Key Insights

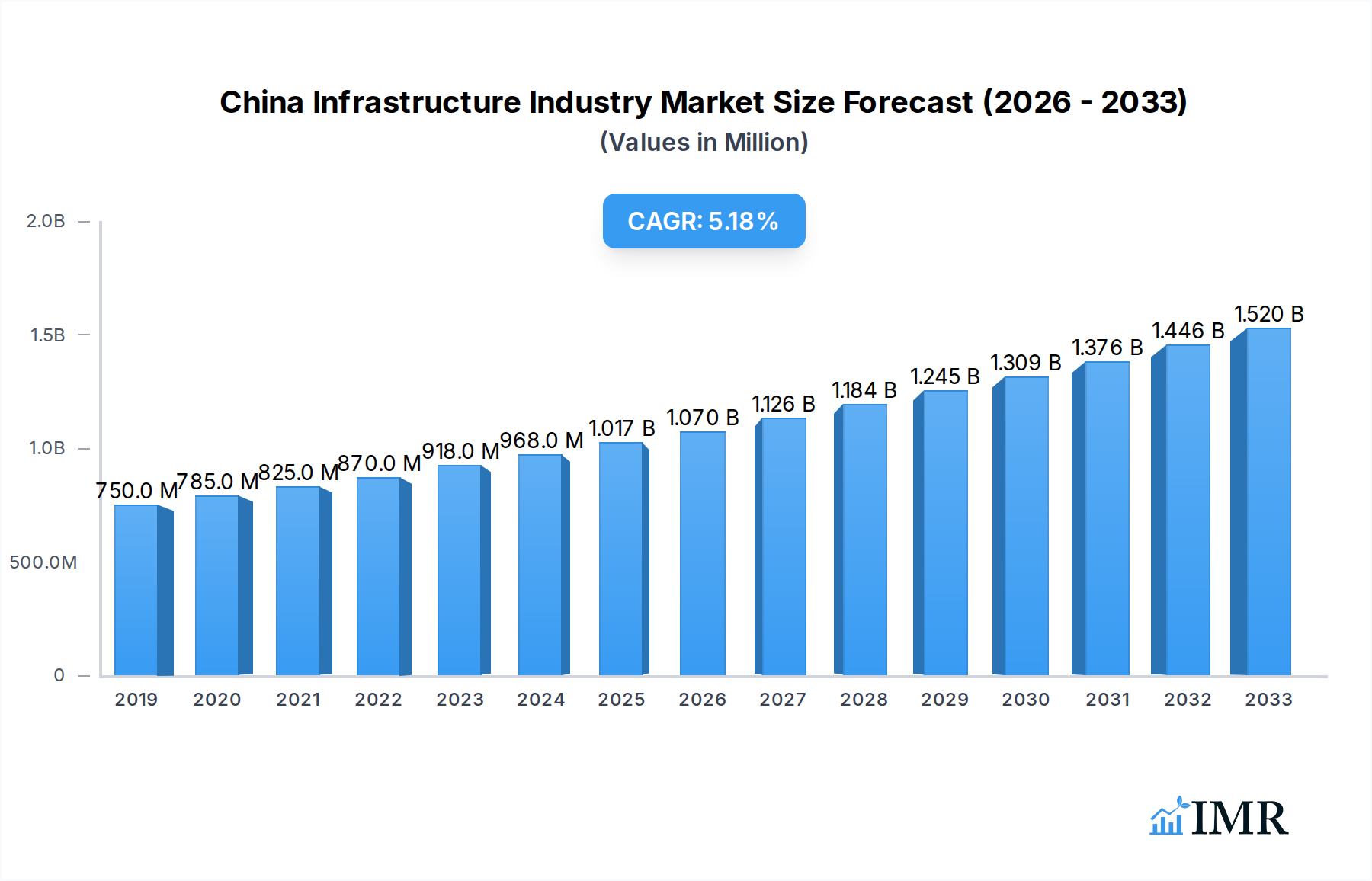

The China Infrastructure Industry is poised for substantial growth, projected to reach $1.10 billion by 2025 and expand at a robust Compound Annual Growth Rate (CAGR) of 6.32% through 2033. This dynamic market is being propelled by significant investments in a diverse range of infrastructure segments. Transportation infrastructure, encompassing railways, roadways, airports, and waterways, is a primary driver, facilitating the nation's economic connectivity and trade. Concurrently, the burgeoning demand for energy and digital connectivity is fueling expansion in Extraction Infrastructure, particularly in power generation, electricity transmission and distribution, and telecommunications. Manufacturing infrastructure is also a key area of focus, with ongoing development in metal and ore production, petroleum refining, chemical manufacturing, and the establishment of industrial parks to support domestic production and global supply chains. Social infrastructure, including schools and hospitals, is receiving increased attention to enhance public services and living standards across the nation.

China Infrastructure Industry Market Size (In Million)

The strategic development of key economic hubs like Shanghai, Beijing, and Shenzhen further underscores the concentrated nature of infrastructure investment and innovation. While the market benefits from strong government support and a clear vision for national development, potential restraints could emerge from evolving regulatory landscapes, increasing environmental sustainability demands, and the need for efficient land acquisition and resource allocation. Nevertheless, the sheer scale of planned projects and the continuous technological advancements within the sector, driven by leading companies such as China State Construction Engineering, China Communications Construction Company, and China Railway Group Limited, indicate a resilient and expanding market. The industry's ability to adapt to these challenges and leverage emerging trends, such as smart city technologies and green infrastructure, will be critical in realizing its full growth potential.

China Infrastructure Industry Company Market Share

Unveiling the Future: China Infrastructure Industry Market Report (2019-2033)

This comprehensive report offers an in-depth analysis of the China infrastructure industry, a pivotal sector driving global economic growth. Spanning from 2019 to 2033, with a base and estimated year of 2025 and a forecast period from 2025 to 2033, this research provides critical insights into market dynamics, growth trends, regional dominance, product landscape, key drivers, emerging opportunities, growth accelerators, leading players, notable milestones, and a future market outlook. All monetary values are presented in Million units.

China Infrastructure Industry Market Dynamics & Structure

The China infrastructure industry exhibits a moderate to high market concentration, with a few dominant state-owned enterprises and a growing number of private players. Technological innovation is a significant driver, spurred by the government's push for smart cities, sustainable development, and digital transformation across all infrastructure segments. Regulatory frameworks, though evolving, continue to shape project approvals, environmental standards, and investment policies, often favoring large-scale, integrated projects. Competitive product substitutes are relatively limited in core infrastructure, but advancements in construction materials, energy-efficient technologies, and smart city solutions are emerging. End-user demographics are increasingly sophisticated, demanding resilient, sustainable, and digitally integrated infrastructure. Mergers and acquisitions (M&A) are a strategic tool for consolidation, market expansion, and technology acquisition, with recent deal volumes indicating a strong appetite for strategic alliances.

- Market Concentration: Dominated by major state-owned enterprises, but with increasing participation from private and international firms.

- Technological Innovation Drivers: Smart city initiatives, renewable energy integration, advanced materials, digital construction techniques.

- Regulatory Frameworks: Government-led planning, environmental impact assessments, public-private partnership (PPP) models, evolving standards for safety and sustainability.

- Competitive Product Substitutes: Innovations in green building materials, modular construction, energy storage solutions, and advanced telecommunications.

- End-User Demographics: Growing demand for sustainable, resilient, accessible, and digitally connected infrastructure.

- M&A Trends: Strategic acquisitions for market access, technology integration, and portfolio diversification.

China Infrastructure Industry Growth Trends & Insights

The China infrastructure industry is poised for substantial growth, driven by ongoing urbanization, economic development, and national strategic initiatives. The market size is projected to expand significantly over the forecast period, fueled by consistent government investment and private sector participation. Adoption rates for advanced construction technologies and sustainable practices are accelerating, as the industry embraces efficiency and environmental responsibility. Technological disruptions are a defining characteristic, with the integration of AI, IoT, and big data transforming project planning, execution, and maintenance. Consumer behavior shifts are evident, with an increasing demand for high-quality, user-friendly, and environmentally conscious infrastructure that supports a modern lifestyle. The Compound Annual Growth Rate (CAGR) is expected to remain robust, indicating sustained expansion. Market penetration of digital infrastructure solutions, such as 5G networks and smart grids, is rapidly increasing.

- Market Size Evolution: Projecting consistent and significant expansion fueled by government policy and economic growth.

- Adoption Rates: Rapid uptake of advanced construction methods, digital technologies, and sustainable materials.

- Technological Disruptions: Transformation through AI, IoT, big data, and automation in construction and infrastructure management.

- Consumer Behavior Shifts: Growing demand for resilient, sustainable, accessible, and digitally integrated infrastructure services.

- CAGR: Robust growth expected, reflecting the sector's vital role in national development.

- Market Penetration: Increasing adoption of smart technologies, renewable energy integration, and advanced transportation systems.

Dominant Regions, Countries, or Segments in China Infrastructure Industry

The Extraction Infrastructure segment, particularly Power Generation and Electricity Transmission and Distribution, along with Transportation Infrastructure, specifically Railways and Roadways, are currently the dominant forces driving the China infrastructure industry. These segments benefit from massive, long-term government investment and are critical for supporting the nation's industrial and economic activities. Key cities like Shanghai, Beijing, and Shenzhen serve as epicenters for infrastructure development, embodying the nation's commitment to modernization and smart city living. Shanghai, as a global financial hub and a major port city, leads in port development, urban rail expansion, and smart city solutions. Beijing, the capital, focuses on large-scale transportation networks, urban renewal, and critical social infrastructure. Shenzhen, a technology powerhouse, is at the forefront of smart city infrastructure, advanced telecommunications networks, and innovation-driven development. The dominance is further bolstered by economic policies that prioritize energy security, efficient logistics, and connectivity.

- Dominant Segments: Extraction Infrastructure (Power Generation, Electricity Transmission & Distribution), Transportation Infrastructure (Railways, Roadways).

- Key Cities: Shanghai, Beijing, Shenzhen – spearheading development and innovation.

- Economic Policies: Government prioritization of energy security, sustainable development, and connectivity.

- Infrastructure Investment: Sustained and substantial capital allocation in strategic infrastructure projects.

- Growth Potential: High potential for continued expansion, driven by ongoing urbanization and technological integration.

- Market Share: Extraction and Transportation Infrastructure segments command the largest share of investment and development.

China Infrastructure Industry Product Landscape

The China infrastructure industry's product landscape is characterized by innovation and scale. Products range from massive civil engineering components for high-speed rail and bridges to sophisticated smart grid technologies and advanced telecommunications hardware. Unique selling propositions often lie in the integration of sustainability features, such as low-carbon concrete and energy-efficient lighting systems. Technological advancements are evident in the development of high-strength, lightweight construction materials and intelligent monitoring systems for structural health. Applications span from powering megacities with clean energy to connecting remote regions with high-speed internet, demonstrating a commitment to both economic progress and improved quality of life. Performance metrics are increasingly focused on durability, energy efficiency, and operational intelligence.

Key Drivers, Barriers & Challenges in China Infrastructure Industry

Key Drivers: The China infrastructure industry is propelled by several key forces. Government initiatives such as the Belt and Road Initiative (BRI) and the national strategy for sustainable development are significant accelerators. Technological advancements, including modular construction, AI-powered project management, and renewable energy solutions, are driving efficiency and innovation. Economic growth and increasing urbanization necessitate continuous infrastructure upgrades and expansion. Foreign direct investment and public-private partnerships (PPPs) are also crucial in mobilizing capital and expertise.

Barriers & Challenges: Despite robust growth, the industry faces challenges. Regulatory hurdles and complex approval processes can cause project delays. Supply chain disruptions, particularly for specialized materials and equipment, can impact timelines and costs, with an estimated xx% impact on project timelines in some instances. Environmental concerns and the need for sustainable practices require significant investment in green technologies. Intense competition among domestic and international players can pressure profit margins. Furthermore, rising labor costs and the need for skilled workforce development present ongoing challenges.

Emerging Opportunities in China Infrastructure Industry

Emerging opportunities in the China infrastructure industry are abundant, particularly in the realm of sustainable development and digital transformation. The burgeoning green infrastructure market, encompassing renewable energy projects, smart grids, and sustainable transportation solutions, presents immense potential. The smart city initiatives are creating demand for integrated digital platforms, intelligent traffic management systems, and advanced telecommunications networks, especially 5G deployment. The aging infrastructure renewal market, focusing on modernizing existing assets for increased efficiency and resilience, offers another significant avenue. Furthermore, the increasing focus on rural revitalization is opening up opportunities for infrastructure development in previously underserved regions.

Growth Accelerators in the China Infrastructure Industry Industry

Several catalysts are accelerating the growth of the China infrastructure industry. Technological breakthroughs in areas such as high-speed rail, offshore wind power, and smart grid technology are creating new project pipelines and enhancing efficiency. Strategic partnerships between state-owned enterprises and private firms, as well as international collaborations, are crucial for knowledge transfer and capital mobilization. Government support through policy incentives, favorable financing, and streamlined approval processes remains a critical growth accelerator. The continued expansion of China's global influence, particularly through the Belt and Road Initiative, is creating international demand for Chinese infrastructure expertise and services.

Key Players Shaping the China Infrastructure Industry Market

- China Resources Power Holdings Company Limited

- China National Chemical Engineering

- China Metallurgical Group Corporation

- China State Construction Engineering

- China Electric Power Construction Co LTD

- China Communications Construction Company

- China Energy Engineering Corporation

- Shanghai Construction Group

- China Railway Group Limited

- China Power International Development Limited

- China Railway Construction Corporation

Notable Milestones in China Infrastructure Industry Sector

- 2019: Launch of significant smart city pilot programs in major urban centers.

- 2020: Accelerated construction and deployment of 5G networks nationwide.

- 2021: Increased investment in renewable energy infrastructure, particularly solar and wind power.

- 2022: Major advancements in high-speed rail network expansion and upgrades.

- 2023: Growing emphasis on sustainable construction materials and practices in new projects.

- 2024: Significant project completions in transportation infrastructure, enhancing inter-city connectivity.

In-Depth China Infrastructure Industry Market Outlook

The outlook for the China infrastructure industry remains exceptionally strong, driven by a convergence of strategic government imperatives, technological innovation, and robust economic fundamentals. Growth accelerators like continued investment in smart cities, renewable energy, and advanced transportation systems are set to propel the market forward. Emerging opportunities in green infrastructure and rural development offer vast untapped potential. Strategic partnerships and technological breakthroughs will further enhance efficiency and sustainability. The industry is well-positioned to not only meet domestic demand but also to play an increasingly influential role on the global stage, solidifying its position as a vital engine of economic progress and a key player in shaping the future of global infrastructure.

China Infrastructure Industry Segmentation

-

1. Type

-

1.1. Social Infrastructure

- 1.1.1. Schools

- 1.1.2. Hospitals

- 1.1.3. Defence

- 1.1.4. Other Social Infrastructures

-

1.2. Transportation Infrastructure

- 1.2.1. Railways

- 1.2.2. Roadways

- 1.2.3. Airports

- 1.2.4. Waterways

-

1.3. Extraction Infrastructure

- 1.3.1. Power Generation

- 1.3.2. Electricity Transmission and Distribution

- 1.3.3. Gas

- 1.3.4. Telecoms

-

1.4. Manufacturing Infrastructure

- 1.4.1. Metal and Ore Production

- 1.4.2. Petroleum Refining

- 1.4.3. Chemical Manufacturing

- 1.4.4. Industrial Parks and clusters

- 1.4.5. Other Manufacturing Infrastructures

-

1.1. Social Infrastructure

-

2. Key Cities

- 2.1. Shanghai

- 2.2. Beijing

- 2.3. Shenzhen

China Infrastructure Industry Segmentation By Geography

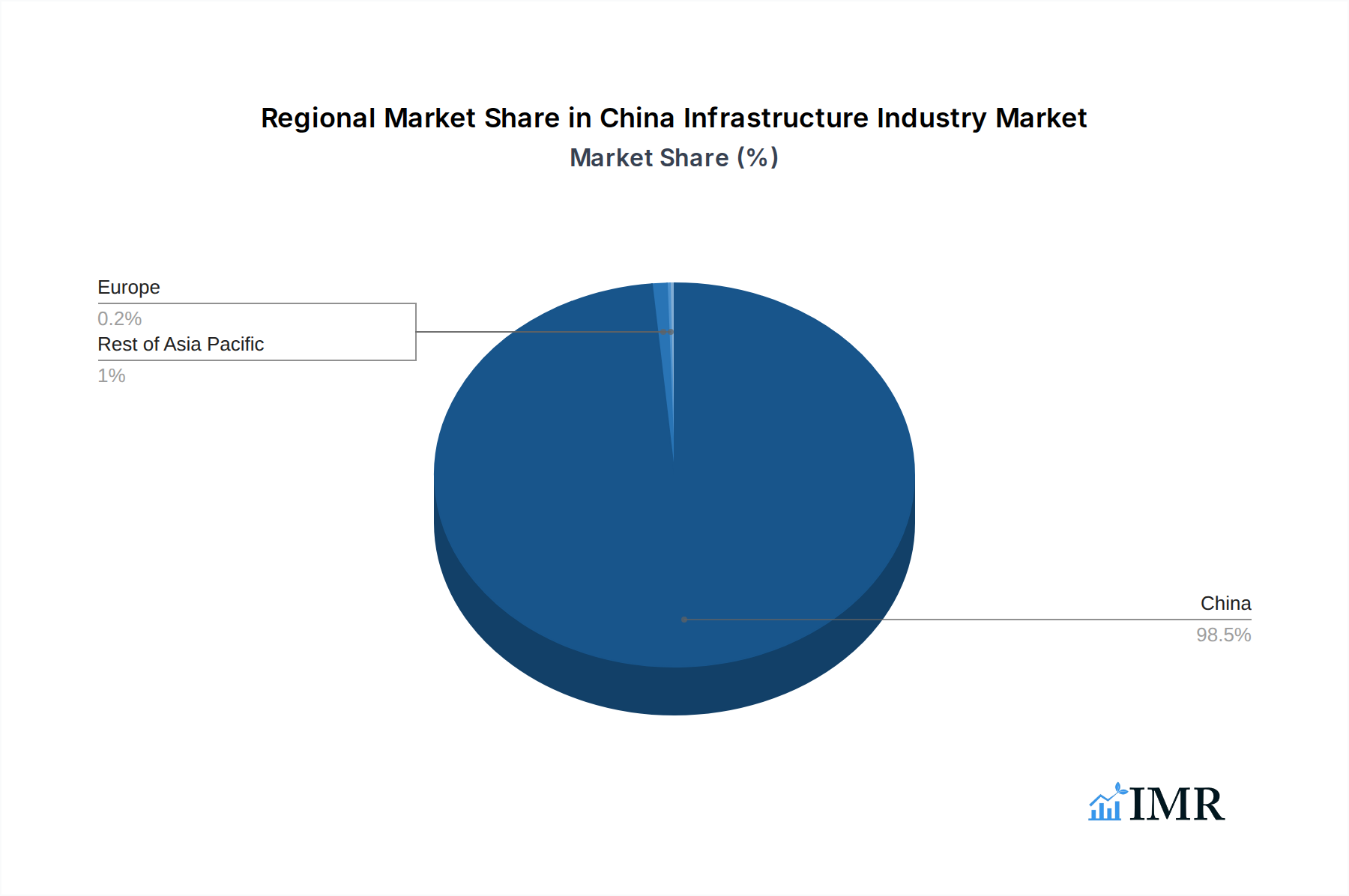

- 1. China

China Infrastructure Industry Regional Market Share

Geographic Coverage of China Infrastructure Industry

China Infrastructure Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.32% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Social Infrastructure

- 5.1.1.1. Schools

- 5.1.1.2. Hospitals

- 5.1.1.3. Defence

- 5.1.1.4. Other Social Infrastructures

- 5.1.2. Transportation Infrastructure

- 5.1.2.1. Railways

- 5.1.2.2. Roadways

- 5.1.2.3. Airports

- 5.1.2.4. Waterways

- 5.1.3. Extraction Infrastructure

- 5.1.3.1. Power Generation

- 5.1.3.2. Electricity Transmission and Distribution

- 5.1.3.3. Gas

- 5.1.3.4. Telecoms

- 5.1.4. Manufacturing Infrastructure

- 5.1.4.1. Metal and Ore Production

- 5.1.4.2. Petroleum Refining

- 5.1.4.3. Chemical Manufacturing

- 5.1.4.4. Industrial Parks and clusters

- 5.1.4.5. Other Manufacturing Infrastructures

- 5.1.1. Social Infrastructure

- 5.2. Market Analysis, Insights and Forecast - by Key Cities

- 5.2.1. Shanghai

- 5.2.2. Beijing

- 5.2.3. Shenzhen

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. China Infrastructure Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Social Infrastructure

- 6.1.1.1. Schools

- 6.1.1.2. Hospitals

- 6.1.1.3. Defence

- 6.1.1.4. Other Social Infrastructures

- 6.1.2. Transportation Infrastructure

- 6.1.2.1. Railways

- 6.1.2.2. Roadways

- 6.1.2.3. Airports

- 6.1.2.4. Waterways

- 6.1.3. Extraction Infrastructure

- 6.1.3.1. Power Generation

- 6.1.3.2. Electricity Transmission and Distribution

- 6.1.3.3. Gas

- 6.1.3.4. Telecoms

- 6.1.4. Manufacturing Infrastructure

- 6.1.4.1. Metal and Ore Production

- 6.1.4.2. Petroleum Refining

- 6.1.4.3. Chemical Manufacturing

- 6.1.4.4. Industrial Parks and clusters

- 6.1.4.5. Other Manufacturing Infrastructures

- 6.1.1. Social Infrastructure

- 6.2. Market Analysis, Insights and Forecast - by Key Cities

- 6.2.1. Shanghai

- 6.2.2. Beijing

- 6.2.3. Shenzhen

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 China Resources Power Holdings Company Limited**List Not Exhaustive

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 China National Chemical Engineering

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 China Metallurgical Group Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 China State Construction Engineering

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 China Electric Power Construction Co LTD

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 China Communications Construction Company

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 China Energy Engineering Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Shanghai Construction Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 China Railway Group Limited

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 China Power International Development Limited

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 China Railway Construction Corporation

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 China Resources Power Holdings Company Limited**List Not Exhaustive

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Infrastructure Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: China Infrastructure Industry Share (%) by Company 2025

List of Tables

- Table 1: China Infrastructure Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: China Infrastructure Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 3: China Infrastructure Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: China Infrastructure Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: China Infrastructure Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 6: China Infrastructure Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Infrastructure Industry?

The projected CAGR is approximately 6.32%.

2. Which companies are prominent players in the China Infrastructure Industry?

Key companies in the market include China Resources Power Holdings Company Limited**List Not Exhaustive, China National Chemical Engineering, China Metallurgical Group Corporation, China State Construction Engineering, China Electric Power Construction Co LTD, China Communications Construction Company, China Energy Engineering Corporation, Shanghai Construction Group, China Railway Group Limited, China Power International Development Limited, China Railway Construction Corporation.

3. What are the main segments of the China Infrastructure Industry?

The market segments include Type, Key Cities.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.10 Million as of 2022.

5. What are some drivers contributing to market growth?

Asia Pacific countries are investing in infrastructure projects to improve regional connectivity and promote economic integration; The Asia Pacific region has a large and growing population. along with a rising middle class.

6. What are the notable trends driving market growth?

Transportation Infrastructure is Witnessing Significant Growth.

7. Are there any restraints impacting market growth?

Limited public budgets and difficulties in attracting private investment can hinder the financing of large-scale projects; Delays in land acquisition can significantly impact project timelines and costs.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Infrastructure Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Infrastructure Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Infrastructure Industry?

To stay informed about further developments, trends, and reports in the China Infrastructure Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence