Key Insights

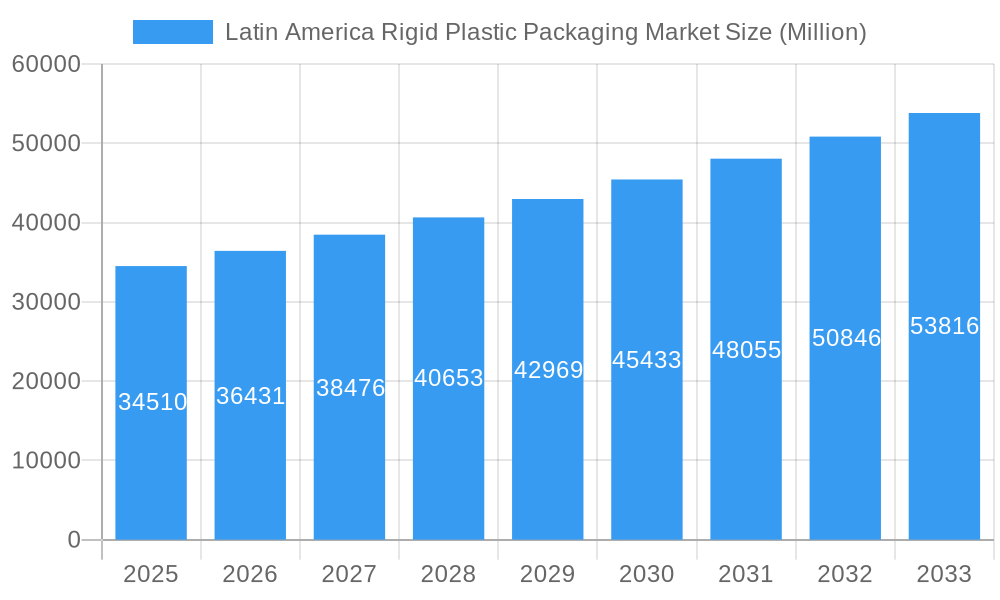

The Latin America Rigid Plastic Packaging Market is poised for robust expansion, with a projected market size of $34.51 billion in 2025 and an anticipated Compound Annual Growth Rate (CAGR) of 5.5% through 2033. This significant growth is fueled by a confluence of factors, including a burgeoning middle class, increasing consumer demand for convenience and product safety across diverse end-user industries, and the inherent benefits of rigid plastic packaging such as its durability, cost-effectiveness, and versatility. The food and beverage sectors, in particular, represent dominant segments, driven by the need for secure and appealing packaging solutions for a wide array of products, from fresh produce to processed goods. Furthermore, the rising adoption of e-commerce and the associated logistical demands are creating a sustained need for robust packaging like Intermediate Bulk Containers (IBCs) and drums.

Latin America Rigid Plastic Packaging Market Market Size (In Billion)

The market's dynamism is further shaped by evolving consumer preferences and regulatory landscapes. While plastic packaging offers advantages, increasing environmental consciousness is driving innovation towards sustainable solutions, including the use of recycled plastics and the development of biodegradable alternatives. This trend is a significant factor influencing market strategies and investments. Key market restraints include fluctuating raw material prices, which can impact production costs, and stringent environmental regulations in certain regions that may necessitate compliance upgrades or shifts in material usage. The competitive landscape is characterized by the presence of both established global players and emerging regional manufacturers, all vying for market share through product innovation, strategic partnerships, and an emphasis on sustainable practices to cater to the evolving demands of the Latin American consumer and industrial base.

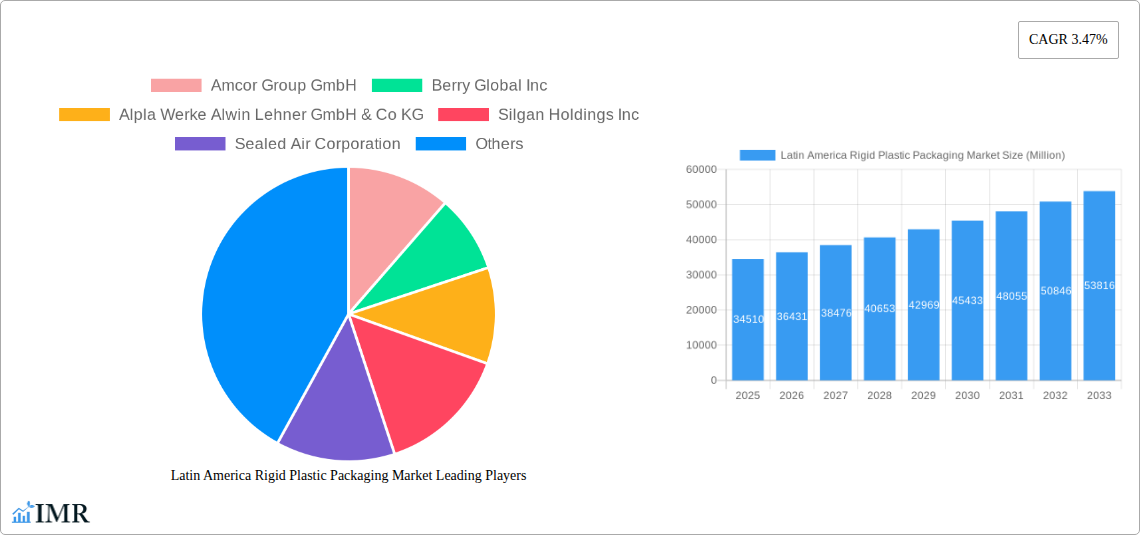

Latin America Rigid Plastic Packaging Market Company Market Share

Here's a compelling, SEO-optimized report description for the Latin America Rigid Plastic Packaging Market, incorporating high-traffic keywords, parent/child markets, and adhering to your specified structure and content requirements.

Report Title: Latin America Rigid Plastic Packaging Market: Market Size, Trends, Share, Growth, and Forecast 2024-2033

Report Description:

Dive into the dynamic Latin America rigid plastic packaging market, a crucial sector projected to witness significant expansion driven by evolving consumer preferences, increasing demand from key end-user industries, and a growing emphasis on sustainable packaging solutions. This comprehensive report offers an in-depth analysis of the rigid plastic packaging market in Latin America, covering market size, growth trends, market share, competitive landscape, and future outlook. Explore the intricate interplay of parent and child markets, from raw material resins like Polyethylene (PE), Polyethylene Terephthalate (PET), and Polypropylene (PP) to diverse product types including bottles, jars, trays, containers, caps, and closures. Uncover the vital role of rigid plastics across major end-user industries such as Food & Beverage, Healthcare, Cosmetics & Personal Care, and Industrial applications. With a detailed forecast period extending from 2025 to 2033, and historical data from 2019-2024, this report is an indispensable resource for stakeholders seeking to understand market dynamics, identify growth opportunities, and navigate the challenges within this burgeoning market.

Latin America Rigid Plastic Packaging Market Market Dynamics & Structure

The Latin America rigid plastic packaging market is characterized by a moderate to high level of concentration, with a few dominant global players alongside a growing number of regional manufacturers. Technological innovation is a key driver, particularly in areas like lightweighting, barrier properties, and the integration of recycled content. Regulatory frameworks, especially concerning environmental sustainability and waste management, are increasingly shaping market strategies and product development. Competitive product substitutes, including glass and metal packaging, exert pressure, but the cost-effectiveness and versatility of rigid plastics often give them an advantage. End-user demographics, particularly the growing middle class and urbanization trends, are fueling demand for packaged goods. Mergers and acquisitions (M&A) are prevalent as companies seek to expand their geographic reach, diversify product portfolios, and gain access to advanced technologies.

- Market Concentration: Dominated by key players, but with increasing regional competition.

- Technological Innovation: Focus on sustainable materials, improved functionality, and recyclability.

- Regulatory Frameworks: Growing emphasis on Extended Producer Responsibility (EPR) and recycled content mandates.

- Competitive Substitutes: Glass and metal packaging present alternatives, but cost and performance often favor plastics.

- End-User Demographics: Urbanization, rising disposable incomes, and evolving consumption patterns are key influencers.

- M&A Trends: Strategic acquisitions to enhance market share, technological capabilities, and supply chain integration.

- Example M&A Impact: Estimated xx number of deals in the historical period, contributing to an estimated xx% consolidation.

Latin America Rigid Plastic Packaging Market Growth Trends & Insights

The Latin America rigid plastic packaging market is poised for robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately XX% from 2025 to 2033. This expansion is fueled by a confluence of factors, including the increasing demand for convenient and safe packaging solutions across various end-user industries, particularly Food & Beverage and Healthcare. The burgeoning middle class and rapid urbanization in countries like Brazil, Mexico, and Colombia are significantly boosting consumer spending on packaged goods, thereby driving the demand for rigid plastic containers, bottles, and jars. Furthermore, technological advancements in material science and manufacturing processes are leading to the development of more sustainable and high-performance rigid plastic packaging, appealing to environmentally conscious consumers and stringent regulatory bodies. Adoption rates for advanced recycling technologies and the incorporation of Post-Consumer Recycled (PCR) content are on the rise, reflecting a broader industry shift towards a circular economy. Consumer behavior is also evolving, with a greater preference for single-serving portions, on-the-go consumption, and products that offer extended shelf life – all areas where rigid plastic packaging excels. The market is witnessing a technological disruption through the development of smart packaging solutions, offering enhanced traceability and consumer engagement. Market penetration of rigid plastic packaging in the food sector is already high, estimated at xx billion units, and is expected to grow further. The beverage segment is another significant contributor, with an estimated xx billion units consumed annually.

Dominant Regions, Countries, or Segments in Latin America Rigid Plastic Packaging Market

The Latin America rigid plastic packaging market is predominantly driven by Brazil and Mexico, which collectively account for over 60% of the regional market share. These countries boast large and diverse economies, substantial populations, and a significant manufacturing base, particularly in the Food & Beverage and Consumer Goods sectors.

Key Dominant Segments:

Resin:

- Polyethylene Terephthalate (PET): This is the dominant resin due to its excellent clarity, strength, and recyclability, making it ideal for beverage bottles and food containers. Its market share is estimated at xx billion units.

- Polyethylene (PE): Including LDPE, LLDPE, and HDPE, PE is crucial for a wide range of applications, from bottles and containers to drums and IBCs, contributing approximately xx billion units to the market.

- Polypropylene (PP): Valued for its heat resistance and chemical inertness, PP is a key material for trays, containers, and caps, with an estimated market contribution of xx billion units.

Product Type:

- Bottles and Jars: This segment is the largest, driven by the beverage and food industries, accounting for an estimated xx billion units.

- Trays and Containers: Essential for food preservation and transport, this segment is also a significant growth area, contributing around xx billion units.

- Caps and Closures: Critical for product integrity and safety, this segment is vital for almost all packaged goods, with an estimated xx billion units.

End-user Industry:

- Food: This is the largest end-user industry, encompassing sub-segments like Dairy Products, Dry Foods, and Frozen Foods, contributing an estimated xx billion units.

- Beverage: A consistently strong performer, this segment relies heavily on PET bottles and contributes approximately xx billion units.

- Cosmetics and Personal Care: Growing demand for aesthetically pleasing and functional packaging drives growth here, with an estimated xx billion units.

- Healthcare: Stringent requirements for safety and sterility make rigid plastics essential, contributing an estimated xx billion units.

The dominance of these regions and segments is further amplified by favorable economic policies, developing infrastructure for manufacturing and logistics, and increasing consumer adoption of packaged goods. Market share projections indicate continued growth in these areas throughout the forecast period.

Latin America Rigid Plastic Packaging Market Product Landscape

The Latin America rigid plastic packaging market is characterized by a continuous stream of product innovations aimed at enhancing functionality, sustainability, and consumer appeal. Key product developments include the introduction of lightweighted bottles and containers that reduce material usage and transportation costs, the incorporation of advanced barrier technologies to extend shelf life, and the design of user-friendly packaging with features like easy-open caps and ergonomic shapes. Applications are diverse, ranging from single-serve beverage bottles and family-sized food tubs to durable industrial drums and sterile medical device packaging. Performance metrics such as impact resistance, chemical inertness, and thermal stability are critical considerations. Unique selling propositions often revolve around recyclability, the use of recycled content, and compliance with food-grade standards. Technological advancements, such as multi-layer co-extrusion for enhanced barrier properties and injection molding techniques for complex designs, are continuously shaping the product landscape.

Key Drivers, Barriers & Challenges in Latin America Rigid Plastic Packaging Market

Key Drivers:

- Growing Demand from End-User Industries: The expansion of the Food & Beverage, Healthcare, and Cosmetics sectors fuels the need for rigid plastic packaging.

- Increasing Disposable Incomes and Urbanization: Leading to higher consumption of packaged goods, particularly in emerging economies.

- Technological Advancements: Development of lightweight, durable, and aesthetically appealing packaging solutions.

- Focus on Sustainability: Growing adoption of recycled plastics and advancements in recycling infrastructure.

- Cost-Effectiveness and Versatility: Rigid plastics offer a balance of performance and affordability.

Barriers & Challenges:

- Environmental Concerns and Regulations: Increasing pressure to reduce plastic waste and improve recycling rates.

- Fluctuating Raw Material Prices: Volatility in the cost of resins like PE and PET can impact profitability.

- Competition from Alternative Materials: Glass, metal, and paper-based packaging pose competitive threats.

- Supply Chain Disruptions: Geopolitical events and logistical challenges can affect raw material availability and delivery timelines.

- Infrastructure Limitations: In some regions, inadequate waste management and recycling infrastructure can hinder growth.

- Capital Investment for Sustainable Technologies: Implementing advanced recycling and bio-based material technologies requires significant investment.

Emerging Opportunities in Latin America Rigid Plastic Packaging Market

Emerging opportunities within the Latin America rigid plastic packaging market lie in the increasing demand for sustainable packaging solutions, including the widespread adoption of Post-Consumer Recycled (PCR) materials and the exploration of bio-based plastics. The growth of e-commerce presents a significant avenue for specialized rigid plastic packaging designed for safe and efficient shipping. Furthermore, the "on-the-go" consumption trend is driving demand for convenient, single-serve rigid plastic packaging across various food and beverage categories. Untapped markets in less developed regions within Latin America, coupled with innovative applications in sectors like personal care and home care, offer substantial growth potential. The development of smart packaging features, such as QR codes for traceability and consumer engagement, represents another promising area.

Growth Accelerators in the Latin America Rigid Plastic Packaging Market Industry

Several catalysts are accelerating the growth of the Latin America rigid plastic packaging market. Technological breakthroughs in chemical recycling are enabling the transformation of hard-to-recycle plastics into virgin-grade materials, bolstering the circular economy. Strategic partnerships between packaging manufacturers, resin producers, and end-users are crucial for driving innovation and ensuring the adoption of sustainable solutions. Market expansion strategies, including investments in new manufacturing facilities and the development of localized supply chains, are crucial for meeting the growing regional demand. The increasing consumer awareness regarding the environmental impact of packaging is pushing brands to adopt more sustainable rigid plastic solutions, thereby accelerating their market penetration and development.

Key Players Shaping the Latin America Rigid Plastic Packaging Market Market

- Amcor Group GmbH

- Berry Global Inc

- Alpla Werke Alwin Lehner GmbH & Co KG

- Silgan Holdings Inc

- Sealed Air Corporation

- Plastipak Holding Inc

- Sonoco Products Company

- Albea Group

- Greiner Packaging International GmbH

- BERICAP Holding GmbH

- Rioplastic

- IPACKCHEM GROUP

Notable Milestones in Latin America Rigid Plastic Packaging Market Sector

- June 2024: Method, in partnership with SC Johnson and Plastic Bank, announced its transparent plastic bottles are now made entirely from 100% recycled coastal plastic, with Plastic Bank having established over 550 collection sites in countries including Brazil.

- August 2023: Indorama Ventures invested USD 20 million to modernize its recycled PET (rePET) resin recycling operations in Brazil, enhancing efficiency and reducing water consumption by 70%.

- May 2023: Greenback announced the commencement of operations at its state-of-the-art plastic recycling facility in Cuautla, Mexico, in collaboration with Nestle, designed to circularize non-recyclable plastics.

In-Depth Latin America Rigid Plastic Packaging Market Market Outlook

The Latin America rigid plastic packaging market is characterized by a robust outlook, driven by the region's economic development and a growing consumer preference for convenient and safe packaged goods. Key growth accelerators include the persistent demand from the Food & Beverage sector, the increasing adoption of sustainable packaging practices, and ongoing technological advancements that enhance product performance and recyclability. Strategic partnerships and investments in advanced recycling technologies will play a pivotal role in shaping the market's future, enabling a more circular economy. The market is expected to witness continued innovation in material science and packaging design, catering to evolving consumer needs and regulatory landscapes. This forward momentum suggests significant future market potential and substantial strategic opportunities for stakeholders within the Latin American rigid plastic packaging industry.

Latin America Rigid Plastic Packaging Market Segmentation

-

1. Resin

-

1.1. Polyethylene (PE)

- 1.1.1. LDPE and LLDPE

- 1.1.2. HDPE

- 1.2. Polyethylene terephthalate (PET)

- 1.3. Polypropylene (PP)

- 1.4. Polystyrene (PS) and Expanded polystyrene (EPS)

- 1.5. Polyvinyl chloride (PVC)

- 1.6. Other Re

-

1.1. Polyethylene (PE)

-

2. Product Type

- 2.1. Bottles and Jars

- 2.2. Trays and Containers

- 2.3. Caps and Closures

- 2.4. Intermediate Bulk Containers (IBCs)

- 2.5. Drums

- 2.6. Pallets

- 2.7. Other Pr

-

3. End-user Industry

-

3.1. Food**

- 3.1.1. Candy and Confectionery

- 3.1.2. Frozen Foods

- 3.1.3. Fresh Produce

- 3.1.4. Dairy Products

- 3.1.5. Dry Foods

- 3.1.6. Meat, Poultry, and Seafood

- 3.1.7. Pet Food

- 3.1.8. Other Fo

-

3.2. Foodservice**

- 3.2.1. Quick Service Restaurants (QSRs)

- 3.2.2. Full-Service Restaurants (FSRs)

- 3.2.3. Coffee and Snack Outlets

- 3.2.4. Retail Establishments

- 3.2.5. Institutional

- 3.2.6. Hospitality

- 3.2.7. Other Foodservice

- 3.3. Beverage

- 3.4. Healthcare

- 3.5. Cosmetics and Personal Care

- 3.6. Industri

- 3.7. Building and Construction

- 3.8. Automotive

- 3.9. Other En

-

3.1. Food**

Latin America Rigid Plastic Packaging Market Segmentation By Geography

-

1. Latin America

- 1.1. Brazil

- 1.2. Argentina

- 1.3. Chile

- 1.4. Colombia

- 1.5. Mexico

- 1.6. Peru

- 1.7. Venezuela

- 1.8. Ecuador

- 1.9. Bolivia

- 1.10. Paraguay

Latin America Rigid Plastic Packaging Market Regional Market Share

Geographic Coverage of Latin America Rigid Plastic Packaging Market

Latin America Rigid Plastic Packaging Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Resin

- 5.1.1. Polyethylene (PE)

- 5.1.1.1. LDPE and LLDPE

- 5.1.1.2. HDPE

- 5.1.2. Polyethylene terephthalate (PET)

- 5.1.3. Polypropylene (PP)

- 5.1.4. Polystyrene (PS) and Expanded polystyrene (EPS)

- 5.1.5. Polyvinyl chloride (PVC)

- 5.1.6. Other Re

- 5.1.1. Polyethylene (PE)

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Bottles and Jars

- 5.2.2. Trays and Containers

- 5.2.3. Caps and Closures

- 5.2.4. Intermediate Bulk Containers (IBCs)

- 5.2.5. Drums

- 5.2.6. Pallets

- 5.2.7. Other Pr

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Food**

- 5.3.1.1. Candy and Confectionery

- 5.3.1.2. Frozen Foods

- 5.3.1.3. Fresh Produce

- 5.3.1.4. Dairy Products

- 5.3.1.5. Dry Foods

- 5.3.1.6. Meat, Poultry, and Seafood

- 5.3.1.7. Pet Food

- 5.3.1.8. Other Fo

- 5.3.2. Foodservice**

- 5.3.2.1. Quick Service Restaurants (QSRs)

- 5.3.2.2. Full-Service Restaurants (FSRs)

- 5.3.2.3. Coffee and Snack Outlets

- 5.3.2.4. Retail Establishments

- 5.3.2.5. Institutional

- 5.3.2.6. Hospitality

- 5.3.2.7. Other Foodservice

- 5.3.3. Beverage

- 5.3.4. Healthcare

- 5.3.5. Cosmetics and Personal Care

- 5.3.6. Industri

- 5.3.7. Building and Construction

- 5.3.8. Automotive

- 5.3.9. Other En

- 5.3.1. Food**

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Latin America

- 5.1. Market Analysis, Insights and Forecast - by Resin

- 6. Latin America Rigid Plastic Packaging Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Resin

- 6.1.1. Polyethylene (PE)

- 6.1.1.1. LDPE and LLDPE

- 6.1.1.2. HDPE

- 6.1.2. Polyethylene terephthalate (PET)

- 6.1.3. Polypropylene (PP)

- 6.1.4. Polystyrene (PS) and Expanded polystyrene (EPS)

- 6.1.5. Polyvinyl chloride (PVC)

- 6.1.6. Other Re

- 6.1.1. Polyethylene (PE)

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Bottles and Jars

- 6.2.2. Trays and Containers

- 6.2.3. Caps and Closures

- 6.2.4. Intermediate Bulk Containers (IBCs)

- 6.2.5. Drums

- 6.2.6. Pallets

- 6.2.7. Other Pr

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Food**

- 6.3.1.1. Candy and Confectionery

- 6.3.1.2. Frozen Foods

- 6.3.1.3. Fresh Produce

- 6.3.1.4. Dairy Products

- 6.3.1.5. Dry Foods

- 6.3.1.6. Meat, Poultry, and Seafood

- 6.3.1.7. Pet Food

- 6.3.1.8. Other Fo

- 6.3.2. Foodservice**

- 6.3.2.1. Quick Service Restaurants (QSRs)

- 6.3.2.2. Full-Service Restaurants (FSRs)

- 6.3.2.3. Coffee and Snack Outlets

- 6.3.2.4. Retail Establishments

- 6.3.2.5. Institutional

- 6.3.2.6. Hospitality

- 6.3.2.7. Other Foodservice

- 6.3.3. Beverage

- 6.3.4. Healthcare

- 6.3.5. Cosmetics and Personal Care

- 6.3.6. Industri

- 6.3.7. Building and Construction

- 6.3.8. Automotive

- 6.3.9. Other En

- 6.3.1. Food**

- 6.1. Market Analysis, Insights and Forecast - by Resin

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Berry Global Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Alpla Werke Alwin Lehner GmbH & Co KG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Silgan Holdings Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Sealed Air Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Plastipak Holding Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Sonoco Products Company

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Albea Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Greiner Packaging International GmbH

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 BERICAP Holding GmbH

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Rioplastic

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 IPACKCHEM GROUP*List Not Exhaustive 7 2 Heat Map Analysis7 3 Competitor Analysis - Emerging vs Established Player

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Amcor Group GmbH

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Latin America Rigid Plastic Packaging Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Latin America Rigid Plastic Packaging Market Share (%) by Company 2025

List of Tables

- Table 1: Latin America Rigid Plastic Packaging Market Revenue billion Forecast, by Resin 2020 & 2033

- Table 2: Latin America Rigid Plastic Packaging Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 3: Latin America Rigid Plastic Packaging Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 4: Latin America Rigid Plastic Packaging Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Latin America Rigid Plastic Packaging Market Revenue billion Forecast, by Resin 2020 & 2033

- Table 6: Latin America Rigid Plastic Packaging Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 7: Latin America Rigid Plastic Packaging Market Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 8: Latin America Rigid Plastic Packaging Market Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Brazil Latin America Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Argentina Latin America Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Chile Latin America Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Colombia Latin America Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico Latin America Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Peru Latin America Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Venezuela Latin America Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Ecuador Latin America Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Bolivia Latin America Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Paraguay Latin America Rigid Plastic Packaging Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Latin America Rigid Plastic Packaging Market?

The projected CAGR is approximately 5.4%.

2. Which companies are prominent players in the Latin America Rigid Plastic Packaging Market?

Key companies in the market include Amcor Group GmbH, Berry Global Inc, Alpla Werke Alwin Lehner GmbH & Co KG, Silgan Holdings Inc, Sealed Air Corporation, Plastipak Holding Inc, Sonoco Products Company, Albea Group, Greiner Packaging International GmbH, BERICAP Holding GmbH, Rioplastic, IPACKCHEM GROUP*List Not Exhaustive 7 2 Heat Map Analysis7 3 Competitor Analysis - Emerging vs Established Player.

3. What are the main segments of the Latin America Rigid Plastic Packaging Market?

The market segments include Resin, Product Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.49 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Sustainable and Innovative Food Packaging Products; Increasing Consumption of Cosmetic Products.

6. What are the notable trends driving market growth?

Food and Beverage Occupies the Largest Market Share.

7. Are there any restraints impacting market growth?

Rising Demand for Sustainable and Innovative Food Packaging Products; Increasing Consumption of Cosmetic Products.

8. Can you provide examples of recent developments in the market?

June 2024: Method, a producer of environmentally conscious cleaning and personal care items, announced a significant shift: all its transparent plastic bottles are crafted entirely from 100% recycled coastal plastic. This move stems from a strategic alliance with SC Johnson and Plastic Bank. Since 2018, SC Johnson, in tandem with Plastic Bank, has overseen the inception of over 550 plastic collection sites, notably in nations like Indonesia, the Philippines, Thailand, and Brazil.August 2023: Indorama Ventures, a player in the production of recycled PET (rePET) resin, extended its recycling operations in Brazil by investing USD 20 million to modernize the facility's operations and purchase new equipment, including washing machines, to facilitate the removal of labels, the grinding of bottles in water, and a 70% reduction in water consumption.May 2023: Greenback claimed to have completed the recycling cycle with its first state-of-the-art plastic recycling facility, which was set to commence operations in collaboration with Nestle, located in the Mexican city of Cuautla. The recycling technology is designed to circularize non-recyclable plastics and trace the origin of the material.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Latin America Rigid Plastic Packaging Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Latin America Rigid Plastic Packaging Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Latin America Rigid Plastic Packaging Market?

To stay informed about further developments, trends, and reports in the Latin America Rigid Plastic Packaging Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence