Key Insights

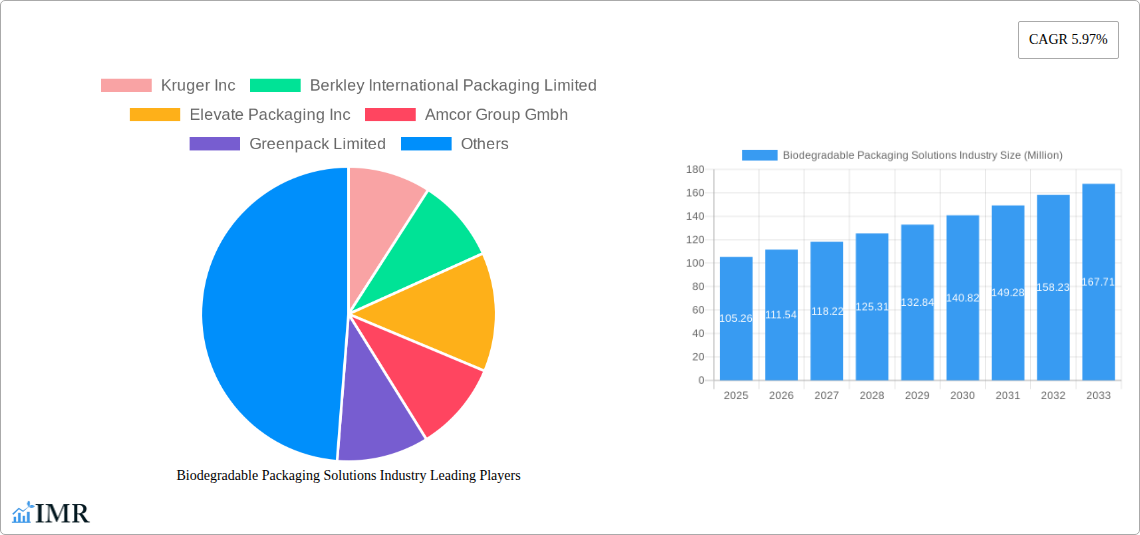

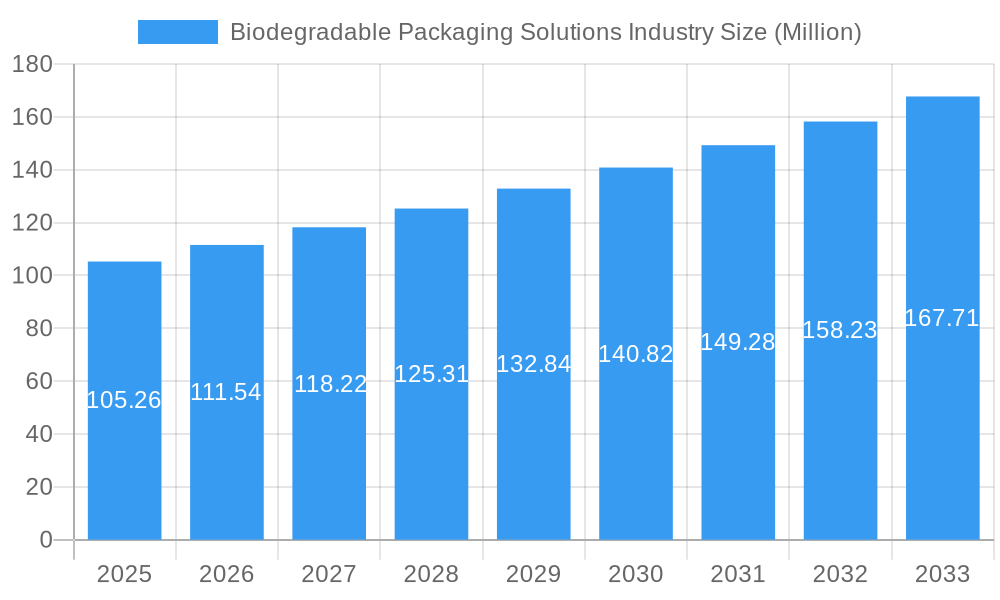

The global Biodegradable Packaging Solutions market is poised for substantial growth, projected to reach an estimated 105.26 million in 2025. This upward trajectory is fueled by a robust Compound Annual Growth Rate (CAGR) of 5.97% throughout the forecast period of 2025-2033. A primary driver behind this expansion is the increasing consumer and regulatory demand for sustainable alternatives to conventional plastics. Growing environmental consciousness, coupled with stringent government regulations aimed at reducing plastic waste and promoting eco-friendly practices, is compelling businesses across various sectors to adopt biodegradable packaging. This shift is particularly evident in the Food Packaging and Beverage Packaging segments, which represent significant application areas due to the high volume of disposable packaging used in these industries. The increasing awareness of the detrimental effects of non-biodegradable materials on ecosystems is further accelerating the adoption of these greener solutions.

Biodegradable Packaging Solutions Industry Market Size (In Million)

The market's expansion is also being significantly influenced by technological advancements in material science and production processes, leading to the development of more cost-effective and performance-driven biodegradable packaging materials. Key material types such as Polylactic Acid (PLA) and Polyhydroxyalkanoates (PHA) are gaining traction due to their enhanced biodegradability and versatility. The Paper segment, including Kraft Paper and Corrugated Fiberboard, continues to be a strong contender, offering readily available and widely accepted sustainable options. While the market is experiencing remarkable growth, certain restraints, such as the higher initial cost of some biodegradable materials compared to traditional plastics and challenges in the existing waste management infrastructure for specialized disposal, need to be addressed to ensure widespread adoption. However, ongoing innovation and scaling of production are expected to mitigate these challenges, paving the way for a more sustainable packaging future.

Biodegradable Packaging Solutions Industry Company Market Share

This in-depth report provides an exhaustive analysis of the global biodegradable packaging solutions market, a rapidly expanding sector driven by increasing environmental consciousness and stringent regulations. Covering the study period from 2019–2033, with 2025 as the base and estimated year, this report offers critical insights into market dynamics, growth trends, dominant segments, and key players. We meticulously examine the evolution of sustainable packaging, including compostable packaging, eco-friendly packaging materials, and bio-based packaging, to guide strategic decision-making for industry stakeholders. This report delves into both the parent market and its crucial child markets, providing a holistic view of the biodegradable packaging industry.

Biodegradable Packaging Solutions Industry Market Dynamics & Structure

The biodegradable packaging solutions market is characterized by a dynamic interplay of factors shaping its current and future trajectory. Market concentration is observed to be moderately fragmented, with both large multinational corporations and agile startups vying for market share. Technological innovation is a primary driver, fueled by the continuous development of novel biodegradable polymers and advanced manufacturing processes for sustainable packaging materials. Regulatory frameworks, including bans on single-use plastics and incentives for eco-friendly packaging, are increasingly influencing market penetration. Competitive product substitutes, primarily conventional plastics, still pose a challenge, but the superior environmental credentials of biodegradable packaging are gaining traction. End-user demographics are shifting towards a greater preference for sustainable products, particularly among younger generations and environmentally conscious consumers. Mergers & Acquisitions (M&A) trends indicate consolidation and strategic partnerships aimed at expanding product portfolios and geographical reach within the green packaging landscape.

- Market Concentration: Moderately fragmented with a mix of established players and new entrants.

- Technological Innovation Drivers: Development of advanced biodegradable plastics (e.g., PLA, PHA), improved barrier properties, and cost-effective production methods.

- Regulatory Frameworks: Stringent environmental regulations, extended producer responsibility schemes, and government subsidies for sustainable packaging solutions.

- Competitive Product Substitutes: Continued reliance on conventional plastics in certain applications, though facing increasing pressure from biodegradable alternatives.

- End-User Demographics: Growing consumer demand for eco-friendly packaging driven by environmental awareness and ethical purchasing habits.

- M&A Trends: Strategic acquisitions and collaborations to enhance R&D capabilities, expand production capacity, and gain market access.

Biodegradable Packaging Solutions Industry Growth Trends & Insights

The biodegradable packaging solutions market is poised for robust growth, driven by a confluence of factors that are fundamentally reshaping the packaging industry. The market size evolution is marked by a consistent upward trajectory, fueled by increasing consumer demand for sustainable packaging options and supportive government policies. Adoption rates for biodegradable packaging materials are accelerating across various applications, demonstrating a clear shift away from traditional, less environmentally friendly alternatives. Technological disruptions, such as advancements in biopolymer research and the development of compostable packaging solutions, are further enhancing the performance and cost-effectiveness of these materials. Consumer behavior shifts, including a heightened awareness of plastic pollution and a preference for brands demonstrating environmental responsibility, are directly translating into increased market penetration for eco-friendly packaging. The food packaging segment, in particular, is witnessing significant innovation, with companies developing biodegradable food packaging that meets stringent safety and performance requirements. The beverage packaging sector is also actively exploring sustainable alternatives to reduce its environmental footprint. The overall CAGR is projected to remain strong throughout the forecast period, reflecting the industry's commitment to sustainability and innovation in plastic alternative packaging.

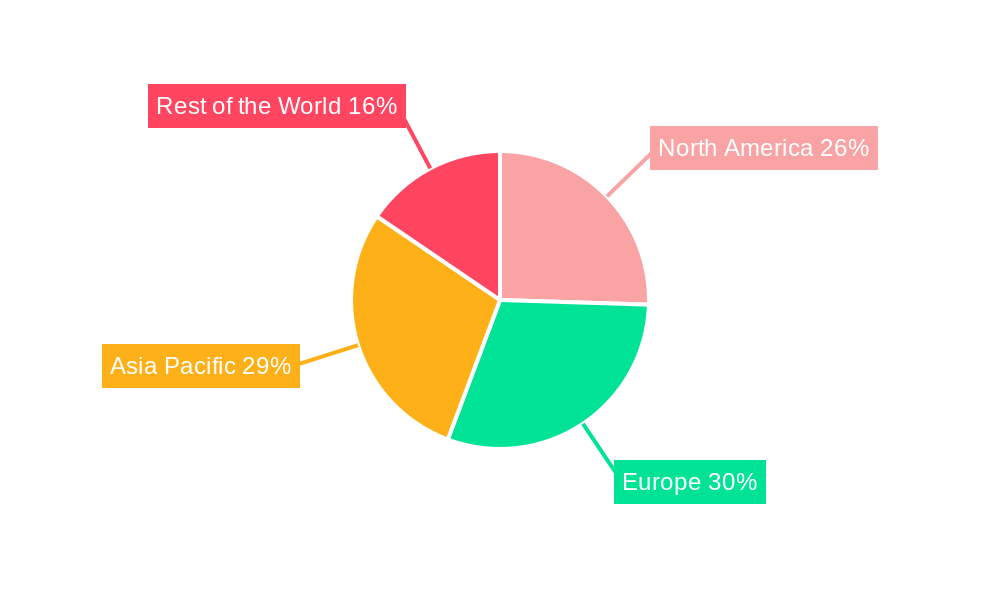

Dominant Regions, Countries, or Segments in Biodegradable Packaging Solutions Industry

The biodegradable packaging solutions industry exhibits distinct regional and segmental dominance, driven by a complex interplay of economic, environmental, and regulatory factors.

North America is emerging as a significant growth engine, propelled by increasing consumer awareness and stringent environmental regulations, particularly in countries like the United States and Canada. Government initiatives promoting sustainable packaging and corporate sustainability goals are creating a fertile ground for market expansion.

Within the Material Type segment, Polylactic Acid (PLA) continues to lead, owing to its versatility, widespread availability, and proven biodegradability in industrial composting facilities. Its application in food packaging and beverage packaging is particularly prominent. However, Polyhydroxyalkanoates (PHA) are gaining considerable traction due to their enhanced biodegradability, even in marine environments, positioning them as a promising material for future growth. Paper-based packaging, including Corrugated Fiberboard and Boxboard, also holds a substantial market share, driven by its recyclability and renewable nature, especially in e-commerce packaging and food packaging.

In terms of Application, Food Packaging commands the largest share. The demand for biodegradable food packaging is immense, driven by concerns over food safety, shelf-life, and the environmental impact of conventional plastic food containers and wraps. Beverage Packaging, including biodegradable bottles and compostable cups, is another major application area experiencing rapid growth. The Personal/Homecare Packaging segment is also witnessing a surge in demand for sustainable solutions.

Key Drivers in North America:

- Strong consumer demand for eco-friendly products.

- Supportive government policies and Extended Producer Responsibility (EPR) schemes.

- Corporate sustainability commitments and reduction targets for plastic waste.

- Advancements in biopolymer research and manufacturing technologies.

Dominance Factors in Material Type:

- Polylactic Acid (PLA): Cost-effectiveness, broad applications, established supply chain.

- Paper: High recyclability, renewable resource, versatility in various forms like Kraft Paper and Corrugated Fiberboard.

- PHA: Superior biodegradability, growing research and development, potential for niche applications.

Dominance Factors in Application:

- Food Packaging: High volume requirements, consumer preference for safe and sustainable options, regulatory pressures.

- Beverage Packaging: Focus on reducing single-use plastic waste, innovation in biodegradable bottles and cups.

Biodegradable Packaging Solutions Industry Product Landscape

The biodegradable packaging solutions market is characterized by a dynamic product landscape, with continuous innovation focused on enhancing performance and expanding applications. Key product advancements include the development of compostable packaging films with improved barrier properties, extending the shelf life of perishable goods. Companies are also innovating in biodegradable rigid packaging for electronics and consumer goods, offering alternatives to plastic clamshells and trays. Unique selling propositions often revolve around certified compostability, recyclability, and the use of plant-based or renewable resources. Technological advancements are enabling the creation of biodegradable packaging with enhanced printability, durability, and moisture resistance, meeting diverse industry needs.

Key Drivers, Barriers & Challenges in Biodegradable Packaging Solutions Industry

The biodegradable packaging solutions industry is propelled by several key drivers, including increasing global awareness of plastic pollution and its detrimental environmental impact. Stringent government regulations worldwide, such as bans on single-use plastics and incentives for sustainable packaging materials, are significantly accelerating market adoption. Furthermore, growing consumer preference for eco-friendly products and corporate sustainability initiatives are creating substantial demand for biodegradable packaging alternatives.

However, several barriers and challenges impede the widespread adoption of biodegradable packaging. High production costs compared to conventional plastics remain a significant restraint, impacting price competitiveness. Limited consumer awareness and confusion regarding the proper disposal of biodegradable packaging (e.g., industrial vs. home composting) can lead to improper waste management and a reduced environmental benefit. Supply chain complexities and the need for specialized infrastructure for composting and recycling also present hurdles. Competitive pressures from the established and cost-effective conventional plastic market continue to pose a challenge.

Key Drivers:

- Environmental concerns and plastic pollution awareness.

- Supportive government policies and regulations.

- Growing consumer demand for sustainable packaging.

- Corporate social responsibility and sustainability targets.

Key Barriers & Challenges:

- Higher production costs and price sensitivity.

- Consumer education and proper disposal infrastructure.

- Performance limitations (e.g., barrier properties) in some applications.

- Supply chain integration and scalability.

- Competition from conventional plastic packaging.

Emerging Opportunities in Biodegradable Packaging Solutions Industry

Emerging opportunities within the biodegradable packaging solutions industry are abundant and span across various sectors. The growth of e-commerce presents a significant opportunity for sustainable shipping solutions, including biodegradable mailers and protective packaging. The food service industry is actively seeking compostable takeaway containers and cutlery to meet regulatory demands and consumer expectations. Furthermore, advancements in material science are unlocking new applications for biodegradable packaging in sectors like electronics and medical devices. Evolving consumer preferences for transparency and traceability in product sourcing and packaging also create opportunities for brands that can demonstrate the sustainable origins of their eco-friendly packaging. The development of home-compostable packaging solutions further expands the market's reach beyond industrial composting facilities.

Growth Accelerators in the Biodegradable Packaging Solutions Industry Industry

Several factors are poised to act as significant growth accelerators for the biodegradable packaging solutions industry. Technological breakthroughs in biopolymer innovation, leading to enhanced performance characteristics and reduced production costs, will be a major catalyst. Strategic partnerships between material manufacturers, packaging converters, and end-user brands will streamline the adoption process and foster market expansion. The increasing global adoption of Extended Producer Responsibility (EPR) schemes, which hold producers accountable for the end-of-life management of their packaging, will incentivize the use of more sustainable materials. Market expansion into developing economies, where environmental awareness is growing and regulations are being implemented, represents another crucial growth avenue. The continued development of robust composting infrastructure will also remove a key barrier to adoption.

Key Players Shaping the Biodegradable Packaging Solutions Industry Market

- Kruger Inc

- Berkley International Packaging Limited

- Elevate Packaging Inc

- Amcor Group Gmbh

- Greenpack Limited

- Ranpak Holding Corporation

- Mondi Group

- International Paper Company

- Smurfit Kappa Group PLC

- Tetra Pak International SA

- Sealed Air Corporation

- Biopak PTY Ltd (Duni Group)

Notable Milestones in Biodegradable Packaging Solutions Industry Sector

- February 2024: TIPA launches compostable packaging with comparable durability, shelf life, barrier, transparency, and clarity to virgin plastic packaging. Certified to biodegrade in domestic or industrial compost bins, offering a plastic-free alternative for products like coffee capsules, zipper bags, mesh packaging, and resealable plastic containers. TIPA also introduced a fully compostable and recyclable rice straw container line.

- February 2024: Print & Pack officially launches to provide sustainable packaging solutions to North America’s small businesses and eco-friendly brands. Their portfolio features BDP for Biodegradable Packaging and GREENGUARD Gold Certified inks, including INVISIBLEBAG, a compostable and water-soluble solution.

In-Depth Biodegradable Packaging Solutions Industry Market Outlook

The future outlook for the biodegradable packaging solutions industry is exceptionally positive, characterized by sustained growth and increasing innovation. Key accelerators will continue to be driven by technological advancements in biopolymer development, leading to more cost-effective and high-performance eco-friendly packaging materials. Strategic alliances between stakeholders across the value chain will be crucial for market penetration and scaling production capabilities. The ongoing global implementation of robust regulatory frameworks and the growing consumer demand for sustainable products will further solidify the market's expansion. Emerging opportunities in sectors like e-commerce packaging and food service packaging will unlock new revenue streams. Investment in developing comprehensive waste management and composting infrastructure will be critical to address disposal challenges and fully realize the environmental benefits of biodegradable packaging. The market is projected to witness significant growth in applications requiring high barrier properties and enhanced shelf-life solutions.

Biodegradable Packaging Solutions Industry Segmentation

-

1. Material Type

-

1.1. Plastic

- 1.1.1. Starch-Based Plastics

- 1.1.2. Cellulose-Based Plastics

- 1.1.3. Polylactic Acid (PLA)

- 1.1.4. Poly-3-Hydroxybutyrate (PHB)

- 1.1.5. Polyhydroxyalkanoates (PHA)

-

1.2. Paper

- 1.2.1. Kraft Paper

- 1.2.2. Flexible Paper

- 1.2.3. Corrugated Fiberboard

- 1.2.4. Boxboard

-

1.1. Plastic

-

2. Application

- 2.1. Food Packaging

- 2.2. Beverage Packaging

- 2.3. Pharmaceutical Packaging

- 2.4. Personal/Homecare Packaging

- 3. Rest of the World

Biodegradable Packaging Solutions Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. Rest of Asia Pacific

Biodegradable Packaging Solutions Industry Regional Market Share

Geographic Coverage of Biodegradable Packaging Solutions Industry

Biodegradable Packaging Solutions Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.97% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Plastic

- 5.1.1.1. Starch-Based Plastics

- 5.1.1.2. Cellulose-Based Plastics

- 5.1.1.3. Polylactic Acid (PLA)

- 5.1.1.4. Poly-3-Hydroxybutyrate (PHB)

- 5.1.1.5. Polyhydroxyalkanoates (PHA)

- 5.1.2. Paper

- 5.1.2.1. Kraft Paper

- 5.1.2.2. Flexible Paper

- 5.1.2.3. Corrugated Fiberboard

- 5.1.2.4. Boxboard

- 5.1.1. Plastic

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Food Packaging

- 5.2.2. Beverage Packaging

- 5.2.3. Pharmaceutical Packaging

- 5.2.4. Personal/Homecare Packaging

- 5.3. Market Analysis, Insights and Forecast - by Rest of the World

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. Global Biodegradable Packaging Solutions Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Plastic

- 6.1.1.1. Starch-Based Plastics

- 6.1.1.2. Cellulose-Based Plastics

- 6.1.1.3. Polylactic Acid (PLA)

- 6.1.1.4. Poly-3-Hydroxybutyrate (PHB)

- 6.1.1.5. Polyhydroxyalkanoates (PHA)

- 6.1.2. Paper

- 6.1.2.1. Kraft Paper

- 6.1.2.2. Flexible Paper

- 6.1.2.3. Corrugated Fiberboard

- 6.1.2.4. Boxboard

- 6.1.1. Plastic

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Food Packaging

- 6.2.2. Beverage Packaging

- 6.2.3. Pharmaceutical Packaging

- 6.2.4. Personal/Homecare Packaging

- 6.3. Market Analysis, Insights and Forecast - by Rest of the World

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. North America Biodegradable Packaging Solutions Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 7.1.1. Plastic

- 7.1.1.1. Starch-Based Plastics

- 7.1.1.2. Cellulose-Based Plastics

- 7.1.1.3. Polylactic Acid (PLA)

- 7.1.1.4. Poly-3-Hydroxybutyrate (PHB)

- 7.1.1.5. Polyhydroxyalkanoates (PHA)

- 7.1.2. Paper

- 7.1.2.1. Kraft Paper

- 7.1.2.2. Flexible Paper

- 7.1.2.3. Corrugated Fiberboard

- 7.1.2.4. Boxboard

- 7.1.1. Plastic

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Food Packaging

- 7.2.2. Beverage Packaging

- 7.2.3. Pharmaceutical Packaging

- 7.2.4. Personal/Homecare Packaging

- 7.3. Market Analysis, Insights and Forecast - by Rest of the World

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 8. Europe Biodegradable Packaging Solutions Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 8.1.1. Plastic

- 8.1.1.1. Starch-Based Plastics

- 8.1.1.2. Cellulose-Based Plastics

- 8.1.1.3. Polylactic Acid (PLA)

- 8.1.1.4. Poly-3-Hydroxybutyrate (PHB)

- 8.1.1.5. Polyhydroxyalkanoates (PHA)

- 8.1.2. Paper

- 8.1.2.1. Kraft Paper

- 8.1.2.2. Flexible Paper

- 8.1.2.3. Corrugated Fiberboard

- 8.1.2.4. Boxboard

- 8.1.1. Plastic

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Food Packaging

- 8.2.2. Beverage Packaging

- 8.2.3. Pharmaceutical Packaging

- 8.2.4. Personal/Homecare Packaging

- 8.3. Market Analysis, Insights and Forecast - by Rest of the World

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 9. Asia Pacific Biodegradable Packaging Solutions Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 9.1.1. Plastic

- 9.1.1.1. Starch-Based Plastics

- 9.1.1.2. Cellulose-Based Plastics

- 9.1.1.3. Polylactic Acid (PLA)

- 9.1.1.4. Poly-3-Hydroxybutyrate (PHB)

- 9.1.1.5. Polyhydroxyalkanoates (PHA)

- 9.1.2. Paper

- 9.1.2.1. Kraft Paper

- 9.1.2.2. Flexible Paper

- 9.1.2.3. Corrugated Fiberboard

- 9.1.2.4. Boxboard

- 9.1.1. Plastic

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Food Packaging

- 9.2.2. Beverage Packaging

- 9.2.3. Pharmaceutical Packaging

- 9.2.4. Personal/Homecare Packaging

- 9.3. Market Analysis, Insights and Forecast - by Rest of the World

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Kruger Inc

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Berkley International Packaging Limited

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Elevate Packaging Inc

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Amcor Group Gmbh

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Greenpack Limited

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Ranpak Holding Corporation*List Not Exhaustive

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Mondi Group

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 International Paper Company

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Smurfit Kappa Group PLC

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 Tetra Pak International SA

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.11 Sealed Air Corporation

- 10.1.11.1. Company Overview

- 10.1.11.2. Products

- 10.1.11.3. Company Financials

- 10.1.11.4. SWOT Analysis

- 10.1.12 Biopak PTY Ltd (Duni Group)

- 10.1.12.1. Company Overview

- 10.1.12.2. Products

- 10.1.12.3. Company Financials

- 10.1.12.4. SWOT Analysis

- 10.1.1 Kruger Inc

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: Global Biodegradable Packaging Solutions Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Biodegradable Packaging Solutions Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 3: North America Biodegradable Packaging Solutions Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 4: North America Biodegradable Packaging Solutions Industry Revenue (Million), by Application 2025 & 2033

- Figure 5: North America Biodegradable Packaging Solutions Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Biodegradable Packaging Solutions Industry Revenue (Million), by Rest of the World 2025 & 2033

- Figure 7: North America Biodegradable Packaging Solutions Industry Revenue Share (%), by Rest of the World 2025 & 2033

- Figure 8: North America Biodegradable Packaging Solutions Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Biodegradable Packaging Solutions Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Biodegradable Packaging Solutions Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 11: Europe Biodegradable Packaging Solutions Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 12: Europe Biodegradable Packaging Solutions Industry Revenue (Million), by Application 2025 & 2033

- Figure 13: Europe Biodegradable Packaging Solutions Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: Europe Biodegradable Packaging Solutions Industry Revenue (Million), by Rest of the World 2025 & 2033

- Figure 15: Europe Biodegradable Packaging Solutions Industry Revenue Share (%), by Rest of the World 2025 & 2033

- Figure 16: Europe Biodegradable Packaging Solutions Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Biodegradable Packaging Solutions Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Biodegradable Packaging Solutions Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 19: Asia Pacific Biodegradable Packaging Solutions Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 20: Asia Pacific Biodegradable Packaging Solutions Industry Revenue (Million), by Application 2025 & 2033

- Figure 21: Asia Pacific Biodegradable Packaging Solutions Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Asia Pacific Biodegradable Packaging Solutions Industry Revenue (Million), by Rest of the World 2025 & 2033

- Figure 23: Asia Pacific Biodegradable Packaging Solutions Industry Revenue Share (%), by Rest of the World 2025 & 2033

- Figure 24: Asia Pacific Biodegradable Packaging Solutions Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific Biodegradable Packaging Solutions Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Biodegradable Packaging Solutions Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 2: Global Biodegradable Packaging Solutions Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Global Biodegradable Packaging Solutions Industry Revenue Million Forecast, by Rest of the World 2020 & 2033

- Table 4: Global Biodegradable Packaging Solutions Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Biodegradable Packaging Solutions Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 6: Global Biodegradable Packaging Solutions Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 7: Global Biodegradable Packaging Solutions Industry Revenue Million Forecast, by Rest of the World 2020 & 2033

- Table 8: Global Biodegradable Packaging Solutions Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Biodegradable Packaging Solutions Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada Biodegradable Packaging Solutions Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Global Biodegradable Packaging Solutions Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 12: Global Biodegradable Packaging Solutions Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 13: Global Biodegradable Packaging Solutions Industry Revenue Million Forecast, by Rest of the World 2020 & 2033

- Table 14: Global Biodegradable Packaging Solutions Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 15: United Kingdom Biodegradable Packaging Solutions Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Germany Biodegradable Packaging Solutions Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: France Biodegradable Packaging Solutions Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Biodegradable Packaging Solutions Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Global Biodegradable Packaging Solutions Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 20: Global Biodegradable Packaging Solutions Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 21: Global Biodegradable Packaging Solutions Industry Revenue Million Forecast, by Rest of the World 2020 & 2033

- Table 22: Global Biodegradable Packaging Solutions Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 23: China Biodegradable Packaging Solutions Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: India Biodegradable Packaging Solutions Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Japan Biodegradable Packaging Solutions Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Rest of Asia Pacific Biodegradable Packaging Solutions Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Biodegradable Packaging Solutions Industry?

The projected CAGR is approximately 5.97%.

2. Which companies are prominent players in the Biodegradable Packaging Solutions Industry?

Key companies in the market include Kruger Inc, Berkley International Packaging Limited, Elevate Packaging Inc, Amcor Group Gmbh, Greenpack Limited, Ranpak Holding Corporation*List Not Exhaustive, Mondi Group, International Paper Company, Smurfit Kappa Group PLC, Tetra Pak International SA, Sealed Air Corporation, Biopak PTY Ltd (Duni Group).

3. What are the main segments of the Biodegradable Packaging Solutions Industry?

The market segments include Material Type, Application, Rest of the World.

4. Can you provide details about the market size?

The market size is estimated to be USD 105.26 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand For Sustainable Products By Consumers And Brands; Stringent Government Regulations.

6. What are the notable trends driving market growth?

Plastic will Hold a Significant Market Share.

7. Are there any restraints impacting market growth?

Lack of Supply of Bio-plastics and Related Materials.

8. Can you provide examples of recent developments in the market?

February 2024: With the same durability, shelf life, barrier, transparency, and clarity as virgin plastic packaging, TIPA launches compostable packaging, offering an alternative to plastic packaging. Certified to biodegrade in domestic or industrial compost bins, they leave no trace in the environment and provide maximum convenience to consumers. The product range comprises coffee capsules, zipper bags, mesh packaging, and resealable plastic containers. At the same time, TIPA launched a fully compostable and recyclable rice straw container line.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Biodegradable Packaging Solutions Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Biodegradable Packaging Solutions Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Biodegradable Packaging Solutions Industry?

To stay informed about further developments, trends, and reports in the Biodegradable Packaging Solutions Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence