Key Insights

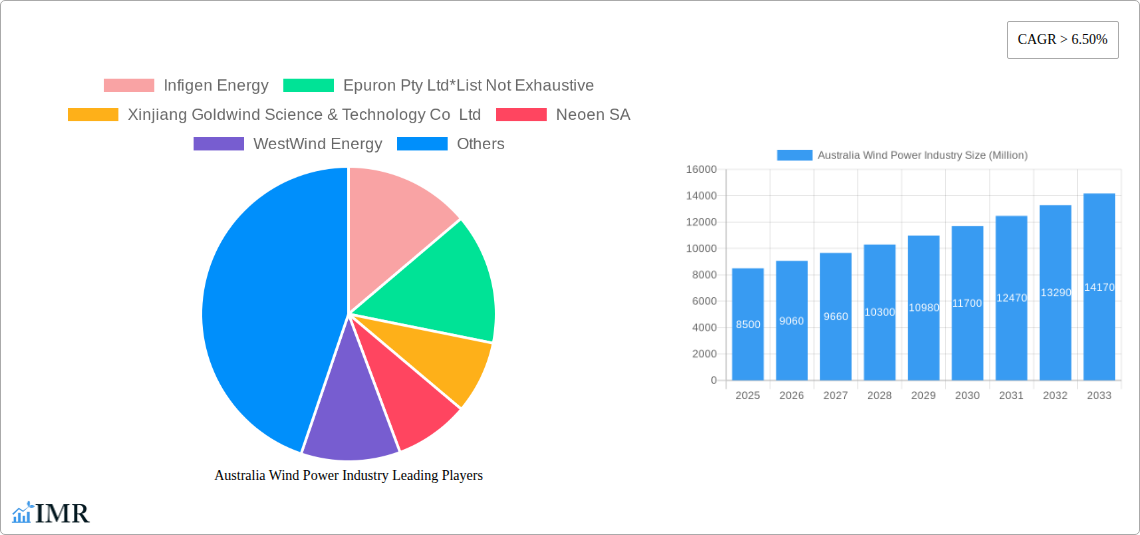

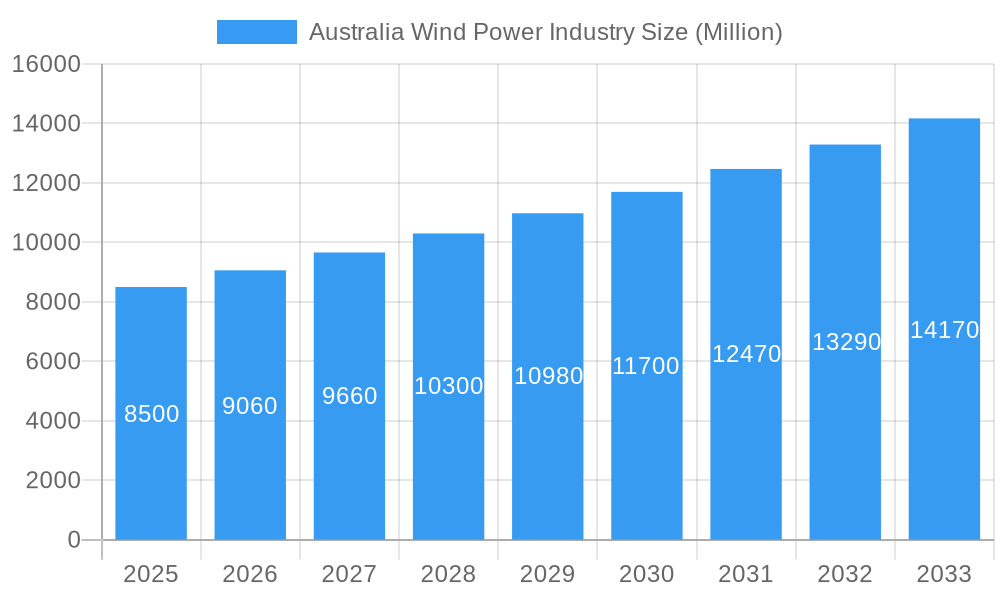

The Australian wind power sector is set for significant expansion, with a projected Compound Annual Growth Rate (CAGR) of 13.1%. The market size is estimated at 34.07 billion in the base year 2025. This growth is fueled by supportive government policies, rising environmental awareness, and the critical need for clean energy to meet escalating demand and climate objectives. Key drivers include robust renewable energy targets, substantial government incentives, and the increasing cost-competitiveness of wind energy technology against fossil fuels. Advancements in turbine efficiency and the development of larger, more powerful wind farms are also enhancing energy output and reducing the levelized cost of electricity.

Australia Wind Power Industry Market Size (In Billion)

The market encompasses significant investments in both onshore and offshore wind projects. While onshore developments have historically led, there is a notable increase in interest and activity in offshore wind, particularly in areas with consistent wind resources. This geographical diversification indicates a maturing market and a strategic focus on maximizing wind energy generation. Leading companies such as Vestas Wind Systems AS, Goldwind, and Neoen SA are actively expanding their presence in Australia, fostering a competitive environment and driving innovation. However, challenges related to grid integration, regulatory complexities, and the necessity for substantial infrastructure upgrades to accommodate increased renewable capacity may moderate the growth trajectory. Despite these challenges, the Australian wind power sector is on a robust growth path, vital for achieving national energy transition goals.

Australia Wind Power Industry Company Market Share

Australia Wind Power Market Analysis: Growth Drivers, Trends, and Forecast (2025-2033)

This comprehensive report delivers an in-depth analysis of the Australian wind power industry, a cornerstone of the nation's clean energy transition. Focusing on the forecast period from 2025 to 2033, with 2025 as the base year, the report provides critical insights into market dynamics, segmentation, key stakeholders, and future opportunities. We examine both overarching and specific market segments, offering a detailed view of the industry's evolution and its contribution to Australia's energy landscape. All data is presented in billions of Australian dollars.

Australia Wind Power Industry Market Dynamics & Structure

The Australian wind power industry is characterized by a moderately concentrated market structure, with a handful of key developers and turbine manufacturers dominating. Technological innovation is a primary driver, fueled by ongoing advancements in turbine efficiency and the increasing adoption of digital solutions for O&M. Regulatory frameworks, while supportive of renewable energy targets, can present complexities for project development. Competitive product substitutes are primarily other renewable energy sources like solar and battery storage, though wind power's scale and dispatchability offer distinct advantages. End-user demographics are shifting towards a greater demand for green energy from both industrial and residential sectors, driven by sustainability goals and energy security concerns. Mergers and acquisitions (M&A) trends are active, reflecting consolidation and strategic expansion within the sector.

- Market Concentration: Dominated by key players, indicating potential for strategic alliances and competitive dynamics.

- Technological Innovation: Driven by turbine upgrades, grid integration solutions, and data analytics for performance optimization.

- Regulatory Frameworks: Evolving policies and incentives continue to shape project viability and investment attractiveness.

- Competitive Substitutes: Solar PV and battery storage represent the primary alternatives, but wind's established infrastructure and capacity offer unique benefits.

- End-User Demographics: Growing demand from large industrial consumers seeking to decarbonize their operations and reduce energy costs.

- M&A Trends: Ongoing consolidation and strategic investments signal market maturity and a drive for scale.

Australia Wind Power Industry Growth Trends & Insights

The Australian wind power industry is poised for substantial growth, projected to expand significantly over the forecast period. Market size evolution is directly linked to Australia's ambitious renewable energy targets and the decreasing cost of wind energy technology. Adoption rates for new wind power projects are steadily increasing, driven by strong government policy support and growing investor confidence. Technological disruptions, such as the development of larger and more efficient turbines and advancements in energy storage integration, are further accelerating this growth. Consumer behavior shifts are evident, with an increasing preference for sustainably sourced energy and a willingness to invest in renewable solutions. The industry is projected to achieve a Compound Annual Growth Rate (CAGR) of approximately xx% between 2025 and 2033, with market penetration reaching xx% by the end of the forecast period.

Dominant Regions, Countries, or Segments in Australia Wind Power Industry

The Onshore wind power segment is currently the dominant force driving market growth in Australia. This dominance is attributable to a confluence of factors, including established infrastructure, favorable land availability, and a mature understanding of onshore wind technology. Economic policies, such as renewable energy certificates and tax incentives, have historically supported the development of numerous onshore wind farms across the country, particularly in regions with consistent wind resources. Infrastructure development, including transmission line upgrades and improved access to project sites, has also been crucial in facilitating the deployment of large-scale onshore wind projects.

- Key Drivers for Onshore Dominance:

- Favorable Wind Resource Availability: Extensive coastlines and interior regions with consistent wind patterns.

- Cost-Effectiveness: Lower capital expenditure and operational costs compared to offshore wind in the current Australian market.

- Policy Support: Government incentives and renewable energy targets have historically prioritized onshore development.

- Established Supply Chain: A more developed and accessible supply chain for onshore wind components and services.

- Land Availability: Ample suitable land for large-scale wind farm development across various states.

The market share for onshore wind power is estimated to be xx% of the total Australian wind power capacity in 2025. Growth potential remains robust, with ongoing project pipelines indicating continued expansion. While offshore wind is emerging as a significant future growth area, onshore wind is expected to maintain its leadership position for the foreseeable future due to its current maturity and economic advantages.

Australia Wind Power Industry Product Landscape

The Australian wind power industry's product landscape is defined by increasingly sophisticated and high-performance wind turbines. Innovations are focused on enhancing energy capture through larger rotor diameters and advanced aerodynamic blade designs, exemplified by Vestas' EnVentus platform. These turbines offer higher capacity factors and improved reliability. Applications span utility-scale power generation for grid supply to smaller, distributed systems for industrial and agricultural use. Performance metrics like annual energy production (AEP) and capacity factor continue to improve, driven by better wind resource assessment and predictive maintenance capabilities. Unique selling propositions include enhanced efficiency, reduced noise emissions, and greater adaptability to diverse site conditions, all contributing to a lower levelized cost of energy (LCOE).

Key Drivers, Barriers & Challenges in Australia Wind Power Industry

Key Drivers: The primary forces propelling the Australian wind power industry include supportive government policies aiming for carbon neutrality, declining technology costs making wind energy increasingly competitive, and a growing demand for clean energy from businesses and consumers. Technological advancements in turbine design and grid integration are also significant catalysts.

Barriers & Challenges: Significant challenges include the need for substantial grid infrastructure upgrades to accommodate intermittent generation, complex and sometimes lengthy planning and approval processes, and community acceptance for new project developments. Supply chain constraints for specialized components and the availability of skilled labor also pose potential restraints. The intermittency of wind power necessitates robust storage solutions, which adds to overall project costs.

Emerging Opportunities in Australia Wind Power Industry

Emerging opportunities lie in the development of offshore wind farms, unlocking vast untapped wind resources along Australia's extensive coastline. This segment promises higher capacity factors and reduced visual impact compared to onshore developments. Innovative applications such as green hydrogen production powered by wind energy present a significant future growth avenue. Evolving consumer preferences for certified green energy are also creating opportunities for community-owned wind projects and corporate power purchase agreements (PPAs) that directly support renewable energy generation. The integration of advanced energy storage solutions with wind farms offers further potential for grid stability and enhanced profitability.

Growth Accelerators in the Australia Wind Power Industry Industry

Growth in the Australian wind power industry is significantly accelerated by ongoing technological breakthroughs, particularly in turbine efficiency and materials science, leading to higher energy yields and lower costs. Strategic partnerships between developers, turbine manufacturers, and grid operators are crucial for overcoming infrastructure challenges and streamlining project execution. Market expansion strategies, including the pursuit of new project sites with exceptional wind resources and the development of hybrid renewable energy projects (wind and solar/storage), are further fueling growth. Investment in research and development for next-generation wind technologies, such as floating offshore wind platforms, will also be a key accelerator for long-term expansion.

Key Players Shaping the Australia Wind Power Industry Market

- Infigen Energy

- Epuron Pty Ltd

- Xinjiang Goldwind Science & Technology Co Ltd

- Neoen SA

- WestWind Energy

- Tilt Renewables

- Suzlon Energy Limited

- WestWind Energy Australia

- Vestas Wind Systems AS

- Acciona SA

Notable Milestones in Australia Wind Power Industry Sector

- December 2021: Alinta Energy announced plans to build a 1GW wind farm in Portland, south-western Victoria, aimed at supplying the Portland Aluminium Smelter and connecting to the east coast electricity grid.

- September 2021: Vestas, in partnership with Tilt Renewables, secured a 396 MW contract for the Rye Park Wind Farm in New South Wales. This project features Vestas' EnVentus platform, with 66 V162-6.2 MW wind turbines to be supplied and installed.

In-Depth Australia Wind Power Industry Market Outlook

The Australian wind power industry is set for sustained and robust growth, driven by a confluence of supportive policy frameworks, declining technological costs, and increasing demand for clean energy. Future market potential is immense, particularly with the burgeoning offshore wind sector poised to unlock significant new capacity. Strategic opportunities lie in fostering innovation in energy storage integration to enhance grid reliability and developing advanced manufacturing capabilities for wind turbine components within Australia. Furthermore, the industry will benefit from continued investment in grid modernization and the expansion of transmission infrastructure to facilitate the connection of new wind power projects. Continued collaboration between government, industry, and research institutions will be paramount in capitalizing on these opportunities and solidifying Australia's position as a leader in wind energy.

Australia Wind Power Industry Segmentation

-

1. Location of Deployment

- 1.1. Onshore

- 1.2. Offshore

Australia Wind Power Industry Segmentation By Geography

- 1. Australia

Australia Wind Power Industry Regional Market Share

Geographic Coverage of Australia Wind Power Industry

Australia Wind Power Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 5.1.1. Onshore

- 5.1.2. Offshore

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 6. Australia Wind Power Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 6.1.1. Onshore

- 6.1.2. Offshore

- 6.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Infigen Energy

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Epuron Pty Ltd*List Not Exhaustive

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Xinjiang Goldwind Science & Technology Co Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Neoen SA

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 WestWind Energy

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Tilt Renewables

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Suzlon Energy Limited

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 WestWind Energy Australia

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Vestas Wind Systems AS

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Acciona SA

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Infigen Energy

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Australia Wind Power Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Australia Wind Power Industry Share (%) by Company 2025

List of Tables

- Table 1: Australia Wind Power Industry Revenue billion Forecast, by Location of Deployment 2020 & 2033

- Table 2: Australia Wind Power Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Australia Wind Power Industry Revenue billion Forecast, by Location of Deployment 2020 & 2033

- Table 4: Australia Wind Power Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia Wind Power Industry?

The projected CAGR is approximately 13.1%.

2. Which companies are prominent players in the Australia Wind Power Industry?

Key companies in the market include Infigen Energy, Epuron Pty Ltd*List Not Exhaustive, Xinjiang Goldwind Science & Technology Co Ltd, Neoen SA, WestWind Energy, Tilt Renewables, Suzlon Energy Limited, WestWind Energy Australia, Vestas Wind Systems AS, Acciona SA.

3. What are the main segments of the Australia Wind Power Industry?

The market segments include Location of Deployment.

4. Can you provide details about the market size?

The market size is estimated to be USD 34.07 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Offshore Exploration and Production Activities4.; Development of Offshore Wind Energy.

6. What are the notable trends driving market growth?

Onshore Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Rising Demand for Dynamic Positioning (DP) Drilling Rigs.

8. Can you provide examples of recent developments in the market?

In December 2021, Australian energy company Alinta Energy announced to build a 1GW wind farm in Portland, south-western Victoria. The project would supply the Portland Aluminium Smelter and connect to the east coast electricity grid.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia Wind Power Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia Wind Power Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia Wind Power Industry?

To stay informed about further developments, trends, and reports in the Australia Wind Power Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence