Key Insights

The North America fertilizer industry is poised for significant growth, projected to reach a market size of $63.76 billion in 2025, expanding at a robust CAGR of 5.13% during the forecast period from 2025 to 2033. This robust expansion is primarily driven by the escalating demand for food due to a growing population, diminishing arable land, and a heightened focus on food security across the region. Farmers are increasingly adopting advanced fertilization techniques and high-efficiency nutrient products to maximize yields and improve crop quality, especially for key agricultural outputs in the United States, Canada, and Mexico. Furthermore, the push towards sustainable agriculture and precision farming practices, which optimize nutrient application and reduce environmental impact, is fueling the adoption of specialized and innovative fertilizer solutions, including nitrogen, phosphate, and potash fertilizers, alongside the rising interest in micronutrient and organic alternatives.

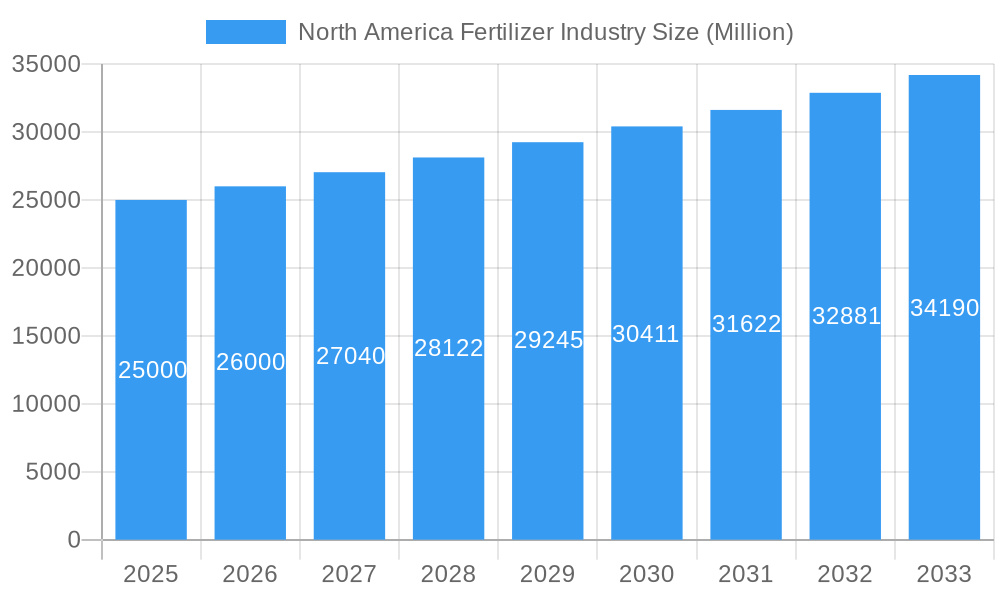

North America Fertilizer Industry Market Size (In Billion)

Key trends shaping the North American fertilizer market include the growing emphasis on nutrient use efficiency (NUE) technologies, the integration of digital agriculture solutions for optimized fertilizer application, and a discernible shift towards specialty and bio-based fertilizers. While the industry benefits from strong agricultural support and technological advancements, it also faces challenges such as volatile raw material prices, stringent environmental regulations governing nutrient runoff, and the need for significant capital investment in research and development. Leading players like Nutrien Ltd., CF Industries Holdings, Inc., and The Mosaic Company are continuously innovating, offering diverse formulations from liquid to granular, catering to applications spanning large-scale agriculture, horticulture, and even home gardening. This dynamic landscape underscores a resilient and evolving market, strategically positioned to meet the future demands of food production and sustainable resource management.

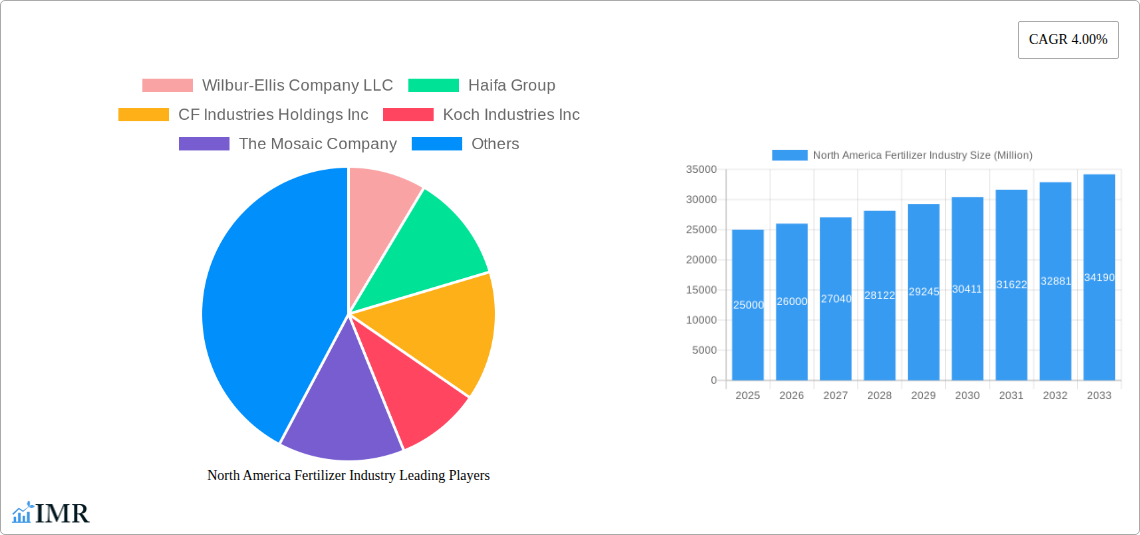

North America Fertilizer Industry Company Market Share

Unlocking Growth: The North America Fertilizer Industry Market Report (2025-2033)

SEO Keywords: North America fertilizer market, agricultural inputs, crop nutrition, sustainable agriculture, precision farming, nutrient management, nitrogen fertilizers, phosphate fertilizers, potash fertilizers, micronutrient fertilizers, organic fertilizers, farming technology, agricultural chemicals, soil health, fertilizer trends, market analysis North America, fertilizer industry growth, agricultural productivity.

The North America Fertilizer Industry is a cornerstone of global food security, witnessing significant expansion driven by escalating demand for enhanced agricultural productivity and sustainable farming practices. This comprehensive report delves into the intricate dynamics of the parent North America agricultural inputs market and its vital child market, the fertilizer industry, providing an unparalleled outlook on its trajectory from 2025 to 2033. Valued at an estimated $52.7 billion in 2025, the market is projected to reach approximately $72.3 billion by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of 4.0%. It offers critical insights for stakeholders, investors, and industry professionals navigating this evolving landscape, highlighting market segmentation, competitive strategies, technological innovations, and regulatory impacts across the region.

Companies Profiled:

- [Nutrien Ltd.](https://www.nutrien.com/ rel="noopener noreferrer")

- [CF Industries Holdings, Inc.](https://www.cfindustries.com/ rel="noopener noreferrer")

- [The Mosaic Company](https://www.mosaicco.com/ rel="noopener noreferrer")

- [Yara International ASA](https://www.yara.com/ rel="noopener noreferrer")

- [The Andersons, Inc.](https://www.andersonsinc.com/ rel="noopener noreferrer")

- [ICL Group Ltd.](https://www.icl-group.com/ rel="noopener noreferrer")

- [Koch Industries, Inc.](https://www.kochind.com/ rel="noopener noreferrer")

- [Haifa Group](https://www.haifa-group.com/ rel="noopener noreferrer")

- [Sociedad Química y Minera de Chile (SQM)](https://www.sqm.com/ rel="noopener noreferrer")

- [Wilbur-Ellis Company LLC](https://www.wilbur-ellis.com/ rel="noopener noreferrer")

- [Compass Minerals](https://www.compassminerals.com/ rel="noopener noreferrer")

- [OCP Group](https://www.ocpgroup.ma/ rel="noopener noreferrer")

- Others

Market Segments Analyzed:

- Type: Nitrogen Fertilizers, Phosphate Fertilizers, Potash Fertilizers, Micronutrient Fertilizers, Organic Fertilizers

- Formulation: Liquid, Granular, Powder, Pellets

- Application: Agriculture, Horticulture, Gardening, Others

- Sales Channel: Direct Sales, Distributors and Wholesalers, Online, Others

Timelines:

- Study Period: 2019–2033

- Historical Period: 2019–2024

- Base Year: 2025

- Estimated Year: 2025

- Forecast Period: 2025–2033

North America Fertilizer Industry Market Dynamics & Structure

The North America fertilizer market exhibits a moderately concentrated structure, with leading players like Nutrien, CF Industries, and The Mosaic Company holding an estimated combined market share of xx% across key segments, particularly in nitrogen, phosphate, and potash production. This concentration often leads to economies of scale and significant capital investments in infrastructure. Technological innovation acts as a pivotal driver, with increasing R&D focus on Enhanced Efficiency Fertilizers (EEFs), controlled-release formulations, and bio-fertilizers designed to optimize nutrient uptake and reduce environmental impact. Precision agriculture technologies, including IoT sensors and AI-driven nutrient management systems, are transforming application practices, despite initial investment barriers. Regulatory frameworks, particularly those addressing nutrient runoff and greenhouse gas emissions, significantly influence product development and market access, driving demand for more sustainable solutions. For instance, regulations like those in the Chesapeake Bay watershed push for improved nitrogen and phosphorus management.

Competitive product substitutes, such as organic amendments, biologicals, and plant growth regulators, are gaining traction, though their market penetration remains smaller compared to conventional fertilizers. The end-user demographic is shifting towards larger, technologically adept commercial farms that are more likely to adopt advanced fertilizer solutions and precision farming techniques. However, the presence of numerous small and medium-sized farms also necessitates diverse product offerings. Mergers and Acquisitions (M&A) trends indicate a continuous drive for consolidation, diversification, and strategic expansion. Between 2019 and 2024, the industry witnessed approximately xx M&A deals valued at over $xx billion, focusing on expanding retail networks, acquiring specialty product lines, and securing raw material sources. Innovation barriers predominantly include the high capital expenditure required for new production facilities, the lengthy regulatory approval processes for novel formulations, and the volatility of raw material prices. These dynamics collectively shape a market characterized by both intense competition and collaborative innovation, all aimed at enhancing agricultural sustainability and productivity in the region.

North America Fertilizer Industry Growth Trends & Insights

The North America Fertilizer Industry is experiencing a dynamic growth trajectory, evolving from an estimated market size of $42.5 billion in 2019 to $52.7 billion in 2025, and projected to reach approximately $72.3 billion by 2033, driven by a compelling CAGR of 4.0% from 2025-2033. This growth is intrinsically linked to the escalating global food demand, necessitating higher crop yields from finite arable land. The adoption rates of advanced fertilizers and precision agriculture technologies are steadily increasing across the region. Farmers are increasingly investing in specialty fertilizers, such as micronutrients and organic blends, to address specific soil deficiencies and enhance crop quality, moving beyond conventional NPK applications. This shift is particularly evident in the corn belt and specialty crop regions.

Technological disruptions are at the forefront of market evolution, with the proliferation of digital farming platforms, remote sensing, and AI-powered analytics revolutionizing nutrient management. These innovations enable hyper-localized application, minimizing waste and maximizing efficiency, thereby boosting nutrient use efficiency (NUE) by an estimated xx% in early adopter regions. Furthermore, the development of bio-fertilizers and biostimulants offers sustainable alternatives, capturing a growing segment of environmentally conscious growers. Consumer behavior shifts are also influencing the market, with increasing demand for sustainably produced food, traceability, and products with a lower environmental footprint. This societal pressure encourages fertilizer manufacturers to innovate cleaner, more efficient, and eco-friendly products. Market penetration of these next-generation solutions, while still nascent in some areas, is accelerating, particularly in large-scale commercial farming operations that possess the capital and technical expertise to implement them. The persistent need for enhanced crop resilience against climate change impacts, coupled with optimizing input costs, further underpins the consistent growth and transformative insights within the North America fertilizer sector.

Dominant Regions, Countries, or Segments in North America Fertilizer Industry

Among the various classifications, Nitrogen Fertilizers within the Type segment stands as the leading category driving market growth in the North America Fertilizer Industry. This dominance is primarily attributed to the widespread requirement for nitrogen in virtually all major crops, including corn, wheat, and soybeans, which are extensively cultivated across the United States and Canada. Nitrogen is critical for vegetative growth, chlorophyll formation, and protein synthesis, making it the most consumed nutrient in agricultural practices. In 2025, Nitrogen Fertilizers are estimated to command approximately 55-60% of the total market share by type, valued at around $30.1-$31.6 billion. The United States, due to its vast agricultural acreage and intense farming practices, emerges as the dominant country, accounting for an estimated 70-75% of the North American fertilizer consumption.

- Economic Policies: Favorable agricultural subsidies and farm bill provisions in the U.S. and Canada incentivize farmers to maintain high yields, directly translating into sustained demand for nitrogen fertilizers.

- Infrastructure: Well-established production facilities and extensive distribution networks, including pipelines and rail lines for anhydrous ammonia and urea, ensure efficient supply to agricultural hubs.

- Crop Mix: The prevalence of nitrogen-intensive crops like corn, which alone accounts for over 90 million acres in the U.S., guarantees a foundational demand.

- Technological Advancements: Innovations in nitrogen stabilization and slow/controlled-release fertilizers (e.g., UAN) enhance efficiency and reduce environmental impact, further solidifying its market position.

- Soil Health Initiatives: While driving demand for other types like micronutrients, these initiatives also emphasize precise nitrogen application, preventing overuse and promoting sustainable practices.

The growth potential for Nitrogen Fertilizers remains high, particularly with the continuous development of Enhanced Efficiency Fertilizers (EEFs) that mitigate nutrient loss through volatilization, leaching, and denitrification. These innovations address environmental concerns while maintaining productivity, ensuring nitrogen's enduring role as the primary growth accelerator in North American agriculture. The significant investments by major players in expanding production capacities, such as Koch's USD 30 million investment in its Kansas nitrogen plant to increase UAN production, further underscore the segment's robust growth trajectory and market dominance.

North America Fertilizer Industry Product Landscape

The North America fertilizer product landscape is continuously evolving, driven by innovation aimed at enhancing nutrient use efficiency and promoting environmental sustainability. Key innovations include the development of Enhanced Efficiency Fertilizers (EEFs) like slow- and controlled-release fertilizers, which deliver nutrients over extended periods, minimizing losses and maximizing uptake. Bio-fertilizers and biostimulants, derived from natural sources, are also gaining traction, offering biological solutions to improve plant health and nutrient absorption. Applications range from general crop nutrition for staples like corn and wheat to highly specialized blends for horticulture, high-value fruits, vegetables, and even urban farming. Performance metrics focus on improved yield, reduced nutrient runoff, and enhanced soil health. Unique selling propositions highlight sustainability, tailored nutrition solutions, and increased farm profitability, while technological advancements in granular and liquid formulations enable precise application through modern farming equipment, showcasing significant progress from traditional commodity fertilizers.

Key Drivers, Barriers & Challenges in North America Fertilizer Industry

The North America Fertilizer Industry is propelled by several robust drivers. Foremost is the increasing global demand for food, necessitating higher crop yields from static or decreasing arable land, which directly translates to greater fertilizer consumption. Advancements in precision agriculture technologies, including GPS guidance, variable rate application, and drone mapping, significantly boost the efficient and targeted use of fertilizers, promoting their adoption. Government support and agricultural subsidies often incentivize farmers to maintain high productivity, thereby stabilizing fertilizer demand. Furthermore, the rising prices of agricultural commodities make investing in higher-quality fertilizers more economically viable for farmers, and technological innovations in nutrient delivery systems enhance efficacy and sustainability.

However, the industry faces considerable barriers and challenges. Volatile raw material prices, particularly for natural gas (a key input for nitrogen fertilizers) and phosphate rock, lead to unpredictable production costs and market pricing fluctuations. Stringent environmental regulations, aimed at reducing nutrient runoff into waterways and mitigating greenhouse gas emissions, demand significant R&D investment for cleaner formulations and application methods. Supply chain disruptions, exacerbated by geopolitical events and logistical bottlenecks, can impact availability and cost, as seen during recent global crises. High initial investment in advanced fertilizer technologies and precision farming equipment can deter smaller farmers. Lastly, the impact of climate change, including extreme weather events, can disrupt planting and harvesting cycles, affecting fertilizer demand and application windows, posing quantifiable risks to market stability and growth.

Emerging Opportunities in North America Fertilizer Industry

Emerging opportunities in the North America Fertilizer Industry are centered on sustainability and technological integration. Untapped markets include smaller, independent farms increasingly seeking customized, efficient, and environmentally friendly nutrient solutions that cater to specific soil and crop requirements. There's also a growing niche in urban and vertical farming, which requires specialized hydroponic and aeroponic nutrient formulations. Innovative applications are expanding beyond traditional soil-based agriculture to include advanced foliar sprays, seed treatments, and encapsulated fertilizers that offer targeted nutrient delivery with minimal waste. Evolving consumer preferences for organic, locally sourced, and sustainably produced food are fueling the demand for certified organic fertilizers and biologically enhanced nutrient products. Moreover, the focus on circular economy models presents opportunities for companies to develop fertilizers from recycled waste streams, turning agricultural or municipal waste into valuable inputs and addressing both nutrient management and waste reduction challenges.

Growth Accelerators in the North America Fertilizer Industry Industry

Growth accelerators in the North America Fertilizer Industry are significantly driven by continuous technological breakthroughs, particularly in the realm of nutrient use efficiency and environmental stewardship. Innovations in genetics and crop breeding, such as CRISPR technology, demand specialized nutrient profiles, pushing the development of advanced fertilizer formulations. Strategic partnerships between traditional fertilizer manufacturers and ag-tech companies are fostering integrated solutions that combine smart sensors, data analytics, and bespoke fertilizer blends, leading to highly optimized nutrient management plans. Market expansion strategies are increasingly focusing on high-value specialty crops and organic segments, where premium products and tailored solutions command higher margins. Furthermore, investments in research and development for biostimulants and bio-fertilizers represent a significant catalyst, offering sustainable alternatives that enhance plant health, improve nutrient uptake, and reduce reliance on synthetic inputs, thereby securing long-term growth by aligning with global sustainability goals and regulatory pressures.

Key Players Shaping the North America Fertilizer Industry Market

- [Nutrien Ltd.](https://www.nutrien.com/ rel="noopener noreferrer")

- [CF Industries Holdings, Inc.](https://www.cfindustries.com/ rel="noopener noreferrer")

- [The Mosaic Company](https://www.mosaicco.com/ rel="noopener noreferrer")

- [Yara International ASA](https://www.yara.com/ rel="noopener noreferrer")

- [The Andersons, Inc.](https://www.andersonsinc.com/ rel="noopener noreferrer")

- [ICL Group Ltd.](https://www.icl-group.com/ rel="noopener noreferrer")

- [Koch Industries, Inc.](https://www.kochind.com/ rel="noopener noreferrer")

- [Haifa Group](https://www.haifa-group.com/ rel="noopener noreferrer")

- [Sociedad Química y Minera de Chile (SQM)](https://www.sqm.com/ rel="noopener noreferrer")

- [Wilbur-Ellis Company LLC](https://www.wilbur-ellis.com/ rel="noopener noreferrer")

- [Compass Minerals](https://www.compassminerals.com/ rel="noopener noreferrer")

- [OCP Group](https://www.ocpgroup.ma/ rel="noopener noreferrer")

- Others

Notable Milestones in North America Fertilizer Industry Sector

- January 2023: ICL entered into a strategic partnership agreement with General Mills, positioning ICL as the supplier of strategic specialty phosphate solutions. This long-term agreement signifies a move towards enhancing food product quality through advanced nutrient inputs and hints at international expansion for ICL's specialty solutions.

- October 2022: The Andersons expanded its retail farm center network by acquiring the assets of Mote Farm Service, Inc. This acquisition strengthens The Andersons' presence in key agricultural regions, improving direct access to farmers and bolstering their distribution capabilities for fertilizer products.

- August 2022: Koch invested approximately USD 30 million in its Kansas nitrogen plant, aiming to increase UAN (Urea Ammonium Nitrate) production by 35,000 tons per year. This investment directly addresses the growing demand for UAN across western Kansas and eastern Colorado, showcasing a commitment to meeting regional agricultural needs and optimizing production capacity for a crucial nitrogen fertilizer.

In-Depth North America Fertilizer Industry Market Outlook

The North America Fertilizer Industry is poised for significant expansion, fueled by a combination of technological ingenuity, strategic market realignments, and an overarching commitment to sustainable agriculture. Growth accelerators, including continuous advancements in nutrient use efficiency, the burgeoning adoption of precision farming technologies, and the rise of biologically enhanced fertilizer solutions, are setting the stage for a more productive and environmentally conscious sector. The future market potential is vast, particularly in areas focused on tailored crop nutrition and digital agricultural platforms, which optimize input application and minimize waste. Strategic opportunities lie in developing highly specialized products for emerging niche markets like urban agriculture and controlled-environment farming, expanding into high-growth organic and micronutrient segments, and forging cross-sector partnerships to deliver integrated farm management solutions. These trends collectively underscore a compelling market outlook, promising sustained growth and innovation within North America's vital fertilizer industry.

North America Fertilizer Industry Segmentation

-

1. Type

- 1.1. Nitrogen Fertilizers

- 1.2. Phosphate Fertilizers

- 1.3. Potash Fertilizers

- 1.4. Micronutrient Fertilizers

- 1.5. Organic Fertilizers

-

2. Formulation

- 2.1. Liquid

- 2.2. Granular

- 2.3. Powder

- 2.4. Pellets

-

3. Application

- 3.1. Agriculture

- 3.2. Horticulture

- 3.3. Gardening

- 3.4. Others

-

4. Sales Channel

- 4.1. Direct Sales

- 4.2. Distributors and Wholesalers

- 4.3. Online

- 4.4. Others

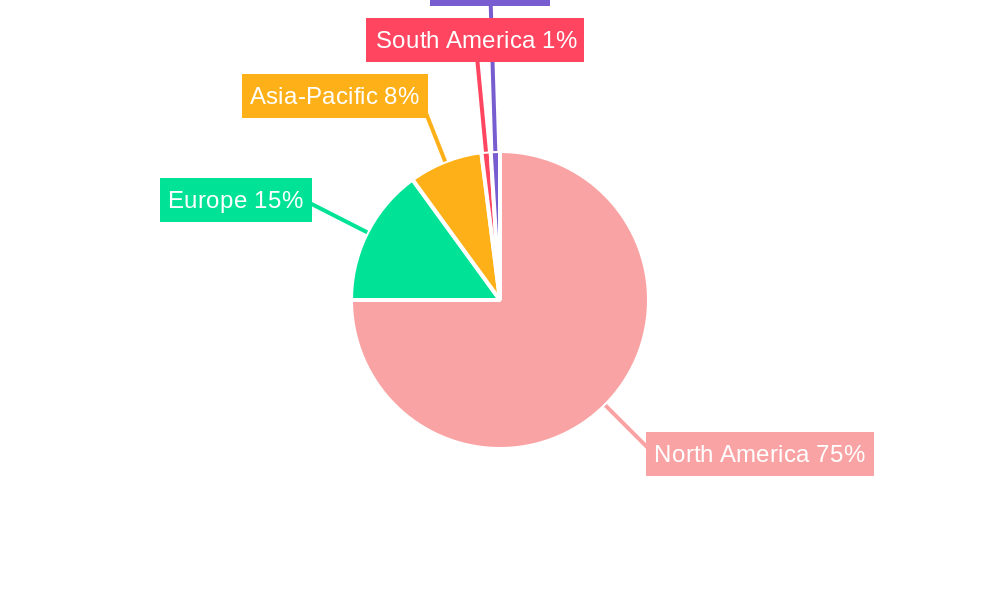

North America Fertilizer Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Fertilizer Industry Regional Market Share

Geographic Coverage of North America Fertilizer Industry

North America Fertilizer Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.13% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Nitrogen Fertilizers

- 5.1.2. Phosphate Fertilizers

- 5.1.3. Potash Fertilizers

- 5.1.4. Micronutrient Fertilizers

- 5.1.5. Organic Fertilizers

- 5.2. Market Analysis, Insights and Forecast - by Formulation

- 5.2.1. Liquid

- 5.2.2. Granular

- 5.2.3. Powder

- 5.2.4. Pellets

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Agriculture

- 5.3.2. Horticulture

- 5.3.3. Gardening

- 5.3.4. Others

- 5.4. Market Analysis, Insights and Forecast - by Sales Channel

- 5.4.1. Direct Sales

- 5.4.2. Distributors and Wholesalers

- 5.4.3. Online

- 5.4.4. Others

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Fertilizer Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Nitrogen Fertilizers

- 6.1.2. Phosphate Fertilizers

- 6.1.3. Potash Fertilizers

- 6.1.4. Micronutrient Fertilizers

- 6.1.5. Organic Fertilizers

- 6.2. Market Analysis, Insights and Forecast - by Formulation

- 6.2.1. Liquid

- 6.2.2. Granular

- 6.2.3. Powder

- 6.2.4. Pellets

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Agriculture

- 6.3.2. Horticulture

- 6.3.3. Gardening

- 6.3.4. Others

- 6.4. Market Analysis, Insights and Forecast - by Sales Channel

- 6.4.1. Direct Sales

- 6.4.2. Distributors and Wholesalers

- 6.4.3. Online

- 6.4.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Nutrien Ltd.

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 CF Industries Holdings Inc.

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 The Mosaic Company

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Yara International ASA

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 The Andersons Inc.

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 ICL Group Ltd.

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Koch Industries Inc.

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Haifa Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Sociedad Química y Minera de Chile (SQM)

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Wilbur-Ellis Company LLC

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Compass Minerals

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 OCP Group

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Others

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 Nutrien Ltd.

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Fertilizer Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Fertilizer Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Fertilizer Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: North America Fertilizer Industry Revenue billion Forecast, by Formulation 2020 & 2033

- Table 3: North America Fertilizer Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 4: North America Fertilizer Industry Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 5: North America Fertilizer Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: North America Fertilizer Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 7: North America Fertilizer Industry Revenue billion Forecast, by Formulation 2020 & 2033

- Table 8: North America Fertilizer Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 9: North America Fertilizer Industry Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 10: North America Fertilizer Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States North America Fertilizer Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada North America Fertilizer Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico North America Fertilizer Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Fertilizer Industry?

The projected CAGR is approximately 5.13%.

2. Which companies are prominent players in the North America Fertilizer Industry?

Key companies in the market include Nutrien Ltd., CF Industries Holdings, Inc., The Mosaic Company, Yara International ASA, The Andersons, Inc., ICL Group Ltd., Koch Industries, Inc., Haifa Group, Sociedad Química y Minera de Chile (SQM), Wilbur-Ellis Company LLC, Compass Minerals, OCP Group, Others.

3. What are the main segments of the North America Fertilizer Industry?

The market segments include Type, Formulation, Application, Sales Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 63.76 billion as of 2022.

5. What are some drivers contributing to market growth?

Awareness of Landscaping Maintenance; Technological Advancements.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Shortage of Skilled Labor; Wastage of High Amount of Water For Irrigating Lawns.

8. Can you provide examples of recent developments in the market?

January 2023: ICL has entered into a strategic partnership agreement with General Mills, in which it will be the supplier of strategic specialty phosphate solutions to General Mills. The long-term agreement will also focus on international expansion.October 2022: The Andersons entered into an agreement to acquire the assets of Mote Farm Service, Inc. to expand thier retail farm center network.August 2022: Koch invested around USD 30 million in the Kansas nitrogen plant to increase UAN production by 35,000 tons per year to meet growing UAN demand across western Kansas and eastern Colorado.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Fertilizer Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Fertilizer Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Fertilizer Industry?

To stay informed about further developments, trends, and reports in the North America Fertilizer Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence