Key Insights

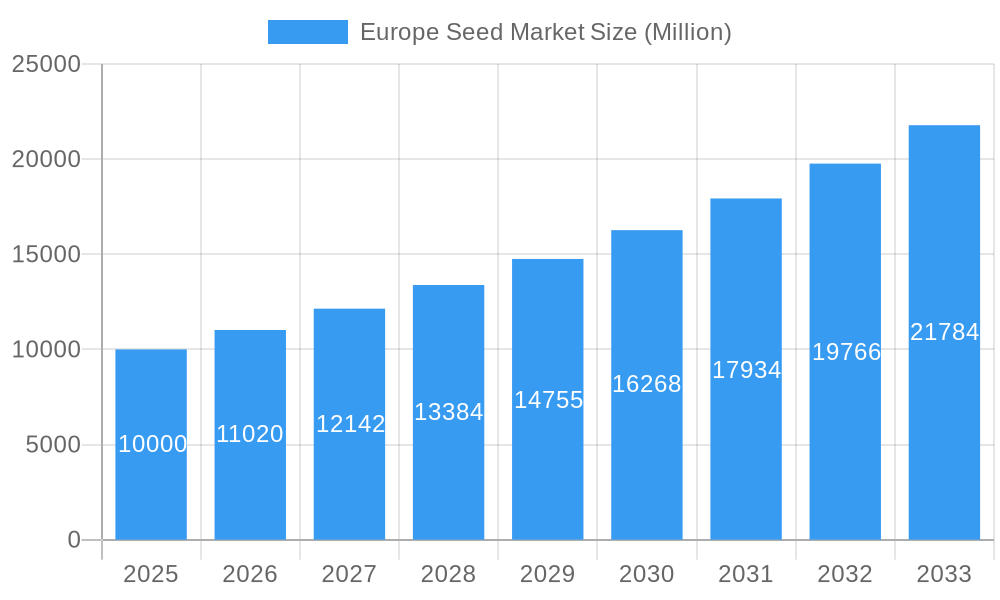

The European seed market, valued at $2.61 billion in 2025, is projected to grow at a CAGR of 6.96% from 2025 to 2033. This expansion is driven by escalating demand for high-yield, disease-resistant crops due to population growth and climate change concerns. Advancements in breeding technologies, particularly hybrid seeds, and the adoption of sustainable agricultural practices like precision farming further bolster market growth. Supportive government initiatives for agricultural innovation also contribute significantly. Key growth segments include row crops, followed by vegetables and pulses. Geographically, Germany, France, Italy, and the UK are major contributors, with Eastern European markets showing emerging potential.

Europe Seed Market Market Size (In Billion)

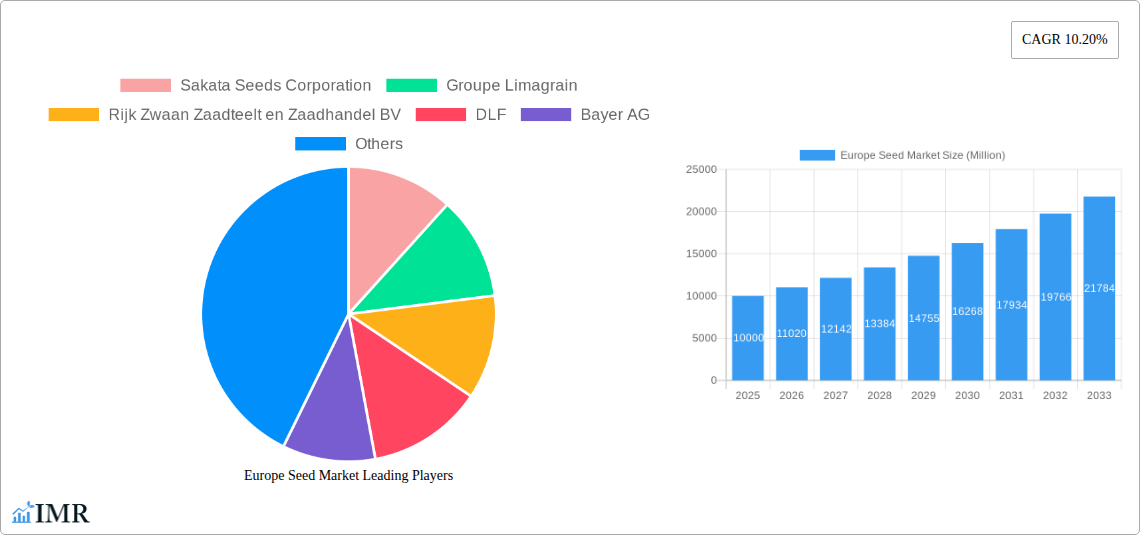

Market growth faces challenges including raw material price volatility and stringent regulatory frameworks for seed production and distribution. The competitive landscape, marked by both multinational corporations and regional players, necessitates strategic adaptation. Despite these restraints, the European seed market demonstrates a positive long-term outlook, fueled by continuous technological innovation, rising agricultural demands, and favorable government policies. Leading companies such as Sakata Seeds Corporation, Limagrain, Rijk Zwaan, DLF, Bayer, KWS, Advanta Seeds, Syngenta, Corteva, and BASF are actively pursuing R&D, portfolio expansion, and strategic partnerships to maintain a competitive advantage.

Europe Seed Market Company Market Share

This report offers a comprehensive analysis of the European seed market, covering historical data (2019-2024), current estimates (2025), and future forecasts (2025-2033). It details market dynamics, growth drivers, regional performance, product segmentation (row crops, vegetables, pulses), cultivation methods (open field, protected cultivation), and key breeding technologies (hybrids). The base year for this analysis is 2025, with market values presented in billions.

Europe Seed Market Market Dynamics & Structure

The European seed market is characterized by a moderately concentrated landscape, with a few major players holding significant market share. However, the presence of numerous smaller, specialized companies creates a dynamic competitive environment. Technological innovation, particularly in hybrid seed development and genetic modification, is a key growth driver. Stringent regulatory frameworks governing seed production, distribution, and labeling significantly influence market operations. The emergence of sustainable and climate-resilient seeds is shaping industry practices. Furthermore, the market witnesses regular mergers and acquisitions (M&A) activity, reflecting consolidation trends and strategic expansions. The increasing demand for high-yielding, disease-resistant varieties is propelling market growth.

- Market Concentration: The top 5 players account for approximately xx% of the market share in 2025.

- Technological Innovation: Focus on hybrid seed development, precision breeding technologies, and GMOs.

- Regulatory Landscape: Stringent regulations impacting seed testing, approval processes, and labeling.

- Competitive Substitutes: Limited substitutes exist due to the specialized nature of seeds.

- M&A Activity: An average of xx M&A deals have been recorded annually during the historical period (2019-2024).

- Innovation Barriers: High R&D costs, lengthy approval processes, and intellectual property protection challenges.

Europe Seed Market Growth Trends & Insights

The European seed market has experienced steady growth during the historical period (2019-2024), driven by factors such as rising agricultural production, increasing demand for high-yielding varieties, and favorable government policies promoting sustainable agriculture. The market is expected to maintain a healthy Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). The adoption of advanced breeding technologies like hybrids is increasing rapidly, while the demand for organic and bio-seeds is also growing. Consumer preferences are shifting towards sustainably produced food, indirectly increasing demand for seeds meeting these standards. Technological disruptions, such as precision agriculture and digital farming, are further optimizing seed usage and yield. Market penetration of advanced seed technologies remains relatively high in Western European countries compared to Eastern European countries.

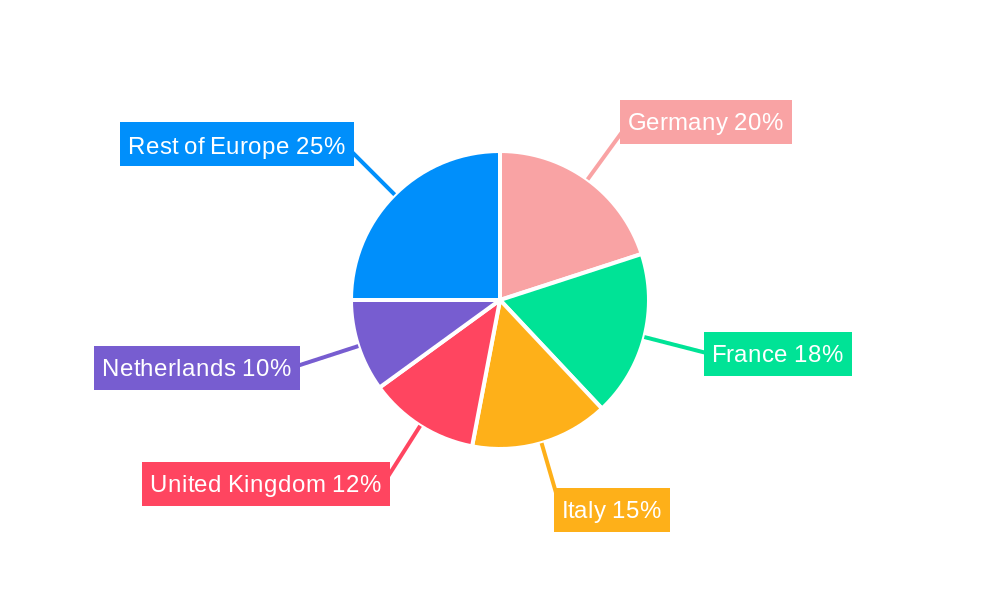

Dominant Regions, Countries, or Segments in Europe Seed Market

Germany, France, and the United Kingdom represent the largest national markets within the European Union. These countries benefit from established agricultural infrastructure, advanced farming practices, and significant government support for the agricultural sector. The row crops segment dominates the market, followed by vegetables. Within the vegetable segment, pulses are showing significant growth potential. The open-field cultivation mechanism remains dominant, but protected cultivation is experiencing rapid growth in response to climate change risks and the potential for enhanced yield and efficiency. Hybrid breeding technology holds a dominant market share due to increased yields and superior crop characteristics.

- Key Drivers:

- Germany: Strong agricultural infrastructure and government support.

- France: Large agricultural land area and diversified crop production.

- United Kingdom: Well-established research institutions and advanced agricultural practices.

- Row Crops: High demand from large-scale farming operations.

- Hybrid Breeding: Superior yield and crop characteristics.

- Open Field Cultivation: Cost-effectiveness and scalability.

Europe Seed Market Product Landscape

The European seed market showcases a diverse range of products, characterized by continuous innovation in genetic modification, hybrid development, and trait enhancements (disease resistance, drought tolerance, pest resistance). Companies are focusing on developing high-yielding varieties suited to diverse agroclimatic conditions. The emphasis is on seeds that offer improved performance metrics, such as increased yields, better nutritional value, and enhanced resilience against biotic and abiotic stresses. Unique selling propositions often involve proprietary breeding technologies or superior germplasm. Technological advancements focus on precision breeding technologies, including marker-assisted selection and gene editing, to enhance the speed and efficiency of varietal development.

Key Drivers, Barriers & Challenges in Europe Seed Market

Key Drivers:

- Growing demand for food security and higher agricultural yields.

- Technological advancements leading to improved seed quality.

- Favorable government policies promoting agricultural innovation.

- Climate change adaptation, leading to a need for resilient seed varieties.

Challenges & Restraints:

- Stringent regulations and lengthy approval processes for new seed varieties.

- High R&D costs associated with developing improved seeds.

- Fluctuations in weather patterns and climatic variability impacting crop yields.

- Increased competitive intensity among seed companies.

- Supply chain disruptions influencing seed availability and pricing. The impact is estimated to have reduced overall market growth by approximately xx% in 2022.

Emerging Opportunities in Europe Seed Market

- Growing demand for organic and sustainably produced seeds.

- Increasing adoption of precision agriculture techniques.

- Development of climate-resilient and stress-tolerant seed varieties.

- Expansion into emerging markets in Eastern Europe.

- Opportunities in seed treatment technologies and precision seed placement.

Growth Accelerators in the Europe Seed Market Industry

Several factors are poised to significantly accelerate growth in the European seed market. These include continued technological innovations in breeding technologies, the development of seeds tailored to specific regional needs and climate change adaptation, strategic partnerships between seed companies and agricultural technology providers, and the expansion into newer and underserved markets. Furthermore, increasing governmental support for agricultural research and development will likely play a role.

Key Players Shaping the Europe Seed Market Market

Notable Milestones in Europe Seed Market Sector

- July 2023: Syngenta launched a new hybrid winter barley with tolerance to barley yellowing virus (BYDV) and higher yield. This launch is expected to significantly increase market share in the winter barley segment.

- July 2023: BASF expanded its Xitavo soybean seed portfolio with the addition of 11 new high-yielding varieties for the 2024 growing season, featuring Enlist E3 technology. This expansion strengthens BASF's position in the soybean market.

- June 2023: Corteva Agriscience opened a new combined crop protection and seed research laboratory in Eschbach, Germany (USD 6.61 million investment). This investment signals a commitment to R&D and sustainability in the European market.

In-Depth Europe Seed Market Market Outlook

The future of the European seed market appears promising, driven by sustained demand for high-yielding and climate-resilient seed varieties. Technological breakthroughs in breeding and seed treatment, coupled with strategic partnerships and market expansion efforts, will play a key role in shaping future growth. The market is poised to benefit from increasing consumer awareness of sustainable agriculture practices and the growing importance of food security. Opportunities exist in the development of seeds tailored to specific regional agroclimatic conditions, further enhancing the overall market potential.

Europe Seed Market Segmentation

-

1. Breeding Technology

-

1.1. Hybrids

- 1.1.1. Non-Transgenic Hybrids

- 1.1.2. Insect Resistant Hybrids

- 1.2. Open Pollinated Varieties & Hybrid Derivatives

-

1.1. Hybrids

-

2. Cultivation Mechanism

- 2.1. Open Field

- 2.2. Protected Cultivation

-

3. Crop Type

-

3.1. Row Crops

-

3.1.1. Fiber Crops

- 3.1.1.1. Cotton

- 3.1.1.2. Other Fiber Crops

-

3.1.2. Forage Crops

- 3.1.2.1. Alfalfa

- 3.1.2.2. Forage Corn

- 3.1.2.3. Forage Sorghum

- 3.1.2.4. Other Forage Crops

-

3.1.3. Grains & Cereals

- 3.1.3.1. Rice

- 3.1.3.2. Wheat

- 3.1.3.3. Other Grains & Cereals

-

3.1.4. Oilseeds

- 3.1.4.1. Canola, Rapeseed & Mustard

- 3.1.4.2. Soybean

- 3.1.4.3. Sunflower

- 3.1.4.4. Other Oilseeds

- 3.1.5. Pulses

-

3.1.1. Fiber Crops

-

3.2. Vegetables

-

3.2.1. Brassicas

- 3.2.1.1. Cabbage

- 3.2.1.2. Carrot

- 3.2.1.3. Cauliflower & Broccoli

- 3.2.1.4. Other Brassicas

-

3.2.2. Cucurbits

- 3.2.2.1. Cucumber & Gherkin

- 3.2.2.2. Pumpkin & Squash

- 3.2.2.3. Other Cucurbits

-

3.2.3. Roots & Bulbs

- 3.2.3.1. Garlic

- 3.2.3.2. Onion

- 3.2.3.3. Potato

- 3.2.3.4. Other Roots & Bulbs

-

3.2.4. Solanaceae

- 3.2.4.1. Chilli

- 3.2.4.2. Eggplant

- 3.2.4.3. Tomato

- 3.2.4.4. Other Solanaceae

-

3.2.5. Unclassified Vegetables

- 3.2.5.1. Asparagus

- 3.2.5.2. Lettuce

- 3.2.5.3. Okra

- 3.2.5.4. Peas

- 3.2.5.5. Spinach

- 3.2.5.6. Other Unclassified Vegetables

-

3.2.1. Brassicas

-

3.1. Row Crops

-

4. Breeding Technology

-

4.1. Hybrids

- 4.1.1. Non-Transgenic Hybrids

- 4.1.2. Insect Resistant Hybrids

- 4.2. Open Pollinated Varieties & Hybrid Derivatives

-

4.1. Hybrids

-

5. Cultivation Mechanism

- 5.1. Open Field

- 5.2. Protected Cultivation

-

6. Crop Type

-

6.1. Row Crops

-

6.1.1. Fiber Crops

- 6.1.1.1. Cotton

- 6.1.1.2. Other Fiber Crops

-

6.1.2. Forage Crops

- 6.1.2.1. Alfalfa

- 6.1.2.2. Forage Corn

- 6.1.2.3. Forage Sorghum

- 6.1.2.4. Other Forage Crops

-

6.1.3. Grains & Cereals

- 6.1.3.1. Rice

- 6.1.3.2. Wheat

- 6.1.3.3. Other Grains & Cereals

-

6.1.4. Oilseeds

- 6.1.4.1. Canola, Rapeseed & Mustard

- 6.1.4.2. Soybean

- 6.1.4.3. Sunflower

- 6.1.4.4. Other Oilseeds

- 6.1.5. Pulses

-

6.1.1. Fiber Crops

-

6.2. Vegetables

-

6.2.1. Brassicas

- 6.2.1.1. Cabbage

- 6.2.1.2. Carrot

- 6.2.1.3. Cauliflower & Broccoli

- 6.2.1.4. Other Brassicas

-

6.2.2. Cucurbits

- 6.2.2.1. Cucumber & Gherkin

- 6.2.2.2. Pumpkin & Squash

- 6.2.2.3. Other Cucurbits

-

6.2.3. Roots & Bulbs

- 6.2.3.1. Garlic

- 6.2.3.2. Onion

- 6.2.3.3. Potato

- 6.2.3.4. Other Roots & Bulbs

-

6.2.4. Solanaceae

- 6.2.4.1. Chilli

- 6.2.4.2. Eggplant

- 6.2.4.3. Tomato

- 6.2.4.4. Other Solanaceae

-

6.2.5. Unclassified Vegetables

- 6.2.5.1. Asparagus

- 6.2.5.2. Lettuce

- 6.2.5.3. Okra

- 6.2.5.4. Peas

- 6.2.5.5. Spinach

- 6.2.5.6. Other Unclassified Vegetables

-

6.2.1. Brassicas

-

6.1. Row Crops

Europe Seed Market Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Seed Market Regional Market Share

Geographic Coverage of Europe Seed Market

Europe Seed Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.96% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 5.1.1. Hybrids

- 5.1.1.1. Non-Transgenic Hybrids

- 5.1.1.2. Insect Resistant Hybrids

- 5.1.2. Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1. Hybrids

- 5.2. Market Analysis, Insights and Forecast - by Cultivation Mechanism

- 5.2.1. Open Field

- 5.2.2. Protected Cultivation

- 5.3. Market Analysis, Insights and Forecast - by Crop Type

- 5.3.1. Row Crops

- 5.3.1.1. Fiber Crops

- 5.3.1.1.1. Cotton

- 5.3.1.1.2. Other Fiber Crops

- 5.3.1.2. Forage Crops

- 5.3.1.2.1. Alfalfa

- 5.3.1.2.2. Forage Corn

- 5.3.1.2.3. Forage Sorghum

- 5.3.1.2.4. Other Forage Crops

- 5.3.1.3. Grains & Cereals

- 5.3.1.3.1. Rice

- 5.3.1.3.2. Wheat

- 5.3.1.3.3. Other Grains & Cereals

- 5.3.1.4. Oilseeds

- 5.3.1.4.1. Canola, Rapeseed & Mustard

- 5.3.1.4.2. Soybean

- 5.3.1.4.3. Sunflower

- 5.3.1.4.4. Other Oilseeds

- 5.3.1.5. Pulses

- 5.3.1.1. Fiber Crops

- 5.3.2. Vegetables

- 5.3.2.1. Brassicas

- 5.3.2.1.1. Cabbage

- 5.3.2.1.2. Carrot

- 5.3.2.1.3. Cauliflower & Broccoli

- 5.3.2.1.4. Other Brassicas

- 5.3.2.2. Cucurbits

- 5.3.2.2.1. Cucumber & Gherkin

- 5.3.2.2.2. Pumpkin & Squash

- 5.3.2.2.3. Other Cucurbits

- 5.3.2.3. Roots & Bulbs

- 5.3.2.3.1. Garlic

- 5.3.2.3.2. Onion

- 5.3.2.3.3. Potato

- 5.3.2.3.4. Other Roots & Bulbs

- 5.3.2.4. Solanaceae

- 5.3.2.4.1. Chilli

- 5.3.2.4.2. Eggplant

- 5.3.2.4.3. Tomato

- 5.3.2.4.4. Other Solanaceae

- 5.3.2.5. Unclassified Vegetables

- 5.3.2.5.1. Asparagus

- 5.3.2.5.2. Lettuce

- 5.3.2.5.3. Okra

- 5.3.2.5.4. Peas

- 5.3.2.5.5. Spinach

- 5.3.2.5.6. Other Unclassified Vegetables

- 5.3.2.1. Brassicas

- 5.3.1. Row Crops

- 5.4. Market Analysis, Insights and Forecast - by Breeding Technology

- 5.4.1. Hybrids

- 5.4.1.1. Non-Transgenic Hybrids

- 5.4.1.2. Insect Resistant Hybrids

- 5.4.2. Open Pollinated Varieties & Hybrid Derivatives

- 5.4.1. Hybrids

- 5.5. Market Analysis, Insights and Forecast - by Cultivation Mechanism

- 5.5.1. Open Field

- 5.5.2. Protected Cultivation

- 5.6. Market Analysis, Insights and Forecast - by Crop Type

- 5.6.1. Row Crops

- 5.6.1.1. Fiber Crops

- 5.6.1.1.1. Cotton

- 5.6.1.1.2. Other Fiber Crops

- 5.6.1.2. Forage Crops

- 5.6.1.2.1. Alfalfa

- 5.6.1.2.2. Forage Corn

- 5.6.1.2.3. Forage Sorghum

- 5.6.1.2.4. Other Forage Crops

- 5.6.1.3. Grains & Cereals

- 5.6.1.3.1. Rice

- 5.6.1.3.2. Wheat

- 5.6.1.3.3. Other Grains & Cereals

- 5.6.1.4. Oilseeds

- 5.6.1.4.1. Canola, Rapeseed & Mustard

- 5.6.1.4.2. Soybean

- 5.6.1.4.3. Sunflower

- 5.6.1.4.4. Other Oilseeds

- 5.6.1.5. Pulses

- 5.6.1.1. Fiber Crops

- 5.6.2. Vegetables

- 5.6.2.1. Brassicas

- 5.6.2.1.1. Cabbage

- 5.6.2.1.2. Carrot

- 5.6.2.1.3. Cauliflower & Broccoli

- 5.6.2.1.4. Other Brassicas

- 5.6.2.2. Cucurbits

- 5.6.2.2.1. Cucumber & Gherkin

- 5.6.2.2.2. Pumpkin & Squash

- 5.6.2.2.3. Other Cucurbits

- 5.6.2.3. Roots & Bulbs

- 5.6.2.3.1. Garlic

- 5.6.2.3.2. Onion

- 5.6.2.3.3. Potato

- 5.6.2.3.4. Other Roots & Bulbs

- 5.6.2.4. Solanaceae

- 5.6.2.4.1. Chilli

- 5.6.2.4.2. Eggplant

- 5.6.2.4.3. Tomato

- 5.6.2.4.4. Other Solanaceae

- 5.6.2.5. Unclassified Vegetables

- 5.6.2.5.1. Asparagus

- 5.6.2.5.2. Lettuce

- 5.6.2.5.3. Okra

- 5.6.2.5.4. Peas

- 5.6.2.5.5. Spinach

- 5.6.2.5.6. Other Unclassified Vegetables

- 5.6.2.1. Brassicas

- 5.6.1. Row Crops

- 5.7. Market Analysis, Insights and Forecast - by Region

- 5.7.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 6. Europe Seed Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 6.1.1. Hybrids

- 6.1.1.1. Non-Transgenic Hybrids

- 6.1.1.2. Insect Resistant Hybrids

- 6.1.2. Open Pollinated Varieties & Hybrid Derivatives

- 6.1.1. Hybrids

- 6.2. Market Analysis, Insights and Forecast - by Cultivation Mechanism

- 6.2.1. Open Field

- 6.2.2. Protected Cultivation

- 6.3. Market Analysis, Insights and Forecast - by Crop Type

- 6.3.1. Row Crops

- 6.3.1.1. Fiber Crops

- 6.3.1.1.1. Cotton

- 6.3.1.1.2. Other Fiber Crops

- 6.3.1.2. Forage Crops

- 6.3.1.2.1. Alfalfa

- 6.3.1.2.2. Forage Corn

- 6.3.1.2.3. Forage Sorghum

- 6.3.1.2.4. Other Forage Crops

- 6.3.1.3. Grains & Cereals

- 6.3.1.3.1. Rice

- 6.3.1.3.2. Wheat

- 6.3.1.3.3. Other Grains & Cereals

- 6.3.1.4. Oilseeds

- 6.3.1.4.1. Canola, Rapeseed & Mustard

- 6.3.1.4.2. Soybean

- 6.3.1.4.3. Sunflower

- 6.3.1.4.4. Other Oilseeds

- 6.3.1.5. Pulses

- 6.3.1.1. Fiber Crops

- 6.3.2. Vegetables

- 6.3.2.1. Brassicas

- 6.3.2.1.1. Cabbage

- 6.3.2.1.2. Carrot

- 6.3.2.1.3. Cauliflower & Broccoli

- 6.3.2.1.4. Other Brassicas

- 6.3.2.2. Cucurbits

- 6.3.2.2.1. Cucumber & Gherkin

- 6.3.2.2.2. Pumpkin & Squash

- 6.3.2.2.3. Other Cucurbits

- 6.3.2.3. Roots & Bulbs

- 6.3.2.3.1. Garlic

- 6.3.2.3.2. Onion

- 6.3.2.3.3. Potato

- 6.3.2.3.4. Other Roots & Bulbs

- 6.3.2.4. Solanaceae

- 6.3.2.4.1. Chilli

- 6.3.2.4.2. Eggplant

- 6.3.2.4.3. Tomato

- 6.3.2.4.4. Other Solanaceae

- 6.3.2.5. Unclassified Vegetables

- 6.3.2.5.1. Asparagus

- 6.3.2.5.2. Lettuce

- 6.3.2.5.3. Okra

- 6.3.2.5.4. Peas

- 6.3.2.5.5. Spinach

- 6.3.2.5.6. Other Unclassified Vegetables

- 6.3.2.1. Brassicas

- 6.3.1. Row Crops

- 6.4. Market Analysis, Insights and Forecast - by Breeding Technology

- 6.4.1. Hybrids

- 6.4.1.1. Non-Transgenic Hybrids

- 6.4.1.2. Insect Resistant Hybrids

- 6.4.2. Open Pollinated Varieties & Hybrid Derivatives

- 6.4.1. Hybrids

- 6.5. Market Analysis, Insights and Forecast - by Cultivation Mechanism

- 6.5.1. Open Field

- 6.5.2. Protected Cultivation

- 6.6. Market Analysis, Insights and Forecast - by Crop Type

- 6.6.1. Row Crops

- 6.6.1.1. Fiber Crops

- 6.6.1.1.1. Cotton

- 6.6.1.1.2. Other Fiber Crops

- 6.6.1.2. Forage Crops

- 6.6.1.2.1. Alfalfa

- 6.6.1.2.2. Forage Corn

- 6.6.1.2.3. Forage Sorghum

- 6.6.1.2.4. Other Forage Crops

- 6.6.1.3. Grains & Cereals

- 6.6.1.3.1. Rice

- 6.6.1.3.2. Wheat

- 6.6.1.3.3. Other Grains & Cereals

- 6.6.1.4. Oilseeds

- 6.6.1.4.1. Canola, Rapeseed & Mustard

- 6.6.1.4.2. Soybean

- 6.6.1.4.3. Sunflower

- 6.6.1.4.4. Other Oilseeds

- 6.6.1.5. Pulses

- 6.6.1.1. Fiber Crops

- 6.6.2. Vegetables

- 6.6.2.1. Brassicas

- 6.6.2.1.1. Cabbage

- 6.6.2.1.2. Carrot

- 6.6.2.1.3. Cauliflower & Broccoli

- 6.6.2.1.4. Other Brassicas

- 6.6.2.2. Cucurbits

- 6.6.2.2.1. Cucumber & Gherkin

- 6.6.2.2.2. Pumpkin & Squash

- 6.6.2.2.3. Other Cucurbits

- 6.6.2.3. Roots & Bulbs

- 6.6.2.3.1. Garlic

- 6.6.2.3.2. Onion

- 6.6.2.3.3. Potato

- 6.6.2.3.4. Other Roots & Bulbs

- 6.6.2.4. Solanaceae

- 6.6.2.4.1. Chilli

- 6.6.2.4.2. Eggplant

- 6.6.2.4.3. Tomato

- 6.6.2.4.4. Other Solanaceae

- 6.6.2.5. Unclassified Vegetables

- 6.6.2.5.1. Asparagus

- 6.6.2.5.2. Lettuce

- 6.6.2.5.3. Okra

- 6.6.2.5.4. Peas

- 6.6.2.5.5. Spinach

- 6.6.2.5.6. Other Unclassified Vegetables

- 6.6.2.1. Brassicas

- 6.6.1. Row Crops

- 6.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Sakata Seeds Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Groupe Limagrain

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Rijk Zwaan Zaadteelt en Zaadhandel BV

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 DLF

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Bayer AG

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 KWS SAAT SE & Co KGaA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Advanta Seeds - UPL

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Syngenta Grou

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Corteva Agriscience

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 BASF SE

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Sakata Seeds Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Seed Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Seed Market Share (%) by Company 2025

List of Tables

- Table 1: Europe Seed Market Revenue billion Forecast, by Breeding Technology 2020 & 2033

- Table 2: Europe Seed Market Revenue billion Forecast, by Cultivation Mechanism 2020 & 2033

- Table 3: Europe Seed Market Revenue billion Forecast, by Crop Type 2020 & 2033

- Table 4: Europe Seed Market Revenue billion Forecast, by Breeding Technology 2020 & 2033

- Table 5: Europe Seed Market Revenue billion Forecast, by Cultivation Mechanism 2020 & 2033

- Table 6: Europe Seed Market Revenue billion Forecast, by Crop Type 2020 & 2033

- Table 7: Europe Seed Market Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Europe Seed Market Revenue billion Forecast, by Breeding Technology 2020 & 2033

- Table 9: Europe Seed Market Revenue billion Forecast, by Cultivation Mechanism 2020 & 2033

- Table 10: Europe Seed Market Revenue billion Forecast, by Crop Type 2020 & 2033

- Table 11: Europe Seed Market Revenue billion Forecast, by Breeding Technology 2020 & 2033

- Table 12: Europe Seed Market Revenue billion Forecast, by Cultivation Mechanism 2020 & 2033

- Table 13: Europe Seed Market Revenue billion Forecast, by Crop Type 2020 & 2033

- Table 14: Europe Seed Market Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United Kingdom Europe Seed Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Germany Europe Seed Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: France Europe Seed Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Italy Europe Seed Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Spain Europe Seed Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Netherlands Europe Seed Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Belgium Europe Seed Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Sweden Europe Seed Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Norway Europe Seed Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Poland Europe Seed Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Denmark Europe Seed Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Seed Market?

The projected CAGR is approximately 6.96%.

2. Which companies are prominent players in the Europe Seed Market?

Key companies in the market include Sakata Seeds Corporation, Groupe Limagrain, Rijk Zwaan Zaadteelt en Zaadhandel BV, DLF, Bayer AG, KWS SAAT SE & Co KGaA, Advanta Seeds - UPL, Syngenta Grou, Corteva Agriscience, BASF SE.

3. What are the main segments of the Europe Seed Market?

The market segments include Breeding Technology, Cultivation Mechanism, Crop Type, Breeding Technology, Cultivation Mechanism, Crop Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.61 billion as of 2022.

5. What are some drivers contributing to market growth?

Demand For Landscaping Maintenance; Adoption of Green Spaces and Green Roofs.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Shortage of Labor In Landscaping; High Maintenance Cost of Lawn Mowers.

8. Can you provide examples of recent developments in the market?

July 2023: Syngenta launched a new hybrid winter barley with tolerance to barley yellowing virus (BYDV) and higher yield.July 2023: BASF expanded its Xitavo soybean seed portfolio with the addition of its 11 new high-yielding varieties for the 2024 growing season, featuring the Enlist E3 technology to combat difficult weeds.June 2023: Corteva Agriscience opened its first combined crop protection and seed research laboratory in the EMEA region. With an investment of USD 6.61 million, the R&D site is located in Eschbach, Germany, which is energy-efficient and in line with Corteva Agriscience's sustainability commitment.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Seed Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Seed Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Seed Market?

To stay informed about further developments, trends, and reports in the Europe Seed Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence