Key Insights

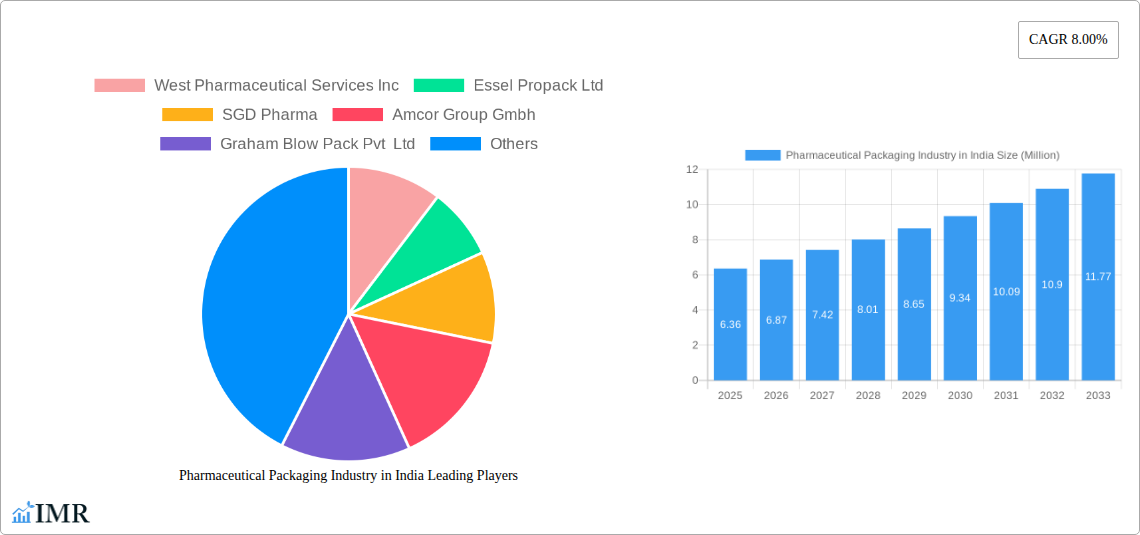

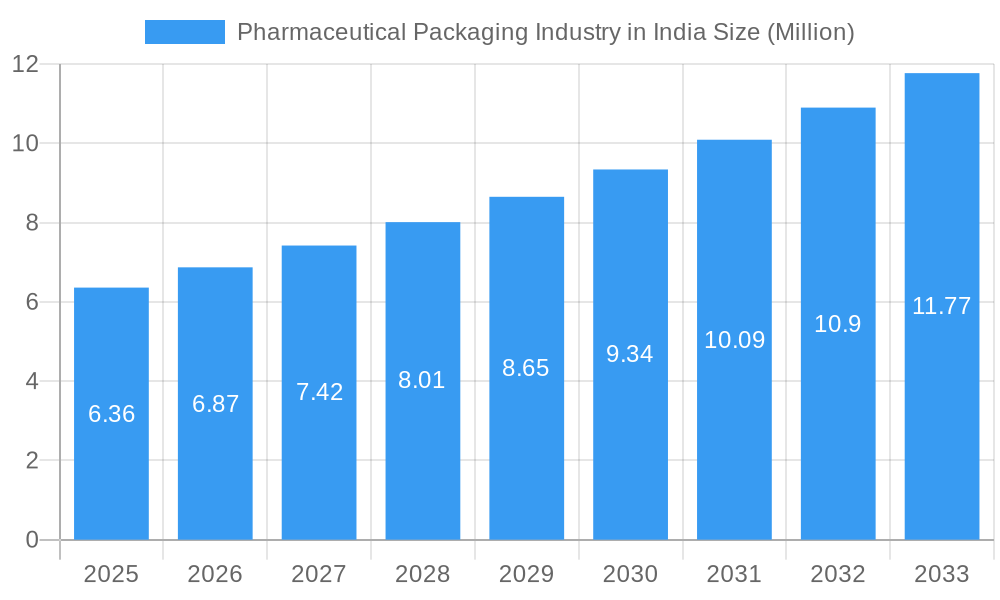

The Indian pharmaceutical packaging market is poised for substantial growth, projected to reach approximately USD 6.36 billion by 2025. This expansion is driven by a robust Compound Annual Growth Rate (CAGR) of 8.00%, indicating a dynamic and expanding industry. Several key factors are fueling this upward trajectory. The increasing prevalence of chronic diseases and the growing demand for advanced pharmaceutical formulations necessitate sophisticated and reliable packaging solutions. Furthermore, the "Make in India" initiative and government support for the pharmaceutical sector are stimulating domestic production and innovation in packaging materials and technologies. An aging global population, coupled with rising healthcare expenditure, especially in emerging economies like India, is a significant driver. Moreover, the growing emphasis on patient safety, drug efficacy, and the need for tamper-evident and child-resistant packaging are pushing manufacturers to adopt higher-quality and specialized packaging. The expanding pharmaceutical export market from India also contributes to the demand for globally compliant and high-quality packaging. Innovations in sustainable packaging materials, such as biodegradable plastics and recycled glass, are also gaining traction, aligning with global environmental concerns and regulatory shifts.

Pharmaceutical Packaging Industry in India Market Size (In Million)

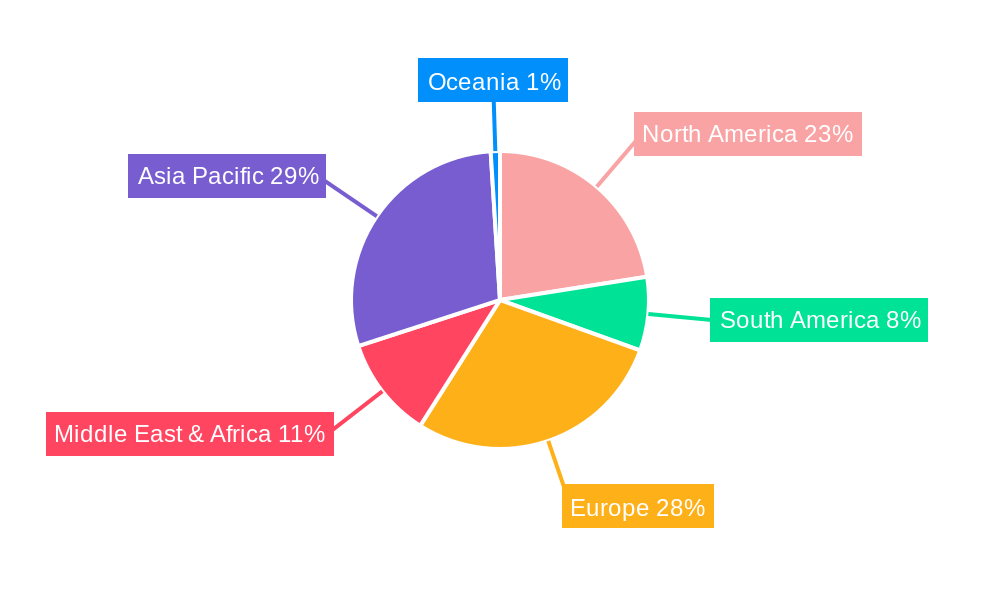

The market is segmented across various material types and product types, reflecting the diverse needs of the pharmaceutical industry. Plastic packaging, including bottles, vials, ampoules, syringes, tubes, caps, and closures, holds a dominant position due to its versatility, cost-effectiveness, and protective qualities. Glass packaging, while traditionally significant, is increasingly being adopted for specialized applications requiring inertness and superior barrier properties. Other material types and product categories like pouches, bags, and labels are also witnessing growth, driven by specific drug delivery systems and branding requirements. Key players such as West Pharmaceutical Services Inc., Essel Propack Ltd., SGD Pharma, and Amcor Group GmbH are at the forefront of innovation, investing in research and development to offer advanced packaging solutions. Regional dominance is expected in Asia Pacific, particularly in China and India, owing to their large pharmaceutical manufacturing bases and growing domestic consumption. North America and Europe, with their established pharmaceutical industries and stringent regulatory standards, also represent significant markets, driving the demand for high-quality and compliant packaging. The growth trajectory suggests continued investment in advanced manufacturing technologies and a focus on sustainability and patient-centric packaging solutions.

Pharmaceutical Packaging Industry in India Company Market Share

Comprehensive Pharmaceutical Packaging Market Analysis: India (2019-2033)

This in-depth report provides an exhaustive analysis of the Indian pharmaceutical packaging market, offering critical insights for stakeholders navigating this dynamic sector. Spanning from 2019 to 2033, with a base year of 2025 and a forecast period of 2025-2033, this report delves into market dynamics, growth trends, regional dominance, product innovations, key players, and future opportunities. We meticulously examine the parent and child market segments, providing quantitative and qualitative data crucial for strategic decision-making. Leverage this report to understand market concentration, technological advancements, regulatory landscapes, competitive forces, and evolving consumer needs within India's burgeoning pharmaceutical packaging industry.

Pharmaceutical Packaging Industry in India Market Dynamics & Structure

The Indian pharmaceutical packaging market is characterized by a moderate level of concentration, with a mix of large multinational corporations and robust domestic players vying for market share. Technological innovation is a key driver, fueled by the increasing demand for advanced, patient-centric packaging solutions that enhance drug efficacy and safety. Regulatory frameworks, evolving to meet global standards for drug traceability and tamper-evidence, significantly influence packaging material choices and design. Competitive product substitutes are becoming more prevalent, pushing manufacturers towards differentiation through material innovation, sustainability, and smart packaging features. End-user demographics, such as the growing elderly population and the rise of chronic diseases, are shaping the demand for specialized packaging like easy-open closures and unit-dose packaging. Mergers and acquisitions (M&A) trends are on the rise as companies seek to expand their product portfolios, geographical reach, and technological capabilities. For instance, the recent acquisition of a smaller specialized packaging firm by a larger entity can unlock new market segments. Barriers to innovation include the high cost of research and development, stringent regulatory approvals, and the need for substantial capital investment in advanced manufacturing technologies.

- Market Concentration: Moderate, with key players holding significant but not dominant market shares.

- Technological Innovation Drivers: Demand for child-resistant packaging, tamper-evident features, and sustainable materials.

- Regulatory Frameworks: Stringent quality control, serialization, and track-and-trace mandates influencing packaging design.

- Competitive Product Substitutes: Increasing adoption of flexible packaging as an alternative to rigid formats in certain applications.

- End-User Demographics: Growing preference for convenient and patient-friendly packaging solutions.

- M&A Trends: Strategic acquisitions to consolidate market position and acquire specialized technologies.

- Innovation Barriers: High R&D costs, lengthy approval processes, and the need for skilled workforce.

Pharmaceutical Packaging Industry in India Growth Trends & Insights

The Indian pharmaceutical packaging market is poised for robust growth, projected to experience a Compound Annual Growth Rate (CAGR) of approximately 7.5% over the forecast period. This expansion is driven by the escalating demand for pharmaceuticals in India, the increasing export of generic drugs, and a growing emphasis on drug safety and regulatory compliance. The market size is expected to grow from an estimated xx million units in 2024 to xx million units by 2033. Adoption rates for advanced packaging solutions, such as high-barrier films and smart packaging technologies incorporating IoT capabilities for temperature monitoring, are steadily increasing. Technological disruptions, including advancements in material science leading to lighter, stronger, and more sustainable packaging options, are reshaping the industry. Consumer behavior shifts are also playing a crucial role, with a greater demand for convenient, single-dose, and eco-friendly packaging. The penetration of specialized packaging for biologics and biosimilars is also on an upward trajectory, indicating a move towards more sophisticated drug delivery systems. The overall market is projected to reach a valuation of over INR 500,000 million by 2033.

Dominant Regions, Countries, or Segments in Pharmaceutical Packaging Industry in India

Within the Indian pharmaceutical packaging landscape, Plastic emerges as the dominant material type, contributing significantly to market growth. Its versatility, cost-effectiveness, and suitability for a wide range of pharmaceutical products make it the preferred choice for manufacturers. This segment is projected to account for over 55% of the total market by volume. Bottles and Vials and Ampoules are leading product types, driven by their widespread use in oral medications and injectable drugs, respectively. The sheer volume of pharmaceutical formulations requiring these primary packaging formats solidifies their dominance. The Western region of India, particularly states like Maharashtra and Gujarat, stands out as a dominant geographical region due to the concentration of major pharmaceutical manufacturing hubs and a robust supply chain infrastructure.

- Material Type Dominance:

- Plastic: High demand due to versatility, cost-effectiveness, and extensive applications in bottles, vials, and pouches. Projected market share of ~55% by volume.

- Glass: Continued significance for sterile injectables and sensitive formulations, particularly Type I borosilicate glass.

- Other Material Types: Growing adoption of advanced polymers and composite materials for specialized applications.

- Product Type Dominance:

- Bottles: Leading product type, catering to the vast market for oral solid dosage forms and liquid medications. Expected volume of xx million units.

- Vials and Ampoules: Crucial for the growing injectable drug market, including vaccines and biologics. Expected volume of xx million units.

- Syringes: Increasing demand for pre-filled syringes driven by convenience and precision dosing.

- Caps and Closures: Essential components with a focus on child-resistance and tamper-evidence.

- Regional Dominance:

- Western India (Maharashtra, Gujarat): Hub of pharmaceutical manufacturing, supported by advanced logistics and a skilled workforce.

- Southern India (Telangana, Andhra Pradesh): Emerging as a significant pharmaceutical and packaging manufacturing cluster.

- Northern India: Growing presence due to government initiatives and expanding pharmaceutical production.

Pharmaceutical Packaging Industry in India Product Landscape

The product landscape of the Indian pharmaceutical packaging industry is continually evolving with a focus on enhanced drug protection, patient compliance, and sustainability. Innovations include the development of advanced barrier films to extend shelf life for sensitive drugs, child-resistant closures that meet stringent safety standards, and tamper-evident seals for product integrity. The introduction of smart packaging solutions, such as those with integrated sensors for temperature and humidity monitoring, is gaining traction for high-value biologics. Furthermore, there is a growing trend towards sustainable packaging materials, including recycled PET and biodegradable plastics, aligning with global environmental consciousness. The performance metrics of these products are evaluated based on their ability to maintain drug stability, ensure user safety, and comply with evolving regulatory requirements, such as serialization for track-and-trace capabilities.

Key Drivers, Barriers & Challenges in Pharmaceutical Packaging Industry in India

Key Drivers: The Indian pharmaceutical packaging market is propelled by several key factors. The burgeoning domestic pharmaceutical market, driven by an increasing population and rising healthcare expenditure, forms a foundational driver. The significant growth in pharmaceutical exports, particularly to regulated markets, necessitates packaging that meets international quality and safety standards. Government initiatives promoting the 'Make in India' campaign and supportive policies for the pharmaceutical sector also act as significant accelerators. Technological advancements in packaging materials and machinery are enabling the creation of more sophisticated and efficient packaging solutions.

Barriers & Challenges: Despite robust growth, the industry faces notable challenges. Volatility in raw material prices, especially for plastics and specialized polymers, can impact manufacturing costs and profit margins. Stringent and ever-evolving regulatory compliance, including serialization and track-and-trace mandates, requires continuous investment in technology and processes. Supply chain disruptions, exacerbated by global events, can affect the availability and timely delivery of critical packaging materials. Intense competition from both domestic and international players puts pressure on pricing and demands constant innovation. Furthermore, the initial capital investment required for advanced packaging technologies can be a significant barrier for smaller players.

Emerging Opportunities in Pharmaceutical Packaging Industry in India

Emerging opportunities in the Indian pharmaceutical packaging sector lie in the growing demand for specialized packaging for biologics and biosimilars, which require advanced cold-chain solutions and tamper-evident features. The increasing focus on sustainability presents significant opportunities for manufacturers of eco-friendly packaging materials, such as biodegradable plastics, recycled content, and reusable packaging systems. The "digitalization of healthcare" trend opens avenues for smart packaging solutions, including those with IoT integration for real-time drug monitoring and patient adherence tracking. Furthermore, the expanding e-pharmacy market is creating a demand for robust and secure secondary packaging to ensure product integrity during transit.

Growth Accelerators in the Pharmaceutical Packaging Industry in India Industry

Several catalysts are accelerating the long-term growth of the Indian pharmaceutical packaging industry. Technological breakthroughs in material science are leading to the development of advanced, high-performance packaging that offers superior protection and extended shelf life. Strategic partnerships between pharmaceutical companies and packaging manufacturers are fostering innovation and co-development of tailored packaging solutions. Market expansion strategies, including a focus on rural healthcare access and the growing demand for affordable generic medicines, are creating new avenues for growth. The increasing emphasis on contract manufacturing organizations (CMOs) and contract development and manufacturing organizations (CDMOs) within the pharmaceutical sector also indirectly fuels demand for specialized packaging services.

Key Players Shaping the Pharmaceutical Packaging Industry in India Market

- West Pharmaceutical Services Inc

- Essel Propack Ltd

- SGD Pharma

- Amcor Group Gmbh

- Graham Blow Pack Pvt Ltd

- Uflex Limited

- Geresheimer AG

- Regent Plast Private Limited

- Parekhplast India Limited

- Huhtamaki Oyj

Notable Milestones in Pharmaceutical Packaging Industry in India Sector

- February 2024: Loop Industries announced the launch of its new pharmaceutical packaging bottle, developed in partnership with the leading pharma company, Bormioli Pharmaceutical, which operates in India. The new pharmaceutical packaging bottle is made from Loop’s 100% recycled, virgin-quality PET (polyethylene terephthalate) resin.

- June 2023: SGD Pharma announced a new partnership with Corning supported by investment from the Government of Telangana in India. This joint venture brings together Corning's cutting-edge coating technology and SGD Pharma's glass-converting experience to produce Velocity Vials, a type I borosilicate glass tubing. The construction of the new tubing plant officially kicked off with a ground-breaking ceremony in June 2023 at the plant located in Vemula, India. Upon completion, this new plant will extend SGD's pharmaceutical packaging manufacturing capabilities in India and provide access to Corning's Velocity Vial technology throughout the region.

In-Depth Pharmaceutical Packaging Industry in India Market Outlook

The outlook for the Indian pharmaceutical packaging industry is exceptionally positive, driven by sustained growth in the pharmaceutical sector and increasing adoption of advanced packaging technologies. Future market potential is significant, particularly in the segments of sustainable packaging, smart packaging solutions, and specialized packaging for biologics. Strategic opportunities abound for companies that can offer innovative, compliant, and cost-effective packaging solutions. The increasing focus on patient-centric design and the growing demand for convenience will continue to shape product development. Investments in R&D, coupled with collaborations between packaging providers and pharmaceutical manufacturers, will be crucial for capitalizing on these opportunities and maintaining a competitive edge in this dynamic market.

Pharmaceutical Packaging Industry in India Segmentation

-

1. Material Type

- 1.1. Plastic

- 1.2. Glass

- 1.3. Other Material Types

-

2. Product Type

- 2.1. Bottles

- 2.2. Vials and Ampoules

- 2.3. Syringes

- 2.4. Tubes

- 2.5. Caps and Closures

- 2.6. Pouches and Bags

- 2.7. Labels

- 2.8. Other Product Types

Pharmaceutical Packaging Industry in India Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Pharmaceutical Packaging Industry in India Regional Market Share

Geographic Coverage of Pharmaceutical Packaging Industry in India

Pharmaceutical Packaging Industry in India REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Plastic

- 5.1.2. Glass

- 5.1.3. Other Material Types

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Bottles

- 5.2.2. Vials and Ampoules

- 5.2.3. Syringes

- 5.2.4. Tubes

- 5.2.5. Caps and Closures

- 5.2.6. Pouches and Bags

- 5.2.7. Labels

- 5.2.8. Other Product Types

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. Global Pharmaceutical Packaging Industry in India Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Plastic

- 6.1.2. Glass

- 6.1.3. Other Material Types

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Bottles

- 6.2.2. Vials and Ampoules

- 6.2.3. Syringes

- 6.2.4. Tubes

- 6.2.5. Caps and Closures

- 6.2.6. Pouches and Bags

- 6.2.7. Labels

- 6.2.8. Other Product Types

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. North America Pharmaceutical Packaging Industry in India Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 7.1.1. Plastic

- 7.1.2. Glass

- 7.1.3. Other Material Types

- 7.2. Market Analysis, Insights and Forecast - by Product Type

- 7.2.1. Bottles

- 7.2.2. Vials and Ampoules

- 7.2.3. Syringes

- 7.2.4. Tubes

- 7.2.5. Caps and Closures

- 7.2.6. Pouches and Bags

- 7.2.7. Labels

- 7.2.8. Other Product Types

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 8. South America Pharmaceutical Packaging Industry in India Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 8.1.1. Plastic

- 8.1.2. Glass

- 8.1.3. Other Material Types

- 8.2. Market Analysis, Insights and Forecast - by Product Type

- 8.2.1. Bottles

- 8.2.2. Vials and Ampoules

- 8.2.3. Syringes

- 8.2.4. Tubes

- 8.2.5. Caps and Closures

- 8.2.6. Pouches and Bags

- 8.2.7. Labels

- 8.2.8. Other Product Types

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 9. Europe Pharmaceutical Packaging Industry in India Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 9.1.1. Plastic

- 9.1.2. Glass

- 9.1.3. Other Material Types

- 9.2. Market Analysis, Insights and Forecast - by Product Type

- 9.2.1. Bottles

- 9.2.2. Vials and Ampoules

- 9.2.3. Syringes

- 9.2.4. Tubes

- 9.2.5. Caps and Closures

- 9.2.6. Pouches and Bags

- 9.2.7. Labels

- 9.2.8. Other Product Types

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 10. Middle East & Africa Pharmaceutical Packaging Industry in India Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 10.1.1. Plastic

- 10.1.2. Glass

- 10.1.3. Other Material Types

- 10.2. Market Analysis, Insights and Forecast - by Product Type

- 10.2.1. Bottles

- 10.2.2. Vials and Ampoules

- 10.2.3. Syringes

- 10.2.4. Tubes

- 10.2.5. Caps and Closures

- 10.2.6. Pouches and Bags

- 10.2.7. Labels

- 10.2.8. Other Product Types

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 11. Asia Pacific Pharmaceutical Packaging Industry in India Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Material Type

- 11.1.1. Plastic

- 11.1.2. Glass

- 11.1.3. Other Material Types

- 11.2. Market Analysis, Insights and Forecast - by Product Type

- 11.2.1. Bottles

- 11.2.2. Vials and Ampoules

- 11.2.3. Syringes

- 11.2.4. Tubes

- 11.2.5. Caps and Closures

- 11.2.6. Pouches and Bags

- 11.2.7. Labels

- 11.2.8. Other Product Types

- 11.1. Market Analysis, Insights and Forecast - by Material Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 West Pharmaceutical Services Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Essel Propack Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 SGD Pharma

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Amcor Group Gmbh

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Graham Blow Pack Pvt Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Uflex Limited

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Geresheimer AG*List Not Exhaustive

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Regent Plast Private Limited

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Parekhplast India Limited

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Huhtamaki Oyj

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 West Pharmaceutical Services Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Pharmaceutical Packaging Industry in India Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Pharmaceutical Packaging Industry in India Revenue (Million), by Material Type 2025 & 2033

- Figure 3: North America Pharmaceutical Packaging Industry in India Revenue Share (%), by Material Type 2025 & 2033

- Figure 4: North America Pharmaceutical Packaging Industry in India Revenue (Million), by Product Type 2025 & 2033

- Figure 5: North America Pharmaceutical Packaging Industry in India Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America Pharmaceutical Packaging Industry in India Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Pharmaceutical Packaging Industry in India Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Pharmaceutical Packaging Industry in India Revenue (Million), by Material Type 2025 & 2033

- Figure 9: South America Pharmaceutical Packaging Industry in India Revenue Share (%), by Material Type 2025 & 2033

- Figure 10: South America Pharmaceutical Packaging Industry in India Revenue (Million), by Product Type 2025 & 2033

- Figure 11: South America Pharmaceutical Packaging Industry in India Revenue Share (%), by Product Type 2025 & 2033

- Figure 12: South America Pharmaceutical Packaging Industry in India Revenue (Million), by Country 2025 & 2033

- Figure 13: South America Pharmaceutical Packaging Industry in India Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Pharmaceutical Packaging Industry in India Revenue (Million), by Material Type 2025 & 2033

- Figure 15: Europe Pharmaceutical Packaging Industry in India Revenue Share (%), by Material Type 2025 & 2033

- Figure 16: Europe Pharmaceutical Packaging Industry in India Revenue (Million), by Product Type 2025 & 2033

- Figure 17: Europe Pharmaceutical Packaging Industry in India Revenue Share (%), by Product Type 2025 & 2033

- Figure 18: Europe Pharmaceutical Packaging Industry in India Revenue (Million), by Country 2025 & 2033

- Figure 19: Europe Pharmaceutical Packaging Industry in India Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Pharmaceutical Packaging Industry in India Revenue (Million), by Material Type 2025 & 2033

- Figure 21: Middle East & Africa Pharmaceutical Packaging Industry in India Revenue Share (%), by Material Type 2025 & 2033

- Figure 22: Middle East & Africa Pharmaceutical Packaging Industry in India Revenue (Million), by Product Type 2025 & 2033

- Figure 23: Middle East & Africa Pharmaceutical Packaging Industry in India Revenue Share (%), by Product Type 2025 & 2033

- Figure 24: Middle East & Africa Pharmaceutical Packaging Industry in India Revenue (Million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Pharmaceutical Packaging Industry in India Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Pharmaceutical Packaging Industry in India Revenue (Million), by Material Type 2025 & 2033

- Figure 27: Asia Pacific Pharmaceutical Packaging Industry in India Revenue Share (%), by Material Type 2025 & 2033

- Figure 28: Asia Pacific Pharmaceutical Packaging Industry in India Revenue (Million), by Product Type 2025 & 2033

- Figure 29: Asia Pacific Pharmaceutical Packaging Industry in India Revenue Share (%), by Product Type 2025 & 2033

- Figure 30: Asia Pacific Pharmaceutical Packaging Industry in India Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific Pharmaceutical Packaging Industry in India Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Pharmaceutical Packaging Industry in India Revenue Million Forecast, by Material Type 2020 & 2033

- Table 2: Global Pharmaceutical Packaging Industry in India Revenue Million Forecast, by Product Type 2020 & 2033

- Table 3: Global Pharmaceutical Packaging Industry in India Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Pharmaceutical Packaging Industry in India Revenue Million Forecast, by Material Type 2020 & 2033

- Table 5: Global Pharmaceutical Packaging Industry in India Revenue Million Forecast, by Product Type 2020 & 2033

- Table 6: Global Pharmaceutical Packaging Industry in India Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global Pharmaceutical Packaging Industry in India Revenue Million Forecast, by Material Type 2020 & 2033

- Table 11: Global Pharmaceutical Packaging Industry in India Revenue Million Forecast, by Product Type 2020 & 2033

- Table 12: Global Pharmaceutical Packaging Industry in India Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Brazil Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Global Pharmaceutical Packaging Industry in India Revenue Million Forecast, by Material Type 2020 & 2033

- Table 17: Global Pharmaceutical Packaging Industry in India Revenue Million Forecast, by Product Type 2020 & 2033

- Table 18: Global Pharmaceutical Packaging Industry in India Revenue Million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Germany Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: France Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Italy Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Spain Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Russia Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Global Pharmaceutical Packaging Industry in India Revenue Million Forecast, by Material Type 2020 & 2033

- Table 29: Global Pharmaceutical Packaging Industry in India Revenue Million Forecast, by Product Type 2020 & 2033

- Table 30: Global Pharmaceutical Packaging Industry in India Revenue Million Forecast, by Country 2020 & 2033

- Table 31: Turkey Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Israel Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: GCC Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Global Pharmaceutical Packaging Industry in India Revenue Million Forecast, by Material Type 2020 & 2033

- Table 38: Global Pharmaceutical Packaging Industry in India Revenue Million Forecast, by Product Type 2020 & 2033

- Table 39: Global Pharmaceutical Packaging Industry in India Revenue Million Forecast, by Country 2020 & 2033

- Table 40: China Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 41: India Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Japan Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Pharmaceutical Packaging Industry in India Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Pharmaceutical Packaging Industry in India?

The projected CAGR is approximately 8.00%.

2. Which companies are prominent players in the Pharmaceutical Packaging Industry in India?

Key companies in the market include West Pharmaceutical Services Inc, Essel Propack Ltd, SGD Pharma, Amcor Group Gmbh, Graham Blow Pack Pvt Ltd, Uflex Limited, Geresheimer AG*List Not Exhaustive, Regent Plast Private Limited, Parekhplast India Limited, Huhtamaki Oyj.

3. What are the main segments of the Pharmaceutical Packaging Industry in India?

The market segments include Material Type, Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.36 Million as of 2022.

5. What are some drivers contributing to market growth?

Low Cost of Production and Increased R&D Activities; Increased Expenditure on Healthcare and Medicine.

6. What are the notable trends driving market growth?

Glass Packaging is Expected to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

Growing Sustainability Concerns.

8. Can you provide examples of recent developments in the market?

February 2024 - Loop Industries announced the launch of its new pharmaceutical packaging bottle, developed in partnership with the leading pharma company, Bormioli Pharmaceutical, which operates in India. The new pharmaceutical packaging bottle is made from Loop’s 100% recycled, virgin-quality PET (polyethylene terephthalate) resin.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Pharmaceutical Packaging Industry in India," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Pharmaceutical Packaging Industry in India report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Pharmaceutical Packaging Industry in India?

To stay informed about further developments, trends, and reports in the Pharmaceutical Packaging Industry in India, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence