Key Insights

The global Meat, Poultry & Seafood Packaging market is projected for substantial growth, reaching a market size of $15.62 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 5.2%. This expansion is driven by increasing consumer demand for convenient, processed, and ready-to-eat food products, coupled with a growing emphasis on food safety and extended shelf-life. Innovations in sustainable packaging solutions are also a key factor, balancing product integrity with environmental responsibility. Rigid packaging, especially plastics and aluminum, remains dominant due to its protective attributes. However, flexible packaging, including pouches and films, is gaining traction for its cost-effectiveness, light weight, and reduced material consumption, aligning with sustainability goals.

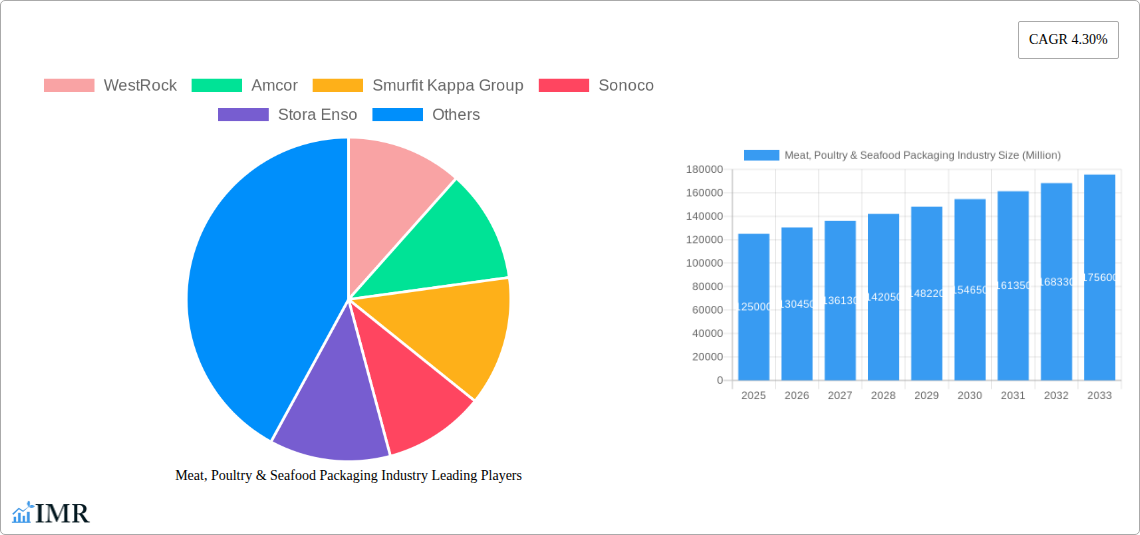

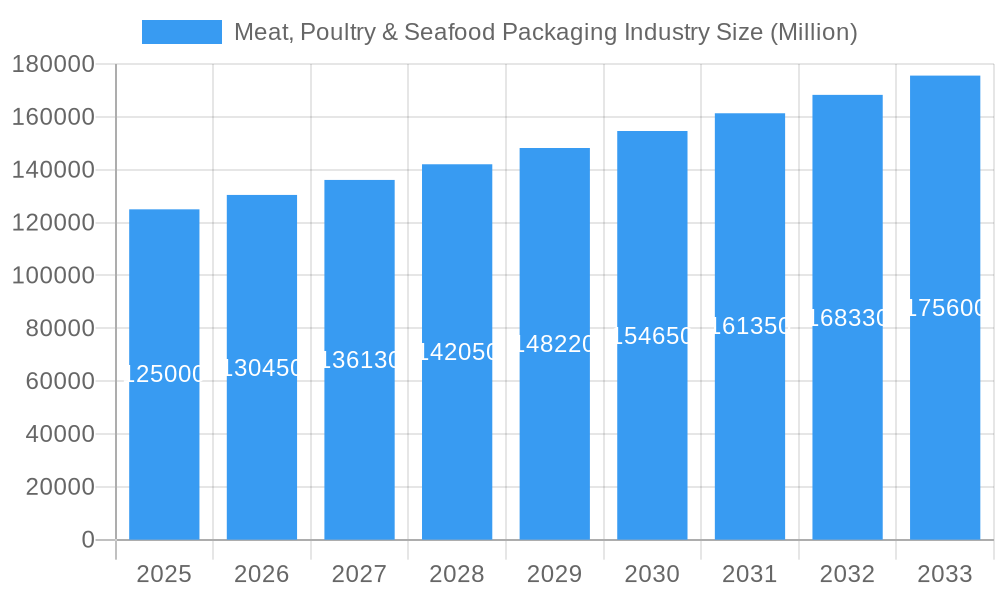

Meat, Poultry & Seafood Packaging Industry Market Size (In Billion)

Key growth drivers include a rising global population and its demand for protein sources, supported by the expansion of organized retail and e-commerce. Emerging economies present significant opportunities due to a growing middle class and increased disposable income. Conversely, stringent regulations on plastic waste and fluctuating raw material prices pose challenges. Nevertheless, advancements in material science and packaging technology, focusing on biodegradable and recyclable materials, are expected to overcome these restraints. The market is competitive, with key players like WestRock, Amcor, and Smurfit Kappa Group investing in R&D for next-generation packaging solutions for the meat, poultry, and seafood sectors.

Meat, Poultry & Seafood Packaging Industry Company Market Share

This report offers a comprehensive analysis of the global Meat, Poultry & Seafood Packaging industry, covering market dynamics, growth trends, and future outlook from 2025 to 2033. With a base year of 2025, it provides in-depth insights into market segmentation, leading players, and emerging trends in food packaging solutions, making it an essential resource for stakeholders in the fresh, frozen, and processed food packaging market.

Meat, Poultry & Seafood Packaging Industry Market Dynamics & Structure

The Meat, Poultry & Seafood Packaging market exhibits a moderately concentrated structure, with key players like WestRock, Amcor, Smurfit Kappa Group, and Sonoco holding significant market shares. Technological innovation is a primary driver, fueled by the demand for enhanced shelf-life, food safety, and sustainable packaging solutions. The regulatory framework, particularly concerning food contact materials and recyclability, plays a crucial role in shaping product development and market entry strategies. Competitive product substitutes, such as alternative protein sources and evolving retail formats, influence packaging material choices. End-user demographics, with a growing preference for convenience and ready-to-eat options, are pushing innovation in packaging design and functionality. Mergers and acquisitions (M&A) remain a significant trend, with companies consolidating to expand their geographical reach and product portfolios. For instance, the flexible packaging market within this sector has seen strategic acquisitions aimed at bolstering capabilities in sustainable material development. Barriers to innovation include the high cost of R&D for advanced materials and the stringent testing required for food-grade compliance.

- Market Concentration: Moderately concentrated with a few dominant players.

- Technological Innovation Drivers: Extended shelf-life solutions, improved barrier properties, antimicrobial packaging, and lightweighting.

- Regulatory Frameworks: Stringent regulations for food safety, material traceability, and recyclability mandates (e.g., single-use plastic bans).

- Competitive Product Substitutes: Plant-based meat alternatives, alternative protein sources, and changes in consumer dietary habits.

- End-User Demographics: Growing demand for convenience, online grocery shopping, and increased awareness of food sustainability.

- M&A Trends: Strategic acquisitions and partnerships focused on sustainable materials, expanded capacity, and market penetration.

- Innovation Barriers: High R&D costs, complex regulatory approvals, and the need for robust supply chain integration for new materials.

Meat, Poultry & Seafood Packaging Industry Growth Trends & Insights

The Meat, Poultry & Seafood Packaging market is projected for robust growth, driven by an escalating global demand for protein-rich foods and evolving consumer preferences. The market size is expected to expand from approximately $45,000 million units in 2019 to an estimated $68,000 million units by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 3.5%. The adoption rate of advanced packaging technologies, such as Modified Atmosphere Packaging (MAP) and Active Packaging, is steadily increasing, particularly for fresh and frozen products, to extend shelf-life and reduce food waste. Technological disruptions, including the development of biodegradable and compostable packaging materials derived from bio-based polymers, are gaining traction. Consumer behavior shifts, such as a growing preference for transparency in sourcing and ingredients, are prompting manufacturers to adopt innovative labeling and traceability solutions within their food cans and plastic containers. The rise of e-commerce for groceries also necessitates specialized packaging that ensures product integrity during transit, boosting demand for durable and protective solutions. The rigid packaging segment, especially plastic containers and board containers, continues to hold a significant share due to its protective qualities, while the flexible packaging segment is witnessing rapid innovation in sustainable materials.

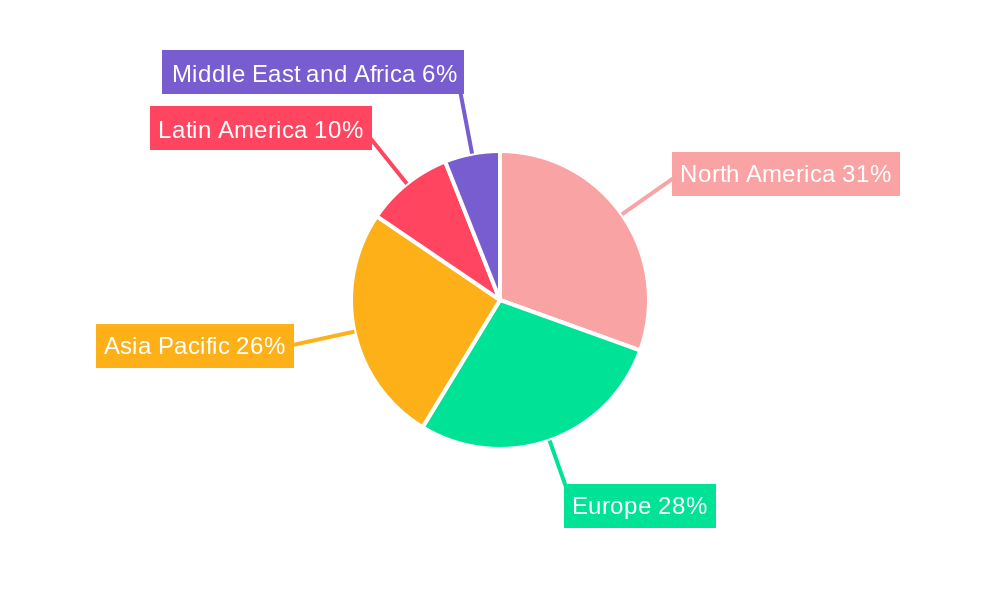

Dominant Regions, Countries, or Segments in Meat, Poultry & Seafood Packaging Industry

North America and Europe currently dominate the Meat, Poultry & Seafood Packaging market, driven by high disposable incomes, established retail infrastructure, and a strong consumer preference for pre-packaged meat, poultry, and seafood. Within these regions, the flexible packaging segment, particularly for pre-made bags and coated films, is a significant growth driver, catering to the demand for convenience and extended shelf-life. The fresh and frozen products application segment is the largest, accounting for over 60% of the market share, due to the widespread consumption of these protein sources. Asia-Pacific is the fastest-growing region, fueled by rapid urbanization, a burgeoning middle class, and increasing adoption of Western dietary habits. Countries like China and India are witnessing substantial growth in demand for packaged meat and poultry.

In terms of material types, Polypropylene (PP) and Polyester (PET) are widely used for their durability, barrier properties, and suitability for various packaging formats, including plastic containers and coated films. The growing emphasis on sustainability is driving innovation in aluminium and other recyclable materials, along with the development of board containers with advanced barrier coatings. The read-to-eat products segment is also experiencing considerable growth, necessitating specialized packaging that maintains food quality and safety while offering on-the-go convenience.

- Dominant Region: North America, Europe.

- Fastest Growing Region: Asia-Pacific.

- Dominant Packaging Type: Flexible Packaging.

- Key Product Types Driving Growth: Pre-made Bags, Food Cans, Plastic Containers.

- Dominant Material Types: Polypropylene (PP), Polyester (PET).

- Dominant Application: Fresh and Frozen Products.

- Emerging Application: Read-to-eat Products.

- Key Drivers of Regional Dominance: High disposable income, advanced retail infrastructure, consumer awareness of food safety and convenience.

- Growth Potential in Asia-Pacific: Rapid urbanization, rising middle class, increasing protein consumption, evolving retail landscape.

Meat, Poultry & Seafood Packaging Industry Product Landscape

The Meat, Poultry & Seafood Packaging industry is characterized by a dynamic product landscape focused on enhanced food safety, extended shelf-life, and consumer convenience. Innovations range from advanced barrier films that prevent oxygen and moisture ingress, thereby preserving product freshness, to retort pouches capable of withstanding high temperatures for sterilization, offering extended shelf-life for processed products. Aluminium foil containers are widely adopted for their excellent barrier properties and heat conductivity, ideal for baking and ready-meal applications. The development of coated films incorporating antimicrobial agents and oxygen scavengers further elevates product protection. The trend towards sustainable packaging is driving the adoption of recycled content in plastic containers and the development of monomaterial solutions for improved recyclability. Unique selling propositions include tamper-evident seals, easy-open features, and microwaveable capabilities, all contributing to an improved consumer experience.

Key Drivers, Barriers & Challenges in Meat, Poultry & Seafood Packaging Industry

Key Drivers:

- Growing Global Protein Demand: Increasing population and rising disposable incomes worldwide drive higher consumption of meat, poultry, and seafood.

- Food Safety and Shelf-Life Extension: Consumers and retailers demand packaging that ensures product safety and extends shelf-life to reduce spoilage and waste.

- Convenience and Ready-to-Eat Trends: The growing preference for convenient, pre-portioned, and ready-to-eat meals fuels innovation in packaging solutions.

- E-commerce Growth: The rise of online grocery shopping necessitates robust packaging to protect products during transit and maintain freshness.

- Sustainability Initiatives: Increasing consumer and regulatory pressure for eco-friendly packaging solutions, including recyclable, compostable, and bio-based materials.

Barriers & Challenges:

- Regulatory Hurdles: Stringent regulations regarding food contact materials, recyclability, and labeling can slow down product development and market entry.

- Cost of Sustainable Materials: Advanced sustainable packaging materials often come with a higher price point, posing a challenge for widespread adoption.

- Supply Chain Disruptions: Global supply chain volatility, including raw material shortages and logistics challenges, can impact production and costs.

- Consumer Education: Educating consumers about the proper disposal and recycling of complex packaging structures is crucial for achieving sustainability goals.

- Performance Trade-offs: Balancing sustainability with the functional requirements of packaging, such as barrier properties and durability, can be challenging.

Emerging Opportunities in Meat, Poultry & Seafood Packaging Industry

Emerging opportunities lie in the development of advanced flexible packaging solutions with enhanced barrier properties and increased recycled content, catering to the demand for sustainable yet high-performance packaging. The growth of the read-to-eat products segment presents significant potential for innovative, portion-controlled, and microwaveable packaging. Untapped markets in developing economies, with their rapidly expanding middle class and increasing adoption of packaged foods, offer substantial growth prospects. Furthermore, smart packaging solutions incorporating QR codes for traceability, authentication, and consumer engagement are poised to gain traction. The development of compostable and biodegradable alternatives to traditional plastics, especially for single-use applications, represents a key area for future innovation and market penetration.

Growth Accelerators in the Meat, Poultry & Seafood Packaging Industry Industry

Growth in the Meat, Poultry & Seafood Packaging industry is significantly accelerated by ongoing technological breakthroughs in material science, leading to the development of more sustainable and high-performance packaging options. Strategic partnerships between packaging manufacturers and food producers are crucial for co-developing tailored solutions that address specific product needs and market demands. Market expansion strategies, particularly in emerging economies where protein consumption is rising, represent a major catalyst for long-term growth. The increasing focus on reducing food waste through improved packaging functionality also acts as a strong growth accelerator. Investments in R&D for advanced barrier technologies, such as active and intelligent packaging, will further propel the industry forward.

Key Players Shaping the Meat, Poultry & Seafood Packaging Industry Market

- WestRock

- Amcor

- Smurfit Kappa Group

- Sonoco

- Stora Enso

- Mondi Group

- Can-Pack SA

- Crown Holdings

- Berry Global

- DS Smith

- Sealed Air

Notable Milestones in Meat, Poultry & Seafood Packaging Industry Sector

- December 2022: Amcor announced the opening of its new state-of-the-art manufacturing plant in Huizhou, China. With an investment of over USD 100 million, the 590,000 sq ft factory is the largest flexible packaging plant in China by production capacity, substantially enhancing Amcor's capabilities to fulfill rising client demand throughout Asia-Pacific. The facility has China's first automated packaging production line, resulting in double-digit decreases in production cycle time, together with high-speed printing presses, laminators, and bag-making equipment.

- October 2022: Berry Global announced Printpack, leveraging its independent strengths in film manufacturing and conversion to create packaging solutions that support increased customer demand for more sustainable packaging. The companies introduced the Preserve PE PCR recyclable polyethylene (PE) pouch. It is How2Recycle pre-qualified and contains 30% FDA-compliant post-consumer recycled resin (PCR) content with a lower carbon footprint than equivalent products made from virgin plastic while maintaining package performance.

In-Depth Meat, Poultry & Seafood Packaging Industry Market Outlook

The future outlook for the Meat, Poultry & Seafood Packaging industry is highly promising, driven by a confluence of favorable market dynamics and evolving consumer expectations. Growth accelerators, including the increasing demand for convenience, the imperative to reduce food waste, and a global push towards sustainable packaging solutions, will continue to shape market trends. Strategic collaborations and technological innovations in areas like biodegradable materials and smart packaging will unlock new avenues for market penetration. The expansion of the processed products and read-to-eat products segments, particularly in emerging economies, presents substantial opportunities. Stakeholders who can effectively navigate regulatory landscapes, invest in sustainable material development, and adapt to shifting consumer preferences will be well-positioned for sustained success in this dynamic market.

Meat, Poultry & Seafood Packaging Industry Segmentation

-

1. Packaging Type

- 1.1. Rigid Packaging

- 1.2. Flexible Packaging

-

2. Product Type

-

2.1. Containers

- 2.1.1. Aluminium Foil Container

- 2.1.2. Plastic Container

- 2.1.3. Board Container

- 2.2. Pre-made Bags

- 2.3. Food Cans

- 2.4. Coated Films

- 2.5. Other Product Types

-

2.1. Containers

-

3. Material Type

- 3.1. Polypropylene (PP)

- 3.2. Polystrene (PS)

- 3.3. Polyester (PET)

- 3.4. Thermoform

- 3.5. Aluminium

- 3.6. Other Material Types

-

4. Application

- 4.1. Fresh and Frozen Products

- 4.2. Processed Products

- 4.3. Read-to-eat Products

Meat, Poultry & Seafood Packaging Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Meat, Poultry & Seafood Packaging Industry Regional Market Share

Geographic Coverage of Meat, Poultry & Seafood Packaging Industry

Meat, Poultry & Seafood Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Packaging Type

- 5.1.1. Rigid Packaging

- 5.1.2. Flexible Packaging

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Containers

- 5.2.1.1. Aluminium Foil Container

- 5.2.1.2. Plastic Container

- 5.2.1.3. Board Container

- 5.2.2. Pre-made Bags

- 5.2.3. Food Cans

- 5.2.4. Coated Films

- 5.2.5. Other Product Types

- 5.2.1. Containers

- 5.3. Market Analysis, Insights and Forecast - by Material Type

- 5.3.1. Polypropylene (PP)

- 5.3.2. Polystrene (PS)

- 5.3.3. Polyester (PET)

- 5.3.4. Thermoform

- 5.3.5. Aluminium

- 5.3.6. Other Material Types

- 5.4. Market Analysis, Insights and Forecast - by Application

- 5.4.1. Fresh and Frozen Products

- 5.4.2. Processed Products

- 5.4.3. Read-to-eat Products

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. Latin America

- 5.5.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Packaging Type

- 6. Global Meat, Poultry & Seafood Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Packaging Type

- 6.1.1. Rigid Packaging

- 6.1.2. Flexible Packaging

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Containers

- 6.2.1.1. Aluminium Foil Container

- 6.2.1.2. Plastic Container

- 6.2.1.3. Board Container

- 6.2.2. Pre-made Bags

- 6.2.3. Food Cans

- 6.2.4. Coated Films

- 6.2.5. Other Product Types

- 6.2.1. Containers

- 6.3. Market Analysis, Insights and Forecast - by Material Type

- 6.3.1. Polypropylene (PP)

- 6.3.2. Polystrene (PS)

- 6.3.3. Polyester (PET)

- 6.3.4. Thermoform

- 6.3.5. Aluminium

- 6.3.6. Other Material Types

- 6.4. Market Analysis, Insights and Forecast - by Application

- 6.4.1. Fresh and Frozen Products

- 6.4.2. Processed Products

- 6.4.3. Read-to-eat Products

- 6.1. Market Analysis, Insights and Forecast - by Packaging Type

- 7. North America Meat, Poultry & Seafood Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Packaging Type

- 7.1.1. Rigid Packaging

- 7.1.2. Flexible Packaging

- 7.2. Market Analysis, Insights and Forecast - by Product Type

- 7.2.1. Containers

- 7.2.1.1. Aluminium Foil Container

- 7.2.1.2. Plastic Container

- 7.2.1.3. Board Container

- 7.2.2. Pre-made Bags

- 7.2.3. Food Cans

- 7.2.4. Coated Films

- 7.2.5. Other Product Types

- 7.2.1. Containers

- 7.3. Market Analysis, Insights and Forecast - by Material Type

- 7.3.1. Polypropylene (PP)

- 7.3.2. Polystrene (PS)

- 7.3.3. Polyester (PET)

- 7.3.4. Thermoform

- 7.3.5. Aluminium

- 7.3.6. Other Material Types

- 7.4. Market Analysis, Insights and Forecast - by Application

- 7.4.1. Fresh and Frozen Products

- 7.4.2. Processed Products

- 7.4.3. Read-to-eat Products

- 7.1. Market Analysis, Insights and Forecast - by Packaging Type

- 8. Europe Meat, Poultry & Seafood Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Packaging Type

- 8.1.1. Rigid Packaging

- 8.1.2. Flexible Packaging

- 8.2. Market Analysis, Insights and Forecast - by Product Type

- 8.2.1. Containers

- 8.2.1.1. Aluminium Foil Container

- 8.2.1.2. Plastic Container

- 8.2.1.3. Board Container

- 8.2.2. Pre-made Bags

- 8.2.3. Food Cans

- 8.2.4. Coated Films

- 8.2.5. Other Product Types

- 8.2.1. Containers

- 8.3. Market Analysis, Insights and Forecast - by Material Type

- 8.3.1. Polypropylene (PP)

- 8.3.2. Polystrene (PS)

- 8.3.3. Polyester (PET)

- 8.3.4. Thermoform

- 8.3.5. Aluminium

- 8.3.6. Other Material Types

- 8.4. Market Analysis, Insights and Forecast - by Application

- 8.4.1. Fresh and Frozen Products

- 8.4.2. Processed Products

- 8.4.3. Read-to-eat Products

- 8.1. Market Analysis, Insights and Forecast - by Packaging Type

- 9. Asia Pacific Meat, Poultry & Seafood Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Packaging Type

- 9.1.1. Rigid Packaging

- 9.1.2. Flexible Packaging

- 9.2. Market Analysis, Insights and Forecast - by Product Type

- 9.2.1. Containers

- 9.2.1.1. Aluminium Foil Container

- 9.2.1.2. Plastic Container

- 9.2.1.3. Board Container

- 9.2.2. Pre-made Bags

- 9.2.3. Food Cans

- 9.2.4. Coated Films

- 9.2.5. Other Product Types

- 9.2.1. Containers

- 9.3. Market Analysis, Insights and Forecast - by Material Type

- 9.3.1. Polypropylene (PP)

- 9.3.2. Polystrene (PS)

- 9.3.3. Polyester (PET)

- 9.3.4. Thermoform

- 9.3.5. Aluminium

- 9.3.6. Other Material Types

- 9.4. Market Analysis, Insights and Forecast - by Application

- 9.4.1. Fresh and Frozen Products

- 9.4.2. Processed Products

- 9.4.3. Read-to-eat Products

- 9.1. Market Analysis, Insights and Forecast - by Packaging Type

- 10. Latin America Meat, Poultry & Seafood Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Packaging Type

- 10.1.1. Rigid Packaging

- 10.1.2. Flexible Packaging

- 10.2. Market Analysis, Insights and Forecast - by Product Type

- 10.2.1. Containers

- 10.2.1.1. Aluminium Foil Container

- 10.2.1.2. Plastic Container

- 10.2.1.3. Board Container

- 10.2.2. Pre-made Bags

- 10.2.3. Food Cans

- 10.2.4. Coated Films

- 10.2.5. Other Product Types

- 10.2.1. Containers

- 10.3. Market Analysis, Insights and Forecast - by Material Type

- 10.3.1. Polypropylene (PP)

- 10.3.2. Polystrene (PS)

- 10.3.3. Polyester (PET)

- 10.3.4. Thermoform

- 10.3.5. Aluminium

- 10.3.6. Other Material Types

- 10.4. Market Analysis, Insights and Forecast - by Application

- 10.4.1. Fresh and Frozen Products

- 10.4.2. Processed Products

- 10.4.3. Read-to-eat Products

- 10.1. Market Analysis, Insights and Forecast - by Packaging Type

- 11. Middle East and Africa Meat, Poultry & Seafood Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Packaging Type

- 11.1.1. Rigid Packaging

- 11.1.2. Flexible Packaging

- 11.2. Market Analysis, Insights and Forecast - by Product Type

- 11.2.1. Containers

- 11.2.1.1. Aluminium Foil Container

- 11.2.1.2. Plastic Container

- 11.2.1.3. Board Container

- 11.2.2. Pre-made Bags

- 11.2.3. Food Cans

- 11.2.4. Coated Films

- 11.2.5. Other Product Types

- 11.2.1. Containers

- 11.3. Market Analysis, Insights and Forecast - by Material Type

- 11.3.1. Polypropylene (PP)

- 11.3.2. Polystrene (PS)

- 11.3.3. Polyester (PET)

- 11.3.4. Thermoform

- 11.3.5. Aluminium

- 11.3.6. Other Material Types

- 11.4. Market Analysis, Insights and Forecast - by Application

- 11.4.1. Fresh and Frozen Products

- 11.4.2. Processed Products

- 11.4.3. Read-to-eat Products

- 11.1. Market Analysis, Insights and Forecast - by Packaging Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 WestRock

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Amcor

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Smurfit Kappa Group

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Sonoco

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Stora Enso

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Mondi Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Can-Pack SA*List Not Exhaustive

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Crown Holdings

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Berry Global

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 DS Smith

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Sealed Air

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 WestRock

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Meat, Poultry & Seafood Packaging Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Packaging Type 2025 & 2033

- Figure 3: North America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Packaging Type 2025 & 2033

- Figure 4: North America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 5: North America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 7: North America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 8: North America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Application 2025 & 2033

- Figure 9: North America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: North America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 11: North America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Packaging Type 2025 & 2033

- Figure 13: Europe Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Packaging Type 2025 & 2033

- Figure 14: Europe Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 15: Europe Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: Europe Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 17: Europe Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 18: Europe Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Application 2025 & 2033

- Figure 19: Europe Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Application 2025 & 2033

- Figure 20: Europe Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Europe Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Packaging Type 2025 & 2033

- Figure 23: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Packaging Type 2025 & 2033

- Figure 24: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 25: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 26: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 27: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 28: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Application 2025 & 2033

- Figure 29: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Latin America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Packaging Type 2025 & 2033

- Figure 33: Latin America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Packaging Type 2025 & 2033

- Figure 34: Latin America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 35: Latin America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 36: Latin America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 37: Latin America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 38: Latin America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Application 2025 & 2033

- Figure 39: Latin America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Application 2025 & 2033

- Figure 40: Latin America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: Latin America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Packaging Type 2025 & 2033

- Figure 43: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Packaging Type 2025 & 2033

- Figure 44: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 45: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 46: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 47: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 48: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Application 2025 & 2033

- Figure 49: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Application 2025 & 2033

- Figure 50: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 51: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Packaging Type 2020 & 2033

- Table 2: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 3: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 4: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Packaging Type 2020 & 2033

- Table 7: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 8: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 9: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 10: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Packaging Type 2020 & 2033

- Table 12: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 13: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 14: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 15: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Packaging Type 2020 & 2033

- Table 17: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 18: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 19: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Packaging Type 2020 & 2033

- Table 22: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 23: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 24: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 25: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 26: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Packaging Type 2020 & 2033

- Table 27: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 28: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 29: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 30: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Meat, Poultry & Seafood Packaging Industry?

The projected CAGR is approximately 5.2%.

2. Which companies are prominent players in the Meat, Poultry & Seafood Packaging Industry?

Key companies in the market include WestRock, Amcor, Smurfit Kappa Group, Sonoco, Stora Enso, Mondi Group, Can-Pack SA*List Not Exhaustive, Crown Holdings, Berry Global, DS Smith, Sealed Air.

3. What are the main segments of the Meat, Poultry & Seafood Packaging Industry?

The market segments include Packaging Type, Product Type, Material Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 15.62 billion as of 2022.

5. What are some drivers contributing to market growth?

Increase in Population May Increase the Demand; Government Regulations for Improved and Better Packaging Materials.

6. What are the notable trends driving market growth?

Flexible Packaging to Witness Growth.

7. Are there any restraints impacting market growth?

Contamination Due to Poor Packaging or Mishandling.

8. Can you provide examples of recent developments in the market?

December 2022 - Amcor announced the opening of its new state-of-the-art manufacturing plant in Huizhou, China. With an investment of over USD 100 million, the 590,000 sq ft factory is the largest flexible packaging plant in China by production capacity, substantially enhancing Amcor's capabilities to fulfill rising client demand throughout Asia-Pacific. The facility has China's first automated packaging production line, resulting in double-digit decreases in production cycle time, together with high-speed printing presses, laminators, and bag-making equipment.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Meat, Poultry & Seafood Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Meat, Poultry & Seafood Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Meat, Poultry & Seafood Packaging Industry?

To stay informed about further developments, trends, and reports in the Meat, Poultry & Seafood Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence