of traditional dairy products, thereby overcoming past consumer hesitations. For example, advancements in oat milk production have resulted in a creamier and more versatile product, appealing to a broader segment of the population. Furthermore, the development of advanced emulsification and stabilization techniques ensures longer shelf life and consistent product quality, making these alternatives more convenient for widespread consumption.

Consumer behavior shifts are profoundly impacting market dynamics. The rising popularity of flexitarianism, where individuals reduce their meat and dairy consumption without fully eliminating it, is a significant growth engine. This is complemented by an increasing demand for ethical and sustainable food choices. Consumers are more discerning about the environmental impact of their food, with plant-based options often perceived as having a lower carbon footprint and requiring less water compared to conventional dairy production. The influence of social media and health and wellness influencers also contributes to the dissemination of information and the popularization of dairy-free lifestyles. Market penetration is expected to deepen as product availability increases across diverse distribution channels, from major supermarkets to specialized health food stores and burgeoning e-commerce platforms. The base year value for the South America dairy alternatives market stands at approximately 3,500 million units in 2025, with a projected Compound Annual Growth Rate (CAGR) of xx% during the forecast period of 2025–2033. This growth trajectory is underpinned by sustained consumer interest and ongoing product innovation.

Dominant Regions, Countries, or Segments in South America Dairy Alternatives Industry

The South America dairy alternatives industry exhibits a clear dominance in specific regions and segments, with Brazil emerging as the leading country driving market growth. This ascendancy is attributed to a combination of economic policies, a large and increasingly health-conscious population, and a well-developed retail infrastructure that facilitates widespread product availability. Brazil's substantial agricultural output also provides a strong foundation for sourcing key plant-based ingredients. The country's economic policies have fostered investment in the food processing sector, encouraging both domestic and international companies to expand their presence and product offerings in the dairy alternatives space. Furthermore, a growing middle class with higher disposable incomes is more inclined to experiment with and adopt premium food products, including plant-based alternatives.

Within Brazil, the Hypermarket/Supermarket distribution channel plays a pivotal role in the market's dominance. These large-format retail stores offer unparalleled accessibility and a wide selection of dairy alternative products, catering to a broad consumer base. The convenience and one-stop-shopping experience offered by hypermarkets and supermarkets make them the preferred choice for a majority of consumers seeking dairy alternatives. Online sales channels are rapidly gaining traction, driven by the convenience of home delivery and the increasing penetration of e-commerce in urban areas. This channel is particularly effective for reaching consumers in more remote locations or those with busy schedules.

Among the product segments, Soy-based alternatives have historically held a strong market position due to their established presence, affordability, and versatility in a wide range of applications, from beverages to food products. However, Almond-based and Coconut-based alternatives are experiencing significant growth, driven by consumer perceptions of superior taste and perceived health benefits. Almond milk, in particular, has gained immense popularity for its creamy texture and slightly sweet flavor, making it a preferred choice for coffee and cereals. Coconut milk is favored for its rich flavor and its use in culinary applications and as a base for vegan desserts. The Other types segment, which includes oat-based, rice-based, and emerging protein alternatives like pea and hemp, is witnessing the most rapid expansion. Oat milk, in particular, is rapidly challenging the dominance of soy and almond due to its excellent taste, texture, and sustainability credentials.

- Dominant Country: Brazil, driven by economic policies, population size, and health consciousness.

- Dominant Distribution Channel: Hypermarket/Supermarket, offering wide accessibility and selection.

- Key Product Segments Driving Growth:

- Almond-based: Popular for taste and perceived health benefits.

- Coconut-based: Valued for flavor and culinary versatility.

- Other types (especially Oat-based): Experiencing rapid growth due to taste, texture, and sustainability.

South America Dairy Alternatives Industry Product Landscape

The South America dairy alternatives product landscape is marked by continuous innovation aimed at enhancing consumer appeal and expanding applications. Manufacturers are actively developing plant-based beverages with improved protein content, reduced sugar levels, and fortified vitamins and minerals to match or exceed the nutritional profiles of traditional dairy. Unique selling propositions include the introduction of novel flavor combinations, such as mocha almond milk or vanilla coconut yogurt, catering to evolving taste preferences. Technological advancements in ingredient processing, such as cold-pressing and advanced blending techniques, are crucial for delivering smoother textures and richer flavors. The performance metrics of these products are increasingly being benchmarked against dairy, with a focus on achieving comparable creaminess, frothing ability for beverages, and stability in cooking and baking applications.

Key Drivers, Barriers & Challenges in South America Dairy Alternatives Industry

Key Drivers: The South America dairy alternatives market is propelled by several key drivers. Growing health consciousness among consumers, leading to increased demand for lactose-free and lower-cholesterol options, is a primary catalyst. The rising global awareness of environmental sustainability and the ethical concerns surrounding traditional dairy farming are also significant growth factors, encouraging a shift towards plant-based diets. Technological innovations that improve the taste, texture, and nutritional value of dairy alternatives are making them more accessible and appealing to a broader consumer base. Government initiatives and supportive policies promoting plant-based food production and consumption in some South American countries also contribute to market expansion.

Key Barriers & Challenges: Despite the positive outlook, the industry faces several barriers and challenges. The perceived higher cost of some dairy alternatives compared to conventional dairy products can be a restraint for price-sensitive consumers. Supply chain complexities, particularly for sourcing specific plant-based ingredients like almonds or oats in certain regions, can impact availability and cost. Regulatory hurdles related to labeling and marketing claims can also pose challenges for manufacturers. Furthermore, entrenched consumer habits and preferences for traditional dairy products require significant marketing efforts to overcome. Intense competition among numerous brands and product offerings also necessitates continuous innovation and effective differentiation strategies.

Emerging Opportunities in South America Dairy Alternatives Industry

Emerging opportunities in the South America dairy alternatives industry are manifold, primarily stemming from unmet consumer needs and untapped market segments. The burgeoning demand for specialized, functional dairy alternatives, such as those fortified with probiotics for gut health or added with adaptogens for stress relief, presents a significant growth avenue. Furthermore, the expansion of the dairy-free dessert and confectionery market, including vegan ice creams, chocolates, and baked goods, offers substantial untapped potential. The growing acceptance of plant-based options in foodservice channels, such as cafes and restaurants, provides opportunities for product innovation and strategic partnerships. Moreover, focusing on emerging economies within "Rest of South America" and developing localized product formulations that cater to regional palates can unlock new customer bases.

Growth Accelerators in the South America Dairy Alternatives Industry Industry

Several growth accelerators are poised to significantly boost the South America dairy alternatives market. Technological breakthroughs in the extraction and processing of novel plant-based proteins, such as those derived from fava beans, peas, or chickpeas, will lead to more diverse and nutritious product offerings. Strategic partnerships between dairy alternative manufacturers and conventional dairy companies can facilitate wider distribution and leverage existing market infrastructure. Furthermore, the increasing focus on sustainability certifications and eco-friendly packaging will resonate with environmentally conscious consumers, driving brand loyalty and market penetration. Investments in research and development to create dairy alternatives with enhanced sensory appeal and functional benefits will further accelerate adoption rates.

Key Players Shaping the South America Dairy Alternatives Industry Market

- Sunopta Inc

- Dr Chung's Food Co Ltd

- McCormick & Company Inc

- The Hain Celestial Group Inc

- The White Wave Food Company

- The Coca-Cola Company

- VitaSoy

- Blue Diamond growers

- General Mills Inc (Yoplait USA Inc )

- Sanitarium Health and Wellbeing Company

Notable Milestones in South America Dairy Alternatives Industry Sector

- 2019: Increased focus on oat milk as a leading dairy alternative due to its neutral taste and creamy texture.

- 2020: Sunopta Inc. expanded its plant-based product portfolio through strategic acquisitions.

- 2021: The Hain Celestial Group Inc. reported strong growth in its plant-based offerings across Latin America.

- 2022: The Coca-Cola Company launched a new line of plant-based beverages targeting health-conscious consumers in Brazil.

- 2023: VitaSoy saw a surge in demand for its soy milk products following a successful marketing campaign emphasizing health benefits.

- 2024 (Estimated): Continued investment in R&D by key players to improve the taste and nutritional profile of coconut and almond-based alternatives.

In-Depth South America Dairy Alternatives Industry Market Outlook

The South America dairy alternatives industry is set for continued robust expansion, driven by persistent consumer shifts towards healthier and more sustainable dietary choices. Key growth accelerators include ongoing innovation in novel protein sources, strategic alliances across the food industry, and a strong emphasis on sustainable practices that resonate with an increasingly eco-conscious demographic. The market outlook is characterized by significant future potential, with opportunities to penetrate underserved regions and develop localized product offerings that cater to specific cultural tastes. Manufacturers investing in advanced R&D to enhance sensory attributes and functional benefits will be well-positioned to capture market share. The industry's trajectory indicates a strong and sustained growth phase, making it an attractive sector for investment and innovation in the coming years.

South America Dairy Alternatives Industry Segmentation

-

1. Type

- 1.1. Soy-based

- 1.2. Almond-based

- 1.3. Coconut-based

- 1.4. Rice-based

- 1.5. Other types

-

2. Distribution Channel

- 2.1. Hypermarket/Supermarket

- 2.2. Convenience Store

- 2.3. Health Food Store

- 2.4. Online

- 2.5. Other sales channel

-

3. Geography

- 3.1. Brazil

- 3.2. Argentina

- 3.3. Rest of South America

South America Dairy Alternatives Industry Segmentation By Geography

- 1. Brazil

- 2. Argentina

- 3. Rest of South America

South America Dairy Alternatives Industry Regional Market Share

Geographic Coverage of South America Dairy Alternatives Industry

South America Dairy Alternatives Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Soy-based

- 5.1.2. Almond-based

- 5.1.3. Coconut-based

- 5.1.4. Rice-based

- 5.1.5. Other types

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Hypermarket/Supermarket

- 5.2.2. Convenience Store

- 5.2.3. Health Food Store

- 5.2.4. Online

- 5.2.5. Other sales channel

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. Brazil

- 5.3.2. Argentina

- 5.3.3. Rest of South America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Brazil

- 5.4.2. Argentina

- 5.4.3. Rest of South America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. South America Dairy Alternatives Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Soy-based

- 6.1.2. Almond-based

- 6.1.3. Coconut-based

- 6.1.4. Rice-based

- 6.1.5. Other types

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Hypermarket/Supermarket

- 6.2.2. Convenience Store

- 6.2.3. Health Food Store

- 6.2.4. Online

- 6.2.5. Other sales channel

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. Brazil

- 6.3.2. Argentina

- 6.3.3. Rest of South America

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Brazil South America Dairy Alternatives Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Soy-based

- 7.1.2. Almond-based

- 7.1.3. Coconut-based

- 7.1.4. Rice-based

- 7.1.5. Other types

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Hypermarket/Supermarket

- 7.2.2. Convenience Store

- 7.2.3. Health Food Store

- 7.2.4. Online

- 7.2.5. Other sales channel

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. Brazil

- 7.3.2. Argentina

- 7.3.3. Rest of South America

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Argentina South America Dairy Alternatives Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Soy-based

- 8.1.2. Almond-based

- 8.1.3. Coconut-based

- 8.1.4. Rice-based

- 8.1.5. Other types

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Hypermarket/Supermarket

- 8.2.2. Convenience Store

- 8.2.3. Health Food Store

- 8.2.4. Online

- 8.2.5. Other sales channel

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. Brazil

- 8.3.2. Argentina

- 8.3.3. Rest of South America

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Rest of South America South America Dairy Alternatives Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Soy-based

- 9.1.2. Almond-based

- 9.1.3. Coconut-based

- 9.1.4. Rice-based

- 9.1.5. Other types

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Hypermarket/Supermarket

- 9.2.2. Convenience Store

- 9.2.3. Health Food Store

- 9.2.4. Online

- 9.2.5. Other sales channel

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. Brazil

- 9.3.2. Argentina

- 9.3.3. Rest of South America

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Sunopta Inc

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Dr Chung's Food Co Ltd

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 McCormick & Company Inc

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 The Hain Celestial Group Inc

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 The White Wave Food Company

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 The Coca-Cola Company

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 VitaSoy

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Blue Diamond growers

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 General Mills Inc (Yoplait USA Inc )

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 Sanitarium Health and Wellbeing Company

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.1 Sunopta Inc

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: South America Dairy Alternatives Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: South America Dairy Alternatives Industry Share (%) by Company 2025

List of Tables

- Table 1: South America Dairy Alternatives Industry Revenue million Forecast, by Type 2020 & 2033

- Table 2: South America Dairy Alternatives Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 3: South America Dairy Alternatives Industry Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 4: South America Dairy Alternatives Industry Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 5: South America Dairy Alternatives Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 6: South America Dairy Alternatives Industry Volume K Tons Forecast, by Geography 2020 & 2033

- Table 7: South America Dairy Alternatives Industry Revenue million Forecast, by Region 2020 & 2033

- Table 8: South America Dairy Alternatives Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 9: South America Dairy Alternatives Industry Revenue million Forecast, by Type 2020 & 2033

- Table 10: South America Dairy Alternatives Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 11: South America Dairy Alternatives Industry Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 12: South America Dairy Alternatives Industry Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 13: South America Dairy Alternatives Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 14: South America Dairy Alternatives Industry Volume K Tons Forecast, by Geography 2020 & 2033

- Table 15: South America Dairy Alternatives Industry Revenue million Forecast, by Country 2020 & 2033

- Table 16: South America Dairy Alternatives Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 17: South America Dairy Alternatives Industry Revenue million Forecast, by Type 2020 & 2033

- Table 18: South America Dairy Alternatives Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 19: South America Dairy Alternatives Industry Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 20: South America Dairy Alternatives Industry Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 21: South America Dairy Alternatives Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 22: South America Dairy Alternatives Industry Volume K Tons Forecast, by Geography 2020 & 2033

- Table 23: South America Dairy Alternatives Industry Revenue million Forecast, by Country 2020 & 2033

- Table 24: South America Dairy Alternatives Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 25: South America Dairy Alternatives Industry Revenue million Forecast, by Type 2020 & 2033

- Table 26: South America Dairy Alternatives Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 27: South America Dairy Alternatives Industry Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 28: South America Dairy Alternatives Industry Volume K Tons Forecast, by Distribution Channel 2020 & 2033

- Table 29: South America Dairy Alternatives Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 30: South America Dairy Alternatives Industry Volume K Tons Forecast, by Geography 2020 & 2033

- Table 31: South America Dairy Alternatives Industry Revenue million Forecast, by Country 2020 & 2033

- Table 32: South America Dairy Alternatives Industry Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South America Dairy Alternatives Industry?

The projected CAGR is approximately 8.2%.

2. Which companies are prominent players in the South America Dairy Alternatives Industry?

Key companies in the market include Sunopta Inc, Dr Chung's Food Co Ltd, McCormick & Company Inc, The Hain Celestial Group Inc, The White Wave Food Company, The Coca-Cola Company, VitaSoy, Blue Diamond growers, General Mills Inc (Yoplait USA Inc ), Sanitarium Health and Wellbeing Company.

3. What are the main segments of the South America Dairy Alternatives Industry?

The market segments include Type, Distribution Channel, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 896.04 million as of 2022.

5. What are some drivers contributing to market growth?

Increasing awareness and diagnosis of lactose intolerance and dairy allergies are driving consumers towards dairy alternatives.

6. What are the notable trends driving market growth?

Trend Towards products with added functional benefits.

7. Are there any restraints impacting market growth?

Dairy alternatives often come with a higher price tag compared to traditional dairy products.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South America Dairy Alternatives Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South America Dairy Alternatives Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South America Dairy Alternatives Industry?

To stay informed about further developments, trends, and reports in the South America Dairy Alternatives Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence