Key Insights

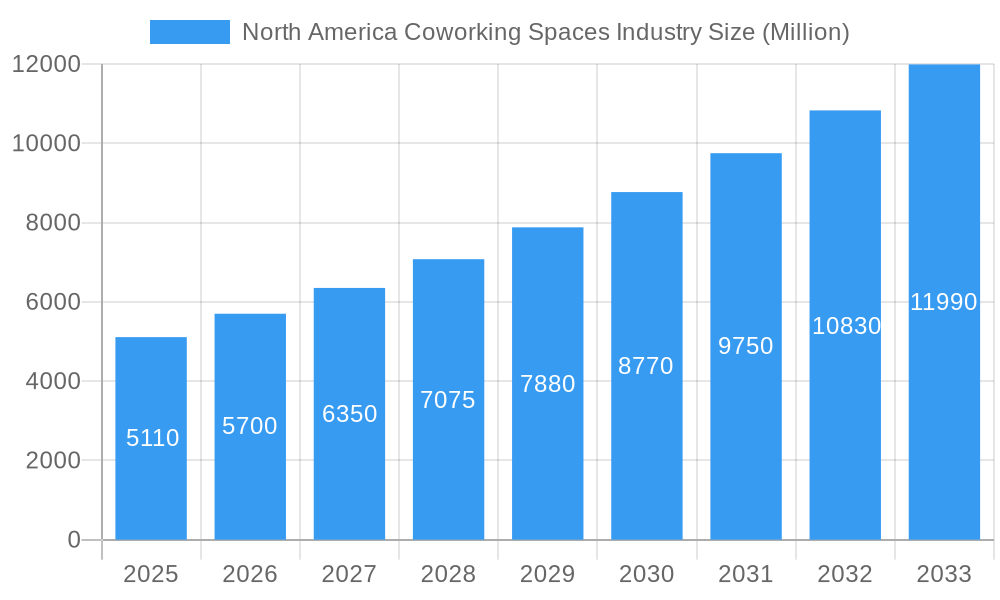

The North American coworking spaces industry is experiencing robust growth, projected to reach a market size of $5.11 billion in 2025 and maintain a Compound Annual Growth Rate (CAGR) exceeding 11% through 2033. This expansion is driven by several key factors. The increasing popularity of remote work and the gig economy fuels demand for flexible, professional workspaces among independent professionals, startups, and SMEs. Large corporations are also adopting coworking spaces for satellite offices, project-based teams, and to access diverse talent pools. Furthermore, the diverse business models—sub-lease, revenue sharing, and owner-operator—cater to various market needs and investment strategies. The industry's segmentation by business type (new spaces, expansions, chains) highlights the multifaceted nature of market development, with established players expanding their footprint alongside new entrants. Geographic distribution across the United States, Canada, and Mexico showcases a strong regional concentration within North America, with the US likely representing the largest market share.

North America Coworking Spaces Industry Market Size (In Billion)

The sustained growth trajectory is underpinned by several trends. Technological advancements, including improved booking systems and workspace management platforms, enhance user experience and operational efficiency. A focus on community building and networking opportunities within coworking spaces adds value beyond simple desk rentals, fostering collaboration and innovation. However, economic downturns could pose a challenge, potentially impacting demand, particularly among smaller businesses. Competition among existing and new players remains a factor that will continue to shape market dynamics. Furthermore, the evolution of hybrid work models—combining remote and in-office work—will influence demand and the nature of services offered by coworking spaces in the coming years. Successful players will likely adapt their offerings to meet these evolving needs, focusing on providing flexible, high-quality spaces with enhanced amenities and community features.

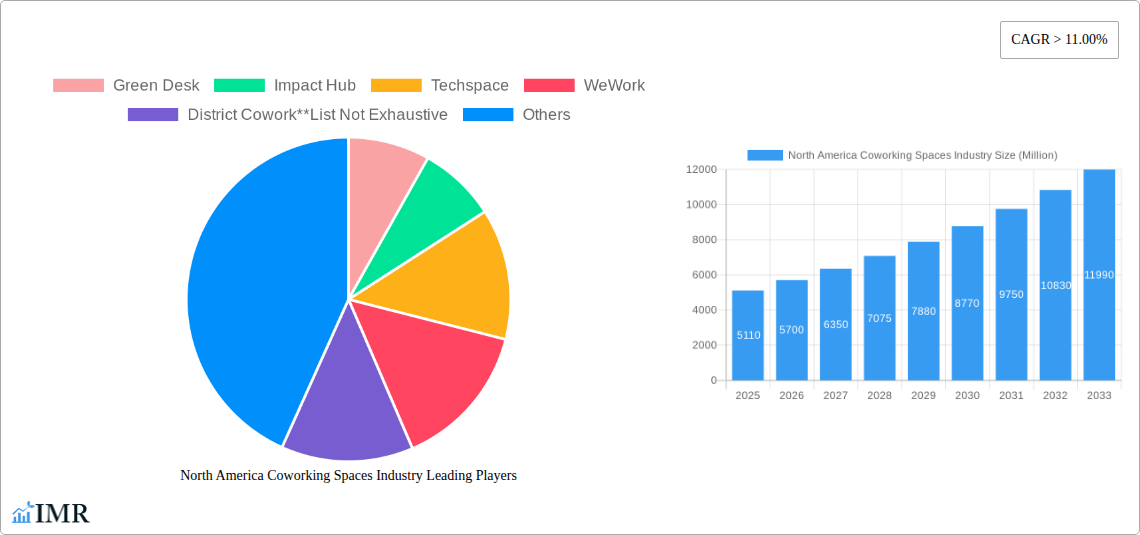

North America Coworking Spaces Industry Company Market Share

North America Coworking Spaces Industry: 2019-2033 Market Report

This comprehensive report delivers an in-depth analysis of the North American coworking spaces industry, encompassing market dynamics, growth trends, key players, and future projections from 2019 to 2033. The report leverages extensive data and expert insights to provide a crucial resource for industry professionals, investors, and strategic planners. We analyze the parent market of commercial real estate and its child market of flexible workspaces, offering a granular view of this dynamic sector. The study period covers 2019–2033, with 2025 as the base and estimated year. The forecast period spans 2025–2033, and the historical period encompasses 2019–2024.

North America Coworking Spaces Industry Market Dynamics & Structure

This section analyzes the competitive landscape, technological advancements, regulatory environment, and market trends within the North American coworking spaces industry. The market is characterized by a diverse range of players, from large international chains like WeWork to smaller, localized operators. Market concentration is moderate, with a few dominant players alongside numerous smaller firms.

- Market Concentration: WeWork and Regus hold significant market share (xx%), followed by a fragmented landscape of regional and independent operators.

- Technological Innovation: Technological advancements, such as smart building technologies and booking platforms, are driving efficiency and enhancing user experience. However, integration and cybersecurity remain significant innovation barriers.

- Regulatory Frameworks: Zoning regulations, building codes, and tax policies vary across different regions and impact the feasibility and cost of establishing new coworking spaces.

- Competitive Product Substitutes: Traditional office spaces, remote work arrangements, and virtual offices pose competitive challenges.

- End-User Demographics: The industry serves a wide spectrum of users, including independent professionals, startups, SMEs, and large corporations. Shifting demographics and work preferences influence demand.

- M&A Trends: The industry has witnessed a wave of mergers and acquisitions (M&A) activity, with xx deals recorded between 2019 and 2024, primarily driven by consolidation and expansion strategies. This consolidation trend is expected to continue, though at a moderate pace.

North America Coworking Spaces Industry Growth Trends & Insights

The North American coworking spaces market has experienced significant growth since 2019. Driven by a shift towards flexible work arrangements, the adoption rate of coworking spaces has accelerated, particularly among younger professionals and startups. This trend is further amplified by factors such as increasing urbanization, the rise of the gig economy, and businesses seeking cost-effective office solutions. The market witnessed a temporary slowdown in 2020 due to the pandemic, but a robust recovery is underway, driven by the hybrid work model’s acceptance. The compound annual growth rate (CAGR) from 2019 to 2024 was xx%, and it is projected to be xx% from 2025 to 2033. Market penetration is expected to reach xx% by 2033. Technological disruptions, such as virtual reality and augmented reality applications for virtual office experiences, will shape future growth. Consumer behavior shifts, driven by increasing demand for amenities and community features, will also play a significant role.

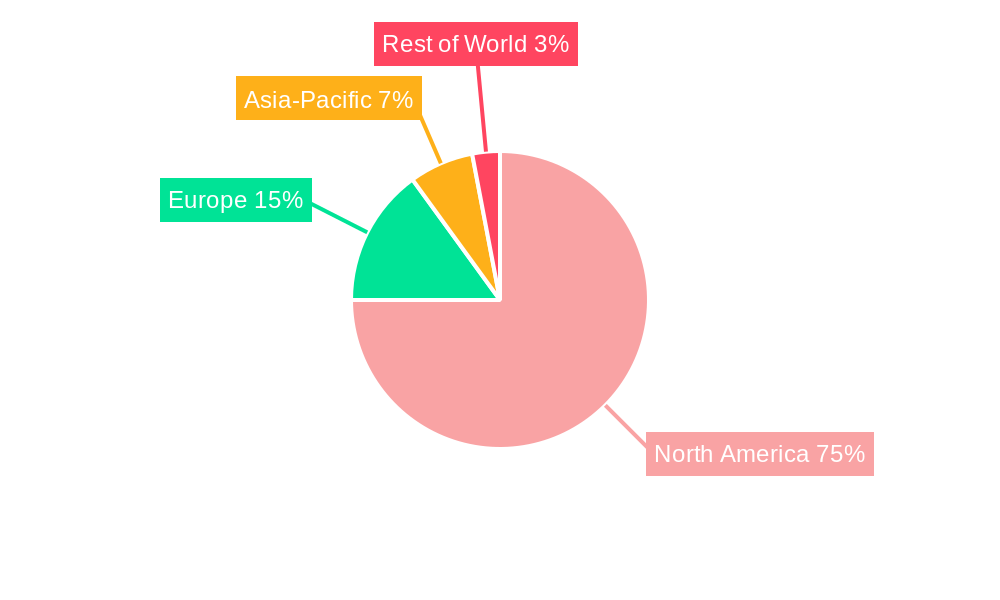

Dominant Regions, Countries, or Segments in North America Coworking Spaces Industry

The United States dominates the North American coworking spaces market, followed by Canada and Mexico. Within the US, major metropolitan areas such as New York, Los Angeles, and San Francisco exhibit the highest concentration of coworking spaces and consequently, the greatest market share.

- By Business Type: The expansion of existing chains dominates the market, followed by the establishment of new spaces.

- By Business Model: The revenue-sharing model is most prevalent, followed by the sub-lease model. Owner-operator models are more common among smaller players.

- By End User: SMEs constitute the largest end-user segment, followed by independent professionals and startup teams. Large-scale corporations are increasingly adopting coworking spaces for specific teams or projects.

- By Country: The United States holds the largest market share, significantly surpassing Canada and Mexico due to its larger economy and denser urban populations. Growth in Canada and Mexico is projected to be higher than in the US in the coming years.

Key drivers for growth include favorable economic policies, the development of robust infrastructure, and the increasing availability of venture capital funding for startups.

North America Coworking Spaces Industry Product Landscape

Coworking spaces offer a variety of products and services, including flexible lease terms, high-speed internet, meeting rooms, shared amenities, and community events. The industry is witnessing product innovation in the form of specialized spaces tailored for specific industries (e.g., tech hubs, creative studios), enhanced technological integration (e.g., smart office solutions, virtual office tools), and a heightened focus on wellness amenities. Unique selling propositions increasingly center on community building, networking opportunities, and a focus on sustainable practices.

Key Drivers, Barriers & Challenges in North America Coworking Spaces Industry

Key Drivers: Increased demand for flexible workspaces, rising urbanization, the growth of the gig economy, and technological advancements are key drivers. Government initiatives promoting entrepreneurship and flexible work arrangements also contribute.

Challenges: Competition from traditional office spaces and remote work options, economic downturns impacting demand, and the need for continuous innovation to stay ahead of evolving customer preferences are significant challenges. Supply chain disruptions impacting construction and furnishing costs also pose a constraint. Regulatory hurdles and obtaining permits in certain locations add further complexity.

Emerging Opportunities in North America Coworking Spaces Industry

Emerging opportunities include the expansion into secondary and tertiary markets, the development of specialized coworking spaces for specific industries, the incorporation of sustainable and eco-friendly practices, and the integration of advanced technologies to enhance user experience and operational efficiency. The growing demand for hybrid work models and the increasing importance of community building present significant opportunities.

Growth Accelerators in the North America Coworking Spaces Industry

Technological innovation in building management systems and booking platforms, strategic partnerships with tech companies and corporations, and expansion into underserved markets are key growth accelerators. Adapting to the changing preferences of users by incorporating wellness and sustainability aspects will also play a crucial role.

Key Players Shaping the North America Coworking Spaces Industry Market

- Green Desk

- Impact Hub

- Techspace

- WeWork

- District Cowork

- Serendipity Labs

- Regus Coworking

- Mix Pace

- Industrious Office

- Knotel

Notable Milestones in North America Coworking Spaces Industry Sector

- June 2022: IWG plans to add 500-700 flexible office sites in the US within 12 months. This significantly expands the market's capacity and intensifies competition.

- November 2022: Knotel secures a long-term lease in Coral Gables, Florida, indicating continued expansion despite market fluctuations. This expansion signals confidence in the long-term growth of the sector.

In-Depth North America Coworking Spaces Industry Market Outlook

The North American coworking spaces market exhibits strong long-term growth potential. Continued urbanization, the rise of remote and hybrid work models, and the increasing adoption of flexible work arrangements will fuel market expansion. Strategic acquisitions, technological innovation, and a focus on creating vibrant and community-driven workspaces will be crucial for continued success in this evolving industry. The market is poised for significant growth, driven by evolving work styles and the ongoing demand for flexible and collaborative work environments. Strategic partnerships and innovations in technology will define the competitive landscape in the coming years.

North America Coworking Spaces Industry Segmentation

-

1. Business Type

- 1.1. New Spaces

- 1.2. Expansions

- 1.3. Chains

-

2. Business Model

- 2.1. Sub-lease Model

- 2.2. Revenue Sharing Model

- 2.3. Owner-Operator Model

-

3. End User

- 3.1. Independent Professionals (Freelancers)

- 3.2. Startup Teams

- 3.3. Small to Medium Sized Enterprises (SMEs)

- 3.4. Large Scale Corporations

North America Coworking Spaces Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Coworking Spaces Industry Regional Market Share

Geographic Coverage of North America Coworking Spaces Industry

North America Coworking Spaces Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 11.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Business Type

- 5.1.1. New Spaces

- 5.1.2. Expansions

- 5.1.3. Chains

- 5.2. Market Analysis, Insights and Forecast - by Business Model

- 5.2.1. Sub-lease Model

- 5.2.2. Revenue Sharing Model

- 5.2.3. Owner-Operator Model

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Independent Professionals (Freelancers)

- 5.3.2. Startup Teams

- 5.3.3. Small to Medium Sized Enterprises (SMEs)

- 5.3.4. Large Scale Corporations

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Business Type

- 6. North America Coworking Spaces Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Business Type

- 6.1.1. New Spaces

- 6.1.2. Expansions

- 6.1.3. Chains

- 6.2. Market Analysis, Insights and Forecast - by Business Model

- 6.2.1. Sub-lease Model

- 6.2.2. Revenue Sharing Model

- 6.2.3. Owner-Operator Model

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Independent Professionals (Freelancers)

- 6.3.2. Startup Teams

- 6.3.3. Small to Medium Sized Enterprises (SMEs)

- 6.3.4. Large Scale Corporations

- 6.1. Market Analysis, Insights and Forecast - by Business Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Green Desk

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Impact Hub

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Techspace

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 WeWork

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 District Cowork**List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Serendipity Labs

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Regus Coworking

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Mix Pace

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Industrious Office

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Knotel

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Green Desk

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Coworking Spaces Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: North America Coworking Spaces Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Coworking Spaces Industry Revenue Million Forecast, by Business Type 2020 & 2033

- Table 2: North America Coworking Spaces Industry Revenue Million Forecast, by Business Model 2020 & 2033

- Table 3: North America Coworking Spaces Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 4: North America Coworking Spaces Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: North America Coworking Spaces Industry Revenue Million Forecast, by Business Type 2020 & 2033

- Table 6: North America Coworking Spaces Industry Revenue Million Forecast, by Business Model 2020 & 2033

- Table 7: North America Coworking Spaces Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 8: North America Coworking Spaces Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States North America Coworking Spaces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada North America Coworking Spaces Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Mexico North America Coworking Spaces Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Coworking Spaces Industry?

The projected CAGR is approximately > 11.00%.

2. Which companies are prominent players in the North America Coworking Spaces Industry?

Key companies in the market include Green Desk, Impact Hub, Techspace, WeWork, District Cowork**List Not Exhaustive, Serendipity Labs, Regus Coworking, Mix Pace, Industrious Office, Knotel.

3. What are the main segments of the North America Coworking Spaces Industry?

The market segments include Business Type, Business Model, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.11 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing demand for flexible office spaces; Surge in investments in niche co-working spaces such as women-only spaces. LGBTQ+ spaces. and other social groups.

6. What are the notable trends driving market growth?

Increasing number of Startups Boosting the Market.

7. Are there any restraints impacting market growth?

Low Awareness and Privacy Issues.

8. Can you provide examples of recent developments in the market?

November 2022: The Newmark-owned firm Knotel secured a long-term lease for 23,700 square feet at Ofizzina, a Coral Gables, Florida, office condo project. Knotel intends to finish three complete stories of the 16-story skyscraper at 1200 Ponce De Leon Boulevard. TSG Group and BF Group created Offizina, which comprises 60 office condominiums.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Coworking Spaces Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Coworking Spaces Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Coworking Spaces Industry?

To stay informed about further developments, trends, and reports in the North America Coworking Spaces Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence