Key Insights

The Thailand power generation market, projected for a 9.1% CAGR, is estimated to reach $1.7 billion by 2024. This growth is driven by rising energy demand, fueled by economic expansion and population increase, necessitating substantial investments in generation capacity. Government initiatives prioritizing renewable energy sources, such as solar and wind, are accelerating the transition from conventional power generation. Prominent companies like JinkoSolar Holding Co Ltd and Vestas Wind Systems AS are key contributors. Challenges include potential grid infrastructure limitations and the need for sustained policy support to attract foreign investment in renewables. The market anticipates a significant shift towards renewable energy sources, though conventional sources will remain integral to the energy mix.

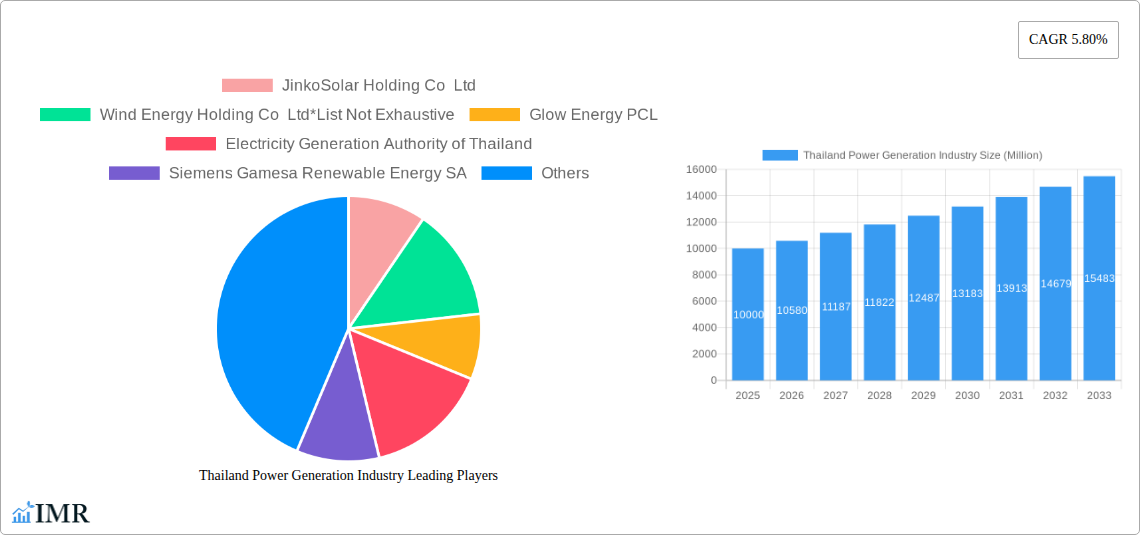

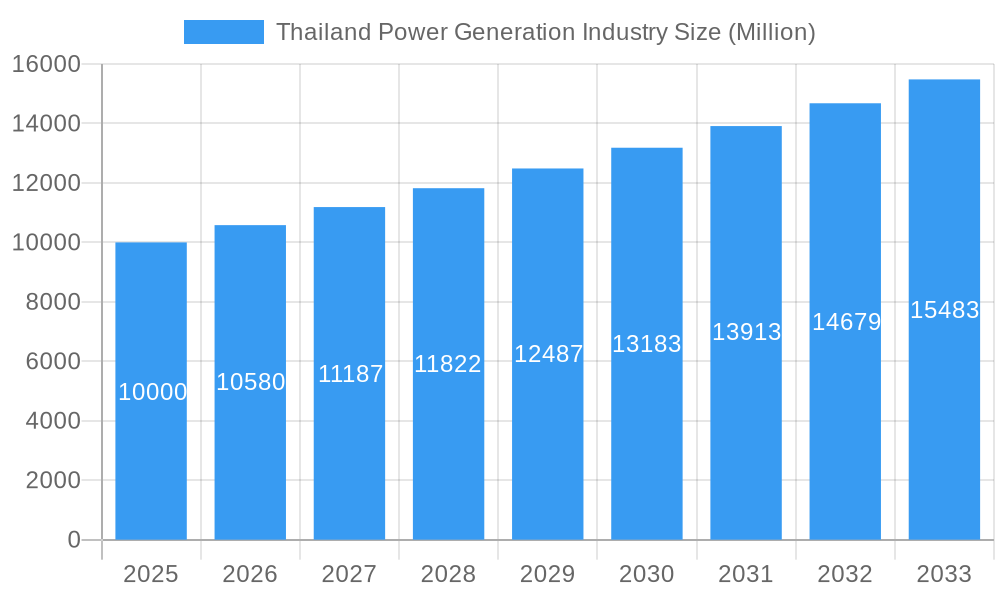

Thailand Power Generation Industry Market Size (In Billion)

The competitive environment features a blend of domestic and international companies. Key players like Electricity Generation Authority of Thailand and BCPG PCL command significant market share, alongside expanding global entities such as Siemens Gamesa Renewable Energy SA and General Electric Company. This competition fosters innovation and technological advancements, improving efficiency and cost-effectiveness. Market success depends on overcoming restraints, including securing funding for large-scale renewable projects and integrating renewables into the grid for stable supply. Regional disparities in energy access and infrastructure require strategic investment and planning for equitable distribution.

Thailand Power Generation Industry Company Market Share

Thailand Power Generation Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Thailand power generation industry, encompassing market dynamics, growth trends, key players, and future outlook. With a focus on both conventional and renewable energy segments, this report is essential for industry professionals, investors, and strategic decision-makers seeking to navigate this dynamic market. The study period covers 2019-2033, with a base year of 2025 and a forecast period of 2025-2033.

Keywords: Thailand power generation, renewable energy Thailand, conventional power generation Thailand, electricity generation Thailand, EGAT, BCPG PCL, Glow Energy PCL, solar power Thailand, wind power Thailand, power purchase agreement Thailand, energy storage Thailand, JinkoSolar, Siemens Gamesa, Vestas Wind Systems, Thailand energy market, power industry Thailand.

Thailand Power Generation Industry Market Dynamics & Structure

The Thailand power generation market is characterized by a mix of state-owned entities and private companies, leading to a moderately concentrated market structure. EGAT, a state-owned enterprise, maintains significant market share in conventional power generation. However, the renewable energy sector witnesses increasing participation from private players, fostering competition. Technological innovation, particularly in solar and wind power, is a key driver, propelled by government incentives and decreasing technology costs. The regulatory framework, while supportive of renewable energy integration, faces challenges in streamlining approvals and ensuring grid stability. Substitutes, primarily from neighboring countries through regional power grids, exert limited influence. The end-user demographics comprise primarily residential, commercial, and industrial consumers, with varying electricity demands. M&A activity has been moderate, with strategic partnerships becoming increasingly prominent.

- Market Concentration: EGAT holds xx% market share (estimated 2025) in conventional power generation. The renewable energy sector is more fragmented.

- Technological Innovation: Significant advancements in solar PV and wind turbine technology are reducing costs and enhancing efficiency.

- Regulatory Framework: Government policies strongly promote renewable energy adoption, but bureaucratic hurdles remain.

- M&A Activity: xx deals (Million units) in the past five years, with a trend towards strategic collaborations.

Thailand Power Generation Industry Growth Trends & Insights

The Thailand power generation market demonstrates robust growth, driven by increasing energy demand and the government's commitment to renewable energy integration. The market size, valued at xx Million units in 2024, is projected to reach xx Million units by 2033, exhibiting a CAGR of xx%. This growth is fueled by rising industrialization, urbanization, and a growing middle class. The adoption rate of renewable energy technologies is accelerating, propelled by decreasing costs and supportive government policies. Technological disruptions, such as advancements in battery storage and smart grids, are further enhancing market dynamics. Consumer behavior is shifting towards greater awareness of sustainability and a preference for cleaner energy sources.

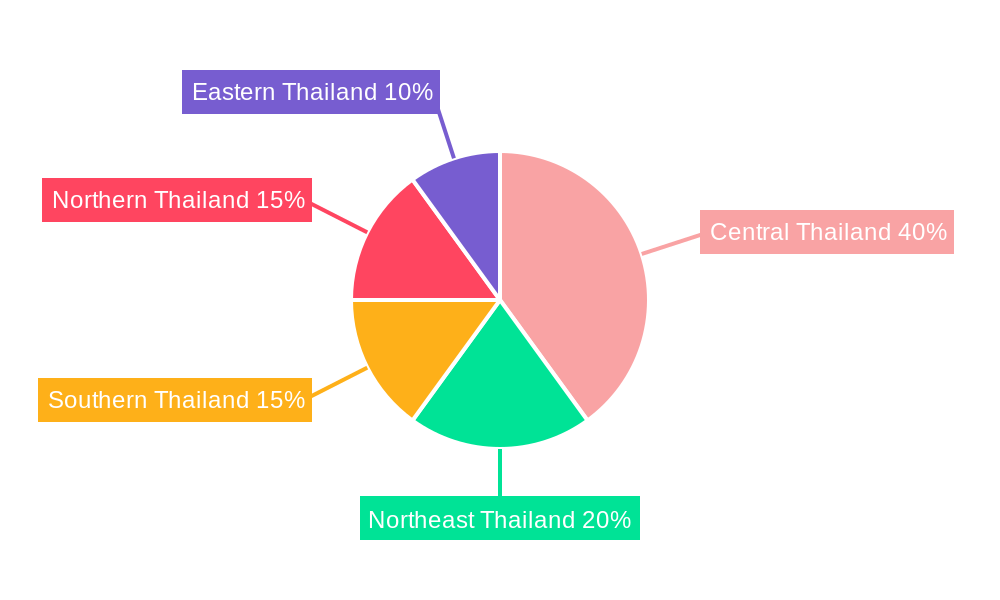

Dominant Regions, Countries, or Segments in Thailand Power Generation Industry

Central Thailand remains the dominant region for power generation, primarily due to its higher population density and industrial concentration. However, the renewable energy sector is experiencing significant growth in other regions with favorable resource conditions, such as the northeast for solar power and the south for wind. The renewable energy segment (solar and wind) exhibits the fastest growth rate, driven by government incentives and decreasing technology costs. Conventional power generation continues to play a significant role, but its share is gradually declining.

- Key Drivers for Renewable Energy Growth:

- Government subsidies and feed-in tariffs

- Decreasing technology costs

- Increasing environmental awareness

- Supportive regulatory framework

- Dominance Factors:

- Existing infrastructure in Central Thailand

- Favorable resource conditions in other regions for renewable energy

Thailand Power Generation Industry Product Landscape

The power generation product landscape comprises a diverse range of technologies, including coal-fired, gas-fired, hydroelectric, solar PV, and wind turbines. Recent innovations focus on improving efficiency, reducing costs, and enhancing grid integration. Solar PV modules with higher efficiency ratings and larger capacities are gaining popularity. Wind turbines are becoming larger and more technologically advanced, maximizing energy capture. Battery energy storage systems are increasingly integrated with renewable energy projects to improve grid stability and reliability. Unique selling propositions often focus on cost-effectiveness, sustainability, and technological advancements.

Key Drivers, Barriers & Challenges in Thailand Power Generation Industry

Key Drivers:

- Increasing energy demand from industrialization and urbanization.

- Government policies promoting renewable energy integration.

- Decreasing costs of renewable energy technologies.

Key Challenges:

- Grid infrastructure limitations in accommodating increasing renewable energy capacity.

- Regulatory hurdles and bureaucratic delays in project approvals.

- Competition from existing conventional power generation sources.

- xx Million units (estimated) shortfall in grid infrastructure investment needed by 2030.

Emerging Opportunities in Thailand Power Generation Industry

- Growth of decentralized power generation using rooftop solar and microgrids.

- Increasing adoption of energy storage technologies to enhance grid stability.

- Development of smart grids for improved efficiency and reliability.

- Exploring opportunities in offshore wind power.

Growth Accelerators in the Thailand Power Generation Industry

Technological breakthroughs in energy storage, artificial intelligence for grid management, and the development of innovative financing mechanisms are driving long-term growth. Strategic partnerships between technology providers and energy companies are accelerating the deployment of renewable energy projects. Expanding the country's power grid infrastructure and strengthening regional power interconnections are key strategies for accommodating the projected increase in power generation capacity.

Key Players Shaping the Thailand Power Generation Industry Market

- JinkoSolar Holding Co Ltd

- Wind Energy Holding Co Ltd

- Glow Energy PCL

- Electricity Generation Authority of Thailand

- Siemens Gamesa Renewable Energy SA

- Schneider Electric SE

- SGS SA

- BCPG PCL

- SIAM SOLAR

- Vestas Wind Systems AS

- General Electric Company

Notable Milestones in Thailand Power Generation Industry Sector

- May 2023: Mae Hing Son province launched a solar power plant and battery energy storage project (3MW solar, 4MW battery).

- May 2023: Acciona Energia and Blue Circle signed a 25-year PPA for five wind farms (436 MW total capacity). Construction of the first wind farm is expected to begin in 2024.

In-Depth Thailand Power Generation Industry Market Outlook

The Thailand power generation industry is poised for sustained growth, driven by increasing energy demand and the government's strong commitment to renewable energy integration. The market presents significant opportunities for investors and industry participants focusing on renewable energy technologies, smart grid infrastructure, and energy storage solutions. Strategic partnerships, technological advancements, and expanding grid capacity will be crucial for unlocking the sector's full potential. The integration of advanced technologies will play a critical role in ensuring a stable and reliable energy supply for Thailand's growing economy.

Thailand Power Generation Industry Segmentation

-

1. Power Generation

- 1.1. Conventional

- 1.2. Renewables

- 2. Power Transmission and Distribution

Thailand Power Generation Industry Segmentation By Geography

- 1. Thailand

Thailand Power Generation Industry Regional Market Share

Geographic Coverage of Thailand Power Generation Industry

Thailand Power Generation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Increasing Renewables Capacity in Thailand4.; Rising Modernization of Existing Transmission and Distribution Infrastructure

- 3.3. Market Restrains

- 3.3.1. 4.; Huge Capital Expenditure Required for Carrying out Modernization of Existing Facilities

- 3.4. Market Trends

- 3.4.1. Renewable Power Generation to Witness Significant Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Thailand Power Generation Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Power Generation

- 5.1.1. Conventional

- 5.1.2. Renewables

- 5.2. Market Analysis, Insights and Forecast - by Power Transmission and Distribution

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Thailand

- 5.1. Market Analysis, Insights and Forecast - by Power Generation

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 JinkoSolar Holding Co Ltd

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Wind Energy Holding Co Ltd*List Not Exhaustive

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Glow Energy PCL

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Electricity Generation Authority of Thailand

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Siemens Gamesa Renewable Energy SA

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Schneider Electric SE

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 SGS SA

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 BCPG PCL

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 SIAM SOLAR

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Vestas Wind Systems AS

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 General Electric Company

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.1 JinkoSolar Holding Co Ltd

List of Figures

- Figure 1: Thailand Power Generation Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Thailand Power Generation Industry Share (%) by Company 2025

List of Tables

- Table 1: Thailand Power Generation Industry Revenue billion Forecast, by Power Generation 2020 & 2033

- Table 2: Thailand Power Generation Industry Revenue billion Forecast, by Power Transmission and Distribution 2020 & 2033

- Table 3: Thailand Power Generation Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Thailand Power Generation Industry Revenue billion Forecast, by Power Generation 2020 & 2033

- Table 5: Thailand Power Generation Industry Revenue billion Forecast, by Power Transmission and Distribution 2020 & 2033

- Table 6: Thailand Power Generation Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Thailand Power Generation Industry?

The projected CAGR is approximately 9.1%.

2. Which companies are prominent players in the Thailand Power Generation Industry?

Key companies in the market include JinkoSolar Holding Co Ltd, Wind Energy Holding Co Ltd*List Not Exhaustive, Glow Energy PCL, Electricity Generation Authority of Thailand, Siemens Gamesa Renewable Energy SA, Schneider Electric SE, SGS SA, BCPG PCL, SIAM SOLAR, Vestas Wind Systems AS, General Electric Company.

3. What are the main segments of the Thailand Power Generation Industry?

The market segments include Power Generation, Power Transmission and Distribution.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.7 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Renewables Capacity in Thailand4.; Rising Modernization of Existing Transmission and Distribution Infrastructure.

6. What are the notable trends driving market growth?

Renewable Power Generation to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; Huge Capital Expenditure Required for Carrying out Modernization of Existing Facilities.

8. Can you provide examples of recent developments in the market?

May 2023: Mae Hing Son province launched a solar power plant and battery energy storage project. The Electricity Generating Authority of Thailand (EGAT) held a commercial operation date (COD) ceremony for a 3 MW solar power plant and 4 MW battery energy storage system project.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Thailand Power Generation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Thailand Power Generation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Thailand Power Generation Industry?

To stay informed about further developments, trends, and reports in the Thailand Power Generation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence