Key Insights

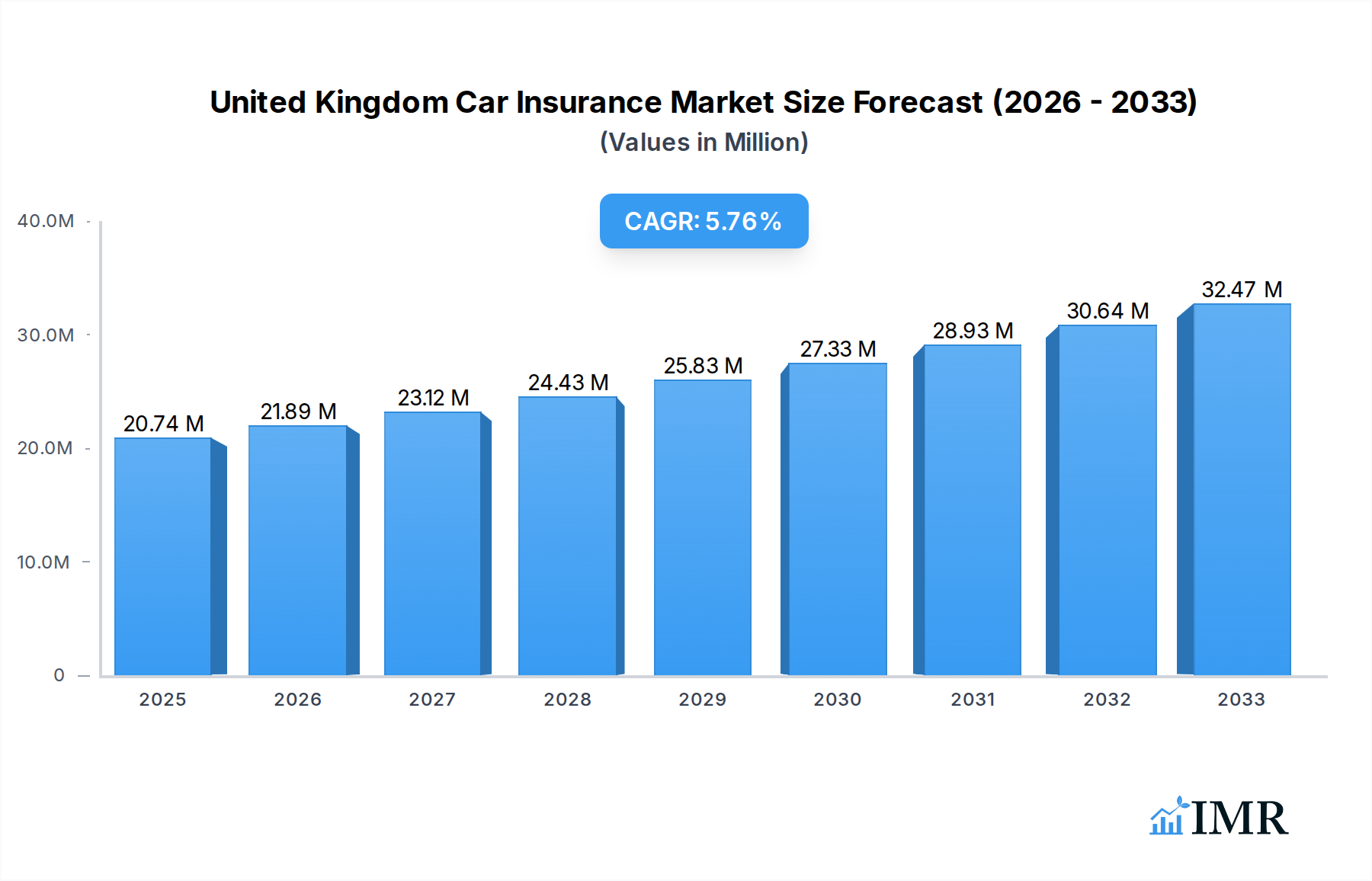

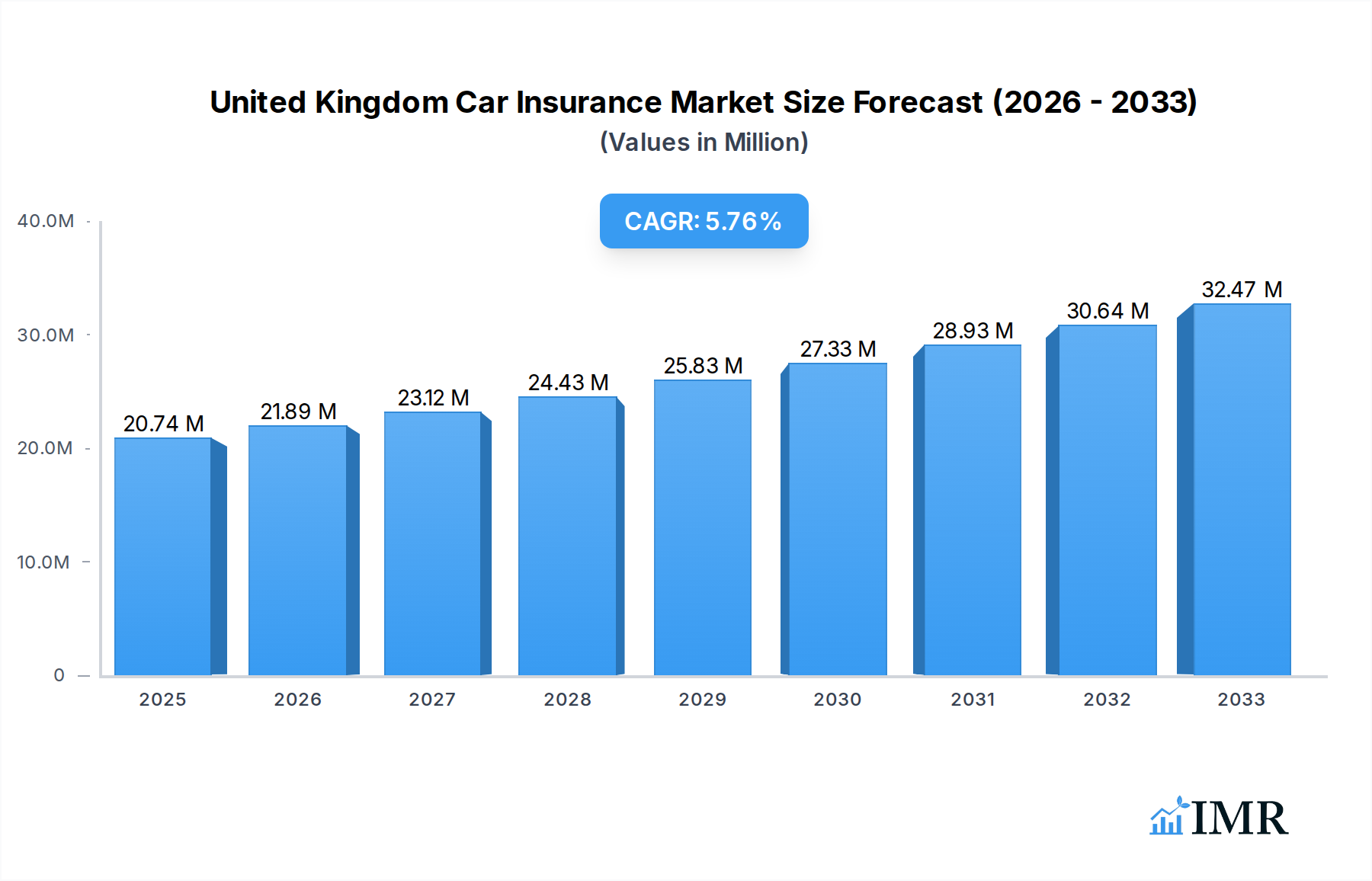

The United Kingdom car insurance market is poised for robust growth, with a **market size of *20.74* million** in the base year 2025, and projected to expand at a Compound Annual Growth Rate (CAGR) of 5.52% throughout the forecast period of 2025-2033. This expansion is driven by a confluence of factors, including the persistent need for mandatory third-party liability coverage, alongside increasing consumer demand for comprehensive and collision protection. The market's dynamism is further fueled by evolving consumer preferences and technological advancements impacting the application of insurance across personal and commercial vehicles. The diverse distribution channels, ranging from direct sales and individual agents to an increasing reliance on online platforms and brokers, are all contributing to wider accessibility and competitive pricing, thereby stimulating market penetration.

United Kingdom Car Insurance Market Market Size (In Million)

Key trends shaping the UK car insurance landscape include the growing adoption of telematics and usage-based insurance (UBI) models, which offer personalized premiums based on driving behavior, promoting safer driving habits and cost savings for consumers. The increasing prevalence of electric vehicles (EVs) and advanced driver-assistance systems (ADAS) also presents unique opportunities and challenges, necessitating specialized coverage options. However, the market faces certain restraints, such as the intensifying competition among established players like Ageas, LV= General Insurance, Aviva, Hastings, NFU Mutual, RSA, Axa, Esure, Direct Line Group, and Admiral Group, which can put pressure on profit margins. Regulatory changes and the potential for rising claims costs due to increased vehicle complexity and repair expenses also warrant careful consideration. Despite these challenges, the overarching trend points towards a resilient and growing market, driven by innovation and a consistent demand for essential vehicle protection.

United Kingdom Car Insurance Market Company Market Share

This in-depth report provides a definitive analysis of the United Kingdom car insurance market, covering its intricate dynamics, growth trajectories, and future outlook. We delve into the parent and child market structures, offering unparalleled insights for industry professionals, insurers, brokers, and investors. The study encompasses a comprehensive Study Period of 2019–2033, with 2025 serving as both the Base Year and Estimated Year, and a detailed Forecast Period of 2025–2033, complemented by a robust Historical Period of 2019–2024. All values are presented in Million units.

United Kingdom Car Insurance Market Market Dynamics & Structure

The United Kingdom car insurance market exhibits a moderately concentrated structure, with major players like Admiral Group, Aviva, and Direct Line Group holding significant market shares. Technological innovation, driven by advancements in telematics, AI-powered claims processing, and digital distribution platforms, is a key disruptor. Regulatory frameworks, including the FCA's pricing and transparency rules, significantly influence market operations. Competitive product substitutes, such as pay-as-you-drive policies and usage-based insurance, are gaining traction among evolving end-user demographics. Mergers and acquisitions (M&A) continue to shape the competitive landscape, with approximately 5-7 significant M&A deals anticipated within the forecast period. Innovation barriers include the cost of implementing new technologies and navigating complex regulatory approvals.

- Market Concentration: Moderate, with a few key players dominating market share.

- Technological Innovation Drivers: Telematics, AI for claims, digital platforms.

- Regulatory Frameworks: FCA pricing and transparency rules.

- Competitive Product Substitutes: Pay-as-you-drive, usage-based insurance.

- End-User Demographics: Shifting towards digital-first consumers, younger demographics seeking flexible options.

- M&A Trends: Ongoing consolidation to enhance market position and expand product portfolios.

United Kingdom Car Insurance Market Growth Trends & Insights

The United Kingdom car insurance market is poised for sustained growth, driven by increasing vehicle parc, evolving consumer needs, and innovative product offerings. The market is projected to experience a Compound Annual Growth Rate (CAGR) of approximately 3-5% over the forecast period, reaching an estimated market size of £XX,XXX Million by 2033. Adoption rates for digital insurance platforms are accelerating, with over 60% of new policies expected to be purchased online by 2028. Technological disruptions, such as the integration of IoT devices for risk assessment and the development of advanced driver-assistance systems (ADAS), are reshaping underwriting and pricing models. Consumer behavior shifts, including a greater emphasis on value, transparency, and personalized insurance solutions, are prompting insurers to adapt their strategies. The market penetration for comprehensive coverage is expected to rise, reflecting a growing consumer demand for broader protection.

Dominant Regions, Countries, or Segments in United Kingdom Car Insurance Market

Personal Vehicles represent the dominant segment within the United Kingdom car insurance market, accounting for over 85% of the total market value in 2025. This dominance is driven by the large and consistently growing private car ownership across the nation. Within the coverage segment, Collision/Comprehensive/Other Optional Coverage is the primary revenue generator, reflecting consumer preference for more extensive protection beyond basic legal requirements. The Online distribution channel is witnessing the most rapid growth, projected to capture over 45% of new policy sales by 2028, owing to its convenience and competitive pricing. Key drivers for the personal vehicle segment include ongoing economic stability, high car ownership rates, and a well-established infrastructure for vehicle maintenance and repair. London and the South East of England remain dominant regions due to higher population density and vehicle density.

- Dominant Application: Personal Vehicles.

- Dominant Coverage: Collision/Comprehensive/Other Optional Coverage.

- Dominant Distribution Channel: Online.

- Key Drivers for Personal Vehicles: High car ownership, economic factors, established infrastructure.

- Growth Potential in Online Distribution: Increasing digital adoption and competitive pricing.

United Kingdom Car Insurance Market Product Landscape

The United Kingdom car insurance product landscape is characterized by continuous innovation, focusing on customer-centricity and technological integration. Insurers are introducing a range of optional add-ons, such as breakdown cover, legal protection, and courtesy car provisions, to cater to diverse consumer needs. Telematics-enabled policies, offering personalized pricing based on driving behavior, are gaining traction, especially among younger drivers. The application of AI in claims processing is streamlining the customer experience, reducing settlement times and improving accuracy. Performance metrics like customer satisfaction scores and claims settlement ratios are becoming crucial differentiators.

Key Drivers, Barriers & Challenges in United Kingdom Car Insurance Market

Key Drivers:

- Technological Advancements: Telematics, AI, and digital platforms enhance efficiency and customer experience.

- Economic Factors: Rising disposable incomes and stable economic conditions support car ownership and insurance uptake.

- Regulatory Support: Evolving regulations often push for greater transparency and consumer protection, fostering trust.

- Increasing Vehicle Parc: A growing number of vehicles on the road directly translates to a larger insurance market.

Barriers & Challenges:

- Regulatory Hurdles: Strict compliance requirements and evolving consumer protection laws can increase operational costs.

- Intense Competition: A saturated market with numerous providers leads to price wars and margin compression, estimated to impact profitability by 5-7%.

- Fraudulent Claims: The persistent issue of insurance fraud adds to claims costs, estimated at £X,XXX Million annually.

- Economic Downturns: Recessions can lead to reduced disposable income, impacting insurance affordability.

- Supply Chain Issues: Disruptions in vehicle repair and parts availability can prolong claims and increase costs.

Emerging Opportunities in United Kingdom Car Insurance Market

Emerging opportunities lie in the expansion of usage-based insurance (UBI) models, particularly for commercial fleets and younger drivers, leveraging telematics data for dynamic pricing. The integration of insurance with broader mobility services and electric vehicle (EV) specific insurance products presents a significant untapped market. Furthermore, personalized insurance packages tailored to individual driving habits and risk profiles, facilitated by AI and data analytics, offer a strong avenue for differentiation and customer loyalty. The growing demand for cyber insurance add-ons for connected vehicles also represents a nascent but promising area.

Growth Accelerators in the United Kingdom Car Insurance Market Industry

Long-term growth in the United Kingdom car insurance industry will be significantly accelerated by the widespread adoption of Artificial Intelligence and Machine Learning across the value chain, from underwriting to claims automation. Strategic partnerships between insurers, technology providers, and automotive manufacturers will foster innovation in connected car insurance and risk management solutions. Market expansion strategies, including entering niche segments like ride-sharing insurance and exploring micro-insurance options, will also contribute to sustained growth. The development of more sophisticated data analytics capabilities will enable insurers to offer highly personalized and competitive products.

Key Players Shaping the United Kingdom Car Insurance Market Market

- Ageas

- LV= General Insurance

- Aviva

- Hastings

- NFU Mutual

- RSA

- Axa

- Esure

- Direct Line Group

- Admiral Group

Notable Milestones in United Kingdom Car Insurance Market Sector

- October 2023: ARAG SE agreed to supply vehicle hire insurance for Hastings Direct, an optional add-on for over a million Hastings Direct motor insurance customers. This partnership aims to enhance customer offerings and provide greater flexibility.

- December 2022: Covea Insurance and BGL Insurance (BGLi) partnered to introduce Nutshell, a new car insurance brand in the United Kingdom designed to deliver significant benefits for vehicle users through a modern and customer-centric approach.

In-Depth United Kingdom Car Insurance Market Market Outlook

The United Kingdom car insurance market outlook is characterized by robust growth potential driven by technological innovation and evolving consumer demands. The increasing adoption of telematics, AI, and digital platforms will continue to enhance operational efficiencies and personalize customer experiences. Strategic collaborations and the development of niche insurance products, particularly for electric vehicles and ride-sharing services, will unlock new revenue streams. Insurers that can effectively leverage data analytics to offer competitive pricing and tailored solutions will be best positioned to capitalize on the evolving market landscape and achieve sustained growth in the coming years. The market is projected to see continued consolidation and innovation, shaping a more dynamic and customer-focused insurance sector.

United Kingdom Car Insurance Market Segmentation

-

1. Coverage

- 1.1. Third-Party Liability Coverage

- 1.2. Collision/Comprehensive/Other Optional Coverage

-

2. Application

- 2.1. Personal Vehicles

- 2.2. Commercial Vehicles

-

3. Distribution Channel

- 3.1. Direct Sales

- 3.2. Individual Agents

- 3.3. Brokers

- 3.4. Banks

- 3.5. Online

- 3.6. Other Distribution Channels

United Kingdom Car Insurance Market Segmentation By Geography

- 1. United Kingdom

United Kingdom Car Insurance Market Regional Market Share

Geographic Coverage of United Kingdom Car Insurance Market

United Kingdom Car Insurance Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.52% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Coverage

- 5.1.1. Third-Party Liability Coverage

- 5.1.2. Collision/Comprehensive/Other Optional Coverage

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Personal Vehicles

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Direct Sales

- 5.3.2. Individual Agents

- 5.3.3. Brokers

- 5.3.4. Banks

- 5.3.5. Online

- 5.3.6. Other Distribution Channels

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United Kingdom

- 5.1. Market Analysis, Insights and Forecast - by Coverage

- 6. United Kingdom Car Insurance Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Coverage

- 6.1.1. Third-Party Liability Coverage

- 6.1.2. Collision/Comprehensive/Other Optional Coverage

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Personal Vehicles

- 6.2.2. Commercial Vehicles

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Direct Sales

- 6.3.2. Individual Agents

- 6.3.3. Brokers

- 6.3.4. Banks

- 6.3.5. Online

- 6.3.6. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Coverage

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Ageas

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 LV= General Insurance

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Aviva

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Hastings

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 NFU Mutual**List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 RSA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Axa

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Esure

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Direct Line Group

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Admiral Group

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Ageas

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United Kingdom Car Insurance Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: United Kingdom Car Insurance Market Share (%) by Company 2025

List of Tables

- Table 1: United Kingdom Car Insurance Market Revenue Million Forecast, by Coverage 2020 & 2033

- Table 2: United Kingdom Car Insurance Market Revenue Million Forecast, by Application 2020 & 2033

- Table 3: United Kingdom Car Insurance Market Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 4: United Kingdom Car Insurance Market Revenue Million Forecast, by Region 2020 & 2033

- Table 5: United Kingdom Car Insurance Market Revenue Million Forecast, by Coverage 2020 & 2033

- Table 6: United Kingdom Car Insurance Market Revenue Million Forecast, by Application 2020 & 2033

- Table 7: United Kingdom Car Insurance Market Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 8: United Kingdom Car Insurance Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United Kingdom Car Insurance Market?

The projected CAGR is approximately 5.52%.

2. Which companies are prominent players in the United Kingdom Car Insurance Market?

Key companies in the market include Ageas, LV= General Insurance, Aviva, Hastings, NFU Mutual**List Not Exhaustive, RSA, Axa, Esure, Direct Line Group, Admiral Group.

3. What are the main segments of the United Kingdom Car Insurance Market?

The market segments include Coverage, Application, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 20.74 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of Innovative Tracking Technologies.

6. What are the notable trends driving market growth?

Growth of Car Sales as Demand for Electric Car in United Kingdom.

7. Are there any restraints impacting market growth?

Rising Competition of Banks with Fintech and Financial Services.

8. Can you provide examples of recent developments in the market?

October 2023: ARAG SE agreed to supply vehicle hire insurance for Hastings Direct. The vehicle hire insurance policy will be offered to over a million Hastings Direct motor insurance customers as an optional add-on to their primary motor policy.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United Kingdom Car Insurance Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United Kingdom Car Insurance Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United Kingdom Car Insurance Market?

To stay informed about further developments, trends, and reports in the United Kingdom Car Insurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence