Key Insights

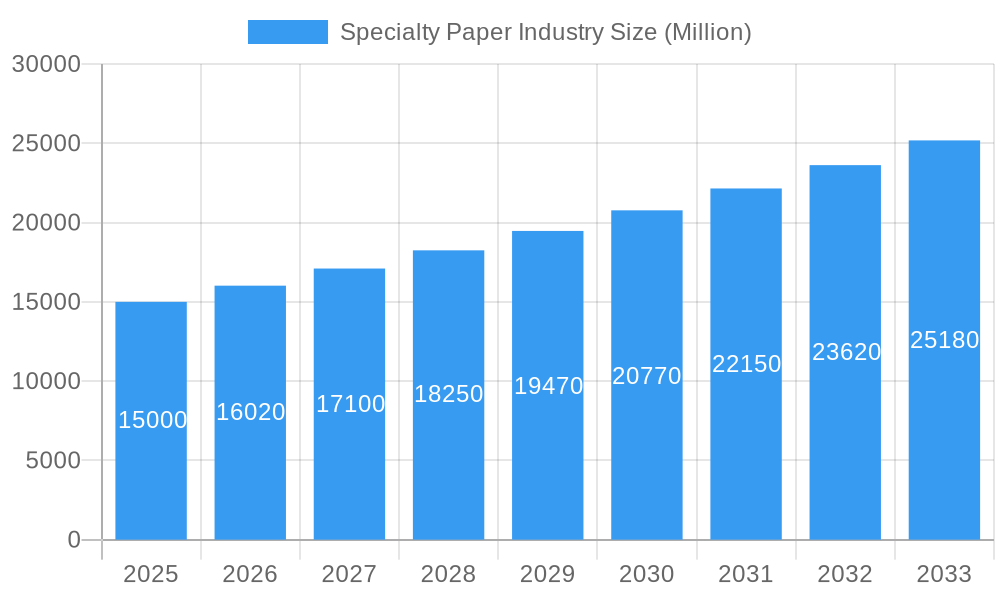

The global specialty paper market is projected for substantial growth, with an estimated market size of $18 billion in 2025. The market is expected to expand at a compound annual growth rate (CAGR) of 5.1% from 2025 to 2033. This upward trend is propelled by increasing demand for sustainable packaging solutions across sectors such as food service, printing, and construction. The surge in e-commerce packaging, particularly for kraft paper and container board, along with growing adoption of specialty labels and flexible packaging, further fuels market expansion. Innovations in paper manufacturing, offering enhanced functionality and customization, also contribute positively. Key challenges include raw material price volatility and stringent environmental regulations. The market is segmented by end-user industry, with packaging and labeling dominating, and by paper type, led by kraft paper and container board. North America and Europe currently lead market share, while Asia Pacific is poised for significant growth due to its expanding industrial base and rising consumer expenditure.

Specialty Paper Industry Market Size (In Billion)

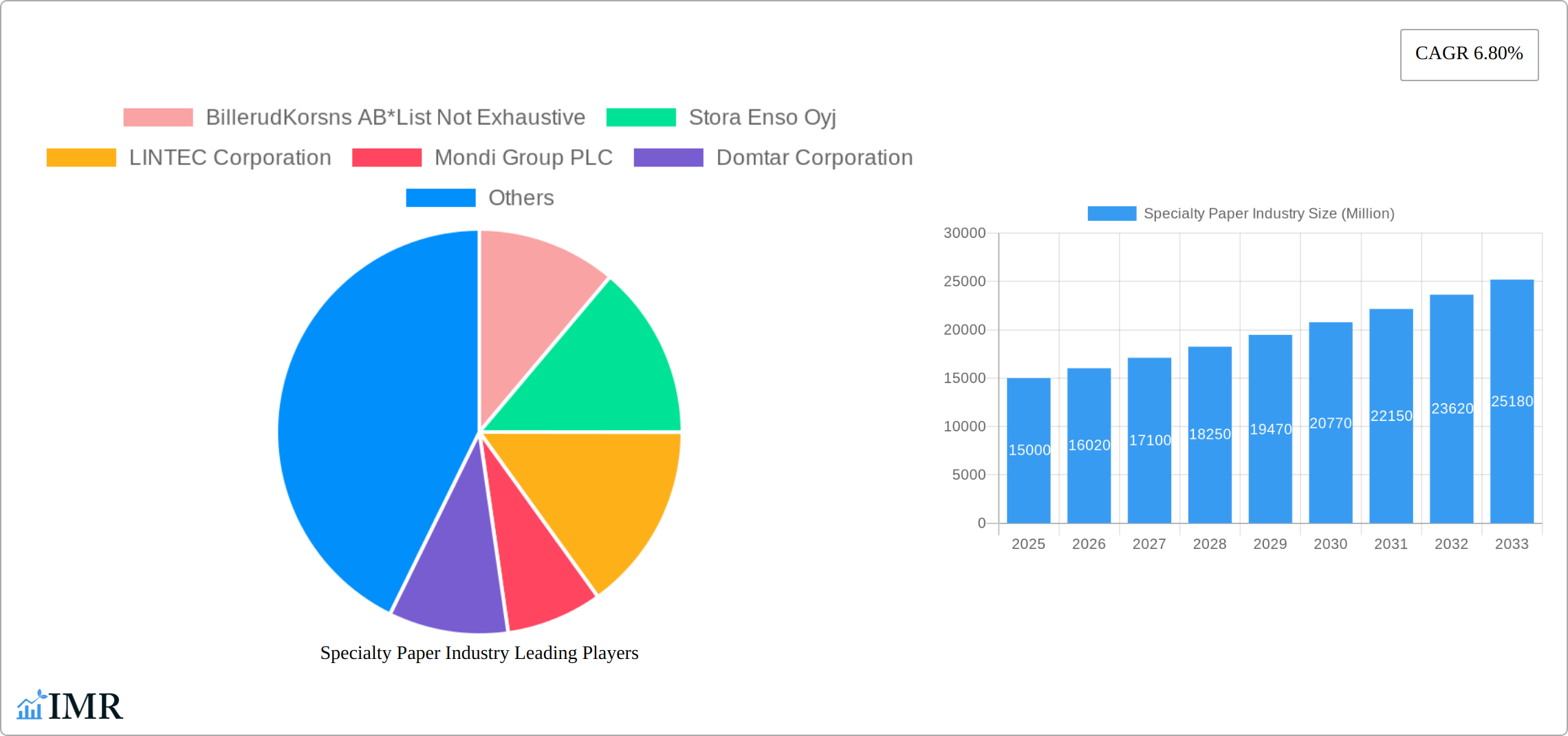

The competitive environment features both global corporations and regional entities. Leading companies like BillerudKorsnäs AB, Stora Enso Oyj, Mondi Group PLC, and Sappi Limited are actively pursuing innovation and strategic growth to strengthen their market standing. While digitalization poses a challenge in sectors like print media, this is counterbalanced by growth in e-commerce and sustainable packaging. Future market dynamics will be shaped by sustainability initiatives, technological advancements in paper production, and a growing consumer preference for eco-conscious products. Government policies supporting sustainable packaging practices will also be critical in defining the market's trajectory.

Specialty Paper Industry Company Market Share

Specialty Paper Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the global specialty paper industry, encompassing market dynamics, growth trends, competitive landscape, and future outlook. The study period covers 2019-2033, with 2025 as the base year and a forecast period of 2025-2033. The report is essential for industry professionals, investors, and strategic decision-makers seeking to understand and capitalize on opportunities within this dynamic sector. Market values are presented in millions of units.

Specialty Paper Industry Market Dynamics & Structure

The specialty paper market is a dynamic and evolving landscape, characterized by a moderate level of concentration. Leading global manufacturers such as BillerudKorsnäs AB, Stora Enso Oyj, Mondi Group PLC, and Sappi Limited are key influencers, collectively holding a substantial portion of the market share (xx%). A pivotal driver of this market is continuous technological innovation, with a strong emphasis on developing sustainable and high-performance functional paper solutions. This innovation is increasingly being shaped by evolving regulatory frameworks that prioritize environmental sustainability and circular economy principles. However, the industry faces significant competitive pressures from alternative packaging materials, notably plastics, which necessitate ongoing adaptation and differentiation.

The market is intricately segmented to cater to diverse needs, broadly categorized by end-user industry, including Packaging & Labelling, Food Service, Printing & Publication, Building & Construction, and Other specialized applications. Further segmentation occurs based on paper type, encompassing Kraft Paper, Container Board/Paper Board, Label Paper, Silicon-based Paper, and a range of other specialized grades. Mergers and acquisitions (M&A) have been a notable, albeit moderate, feature of the sector in recent years (xx deals in the last 5 years). These strategic moves are largely driven by consolidation efforts, the pursuit of economies of scale, and expansion into rapidly growing, high-demand segments of the market.

- Market Concentration: Moderately concentrated, with top players holding approximately xx% of the market share.

- Technological Innovation: A significant focus is placed on developing sustainable materials, enhancing functional properties, and improving manufacturing processes for eco-friendly paper solutions.

- Regulatory Framework: An increasing emphasis on stringent environmental regulations and policies supporting the transition to a circular economy is shaping product development and market strategies.

- Competitive Substitutes: The persistent challenge posed by plastic packaging materials necessitates continuous innovation in performance and sustainability to maintain market relevance.

- End-User Demographics: Shifting consumer preferences towards eco-friendly, sustainable, and ethically sourced products are profoundly influencing demand patterns across various end-user segments.

- M&A Trends: Moderate M&A activity is observed, primarily driven by industry consolidation, strategic partnerships, and the acquisition of innovative technologies or market access.

Specialty Paper Industry Growth Trends & Insights

The global specialty paper market has demonstrated a trajectory of steady growth during the historical period (2019-2024), evidenced by a Compound Annual Growth Rate (CAGR) of xx%. This robust expansion is predominantly fueled by the escalating demand from the packaging and labeling sectors. This surge is intricately linked to the proliferation of e-commerce, which has amplified the need for efficient and attractive packaging, coupled with a growing consumer inclination towards sustainable packaging solutions. Technological advancements are playing a crucial role in this growth, with innovations in improved barrier properties for enhanced product protection and the development of advanced functional coatings contributing to market expansion.

While the growth trajectory is positive, the market is susceptible to external factors. Fluctuations in raw material prices and periods of economic downturn can introduce volatility and impact overall growth rates. Looking ahead, the adoption of specialized paper types, such as silicon-based papers crucial for applications in the electronics industry, is projected to witness significant expansion, with an estimated CAGR of xx% during the forecast period. The market penetration of sustainable packaging solutions is anticipated to reach an impressive xx% by 2033, underscoring the pivotal role of environmental consciousness. This trend is further amplified by pervasive consumer behavior shifts towards environmentally responsible and eco-friendly products, directly boosting demand for specialty papers that align with these values.

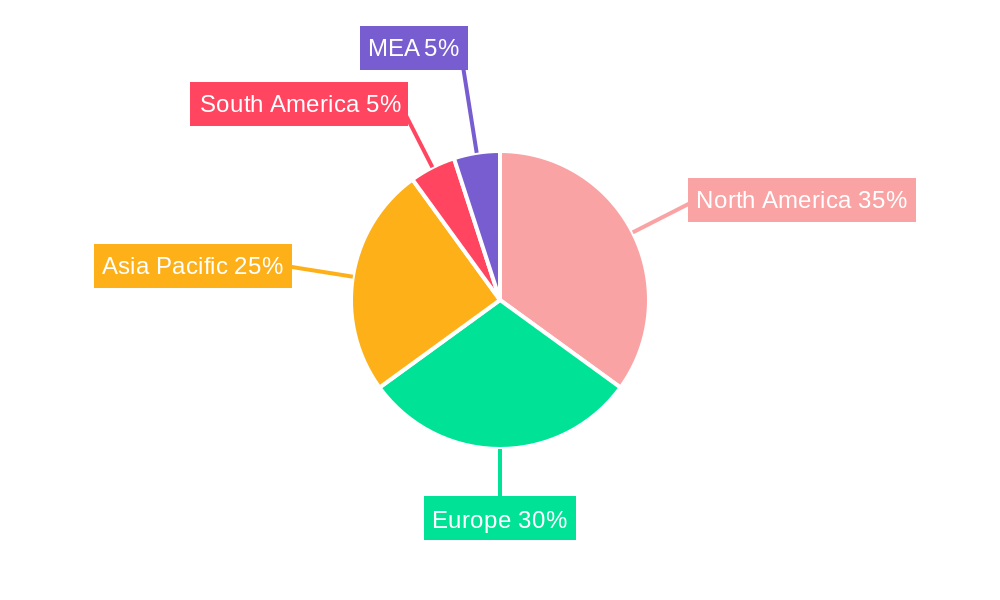

Dominant Regions, Countries, or Segments in Specialty Paper Industry

North America and Europe currently dominate the specialty paper market, accounting for xx% of global revenue. However, Asia-Pacific is exhibiting the highest growth rate, fueled by rapid economic expansion and increasing industrialization. Within end-user segments, Packaging & Labelling holds the largest market share (xx%), driven by robust demand from the food and beverage industries. Similarly, Container Board/Paper Board represents a substantial segment by type, driven by its wide use in packaging.

- Key Drivers (North America & Europe): Established infrastructure, high consumer spending, and stringent environmental regulations.

- Key Drivers (Asia-Pacific): Rapid economic growth, industrialization, and increasing demand for packaging materials.

- Packaging & Labeling Segment: Largest market share due to high demand from food and beverage sectors.

- Container Board/Paper Board: Significant market share due to widespread use in packaging.

Specialty Paper Industry Product Landscape

Specialty paper products are continuously evolving to meet specific performance requirements. Innovations include improved barrier properties for food packaging, enhanced printability for label applications, and functional coatings for specialized uses. Key selling propositions often include sustainability, biodegradability, and enhanced performance characteristics. Technological advancements are focusing on reducing environmental impact and improving efficiency in manufacturing processes.

Key Drivers, Barriers & Challenges in Specialty Paper Industry

Key Drivers: Increasing demand for sustainable packaging solutions, technological advancements in functional paper, and government regulations promoting sustainable alternatives to plastics. For example, the EU's single-use plastics directive is driving demand for paper-based alternatives.

Key Challenges: Fluctuations in raw material prices (pulp), intense competition from alternative packaging materials (plastics), and supply chain disruptions (especially in the post-pandemic era) which have impacted supply by xx% in 2022. Environmental regulations, while driving innovation, also increase production costs.

Emerging Opportunities in Specialty Paper Industry

The specialty paper industry is ripe with emerging opportunities. The relentless expansion of e-commerce continues to drive substantial demand for innovative and efficient packaging solutions that ensure product integrity and enhance unboxing experiences. A significant and growing opportunity lies in the development and widespread adoption of sustainable and biodegradable packaging solutions, aligning with global environmental imperatives and consumer preferences. Furthermore, the increasing application of specialty papers in niche and high-value sectors, such as medical supplies for advanced wound care and diagnostic tools, and in the electronics industry for components like insulation and flexible substrates, presents substantial growth potential. Moreover, untapped markets in developing economies offer significant untapped growth potential for specialty paper manufacturers willing to adapt their offerings to local needs and economic conditions.

Growth Accelerators in the Specialty Paper Industry

Long-term growth will be driven by technological breakthroughs in paper manufacturing, leading to more sustainable and cost-effective production methods. Strategic partnerships to expand distribution networks and access to new markets will play a critical role. Furthermore, successful marketing campaigns emphasizing sustainability and the superior properties of specialty paper over alternative materials will drive adoption.

Key Players Shaping the Specialty Paper Industry Market

- BillerudKorsnäs AB

- Stora Enso Oyj

- LINTEC Corporation

- Mondi Group PLC

- Domtar Corporation

- Sappi Limited

- Nippon Paper Industries Co Ltd

- ITC Limited

- Twin Rivers Paper Company

- Nordic Paper AS

Notable Milestones in Specialty Paper Industry Sector

- November 2022: Sappi North America invested USD 418 million in paper machine rebuilds, increasing capacity for sustainable board products.

- September 2022: Sappi Europe invested a double-digit million-euro sum to expand wet-strength label paper production.

In-Depth Specialty Paper Industry Market Outlook

The specialty paper industry is strategically positioned for sustained and robust growth in the coming years. This positive outlook is underpinned by two primary, interconnected forces: a global escalation in sustainability concerns and continuous technological advancements. Companies that strategically invest in cutting-edge research and development (R&D) will be at the forefront of innovation, enabling them to create next-generation paper products with enhanced functionalities and reduced environmental impact. Furthermore, proactive expansion into new geographical markets and emerging applications will be crucial for capturing market share and diversifying revenue streams.

The unwavering focus on developing sustainable and functional papers will unlock significant opportunities for forward-thinking companies. Those that embrace innovation, adapt swiftly to the evolving needs of discerning consumers, and proactively respond to increasingly stringent regulatory demands will be best placed to thrive. Projections indicate that the global specialty paper market is set to reach an impressive xx Million units by 2033, signifying a substantial expansion and a testament to the industry's resilience and adaptability.

Specialty Paper Industry Segmentation

-

1. Type

- 1.1. Kraft Paper

- 1.2. Container Board/Paper Board

- 1.3. Label Paper

- 1.4. Silicon-based Paper

- 1.5. Others

-

2. End-user Industry

- 2.1. Packaging & Labelling

- 2.2. Food Service

- 2.3. Printing & Publication

- 2.4. Building & Construction

- 2.5. Other En

Specialty Paper Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Mexico

- 4.3. Rest of Latin America

- 5. Middle East and Africa

Specialty Paper Industry Regional Market Share

Geographic Coverage of Specialty Paper Industry

Specialty Paper Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Kraft Paper

- 5.1.2. Container Board/Paper Board

- 5.1.3. Label Paper

- 5.1.4. Silicon-based Paper

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Packaging & Labelling

- 5.2.2. Food Service

- 5.2.3. Printing & Publication

- 5.2.4. Building & Construction

- 5.2.5. Other En

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Specialty Paper Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Kraft Paper

- 6.1.2. Container Board/Paper Board

- 6.1.3. Label Paper

- 6.1.4. Silicon-based Paper

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Packaging & Labelling

- 6.2.2. Food Service

- 6.2.3. Printing & Publication

- 6.2.4. Building & Construction

- 6.2.5. Other En

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Specialty Paper Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Kraft Paper

- 7.1.2. Container Board/Paper Board

- 7.1.3. Label Paper

- 7.1.4. Silicon-based Paper

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Packaging & Labelling

- 7.2.2. Food Service

- 7.2.3. Printing & Publication

- 7.2.4. Building & Construction

- 7.2.5. Other En

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Specialty Paper Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Kraft Paper

- 8.1.2. Container Board/Paper Board

- 8.1.3. Label Paper

- 8.1.4. Silicon-based Paper

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Packaging & Labelling

- 8.2.2. Food Service

- 8.2.3. Printing & Publication

- 8.2.4. Building & Construction

- 8.2.5. Other En

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Specialty Paper Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Kraft Paper

- 9.1.2. Container Board/Paper Board

- 9.1.3. Label Paper

- 9.1.4. Silicon-based Paper

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Packaging & Labelling

- 9.2.2. Food Service

- 9.2.3. Printing & Publication

- 9.2.4. Building & Construction

- 9.2.5. Other En

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Latin America Specialty Paper Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Kraft Paper

- 10.1.2. Container Board/Paper Board

- 10.1.3. Label Paper

- 10.1.4. Silicon-based Paper

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Packaging & Labelling

- 10.2.2. Food Service

- 10.2.3. Printing & Publication

- 10.2.4. Building & Construction

- 10.2.5. Other En

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa Specialty Paper Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Kraft Paper

- 11.1.2. Container Board/Paper Board

- 11.1.3. Label Paper

- 11.1.4. Silicon-based Paper

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Packaging & Labelling

- 11.2.2. Food Service

- 11.2.3. Printing & Publication

- 11.2.4. Building & Construction

- 11.2.5. Other En

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 BillerudKorsns AB*List Not Exhaustive

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Stora Enso Oyj

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 LINTEC Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Mondi Group PLC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Domtar Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Sappi Limited

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Nippon Paper Industries Co Ltd

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 ITC Limited

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Twin Rivers Paper Company

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Nordic Paper AS

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 BillerudKorsns AB*List Not Exhaustive

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Specialty Paper Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Specialty Paper Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Specialty Paper Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Specialty Paper Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 5: North America Specialty Paper Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: North America Specialty Paper Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Specialty Paper Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Specialty Paper Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: Europe Specialty Paper Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: Europe Specialty Paper Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 11: Europe Specialty Paper Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: Europe Specialty Paper Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Specialty Paper Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Specialty Paper Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Asia Pacific Specialty Paper Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Asia Pacific Specialty Paper Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 17: Asia Pacific Specialty Paper Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Asia Pacific Specialty Paper Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Specialty Paper Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Specialty Paper Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: Latin America Specialty Paper Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Latin America Specialty Paper Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 23: Latin America Specialty Paper Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Latin America Specialty Paper Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Latin America Specialty Paper Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Specialty Paper Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: Middle East and Africa Specialty Paper Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Middle East and Africa Specialty Paper Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 29: Middle East and Africa Specialty Paper Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 30: Middle East and Africa Specialty Paper Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Specialty Paper Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Specialty Paper Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Specialty Paper Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Specialty Paper Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Specialty Paper Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global Specialty Paper Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Specialty Paper Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Specialty Paper Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Specialty Paper Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Global Specialty Paper Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Global Specialty Paper Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 11: Global Specialty Paper Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Germany Specialty Paper Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: United Kingdom Specialty Paper Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: France Specialty Paper Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of Europe Specialty Paper Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Specialty Paper Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 17: Global Specialty Paper Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 18: Global Specialty Paper Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: China Specialty Paper Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: India Specialty Paper Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Japan Specialty Paper Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Rest of Asia Pacific Specialty Paper Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Global Specialty Paper Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 24: Global Specialty Paper Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 25: Global Specialty Paper Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 26: Brazil Specialty Paper Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Mexico Specialty Paper Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Rest of Latin America Specialty Paper Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Global Specialty Paper Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Specialty Paper Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 31: Global Specialty Paper Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Specialty Paper Industry?

The projected CAGR is approximately 5.1%.

2. Which companies are prominent players in the Specialty Paper Industry?

Key companies in the market include BillerudKorsns AB*List Not Exhaustive, Stora Enso Oyj, LINTEC Corporation, Mondi Group PLC, Domtar Corporation, Sappi Limited, Nippon Paper Industries Co Ltd, ITC Limited, Twin Rivers Paper Company, Nordic Paper AS.

3. What are the main segments of the Specialty Paper Industry?

The market segments include Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 18 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Trend of Online Food Ordering; Changing Consumer Preference to Adopt Sustainable Decorative Lamination.

6. What are the notable trends driving market growth?

Food Service Industry is Expected to hold Significant Share.

7. Are there any restraints impacting market growth?

Greenhouse Gas Emission Due To Dairy Activities Leading To Legislative Issues.

8. Can you provide examples of recent developments in the market?

November 2022: Sappi North America announced the investment of USD 418 million in paper machine rebuilds at its Somerset Mill in Skowhegan. With this investment, the company is focusing on increasing Paper Machine No. 2's capacity to produce solid bleached sulfate board products, a sustainable alternative to plastic packaging. This move of the company indicates its long-term Thrive25 strategy, which focuses on growing its portfolio in packaging and speciality papers, pulp, and biomaterials.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Specialty Paper Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Specialty Paper Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Specialty Paper Industry?

To stay informed about further developments, trends, and reports in the Specialty Paper Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence