Key Insights into the Auto-steer System for Agriculture Market

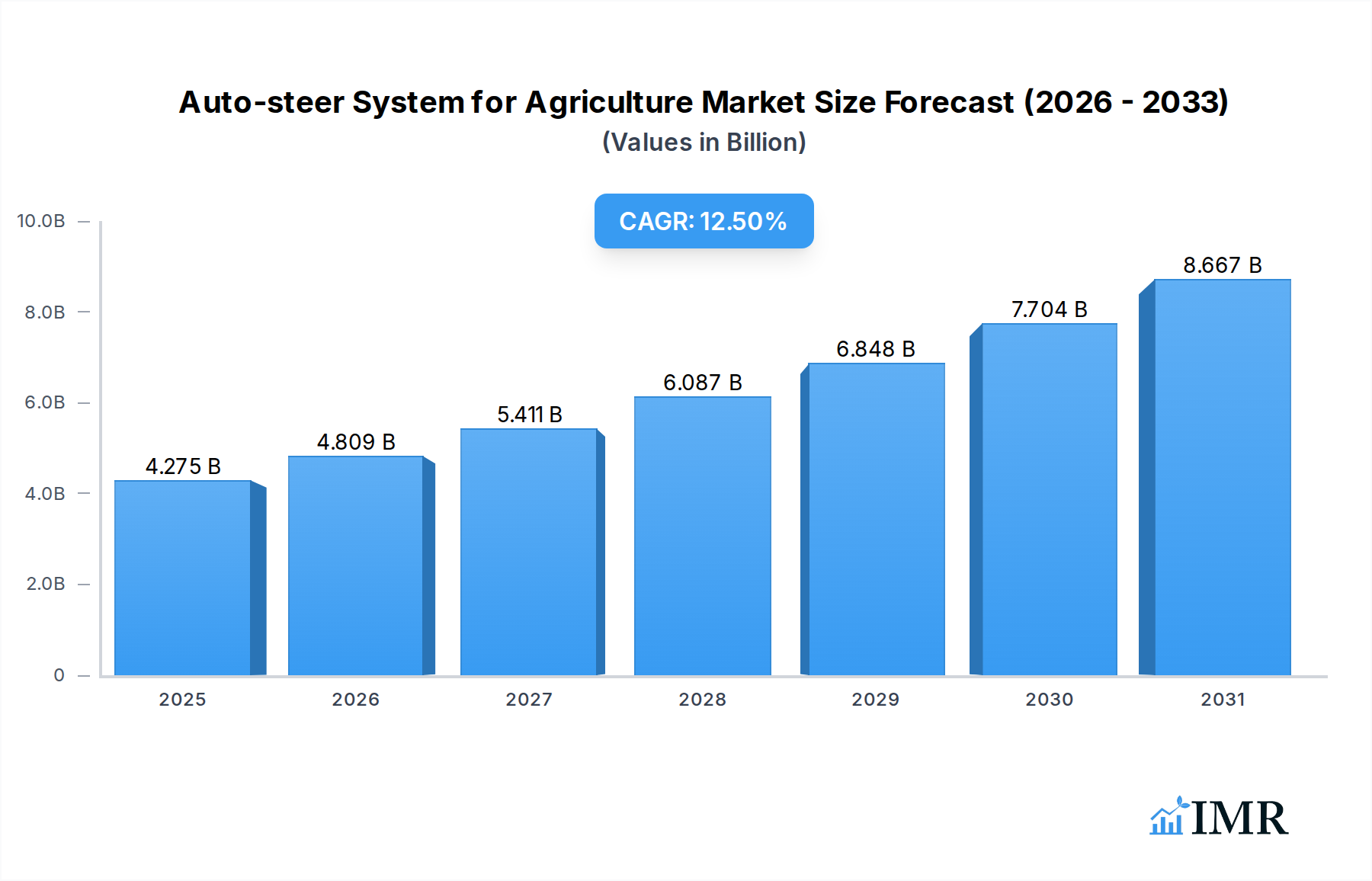

The Global Auto-steer System for Agriculture Market was valued at an estimated $3.8 billion in 2024. Projections indicate a robust expansion, with the market expected to reach approximately $12.34 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 12.5% over the forecast period. This significant growth trajectory is underpinned by an escalating global demand for agricultural efficiency, optimized resource utilization, and enhanced farm productivity. Key demand drivers include the pervasive challenge of labor shortages in the agricultural sector, the imperative to reduce operational costs associated with fuel and inputs, and the increasing adoption of advanced farming techniques to meet rising food demand.

Auto-steer System for Agriculture Market Size (In Billion)

Macroeconomic tailwinds, such as favorable government subsidies and policies promoting modern agricultural technologies, particularly in developing economies, further stimulate market penetration. The integration of auto-steer systems with broader precision agriculture frameworks is transforming traditional farming practices, allowing for more precise field operations, minimized overlap, and improved crop yields. These systems, utilizing technologies like GPS/GNSS and RTK, enable farm machinery to navigate fields with unparalleled accuracy, significantly reducing operator fatigue and increasing the operational window. The increasing sophistication of hardware components, including advanced GPS/GNSS Receivers Market offerings, along with innovations in accompanying software, positions the Auto-steer System for Agriculture Market as a critical component of future food security strategies. Furthermore, the growing awareness among farmers regarding the long-term economic and environmental benefits, such as reduced carbon footprint and optimized pesticide/fertilizer application, is fueling consistent demand. The aftermarket segment also plays a crucial role, allowing existing farm equipment to be retrofitted with auto-steer capabilities, thereby democratizing access to this transformative technology for a wider base of farmers, from individual operators to large-scale commercial farming enterprises.

Auto-steer System for Agriculture Company Market Share

GNSS-Based Technology Dominance in the Auto-steer System for Agriculture Market

Within the Auto-steer System for Agriculture Market, the GNSS-Based technology segment stands out as the dominant force, commanding the largest revenue share. This segment’s supremacy is attributed primarily to its foundational role in providing the high-precision positioning data essential for automated steering. Global Navigation Satellite Systems (GNSS), encompassing GPS, GLONASS, Galileo, and BeiDou, offer the ubiquitous and reliable satellite signals necessary for guiding agricultural machinery with centimeter-level accuracy, especially when augmented by Real-Time Kinematic (RTK) or Precise Point Positioning (PPP) corrections. The inherent reliability, widespread availability, and continuous advancements in GNSS technology make it the preferred choice for auto-steer applications, ranging from basic parallel tracking to fully autonomous operations.

The dominance of GNSS-based systems stems from their ability to deliver consistent and repeatable pass-to-pass accuracy, which is critical for operations like planting, spraying, and harvesting. This precision minimizes overlap and skips, leading to significant reductions in fuel consumption, fertilizer, pesticide, and seed waste. Companies like John Deere, Trimble, and Topcon Positioning Systems have heavily invested in developing sophisticated GNSS-based solutions, integrating them seamlessly into their flagship agricultural machinery and aftermarket kits. These industry leaders continually push the boundaries of accuracy and user-friendliness, fostering broader adoption. The evolution of RTK-guided systems, in particular, has cemented the segment's lead, offering sub-inch accuracy crucial for high-value crops and specialized farming practices. While other technologies, such as satellite-based systems and Inertial Measurement Units (IMUs), contribute to the overall system robustness, they often complement or enhance GNSS rather than replace it.

Furthermore, the integration of GNSS with advanced mapping and Precision Farming Software Market solutions allows for dynamic adjustments to steering paths based on real-time field data, soil conditions, and crop health. This holistic approach reinforces the segment's leadership by offering comprehensive solutions that extend beyond mere steering assistance to full-spectrum precision farming. The segment's share is expected to remain dominant, propelled by ongoing technological refinements, such as multi-frequency GNSS receivers and robust correction service networks, which enhance accuracy and reliability even in challenging environments. The increasing adoption of auto-steer systems across all vehicle types, from tractors to agricultural sprayers, further solidifies the foundational role of GNSS-based technology in the Auto-steer System for Agriculture Market.

Key Market Drivers and Constraints in the Auto-steer System for Agriculture Market

The Auto-steer System for Agriculture Market is shaped by several powerful drivers and notable constraints, each influencing its growth trajectory.

Drivers:

- Enhanced Operational Efficiency and Input Cost Reduction: A primary driver is the agricultural sector's relentless pursuit of efficiency. Auto-steer systems enable farmers to achieve greater precision in field operations, reducing overlap during planting, spraying, and harvesting. This precision directly translates to significant savings. For instance, studies indicate that auto-steer systems can reduce fuel consumption by 10-15% and optimize the use of fertilizers, pesticides, and seeds by 5-10%, directly impacting the profitability of farming operations and thus driving the Auto-steer System for Agriculture Market. The desire to minimize these variable costs is a compelling factor for adoption, particularly for large-scale commercial farming.

- Addressing Labor Shortages: Agriculture globally faces persistent labor shortages, making automation a critical solution. Auto-steer systems reduce the demanding workload on operators, allowing them to monitor other aspects of equipment performance rather than constantly steering. This not only mitigates the impact of labor scarcity but also enhances worker productivity and reduces fatigue, making agricultural jobs more attractive and sustainable. The integration of auto-steer technology with broader Agricultural Robotics Market initiatives further amplifies this impact.

- Government Support and Subsidies for Precision Agriculture: Many governments worldwide are actively promoting the adoption of precision agriculture technologies through subsidies, grants, and favorable policies. These initiatives aim to boost food security, improve environmental sustainability, and enhance national agricultural competitiveness. For example, programs in the European Union and the United States often offer financial incentives for farmers investing in technologies like auto-steer systems, thereby lowering the initial investment barrier and accelerating market uptake.

Constraints:

- High Initial Investment Costs: Despite long-term benefits, the upfront cost of acquiring and integrating sophisticated auto-steer systems can be substantial. For smaller farms or those in regions with limited capital access, this high initial outlay acts as a significant deterrent. The cost of advanced components, such as high-accuracy GNSS Receivers Market and steering controllers, can represent a considerable investment, limiting widespread adoption in certain farmer segments.

- Connectivity and Infrastructure Limitations: The optimal performance of advanced auto-steer systems, particularly those relying on RTK correction signals, requires robust and reliable connectivity. Many rural and remote agricultural areas lack adequate cellular or internet infrastructure, hindering the seamless operation and data transmission capabilities essential for RTK-guided systems. This infrastructural gap can lead to signal loss and reduced accuracy, impacting the efficacy of the Auto-steer System for Agriculture Market in such regions. Furthermore, the reliance on high-quality Agricultural Sensors Market inputs for decision-making also mandates reliable data infrastructure.

Competitive Ecosystem of Auto-steer System for Agriculture Market

The Auto-steer System for Agriculture Market is characterized by a mix of established agricultural machinery giants and specialized precision technology providers. Competition revolves around accuracy, ease of integration, cost-effectiveness, and the breadth of compatible equipment.

- John Deere: A leading global manufacturer of agricultural machinery, John Deere offers integrated auto-steer solutions, including its AutoTrac system, deeply embedded into its tractor and harvester platforms, emphasizing seamless operation and advanced connectivity.

- Trimble: A prominent provider of advanced positioning technologies, Trimble offers a comprehensive suite of auto-steer solutions, including GPS/GNSS receivers, displays, and steering controllers, catering to both OEM and aftermarket segments with a focus on high-precision applications.

- Topcon Positioning Systems: Known for its robust and accurate GNSS-based solutions, Topcon provides a range of auto-steer products and services, including its AGI-4 receiver and AES-35 electric steering system, serving a global agricultural client base.

- Ag Leader Technology: Specializes in precision farming solutions, offering a variety of auto-steer kits, displays, and sensors designed for various machinery types, with an emphasis on user-friendly interfaces and versatile integration.

- Raven Industries: A diversified technology company, Raven Industries provides advanced precision agriculture products, including guidance and steering systems, booms, and spray controls, focusing on optimizing application accuracy for diverse farming operations.

- AgJunction: A pure-play precision agriculture company, AgJunction develops auto-steer solutions and related technologies, including machine control and guidance products, with a focus on open architecture and compatibility.

- Patchwork: Offers a range of farm management and precision agriculture tools, including auto-steer systems, aiming to provide practical and cost-effective solutions for enhancing farm efficiency.

- CNH Industrial: A global capital goods company, CNH Industrial (parent of brands like Case IH and New Holland Agriculture) integrates proprietary and third-party auto-steer technologies into its extensive line of agricultural machinery, emphasizing productivity and sustainability.

- AGCO Corporation: A major global manufacturer of agricultural equipment, AGCO offers its Fuse Technologies platform, which includes auto-steer and guidance systems, aiming to provide a connected farm ecosystem across its various brands.

- FieldBee: Provides affordable and accessible RTK GPS systems and auto-steer solutions, targeting smaller farms and those seeking to adopt precision agriculture technologies without significant upfront investment.

- ARAG: Focuses on spraying components and solutions, including guidance systems that integrate with auto-steer technology to optimize the precision and efficiency of agricultural sprayers.

- Homburg Holland: A specialist in drainage solutions, Homburg Holland also offers precision agriculture products, including auto-steer systems, to support efficient land management and cultivation.

- Sveaverken Svea Agri: A European provider of agricultural equipment, Sveaverken also offers precision farming tools, including auto-steer systems, to improve the efficiency of various farm tasks.

- Geometer International: Develops GPS/GNSS receivers and precision farming software solutions, often integrated with auto-steer capabilities, catering to a range of agricultural applications.

- Hexagon Agriculture: Part of Hexagon AB, this division offers integrated precision agriculture solutions, including auto-steer, guidance, and machine control systems, leveraging advanced geospatial technology.

- Reichhardt: Specializes in steering systems for agricultural machinery, offering highly precise and robust auto-steer solutions compatible with a wide array of tractor brands and implements.

- Rostselmash: A major Russian manufacturer of agricultural machinery, Rostselmash integrates modern guidance and auto-steer systems into its combines and tractors to enhance operational efficiency.

- FJDynamics: A technology company that develops intelligent agricultural solutions, including auto-steer systems, focusing on smart farming and automation for various farming operations.

- SMAJAYU(SHENZHEN): Provides innovative GNSS positioning solutions and related hardware for various applications, including precision agriculture and auto-steer systems.

- ComNav Technology: Offers high-precision GNSS OEM boards and receivers, which are critical components for auto-steer systems, supporting applications requiring centimeter-level accuracy.

- CP Device: Develops and manufactures GPS/GNSS receivers and modules, providing essential hardware components that are integrated into various auto-steer system for agriculture market offerings.

Recent Developments & Milestones in the Auto-steer System for Agriculture Market

The Auto-steer System for Agriculture Market has seen continuous innovation and strategic collaborations, reflecting its dynamic growth.

- November 2024: John Deere launched its next-generation AutoTrac™ guidance system with enhanced machine learning capabilities for improved path planning in varied terrain, further solidifying its position in the Precision Agriculture Market.

- September 2024: Trimble announced a strategic partnership with a major satellite communication provider to expand the reach and reliability of its RTK correction services in remote agricultural regions, addressing critical connectivity challenges.

- July 2024: Topcon Positioning Systems unveiled new software updates for its auto-steer solutions, introducing advanced implement control features for better integration with various agricultural tools and significantly enhancing the efficiency of the Agricultural Machinery Market.

- May 2025: Ag Leader Technology introduced a new line of compact, retrofittable auto-steer kits designed specifically for older tractor models, aiming to broaden access to precision guidance for small to medium-sized farms.

- March 2025: Raven Industries showcased its latest integrated system combining auto-steer with intelligent boom control for agricultural sprayers, optimizing chemical application and demonstrating a significant stride in the Agricultural Sprayers Market.

- January 2025: A consortium of leading agricultural technology companies, including Hexagon Agriculture and FJDynamics, received a substantial grant to accelerate research and development in fully autonomous agricultural robotics, hinting at future advancements in the Agricultural Robotics Market.

- December 2024: FieldBee expanded its European distribution network, making its affordable RTK GPS and auto-steer solutions more accessible to individual farmers and smaller cooperative enterprises across several new markets.

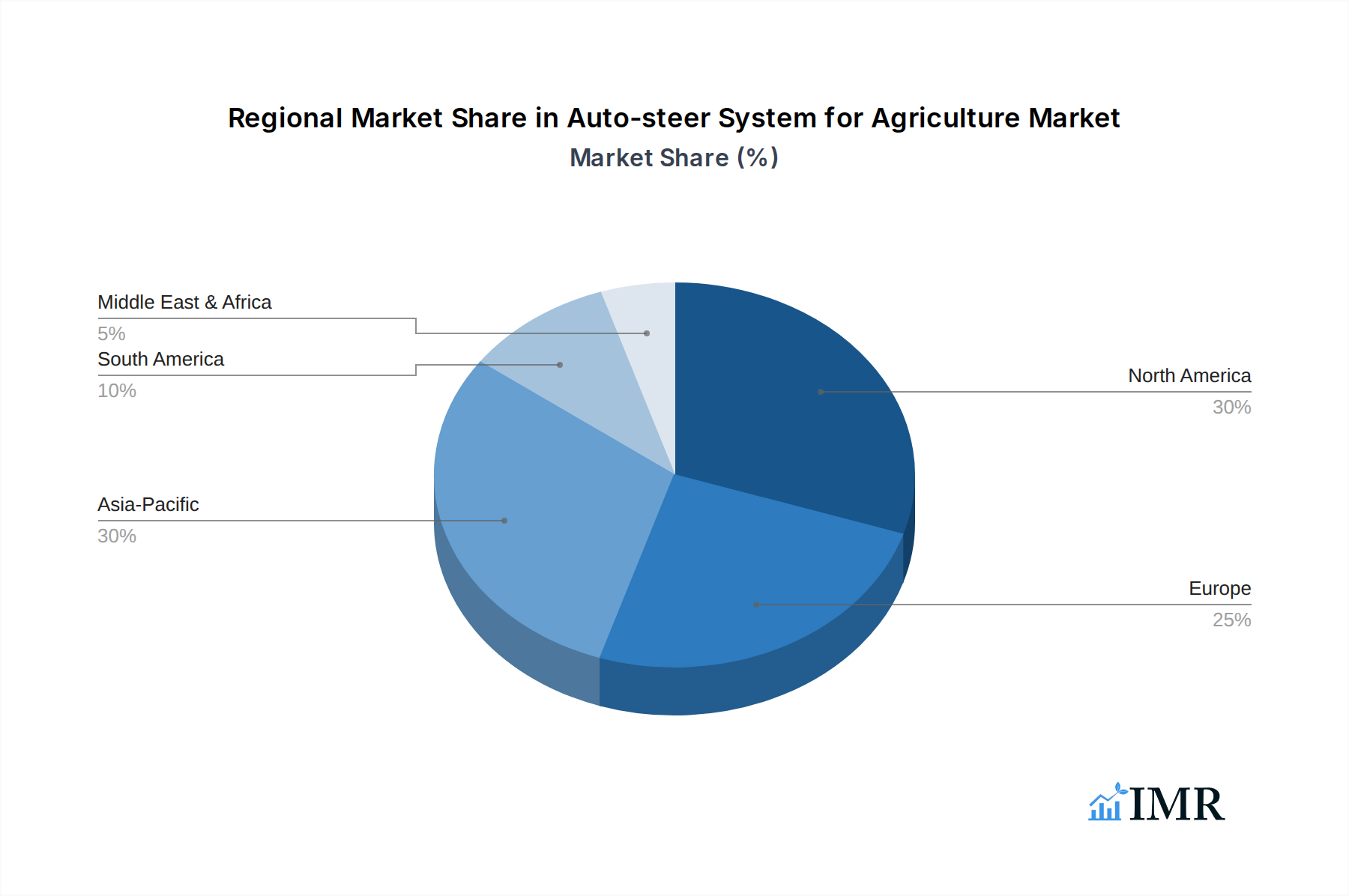

Regional Market Breakdown for the Auto-steer System for Agriculture Market

The Auto-steer System for Agriculture Market exhibits distinct regional dynamics, influenced by varying agricultural practices, technological adoption rates, and economic conditions across key geographies.

North America holds a significant share of the global Auto-steer System for Agriculture Market, estimated to account for roughly 35-40% of the revenue in 2024. The region is characterized by large farm sizes, high mechanization levels, and an early adoption of precision agriculture technologies. Demand is primarily driven by the imperative for efficient operations, particularly in large-scale commercial farming enterprises, and the availability of sophisticated infrastructure for GNSS correction services. The presence of key market players and a robust dealer network further supports market growth in this mature region.

Europe is another substantial market, driven by stringent environmental regulations, government support for sustainable farming practices, and the increasing cost of labor. Countries like Germany, France, and the UK are at the forefront of adopting auto-steer systems, fueled by policies under the Common Agricultural Policy (CAP) that incentivize precision farming. The emphasis on resource efficiency and environmental stewardship provides a strong impetus for growth, with a steady CAGR reflecting continuous innovation and farmer education.

Asia Pacific is poised to be the fastest-growing region in the Auto-steer System for Agriculture Market, projected to exhibit a CAGR potentially exceeding 15% over the forecast period. This rapid expansion is attributed to increasing mechanization in countries like China and India, the fragmentation of land holdings gradually consolidating into larger commercial farms, and strong government support for agricultural modernization. As farmers in these regions seek to improve yields and reduce manual labor, the demand for cost-effective auto-steer solutions, often through aftermarket channels, is surging. The region is also becoming a hub for manufacturing and innovation in agricultural sensors and related hardware, driving the Agricultural Sensors Market.

South America, particularly Brazil and Argentina, represents an emerging market with significant growth potential. The region's vast agricultural lands and focus on export-oriented farming necessitate high levels of efficiency and productivity. Increasing investment in agricultural infrastructure and technology, coupled with the need to optimize input usage on large plantations, is driving the adoption of auto-steer systems. While still in an earlier stage of adoption compared to North America and Europe, the region is rapidly catching up, demonstrating robust year-on-year growth.

Auto-steer System for Agriculture Regional Market Share

Technology Innovation Trajectory in the Auto-steer System for Agriculture Market

The Auto-steer System for Agriculture Market is on a trajectory of profound technological innovation, primarily driven by advancements in sensor technology, artificial intelligence (AI), and enhanced connectivity. The convergence of these technologies is paving the way for more autonomous, precise, and adaptive farming solutions.

One of the most disruptive emerging technologies is the integration of AI and Machine Learning (ML) for enhanced path planning and obstacle detection. Current auto-steer systems rely heavily on pre-programmed paths or real-time GNSS data. However, AI/ML algorithms, leveraging data from various agricultural sensors, can learn to optimize paths in dynamic field conditions, predict machinery behavior, and detect unexpected obstacles (e.g., rocks, wildlife, fallen branches) with greater accuracy. This enables more sophisticated decision-making at the edge, reducing human intervention and increasing safety. Adoption timelines for advanced AI-driven autonomy are in the medium to long term (5-10 years), requiring significant R&D investment by major players like John Deere and Trimble. These advancements threaten incumbent models that rely solely on GNSS guidance, pushing for more integrated, intelligent systems and significantly enhancing the capabilities of the overall Agricultural Machinery Market.

Another critical innovation is the widespread adoption and refinement of Real-Time Kinematic (RTK) and Precise Point Positioning (PPP) GNSS solutions. While RTK is already prevalent, advancements in network RTK (NRTK) and the rollout of more robust PPP services, which do not require a local base station, are expanding ultra-high precision guidance to more remote areas. These technologies offer centimeter-level accuracy, crucial for tasks like strip-tillage, precision planting, and controlled traffic farming, which demand exact repeatability year after year. R&D investments are focusing on improving signal robustness, reducing latency, and creating more cost-effective receivers for broader penetration within the GNSS Receivers Market. These innovations reinforce the value proposition of auto-steer systems by delivering unparalleled precision, making them indispensable for high-value crop production and resource optimization. This directly impacts the efficiency and output of the Commercial Farming Market.

Finally, the proliferation of the Internet of Things (IoT) in Agriculture Market is fundamentally changing how auto-steer systems operate. IoT sensors on machinery, implements, and even in the soil provide a constant stream of data that can be fed into auto-steer algorithms. This data-driven approach allows for dynamic adjustments to steering parameters based on real-time feedback regarding soil moisture, nutrient levels, and crop health. The enhanced connectivity facilitates cloud-based processing and remote monitoring, enabling predictive maintenance and optimized fleet management. Adoption of IoT integration is already underway and rapidly accelerating, with R&D focused on interoperability standards and secure data transmission. This trend reinforces incumbent business models by enabling them to offer more comprehensive, data-rich solutions, effectively transforming auto-steer from a standalone function into an integral part of a connected, smart farm ecosystem, further supporting the broader Precision Farming Software Market.

Regulatory & Policy Landscape Shaping the Auto-steer System for Agriculture Market

The Auto-steer System for Agriculture Market is increasingly influenced by a complex web of regulatory frameworks, technical standards, and government policies across key agricultural regions. These regulations often aim to balance agricultural productivity with environmental sustainability, worker safety, and data privacy.

Globally, ISO standards for agricultural machinery play a crucial role in shaping the development and interoperability of auto-steer systems. Standards such as ISO 11783 (ISOBUS) facilitate communication between tractors, implements, and software, ensuring that auto-steer components from different manufacturers can work together seamlessly. Compliance with these standards promotes market growth by reducing barriers to adoption and fostering a more competitive environment. Additionally, regulations around electromagnetic compatibility (EMC) ensure that electronic components within auto-steer systems do not interfere with other critical equipment or communication signals, which is vital for the reliability of high-precision GNSS Receivers Market.

In the European Union, the Common Agricultural Policy (CAP) is a significant driver. CAP reforms often include provisions and subsidies that incentivize farmers to adopt precision agriculture technologies, including auto-steer systems, to meet environmental objectives (e.g., reduced chemical use, soil health protection) and enhance competitiveness. The EU's focus on data privacy, particularly under GDPR, also has implications for farm data collected by auto-steer systems and integrated Precision Farming Software Market. Manufacturers must ensure secure data handling and transparency regarding data ownership and usage, which can influence product design and service offerings.

In North America, particularly the United States, the Farm Bill provides various programs and grants that support the adoption of new agricultural technologies. Federal and state-level initiatives often fund research into precision agriculture and offer cost-sharing programs for farmers investing in equipment like auto-steer systems. Regulations related to spectrum allocation for GNSS signals are also critical, ensuring the availability and reliability of the satellite signals essential for these systems. Concerns around cybersecurity in agricultural technology are emerging, prompting discussions and potential future regulations regarding the protection of farm data and operational integrity.

In Asia Pacific, governments in countries like China and India are aggressively promoting agricultural mechanization and modernization through subsidies and policy support. For example, direct financial assistance for purchasing agricultural machinery, including those equipped with auto-steer, is common. While specific regulations on auto-steer systems are still evolving in many parts of the region, the general policy direction strongly favors technology adoption to enhance food security and rural incomes. These policy changes are projected to have a positive market impact, accelerating the uptake of auto-steer systems, particularly in the rapidly expanding Commercial Farming Market, and fostering local innovation in related sectors like the Agricultural Sensors Market.

Auto-steer System for Agriculture Segmentation

-

1. Component

-

1.1. Hardware

- 1.1.1. GPS/GNSS Receivers

- 1.1.2. Steering Controllers

- 1.1.3. Sensors

- 1.1.4. Displays & Monitors

- 1.1.5. Antennas

- 1.1.6. Others

- 1.2. Software

-

1.1. Hardware

-

2. Technology

- 2.1. GNSS-Based

- 2.2. RTK-Guided

- 2.3. Satellite-Based

- 2.4. Others

-

3. Vehicle Type

- 3.1. Tractors

- 3.2. Harvesters

- 3.3. Sprayers

- 3.4. Seeders & Planters

- 3.5. Others

-

4. Sales Channel

- 4.1. OEM

- 4.2. Aftermarket

-

5. End User

- 5.1. Individual Farmers

- 5.2. Commercial Farming Enterprises

- 5.3. Agricultural Cooperatives

- 5.4. Others

Auto-steer System for Agriculture Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Auto-steer System for Agriculture Regional Market Share

Geographic Coverage of Auto-steer System for Agriculture

Auto-steer System for Agriculture REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.1.1. GPS/GNSS Receivers

- 5.1.1.2. Steering Controllers

- 5.1.1.3. Sensors

- 5.1.1.4. Displays & Monitors

- 5.1.1.5. Antennas

- 5.1.1.6. Others

- 5.1.2. Software

- 5.1.1. Hardware

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. GNSS-Based

- 5.2.2. RTK-Guided

- 5.2.3. Satellite-Based

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.3.1. Tractors

- 5.3.2. Harvesters

- 5.3.3. Sprayers

- 5.3.4. Seeders & Planters

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by Sales Channel

- 5.4.1. OEM

- 5.4.2. Aftermarket

- 5.5. Market Analysis, Insights and Forecast - by End User

- 5.5.1. Individual Farmers

- 5.5.2. Commercial Farming Enterprises

- 5.5.3. Agricultural Cooperatives

- 5.5.4. Others

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 5.6.2. South America

- 5.6.3. Europe

- 5.6.4. Middle East & Africa

- 5.6.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Global Auto-steer System for Agriculture Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Hardware

- 6.1.1.1. GPS/GNSS Receivers

- 6.1.1.2. Steering Controllers

- 6.1.1.3. Sensors

- 6.1.1.4. Displays & Monitors

- 6.1.1.5. Antennas

- 6.1.1.6. Others

- 6.1.2. Software

- 6.1.1. Hardware

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. GNSS-Based

- 6.2.2. RTK-Guided

- 6.2.3. Satellite-Based

- 6.2.4. Others

- 6.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.3.1. Tractors

- 6.3.2. Harvesters

- 6.3.3. Sprayers

- 6.3.4. Seeders & Planters

- 6.3.5. Others

- 6.4. Market Analysis, Insights and Forecast - by Sales Channel

- 6.4.1. OEM

- 6.4.2. Aftermarket

- 6.5. Market Analysis, Insights and Forecast - by End User

- 6.5.1. Individual Farmers

- 6.5.2. Commercial Farming Enterprises

- 6.5.3. Agricultural Cooperatives

- 6.5.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. North America Auto-steer System for Agriculture Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Hardware

- 7.1.1.1. GPS/GNSS Receivers

- 7.1.1.2. Steering Controllers

- 7.1.1.3. Sensors

- 7.1.1.4. Displays & Monitors

- 7.1.1.5. Antennas

- 7.1.1.6. Others

- 7.1.2. Software

- 7.1.1. Hardware

- 7.2. Market Analysis, Insights and Forecast - by Technology

- 7.2.1. GNSS-Based

- 7.2.2. RTK-Guided

- 7.2.3. Satellite-Based

- 7.2.4. Others

- 7.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.3.1. Tractors

- 7.3.2. Harvesters

- 7.3.3. Sprayers

- 7.3.4. Seeders & Planters

- 7.3.5. Others

- 7.4. Market Analysis, Insights and Forecast - by Sales Channel

- 7.4.1. OEM

- 7.4.2. Aftermarket

- 7.5. Market Analysis, Insights and Forecast - by End User

- 7.5.1. Individual Farmers

- 7.5.2. Commercial Farming Enterprises

- 7.5.3. Agricultural Cooperatives

- 7.5.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. South America Auto-steer System for Agriculture Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Hardware

- 8.1.1.1. GPS/GNSS Receivers

- 8.1.1.2. Steering Controllers

- 8.1.1.3. Sensors

- 8.1.1.4. Displays & Monitors

- 8.1.1.5. Antennas

- 8.1.1.6. Others

- 8.1.2. Software

- 8.1.1. Hardware

- 8.2. Market Analysis, Insights and Forecast - by Technology

- 8.2.1. GNSS-Based

- 8.2.2. RTK-Guided

- 8.2.3. Satellite-Based

- 8.2.4. Others

- 8.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.3.1. Tractors

- 8.3.2. Harvesters

- 8.3.3. Sprayers

- 8.3.4. Seeders & Planters

- 8.3.5. Others

- 8.4. Market Analysis, Insights and Forecast - by Sales Channel

- 8.4.1. OEM

- 8.4.2. Aftermarket

- 8.5. Market Analysis, Insights and Forecast - by End User

- 8.5.1. Individual Farmers

- 8.5.2. Commercial Farming Enterprises

- 8.5.3. Agricultural Cooperatives

- 8.5.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. Europe Auto-steer System for Agriculture Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Hardware

- 9.1.1.1. GPS/GNSS Receivers

- 9.1.1.2. Steering Controllers

- 9.1.1.3. Sensors

- 9.1.1.4. Displays & Monitors

- 9.1.1.5. Antennas

- 9.1.1.6. Others

- 9.1.2. Software

- 9.1.1. Hardware

- 9.2. Market Analysis, Insights and Forecast - by Technology

- 9.2.1. GNSS-Based

- 9.2.2. RTK-Guided

- 9.2.3. Satellite-Based

- 9.2.4. Others

- 9.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.3.1. Tractors

- 9.3.2. Harvesters

- 9.3.3. Sprayers

- 9.3.4. Seeders & Planters

- 9.3.5. Others

- 9.4. Market Analysis, Insights and Forecast - by Sales Channel

- 9.4.1. OEM

- 9.4.2. Aftermarket

- 9.5. Market Analysis, Insights and Forecast - by End User

- 9.5.1. Individual Farmers

- 9.5.2. Commercial Farming Enterprises

- 9.5.3. Agricultural Cooperatives

- 9.5.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. Middle East & Africa Auto-steer System for Agriculture Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Component

- 10.1.1. Hardware

- 10.1.1.1. GPS/GNSS Receivers

- 10.1.1.2. Steering Controllers

- 10.1.1.3. Sensors

- 10.1.1.4. Displays & Monitors

- 10.1.1.5. Antennas

- 10.1.1.6. Others

- 10.1.2. Software

- 10.1.1. Hardware

- 10.2. Market Analysis, Insights and Forecast - by Technology

- 10.2.1. GNSS-Based

- 10.2.2. RTK-Guided

- 10.2.3. Satellite-Based

- 10.2.4. Others

- 10.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.3.1. Tractors

- 10.3.2. Harvesters

- 10.3.3. Sprayers

- 10.3.4. Seeders & Planters

- 10.3.5. Others

- 10.4. Market Analysis, Insights and Forecast - by Sales Channel

- 10.4.1. OEM

- 10.4.2. Aftermarket

- 10.5. Market Analysis, Insights and Forecast - by End User

- 10.5.1. Individual Farmers

- 10.5.2. Commercial Farming Enterprises

- 10.5.3. Agricultural Cooperatives

- 10.5.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Component

- 11. Asia Pacific Auto-steer System for Agriculture Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Component

- 11.1.1. Hardware

- 11.1.1.1. GPS/GNSS Receivers

- 11.1.1.2. Steering Controllers

- 11.1.1.3. Sensors

- 11.1.1.4. Displays & Monitors

- 11.1.1.5. Antennas

- 11.1.1.6. Others

- 11.1.2. Software

- 11.1.1. Hardware

- 11.2. Market Analysis, Insights and Forecast - by Technology

- 11.2.1. GNSS-Based

- 11.2.2. RTK-Guided

- 11.2.3. Satellite-Based

- 11.2.4. Others

- 11.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 11.3.1. Tractors

- 11.3.2. Harvesters

- 11.3.3. Sprayers

- 11.3.4. Seeders & Planters

- 11.3.5. Others

- 11.4. Market Analysis, Insights and Forecast - by Sales Channel

- 11.4.1. OEM

- 11.4.2. Aftermarket

- 11.5. Market Analysis, Insights and Forecast - by End User

- 11.5.1. Individual Farmers

- 11.5.2. Commercial Farming Enterprises

- 11.5.3. Agricultural Cooperatives

- 11.5.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Component

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 John Deere

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Trimble

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Topcon Positioning Systems

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Ag Leader Technology

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Raven Industries

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 AgJunction

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Patchwork

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 CNH Industrial

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 AGCO Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 FieldBee

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 ARAG

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Homburg Holland

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Sveaverken Svea Agri

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Geometer International

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Hexagon Agriculture

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Reichhardt

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Rostselmash

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 FJDynamics

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 SMAJAYU(SHENZHEN)

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 ComNav Technology

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 CP Device

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.1 John Deere

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Auto-steer System for Agriculture Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Auto-steer System for Agriculture Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Auto-steer System for Agriculture Revenue (billion), by Component 2025 & 2033

- Figure 4: North America Auto-steer System for Agriculture Volume (K), by Component 2025 & 2033

- Figure 5: North America Auto-steer System for Agriculture Revenue Share (%), by Component 2025 & 2033

- Figure 6: North America Auto-steer System for Agriculture Volume Share (%), by Component 2025 & 2033

- Figure 7: North America Auto-steer System for Agriculture Revenue (billion), by Technology 2025 & 2033

- Figure 8: North America Auto-steer System for Agriculture Volume (K), by Technology 2025 & 2033

- Figure 9: North America Auto-steer System for Agriculture Revenue Share (%), by Technology 2025 & 2033

- Figure 10: North America Auto-steer System for Agriculture Volume Share (%), by Technology 2025 & 2033

- Figure 11: North America Auto-steer System for Agriculture Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 12: North America Auto-steer System for Agriculture Volume (K), by Vehicle Type 2025 & 2033

- Figure 13: North America Auto-steer System for Agriculture Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 14: North America Auto-steer System for Agriculture Volume Share (%), by Vehicle Type 2025 & 2033

- Figure 15: North America Auto-steer System for Agriculture Revenue (billion), by Sales Channel 2025 & 2033

- Figure 16: North America Auto-steer System for Agriculture Volume (K), by Sales Channel 2025 & 2033

- Figure 17: North America Auto-steer System for Agriculture Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 18: North America Auto-steer System for Agriculture Volume Share (%), by Sales Channel 2025 & 2033

- Figure 19: North America Auto-steer System for Agriculture Revenue (billion), by End User 2025 & 2033

- Figure 20: North America Auto-steer System for Agriculture Volume (K), by End User 2025 & 2033

- Figure 21: North America Auto-steer System for Agriculture Revenue Share (%), by End User 2025 & 2033

- Figure 22: North America Auto-steer System for Agriculture Volume Share (%), by End User 2025 & 2033

- Figure 23: North America Auto-steer System for Agriculture Revenue (billion), by Country 2025 & 2033

- Figure 24: North America Auto-steer System for Agriculture Volume (K), by Country 2025 & 2033

- Figure 25: North America Auto-steer System for Agriculture Revenue Share (%), by Country 2025 & 2033

- Figure 26: North America Auto-steer System for Agriculture Volume Share (%), by Country 2025 & 2033

- Figure 27: South America Auto-steer System for Agriculture Revenue (billion), by Component 2025 & 2033

- Figure 28: South America Auto-steer System for Agriculture Volume (K), by Component 2025 & 2033

- Figure 29: South America Auto-steer System for Agriculture Revenue Share (%), by Component 2025 & 2033

- Figure 30: South America Auto-steer System for Agriculture Volume Share (%), by Component 2025 & 2033

- Figure 31: South America Auto-steer System for Agriculture Revenue (billion), by Technology 2025 & 2033

- Figure 32: South America Auto-steer System for Agriculture Volume (K), by Technology 2025 & 2033

- Figure 33: South America Auto-steer System for Agriculture Revenue Share (%), by Technology 2025 & 2033

- Figure 34: South America Auto-steer System for Agriculture Volume Share (%), by Technology 2025 & 2033

- Figure 35: South America Auto-steer System for Agriculture Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 36: South America Auto-steer System for Agriculture Volume (K), by Vehicle Type 2025 & 2033

- Figure 37: South America Auto-steer System for Agriculture Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 38: South America Auto-steer System for Agriculture Volume Share (%), by Vehicle Type 2025 & 2033

- Figure 39: South America Auto-steer System for Agriculture Revenue (billion), by Sales Channel 2025 & 2033

- Figure 40: South America Auto-steer System for Agriculture Volume (K), by Sales Channel 2025 & 2033

- Figure 41: South America Auto-steer System for Agriculture Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 42: South America Auto-steer System for Agriculture Volume Share (%), by Sales Channel 2025 & 2033

- Figure 43: South America Auto-steer System for Agriculture Revenue (billion), by End User 2025 & 2033

- Figure 44: South America Auto-steer System for Agriculture Volume (K), by End User 2025 & 2033

- Figure 45: South America Auto-steer System for Agriculture Revenue Share (%), by End User 2025 & 2033

- Figure 46: South America Auto-steer System for Agriculture Volume Share (%), by End User 2025 & 2033

- Figure 47: South America Auto-steer System for Agriculture Revenue (billion), by Country 2025 & 2033

- Figure 48: South America Auto-steer System for Agriculture Volume (K), by Country 2025 & 2033

- Figure 49: South America Auto-steer System for Agriculture Revenue Share (%), by Country 2025 & 2033

- Figure 50: South America Auto-steer System for Agriculture Volume Share (%), by Country 2025 & 2033

- Figure 51: Europe Auto-steer System for Agriculture Revenue (billion), by Component 2025 & 2033

- Figure 52: Europe Auto-steer System for Agriculture Volume (K), by Component 2025 & 2033

- Figure 53: Europe Auto-steer System for Agriculture Revenue Share (%), by Component 2025 & 2033

- Figure 54: Europe Auto-steer System for Agriculture Volume Share (%), by Component 2025 & 2033

- Figure 55: Europe Auto-steer System for Agriculture Revenue (billion), by Technology 2025 & 2033

- Figure 56: Europe Auto-steer System for Agriculture Volume (K), by Technology 2025 & 2033

- Figure 57: Europe Auto-steer System for Agriculture Revenue Share (%), by Technology 2025 & 2033

- Figure 58: Europe Auto-steer System for Agriculture Volume Share (%), by Technology 2025 & 2033

- Figure 59: Europe Auto-steer System for Agriculture Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 60: Europe Auto-steer System for Agriculture Volume (K), by Vehicle Type 2025 & 2033

- Figure 61: Europe Auto-steer System for Agriculture Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 62: Europe Auto-steer System for Agriculture Volume Share (%), by Vehicle Type 2025 & 2033

- Figure 63: Europe Auto-steer System for Agriculture Revenue (billion), by Sales Channel 2025 & 2033

- Figure 64: Europe Auto-steer System for Agriculture Volume (K), by Sales Channel 2025 & 2033

- Figure 65: Europe Auto-steer System for Agriculture Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 66: Europe Auto-steer System for Agriculture Volume Share (%), by Sales Channel 2025 & 2033

- Figure 67: Europe Auto-steer System for Agriculture Revenue (billion), by End User 2025 & 2033

- Figure 68: Europe Auto-steer System for Agriculture Volume (K), by End User 2025 & 2033

- Figure 69: Europe Auto-steer System for Agriculture Revenue Share (%), by End User 2025 & 2033

- Figure 70: Europe Auto-steer System for Agriculture Volume Share (%), by End User 2025 & 2033

- Figure 71: Europe Auto-steer System for Agriculture Revenue (billion), by Country 2025 & 2033

- Figure 72: Europe Auto-steer System for Agriculture Volume (K), by Country 2025 & 2033

- Figure 73: Europe Auto-steer System for Agriculture Revenue Share (%), by Country 2025 & 2033

- Figure 74: Europe Auto-steer System for Agriculture Volume Share (%), by Country 2025 & 2033

- Figure 75: Middle East & Africa Auto-steer System for Agriculture Revenue (billion), by Component 2025 & 2033

- Figure 76: Middle East & Africa Auto-steer System for Agriculture Volume (K), by Component 2025 & 2033

- Figure 77: Middle East & Africa Auto-steer System for Agriculture Revenue Share (%), by Component 2025 & 2033

- Figure 78: Middle East & Africa Auto-steer System for Agriculture Volume Share (%), by Component 2025 & 2033

- Figure 79: Middle East & Africa Auto-steer System for Agriculture Revenue (billion), by Technology 2025 & 2033

- Figure 80: Middle East & Africa Auto-steer System for Agriculture Volume (K), by Technology 2025 & 2033

- Figure 81: Middle East & Africa Auto-steer System for Agriculture Revenue Share (%), by Technology 2025 & 2033

- Figure 82: Middle East & Africa Auto-steer System for Agriculture Volume Share (%), by Technology 2025 & 2033

- Figure 83: Middle East & Africa Auto-steer System for Agriculture Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 84: Middle East & Africa Auto-steer System for Agriculture Volume (K), by Vehicle Type 2025 & 2033

- Figure 85: Middle East & Africa Auto-steer System for Agriculture Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 86: Middle East & Africa Auto-steer System for Agriculture Volume Share (%), by Vehicle Type 2025 & 2033

- Figure 87: Middle East & Africa Auto-steer System for Agriculture Revenue (billion), by Sales Channel 2025 & 2033

- Figure 88: Middle East & Africa Auto-steer System for Agriculture Volume (K), by Sales Channel 2025 & 2033

- Figure 89: Middle East & Africa Auto-steer System for Agriculture Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 90: Middle East & Africa Auto-steer System for Agriculture Volume Share (%), by Sales Channel 2025 & 2033

- Figure 91: Middle East & Africa Auto-steer System for Agriculture Revenue (billion), by End User 2025 & 2033

- Figure 92: Middle East & Africa Auto-steer System for Agriculture Volume (K), by End User 2025 & 2033

- Figure 93: Middle East & Africa Auto-steer System for Agriculture Revenue Share (%), by End User 2025 & 2033

- Figure 94: Middle East & Africa Auto-steer System for Agriculture Volume Share (%), by End User 2025 & 2033

- Figure 95: Middle East & Africa Auto-steer System for Agriculture Revenue (billion), by Country 2025 & 2033

- Figure 96: Middle East & Africa Auto-steer System for Agriculture Volume (K), by Country 2025 & 2033

- Figure 97: Middle East & Africa Auto-steer System for Agriculture Revenue Share (%), by Country 2025 & 2033

- Figure 98: Middle East & Africa Auto-steer System for Agriculture Volume Share (%), by Country 2025 & 2033

- Figure 99: Asia Pacific Auto-steer System for Agriculture Revenue (billion), by Component 2025 & 2033

- Figure 100: Asia Pacific Auto-steer System for Agriculture Volume (K), by Component 2025 & 2033

- Figure 101: Asia Pacific Auto-steer System for Agriculture Revenue Share (%), by Component 2025 & 2033

- Figure 102: Asia Pacific Auto-steer System for Agriculture Volume Share (%), by Component 2025 & 2033

- Figure 103: Asia Pacific Auto-steer System for Agriculture Revenue (billion), by Technology 2025 & 2033

- Figure 104: Asia Pacific Auto-steer System for Agriculture Volume (K), by Technology 2025 & 2033

- Figure 105: Asia Pacific Auto-steer System for Agriculture Revenue Share (%), by Technology 2025 & 2033

- Figure 106: Asia Pacific Auto-steer System for Agriculture Volume Share (%), by Technology 2025 & 2033

- Figure 107: Asia Pacific Auto-steer System for Agriculture Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 108: Asia Pacific Auto-steer System for Agriculture Volume (K), by Vehicle Type 2025 & 2033

- Figure 109: Asia Pacific Auto-steer System for Agriculture Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 110: Asia Pacific Auto-steer System for Agriculture Volume Share (%), by Vehicle Type 2025 & 2033

- Figure 111: Asia Pacific Auto-steer System for Agriculture Revenue (billion), by Sales Channel 2025 & 2033

- Figure 112: Asia Pacific Auto-steer System for Agriculture Volume (K), by Sales Channel 2025 & 2033

- Figure 113: Asia Pacific Auto-steer System for Agriculture Revenue Share (%), by Sales Channel 2025 & 2033

- Figure 114: Asia Pacific Auto-steer System for Agriculture Volume Share (%), by Sales Channel 2025 & 2033

- Figure 115: Asia Pacific Auto-steer System for Agriculture Revenue (billion), by End User 2025 & 2033

- Figure 116: Asia Pacific Auto-steer System for Agriculture Volume (K), by End User 2025 & 2033

- Figure 117: Asia Pacific Auto-steer System for Agriculture Revenue Share (%), by End User 2025 & 2033

- Figure 118: Asia Pacific Auto-steer System for Agriculture Volume Share (%), by End User 2025 & 2033

- Figure 119: Asia Pacific Auto-steer System for Agriculture Revenue (billion), by Country 2025 & 2033

- Figure 120: Asia Pacific Auto-steer System for Agriculture Volume (K), by Country 2025 & 2033

- Figure 121: Asia Pacific Auto-steer System for Agriculture Revenue Share (%), by Country 2025 & 2033

- Figure 122: Asia Pacific Auto-steer System for Agriculture Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Auto-steer System for Agriculture Revenue billion Forecast, by Component 2020 & 2033

- Table 2: Global Auto-steer System for Agriculture Volume K Forecast, by Component 2020 & 2033

- Table 3: Global Auto-steer System for Agriculture Revenue billion Forecast, by Technology 2020 & 2033

- Table 4: Global Auto-steer System for Agriculture Volume K Forecast, by Technology 2020 & 2033

- Table 5: Global Auto-steer System for Agriculture Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 6: Global Auto-steer System for Agriculture Volume K Forecast, by Vehicle Type 2020 & 2033

- Table 7: Global Auto-steer System for Agriculture Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 8: Global Auto-steer System for Agriculture Volume K Forecast, by Sales Channel 2020 & 2033

- Table 9: Global Auto-steer System for Agriculture Revenue billion Forecast, by End User 2020 & 2033

- Table 10: Global Auto-steer System for Agriculture Volume K Forecast, by End User 2020 & 2033

- Table 11: Global Auto-steer System for Agriculture Revenue billion Forecast, by Region 2020 & 2033

- Table 12: Global Auto-steer System for Agriculture Volume K Forecast, by Region 2020 & 2033

- Table 13: Global Auto-steer System for Agriculture Revenue billion Forecast, by Component 2020 & 2033

- Table 14: Global Auto-steer System for Agriculture Volume K Forecast, by Component 2020 & 2033

- Table 15: Global Auto-steer System for Agriculture Revenue billion Forecast, by Technology 2020 & 2033

- Table 16: Global Auto-steer System for Agriculture Volume K Forecast, by Technology 2020 & 2033

- Table 17: Global Auto-steer System for Agriculture Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 18: Global Auto-steer System for Agriculture Volume K Forecast, by Vehicle Type 2020 & 2033

- Table 19: Global Auto-steer System for Agriculture Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 20: Global Auto-steer System for Agriculture Volume K Forecast, by Sales Channel 2020 & 2033

- Table 21: Global Auto-steer System for Agriculture Revenue billion Forecast, by End User 2020 & 2033

- Table 22: Global Auto-steer System for Agriculture Volume K Forecast, by End User 2020 & 2033

- Table 23: Global Auto-steer System for Agriculture Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Auto-steer System for Agriculture Volume K Forecast, by Country 2020 & 2033

- Table 25: United States Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: United States Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Canada Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Canada Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Mexico Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Mexico Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Auto-steer System for Agriculture Revenue billion Forecast, by Component 2020 & 2033

- Table 32: Global Auto-steer System for Agriculture Volume K Forecast, by Component 2020 & 2033

- Table 33: Global Auto-steer System for Agriculture Revenue billion Forecast, by Technology 2020 & 2033

- Table 34: Global Auto-steer System for Agriculture Volume K Forecast, by Technology 2020 & 2033

- Table 35: Global Auto-steer System for Agriculture Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 36: Global Auto-steer System for Agriculture Volume K Forecast, by Vehicle Type 2020 & 2033

- Table 37: Global Auto-steer System for Agriculture Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 38: Global Auto-steer System for Agriculture Volume K Forecast, by Sales Channel 2020 & 2033

- Table 39: Global Auto-steer System for Agriculture Revenue billion Forecast, by End User 2020 & 2033

- Table 40: Global Auto-steer System for Agriculture Volume K Forecast, by End User 2020 & 2033

- Table 41: Global Auto-steer System for Agriculture Revenue billion Forecast, by Country 2020 & 2033

- Table 42: Global Auto-steer System for Agriculture Volume K Forecast, by Country 2020 & 2033

- Table 43: Brazil Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Brazil Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Argentina Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Argentina Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Rest of South America Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Rest of South America Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Global Auto-steer System for Agriculture Revenue billion Forecast, by Component 2020 & 2033

- Table 50: Global Auto-steer System for Agriculture Volume K Forecast, by Component 2020 & 2033

- Table 51: Global Auto-steer System for Agriculture Revenue billion Forecast, by Technology 2020 & 2033

- Table 52: Global Auto-steer System for Agriculture Volume K Forecast, by Technology 2020 & 2033

- Table 53: Global Auto-steer System for Agriculture Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 54: Global Auto-steer System for Agriculture Volume K Forecast, by Vehicle Type 2020 & 2033

- Table 55: Global Auto-steer System for Agriculture Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 56: Global Auto-steer System for Agriculture Volume K Forecast, by Sales Channel 2020 & 2033

- Table 57: Global Auto-steer System for Agriculture Revenue billion Forecast, by End User 2020 & 2033

- Table 58: Global Auto-steer System for Agriculture Volume K Forecast, by End User 2020 & 2033

- Table 59: Global Auto-steer System for Agriculture Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Auto-steer System for Agriculture Volume K Forecast, by Country 2020 & 2033

- Table 61: United Kingdom Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: United Kingdom Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Germany Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Germany Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 65: France Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: France Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 67: Italy Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: Italy Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 69: Spain Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: Spain Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Russia Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Russia Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Benelux Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 74: Benelux Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 75: Nordics Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 76: Nordics Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 77: Rest of Europe Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 78: Rest of Europe Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 79: Global Auto-steer System for Agriculture Revenue billion Forecast, by Component 2020 & 2033

- Table 80: Global Auto-steer System for Agriculture Volume K Forecast, by Component 2020 & 2033

- Table 81: Global Auto-steer System for Agriculture Revenue billion Forecast, by Technology 2020 & 2033

- Table 82: Global Auto-steer System for Agriculture Volume K Forecast, by Technology 2020 & 2033

- Table 83: Global Auto-steer System for Agriculture Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 84: Global Auto-steer System for Agriculture Volume K Forecast, by Vehicle Type 2020 & 2033

- Table 85: Global Auto-steer System for Agriculture Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 86: Global Auto-steer System for Agriculture Volume K Forecast, by Sales Channel 2020 & 2033

- Table 87: Global Auto-steer System for Agriculture Revenue billion Forecast, by End User 2020 & 2033

- Table 88: Global Auto-steer System for Agriculture Volume K Forecast, by End User 2020 & 2033

- Table 89: Global Auto-steer System for Agriculture Revenue billion Forecast, by Country 2020 & 2033

- Table 90: Global Auto-steer System for Agriculture Volume K Forecast, by Country 2020 & 2033

- Table 91: Turkey Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Turkey Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 93: Israel Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 94: Israel Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 95: GCC Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 96: GCC Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 97: North Africa Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 98: North Africa Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 99: South Africa Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 100: South Africa Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 101: Rest of Middle East & Africa Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 102: Rest of Middle East & Africa Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 103: Global Auto-steer System for Agriculture Revenue billion Forecast, by Component 2020 & 2033

- Table 104: Global Auto-steer System for Agriculture Volume K Forecast, by Component 2020 & 2033

- Table 105: Global Auto-steer System for Agriculture Revenue billion Forecast, by Technology 2020 & 2033

- Table 106: Global Auto-steer System for Agriculture Volume K Forecast, by Technology 2020 & 2033

- Table 107: Global Auto-steer System for Agriculture Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 108: Global Auto-steer System for Agriculture Volume K Forecast, by Vehicle Type 2020 & 2033

- Table 109: Global Auto-steer System for Agriculture Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 110: Global Auto-steer System for Agriculture Volume K Forecast, by Sales Channel 2020 & 2033

- Table 111: Global Auto-steer System for Agriculture Revenue billion Forecast, by End User 2020 & 2033

- Table 112: Global Auto-steer System for Agriculture Volume K Forecast, by End User 2020 & 2033

- Table 113: Global Auto-steer System for Agriculture Revenue billion Forecast, by Country 2020 & 2033

- Table 114: Global Auto-steer System for Agriculture Volume K Forecast, by Country 2020 & 2033

- Table 115: China Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 116: China Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 117: India Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 118: India Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 119: Japan Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 120: Japan Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 121: South Korea Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 122: South Korea Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 123: ASEAN Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 124: ASEAN Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 125: Oceania Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 126: Oceania Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

- Table 127: Rest of Asia Pacific Auto-steer System for Agriculture Revenue (billion) Forecast, by Application 2020 & 2033

- Table 128: Rest of Asia Pacific Auto-steer System for Agriculture Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Auto-steer System for Agriculture?

The projected CAGR is approximately 12.5%.

2. Which companies are prominent players in the Auto-steer System for Agriculture?

Key companies in the market include John Deere, Trimble, Topcon Positioning Systems, Ag Leader Technology, Raven Industries, AgJunction, Patchwork, CNH Industrial, AGCO Corporation, FieldBee, ARAG, Homburg Holland, Sveaverken Svea Agri, Geometer International, Hexagon Agriculture, Reichhardt, Rostselmash, FJDynamics, SMAJAYU(SHENZHEN), ComNav Technology, CP Device.

3. What are the main segments of the Auto-steer System for Agriculture?

The market segments include Component, Technology, Vehicle Type, Sales Channel, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.8 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Auto-steer System for Agriculture," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Auto-steer System for Agriculture report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Auto-steer System for Agriculture?

To stay informed about further developments, trends, and reports in the Auto-steer System for Agriculture, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence