Key Insights

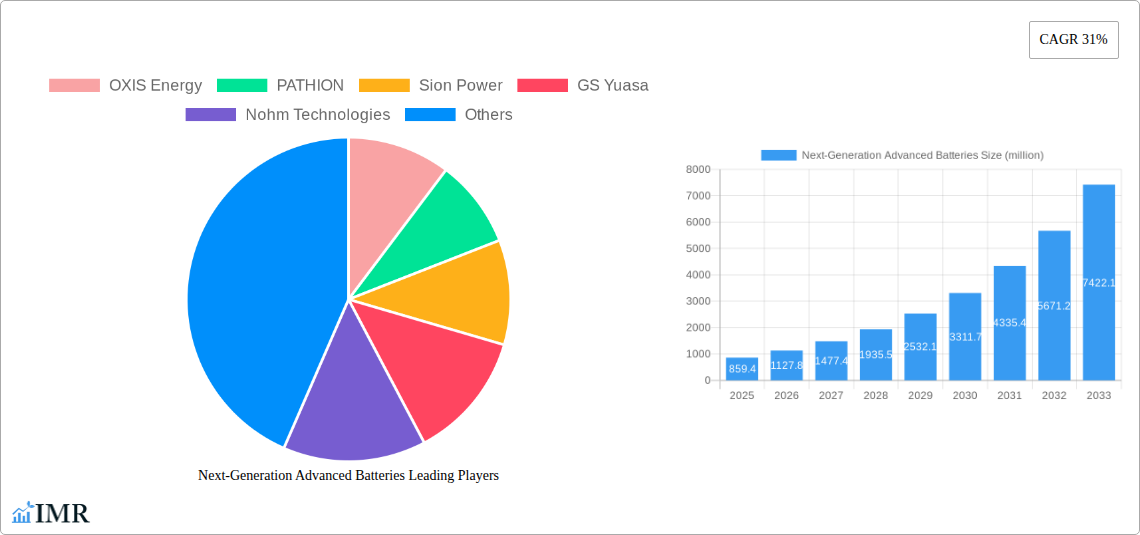

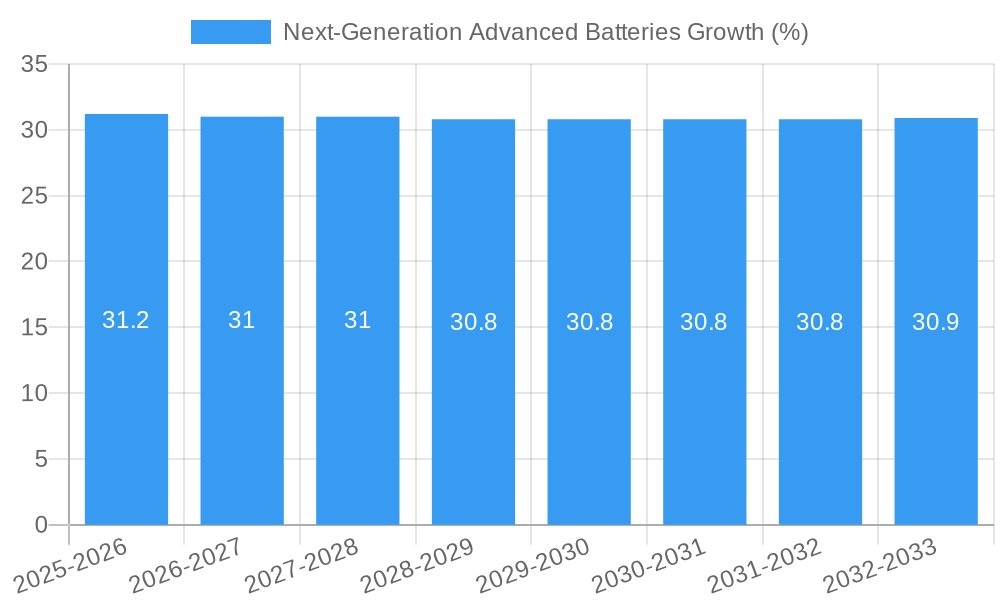

The global market for Next-Generation Advanced Batteries is poised for explosive growth, projected to reach $859.4 million by 2025, driven by an impressive CAGR of 31%. This surge is fueled by the urgent need for superior energy storage solutions across diverse applications, including transportation, energy storage, and consumer electronics. Key market drivers include the escalating demand for electric vehicles (EVs) with longer ranges and faster charging capabilities, alongside the growing adoption of renewable energy sources requiring efficient grid-scale storage. Furthermore, the miniaturization and enhanced performance demands in consumer electronics are pushing battery technology beyond current lithium-ion limitations. Emerging trends such as solid-state batteries promising enhanced safety and energy density, and lithium-sulfur batteries offering a high theoretical energy capacity, are pivotal in shaping the future of this dynamic market. Innovations in magnesium-ion and metal-air batteries also present significant opportunities for disruption.

Despite the tremendous potential, the market faces certain restraints. High manufacturing costs associated with novel materials and complex production processes remain a significant hurdle. Limited infrastructure for the charging and recycling of these advanced batteries, particularly for newer chemistries, could also impede widespread adoption. However, ongoing research and development, coupled with increasing investment from prominent players like OXIS Energy, Sion Power, and Solid Power, are actively addressing these challenges. The market segmentation by type, including lithium-sulfur, magnesium-ion, and solid electrodes, reflects a competitive landscape focused on overcoming existing battery limitations. Regionally, North America, Europe, and Asia Pacific are expected to be key growth centers, with China and the United States leading in both production and consumption, propelled by supportive government policies and robust R&D initiatives.

Next-Generation Advanced Batteries Market Dynamics & Structure

The Next-Generation Advanced Batteries market is characterized by a dynamic and evolving competitive landscape, moving towards increased concentration driven by significant technological advancements and substantial investment. Key innovation drivers include the relentless pursuit of higher energy density, faster charging capabilities, enhanced safety, and improved sustainability, moving beyond the limitations of current lithium-ion technology. Regulatory frameworks are increasingly supportive, particularly in decarbonization initiatives and electric vehicle mandates, creating a favorable environment for advanced battery adoption. Competitive product substitutes, while present in the form of incremental improvements in existing chemistries, are being rapidly outpaced by disruptive technologies like solid-state and metal-air batteries. End-user demographics are shifting, with a growing demand from the transportation sector (Electric Vehicles - EVs) and energy storage solutions for grid stabilization and renewable energy integration. Consumer electronics also represent a significant, albeit more mature, segment. Mergers and acquisitions (M&A) are on the rise as larger players seek to acquire promising technologies and gain market share. For instance, the estimated $5,500 million value of M&A deals in the historical period (2019-2024) signifies this consolidation trend. Innovation barriers, however, include the high cost of research and development, scaling manufacturing processes, and ensuring long-term material availability and recycling solutions.

- Market Concentration: Moderate to High, increasing with R&D investments and M&A activities.

- Technological Innovation Drivers: Energy density, charging speed, safety, cost reduction, lifecycle.

- Regulatory Frameworks: Supportive of EVs, grid modernization, and renewable energy integration.

- Competitive Product Substitutes: Incremental lithium-ion improvements, but rapidly being surpassed by novel chemistries.

- End-User Demographics: Strong growth in Transportation (EVs) and Energy Storage, steady demand from Consumer Electronics.

- M&A Trends: Increasing consolidation, strategic acquisitions of startups with breakthrough technologies.

Next-Generation Advanced Batteries Growth Trends & Insights

The Next-Generation Advanced Batteries market is poised for exponential growth, driven by a confluence of technological breakthroughs, increasing global demand for sustainable energy solutions, and supportive policy landscapes. Projections indicate a compound annual growth rate (CAGR) of approximately 28.5% from 2025 to 2033, transforming the market from an estimated $78,200 million in 2025 to a projected $534,750 million by 2033. This remarkable expansion is fueled by breakthroughs in chemistries such as Lithium Sulfur, Magnesium Ion, and especially Solid Electrodes, which promise higher energy densities and improved safety profiles compared to conventional lithium-ion batteries. The Transportation segment, particularly the burgeoning electric vehicle (EV) market, is the primary engine of this growth. As battery costs decline and performance metrics improve, EV adoption rates are accelerating globally, necessitating a robust supply of advanced battery solutions. Simultaneously, the Energy Storage sector is experiencing a surge in demand, driven by the need for grid stability, integration of intermittent renewable energy sources like solar and wind, and the decentralization of power generation. This segment is expected to grow at a CAGR of 26.0% over the forecast period, reaching an estimated market size of $180,500 million by 2033.

Consumer behavior is also shifting, with a greater emphasis on sustainability and performance. Consumers are increasingly seeking devices with longer battery life and faster charging times, pushing manufacturers to adopt next-generation battery technologies. The Consumer Electronic segment, while already a significant market for batteries, will benefit from these advancements, offering enhanced user experiences and enabling new form factors for portable devices. Furthermore, the development of novel battery types like Metal-Air batteries, with their theoretical high energy densities, and Ultracapacitors, for rapid energy discharge, are opening up new application areas in industrial equipment and specialized transportation. The research and development efforts by key players like OXIS Energy, Sion Power, and Solid Power are crucial in overcoming existing manufacturing challenges and bringing these innovative technologies to mass production. The estimated market penetration for advanced battery technologies in the EV sector is projected to exceed 65% by 2033, a significant leap from the 22% observed in 2019. This widespread adoption will be supported by a continuous stream of technological disruptions, including advancements in battery management systems and novel electrode materials that further enhance performance and lifespan. The increasing focus on battery recycling and the development of more sustainable materials will also play a crucial role in the long-term viability and growth of the market.

Dominant Regions, Countries, or Segments in Next-Generation Advanced Batteries

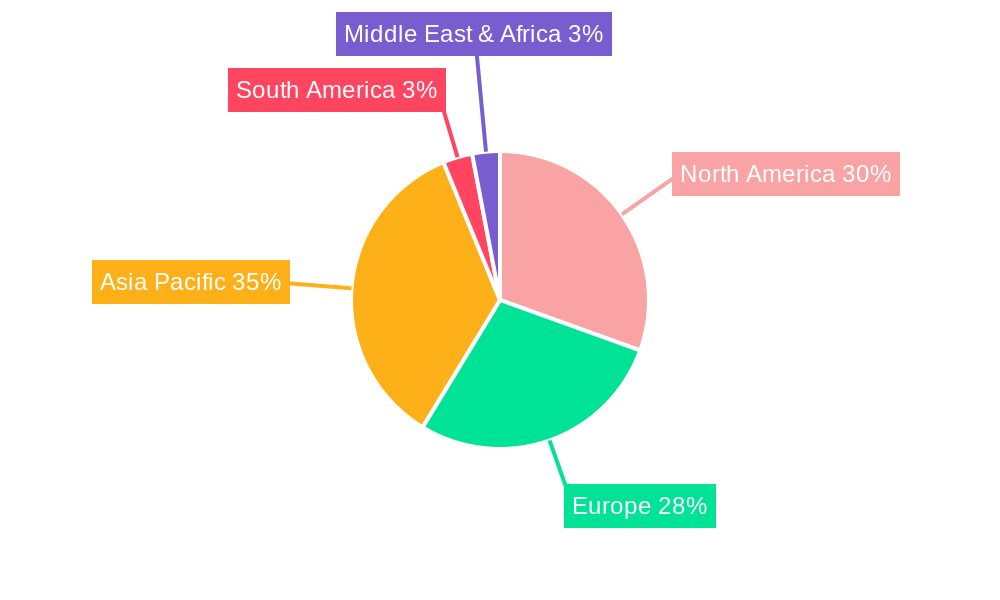

The Next-Generation Advanced Batteries market exhibits a pronounced dominance, primarily driven by geographical regions and specific application segments that are at the forefront of technological adoption and industrial growth. Asia Pacific is currently the leading region, accounting for an estimated 45% of the global market share in 2025. This dominance is attributed to the region's robust manufacturing infrastructure, significant government investments in electric mobility and renewable energy, and the presence of major battery manufacturers and automotive companies. Countries like China, South Korea, and Japan are spearheading this growth, with extensive research and development initiatives and supportive policies aimed at electrifying transportation and enhancing grid stability. The Transportation application segment is unequivocally the most dominant, projected to command approximately 55% of the total market value in 2025, estimated at $42,990 million. This is primarily due to the accelerating global adoption of electric vehicles (EVs), where the demand for high-energy density, fast-charging, and safe battery solutions is paramount.

Within the Transportation segment, the sub-segment of passenger EVs represents the largest growth driver. The Energy Storage segment is the second-largest contributor, expected to hold 30% of the market share in 2025, valued at $23,460 million. This growth is fueled by the increasing integration of renewable energy sources, the need for grid stabilization, and the development of smart grids. Countries with aggressive renewable energy targets and supportive grid modernization policies, such as Germany, the United States, and China, are significant contributors to this segment's expansion. Technological advancements in Solid Electrodes are a key driver of dominance across these segments. Solid-state batteries offer superior safety, higher energy density, and longer cycle life, making them particularly attractive for EV and grid storage applications. The market for Lithium Sulfur batteries, with their very high theoretical energy density, is also gaining traction, especially for specialized applications.

- Dominant Region: Asia Pacific (especially China, South Korea, Japan) – driven by manufacturing prowess, government incentives, and EV market leadership.

- Dominant Country: China – leading in EV production, battery manufacturing, and renewable energy deployment.

- Dominant Application Segment: Transportation (Electric Vehicles) – fueled by global EV adoption and governmental mandates.

- Key Growth Drivers:

- Government subsidies and tax credits for EVs and renewable energy projects.

- Rapid advancements in battery chemistries like solid-state and lithium-sulfur.

- Declining battery costs making EVs and grid storage more economically viable.

- Increasing consumer awareness and demand for sustainable transportation and energy solutions.

- Technological breakthroughs from companies like GS Yuasa and Amprius.

- Market Share Projections (2025):

- Transportation: 55%

- Energy Storage: 30%

- Consumer Electronic: 10%

- Others: 5%

- Dominant Battery Type (Emerging): Solid Electrodes – due to inherent safety and performance advantages.

Next-Generation Advanced Batteries Product Landscape

The product landscape for next-generation advanced batteries is characterized by rapid innovation, pushing the boundaries of energy density, charging speed, and safety. Solid-state battery technologies, such as those developed by Solid Power and exemplified by early prototypes from companies like OXIS Energy, are emerging as key differentiators, offering the potential for significantly higher energy density (exceeding 500 Wh/kg) and enhanced thermal stability compared to current lithium-ion counterparts. Metal-air batteries, including those being explored by Phinergy, promise an even greater theoretical energy density but face challenges in rechargeability and lifespan. Magnesium-ion batteries, while still in earlier stages of development by entities like Lockheed Martin, present a potentially safer and more abundant alternative to lithium. Performance metrics are continuously improving, with next-generation batteries aiming for charging times of under 15 minutes for EVs and lifespans exceeding 2,000 charge cycles. These advancements are enabling new applications in electric aviation, long-duration energy storage, and more powerful, lighter portable electronics.

Key Drivers, Barriers & Challenges in Next-Generation Advanced Batteries

Key Drivers:

The Next-Generation Advanced Batteries market is propelled by several key drivers. The escalating global demand for electric vehicles (EVs) is a primary catalyst, fueled by government mandates, environmental concerns, and improving vehicle performance. Similarly, the imperative to integrate renewable energy sources and stabilize power grids is driving significant growth in the Energy Storage sector. Technological innovation remains central, with ongoing breakthroughs in energy density, charging speed, and safety of chemistries like Solid Electrodes and Lithium Sulfur. Supportive government policies, including subsidies, tax credits, and R&D funding, are also critical in accelerating market adoption and fostering investment.

- Electric Vehicle adoption surge

- Renewable energy integration and grid modernization

- Technological advancements (higher energy density, faster charging, enhanced safety)

- Favorable government policies and incentives

- Growing environmental consciousness

Barriers & Challenges:

Despite the immense potential, several significant barriers and challenges impede the widespread adoption of next-generation advanced batteries. The high cost of manufacturing and scaling up production for novel battery chemistries remains a major hurdle, with the estimated production cost per kWh still significantly higher for many next-gen technologies compared to mature lithium-ion. Supply chain disruptions for critical raw materials, such as cobalt, nickel, and lithium, can impact production volumes and price stability. Regulatory hurdles related to safety standards and material sourcing for emerging technologies also need to be addressed. Furthermore, competition from continuously improving conventional lithium-ion batteries, which benefit from established infrastructure and economies of scale, presents a continuous challenge. The estimated lead time for commercialization of some advanced battery technologies can be upwards of 5-7 years, further impacting their market penetration.

- High manufacturing and scaling costs (estimated 20-30% higher than current Li-ion for early-stage tech)

- Supply chain volatility and availability of critical raw materials

- Regulatory complexities and evolving safety standards

- Intense competition from advanced lithium-ion technologies

- Long commercialization timelines for novel chemistries

Emerging Opportunities in Next-Generation Advanced Batteries

Emerging opportunities in the Next-Generation Advanced Batteries market lie in tapping into niche applications with stringent performance requirements and capitalizing on the growing demand for sustainable and localized energy solutions. The development of advanced batteries for electric aviation presents a significant opportunity, requiring extremely high energy density and safety. Furthermore, the integration of advanced batteries into smart city infrastructure for distributed energy storage and grid resilience offers substantial market potential. The increasing focus on battery-as-a-service models and circular economy principles, including advanced recycling and second-life applications, is also creating new business models and revenue streams. The expansion of Magnesium Ion and other abundant element-based batteries could unlock cost-effective solutions for large-scale energy storage in developing regions.

Growth Accelerators in the Next-Generation Advanced Batteries Industry

Several catalysts are accelerating the long-term growth of the Next-Generation Advanced Batteries industry. Continued breakthroughs in material science and electrochemistry are leading to significant improvements in energy density, lifespan, and charging speeds, making advanced batteries increasingly competitive. Strategic partnerships between battery developers, automotive manufacturers, and energy utilities are crucial for de-risking technology development, co-creating solutions, and securing large-scale demand. Government initiatives, including the establishment of battery manufacturing hubs and the promotion of domestic supply chains, are also playing a vital role in accelerating production and reducing costs. The increasing focus on safety and sustainability is creating a market advantage for advanced battery technologies that inherently offer these benefits, further driving their adoption.

Key Players Shaping the Next-Generation Advanced Batteries Market

- OXIS Energy

- PATHION

- Sion Power

- GS Yuasa

- Nohm Technologies

- PolyPlus

- Lockheed Martin

- Pellion Technologies

- Seeo

- Solid Power

- Amprius

- 24M

- Phinergy

- Fluidic Energy

- Maxwell

- Ambri

- ESS

Notable Milestones in Next-Generation Advanced Batteries Sector

- 2019: OXIS Energy announces advancements in its Lithium-Sulfur battery technology, targeting aviation applications.

- 2020: Solid Power secures significant funding to scale its solid-state battery manufacturing capabilities.

- 2021: Sion Power showcases a high-energy density lithium-metal battery prototype.

- 2022: Amprius demonstrates record-breaking energy density in its silicon-anode lithium-ion batteries.

- 2022: GS Yuasa announces progress in developing next-generation lithium-ion battery technologies with improved safety and performance.

- 2023: 24M Technologies secures partnerships to advance its semi-solid lithium-ion battery manufacturing platform.

- 2023: Pellion Technologies and PolyPlus Battery Company continue to advance their respective thin-film and lithium-air battery technologies.

- 2024: Lockheed Martin announces research into advanced battery materials for defense and aerospace applications, potentially including Magnesium Ion.

- 2024: Nohm Technologies and Seeo Inc. continue their work on solid-state electrolyte innovations.

- 2024: Phinergy explores new applications for its metal-air battery technology in stationary energy storage.

- 2024: Maxwell Technologies (acquired by Tesla) continues its focus on ultracapacitor advancements.

- 2024: Ambri and ESS focus on long-duration energy storage solutions utilizing advanced chemistries.

- 2024: Fluidic Energy continues development of its rechargeable metal-air battery systems.

In-Depth Next-Generation Advanced Batteries Market Outlook

The Next-Generation Advanced Batteries market is poised for substantial growth and transformation over the forecast period. Fueled by relentless technological innovation, particularly in Solid Electrodes, Lithium Sulfur, and Magnesium Ion chemistries, the market is set to exceed $534,750 million by 2033. The Transportation sector, driven by the electrifying automotive industry, and the burgeoning Energy Storage segment for grid modernization and renewable energy integration, will be the primary growth accelerators. Strategic partnerships, significant R&D investments, and supportive government policies will continue to propel market expansion, creating a landscape ripe with opportunities for both established players and emerging innovators. The focus on safety, sustainability, and performance will be paramount, solidifying the indispensable role of advanced batteries in shaping a decarbonized future.

Next-Generation Advanced Batteries Segmentation

-

1. Application

- 1.1. Transportation

- 1.2. Energy Storage

- 1.3. Consumer Electronic

- 1.4. Others

-

2. Types

- 2.1. Lithium Sulfur

- 2.2. Magnesium Ion

- 2.3. Solid Electrodes

- 2.4. Metal-Air

- 2.5. Ultracapacitors

- 2.6. Others

Next-Generation Advanced Batteries Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Next-Generation Advanced Batteries REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 31% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Next-Generation Advanced Batteries Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Transportation

- 5.1.2. Energy Storage

- 5.1.3. Consumer Electronic

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Lithium Sulfur

- 5.2.2. Magnesium Ion

- 5.2.3. Solid Electrodes

- 5.2.4. Metal-Air

- 5.2.5. Ultracapacitors

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Next-Generation Advanced Batteries Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Transportation

- 6.1.2. Energy Storage

- 6.1.3. Consumer Electronic

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Lithium Sulfur

- 6.2.2. Magnesium Ion

- 6.2.3. Solid Electrodes

- 6.2.4. Metal-Air

- 6.2.5. Ultracapacitors

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Next-Generation Advanced Batteries Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Transportation

- 7.1.2. Energy Storage

- 7.1.3. Consumer Electronic

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Lithium Sulfur

- 7.2.2. Magnesium Ion

- 7.2.3. Solid Electrodes

- 7.2.4. Metal-Air

- 7.2.5. Ultracapacitors

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Next-Generation Advanced Batteries Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Transportation

- 8.1.2. Energy Storage

- 8.1.3. Consumer Electronic

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Lithium Sulfur

- 8.2.2. Magnesium Ion

- 8.2.3. Solid Electrodes

- 8.2.4. Metal-Air

- 8.2.5. Ultracapacitors

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Next-Generation Advanced Batteries Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Transportation

- 9.1.2. Energy Storage

- 9.1.3. Consumer Electronic

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Lithium Sulfur

- 9.2.2. Magnesium Ion

- 9.2.3. Solid Electrodes

- 9.2.4. Metal-Air

- 9.2.5. Ultracapacitors

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Next-Generation Advanced Batteries Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Transportation

- 10.1.2. Energy Storage

- 10.1.3. Consumer Electronic

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Lithium Sulfur

- 10.2.2. Magnesium Ion

- 10.2.3. Solid Electrodes

- 10.2.4. Metal-Air

- 10.2.5. Ultracapacitors

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 OXIS Energy

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 PATHION

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Sion Power

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 GS Yuasa

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Nohm Technologies

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 PolyPlus

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Lockheed Martin

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Pellion Technologies

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Seeo

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Solid Power

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Amprius

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 24M

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Phinergy

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Fluidic Energy

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Maxwell

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Ambri

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 ESS

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 OXIS Energy

List of Figures

- Figure 1: Global Next-Generation Advanced Batteries Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Next-Generation Advanced Batteries Revenue (million), by Application 2024 & 2032

- Figure 3: North America Next-Generation Advanced Batteries Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Next-Generation Advanced Batteries Revenue (million), by Types 2024 & 2032

- Figure 5: North America Next-Generation Advanced Batteries Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Next-Generation Advanced Batteries Revenue (million), by Country 2024 & 2032

- Figure 7: North America Next-Generation Advanced Batteries Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Next-Generation Advanced Batteries Revenue (million), by Application 2024 & 2032

- Figure 9: South America Next-Generation Advanced Batteries Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Next-Generation Advanced Batteries Revenue (million), by Types 2024 & 2032

- Figure 11: South America Next-Generation Advanced Batteries Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Next-Generation Advanced Batteries Revenue (million), by Country 2024 & 2032

- Figure 13: South America Next-Generation Advanced Batteries Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Next-Generation Advanced Batteries Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Next-Generation Advanced Batteries Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Next-Generation Advanced Batteries Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Next-Generation Advanced Batteries Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Next-Generation Advanced Batteries Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Next-Generation Advanced Batteries Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Next-Generation Advanced Batteries Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Next-Generation Advanced Batteries Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Next-Generation Advanced Batteries Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Next-Generation Advanced Batteries Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Next-Generation Advanced Batteries Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Next-Generation Advanced Batteries Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Next-Generation Advanced Batteries Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Next-Generation Advanced Batteries Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Next-Generation Advanced Batteries Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Next-Generation Advanced Batteries Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Next-Generation Advanced Batteries Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Next-Generation Advanced Batteries Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Next-Generation Advanced Batteries Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Next-Generation Advanced Batteries Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Next-Generation Advanced Batteries Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Next-Generation Advanced Batteries Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Next-Generation Advanced Batteries Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Next-Generation Advanced Batteries Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Next-Generation Advanced Batteries Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Next-Generation Advanced Batteries Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Next-Generation Advanced Batteries Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Next-Generation Advanced Batteries Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Next-Generation Advanced Batteries Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Next-Generation Advanced Batteries Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Next-Generation Advanced Batteries Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Next-Generation Advanced Batteries Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Next-Generation Advanced Batteries Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Next-Generation Advanced Batteries Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Next-Generation Advanced Batteries Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Next-Generation Advanced Batteries Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Next-Generation Advanced Batteries Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Next-Generation Advanced Batteries Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Next-Generation Advanced Batteries?

The projected CAGR is approximately 31%.

2. Which companies are prominent players in the Next-Generation Advanced Batteries?

Key companies in the market include OXIS Energy, PATHION, Sion Power, GS Yuasa, Nohm Technologies, PolyPlus, Lockheed Martin, Pellion Technologies, Seeo, Solid Power, Amprius, 24M, Phinergy, Fluidic Energy, Maxwell, Ambri, ESS.

3. What are the main segments of the Next-Generation Advanced Batteries?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 859.4 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5900.00, USD 8850.00, and USD 11800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Next-Generation Advanced Batteries," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Next-Generation Advanced Batteries report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Next-Generation Advanced Batteries?

To stay informed about further developments, trends, and reports in the Next-Generation Advanced Batteries, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence