Key Insights

The Middle East and Africa (MEA) private equity fund industry is poised for significant expansion, with a projected Compound Annual Growth Rate (CAGR) of 6.41% from 2025 to 2033. This robust growth is propelled by several key factors. Sovereign wealth funds are actively deploying capital across diverse sectors, fostering investment. A thriving entrepreneurial landscape, coupled with governmental support for startups and SMEs, is generating a strong pipeline of investment opportunities. The region's strategic geographic position as a conduit between Asia, Europe, and Africa further enhances its appeal to international investors seeking diversification and superior returns. Additionally, ongoing infrastructure development projects across MEA are creating substantial demand for private equity capital.

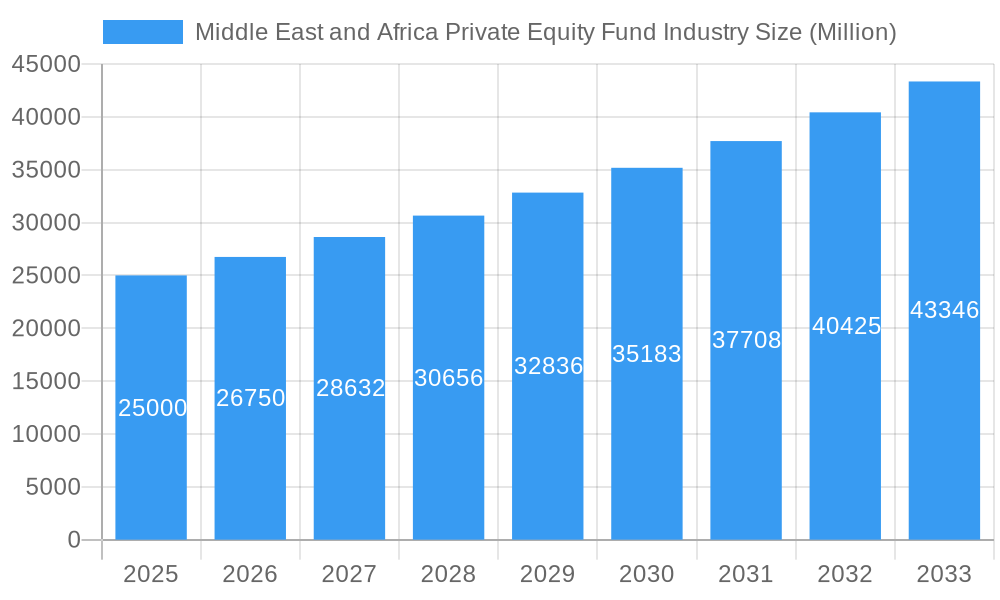

Middle East and Africa Private Equity Fund Industry Market Size (In Billion)

However, the industry navigates certain challenges. Geopolitical instability in specific areas can introduce investment uncertainty. Varying regulatory frameworks across nations can increase operational complexity and compliance burdens for fund managers. Competition from alternative asset classes, such as real estate and infrastructure funds, also presents a notable challenge. Notwithstanding these headwinds, the MEA private equity fund industry maintains a positive long-term outlook, underpinned by sustained economic growth, expanding institutional investor involvement, and the region's pivotal role in the global economy. The market size in 2025 is estimated at $21063.4 million, representing a substantial foundation for future expansion at the projected 6.41% CAGR.

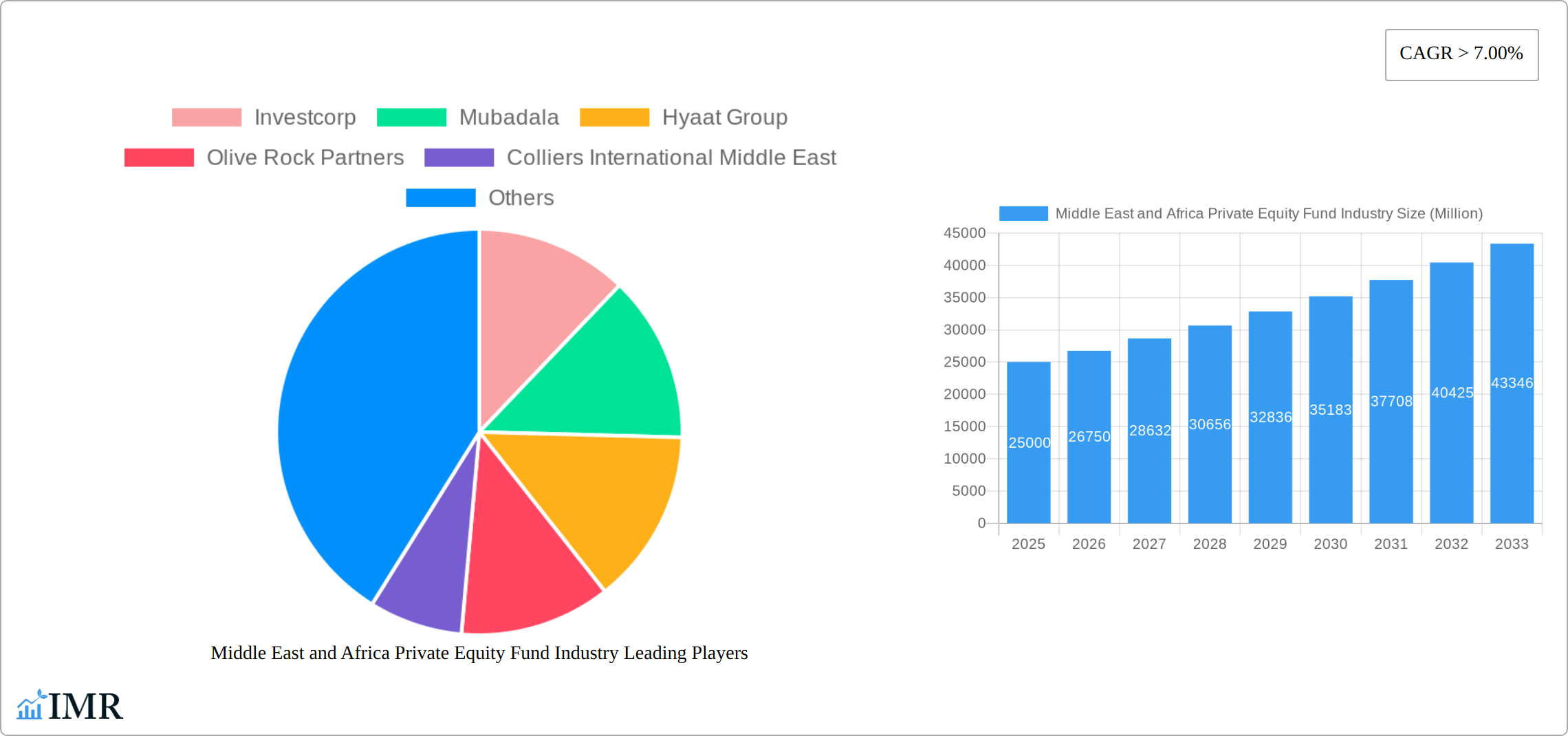

Middle East and Africa Private Equity Fund Industry Company Market Share

This comprehensive report delivers an in-depth analysis of the Middle East and Africa Private Equity Fund industry, providing crucial insights for investors, industry professionals, and strategic decision-makers. The analysis spans the period 2019-2033, with a strategic focus on the base year 2025 and a forecast period from 2025-2033. Employing extensive data analytics and expert perspectives, this report highlights market dynamics, growth trajectories, key stakeholders, and emerging opportunities within this dynamic sector. The granular analysis covers essential segments and geographies, facilitating informed strategic planning and investment decisions.

Middle East and Africa Private Equity Fund Industry Market Dynamics & Structure

This section delves into the intricate competitive landscape of the Middle East and Africa (MEA) private equity fund industry. It examines key structural elements including market concentration, the impact of technological advancements, the evolving regulatory environments, and significant merger and acquisition (M&A) activities. Our analysis employs a blend of quantitative data and qualitative insights to offer a comprehensive and nuanced understanding of the industry's current structure and its trajectory.

- Market Concentration: The MEA private equity market currently displays a moderate level of concentration. Prominent players such as Investcorp and Mubadala command substantial market share, while a multitude of smaller firms actively vie for deal opportunities. Preliminary indications suggest an ongoing trend towards consolidation, with the top 5 entities collectively holding approximately xx% of the market share, a figure that warrants close observation.

- Technological Innovation: The integration of financial technology (Fintech) is proving to be a significant catalyst for enhancing efficiency across the entire investment lifecycle, from deal sourcing and due diligence to portfolio management. However, the widespread adoption of these innovations remains somewhat uneven across the diverse MEA region. This disparity is largely attributed to existing infrastructure gaps and varying levels of digital literacy among stakeholders.

- Regulatory Framework: The distinct and often varied regulatory landscapes present across different MEA countries create a complex interplay of both opportunities and challenges for private equity firms. Initiatives aimed at streamlining regulations and harmonizing standards are proving to be critical determinants of sustained market growth and investor confidence.

- Competitive Substitutes: Private equity funds face competition for capital allocation from a range of alternative investment vehicles, most notably debt financing. The relative attractiveness and accessibility of these alternative options can significantly influence investment flows into the private equity sector, requiring PE firms to continually demonstrate their unique value proposition.

- End-User Demographics: The target companies for private equity investments are highly diversified, spanning a broad spectrum of industries. These include burgeoning sectors like real estate, healthcare, technology, and consumer goods. The investment appetite for companies within these segments is intrinsically linked to prevailing market conditions and specific industry growth drivers.

- M&A Trends: Between 2019 and 2024, the MEA region has been a hub of considerable M&A activity within the private equity sector, with approximately xx significant deals recorded. This robust activity underscores a strong focus on strategic consolidation and market expansion. The average deal value during this period stood at an estimated xx million per transaction, reflecting the scale of investments being made.

Middle East and Africa Private Equity Fund Industry Growth Trends & Insights

This section delivers a comprehensive analysis of market size evolution, adoption rates, and key trends shaping the MEA private equity fund industry’s growth trajectory from 2019 to 2033. Data-driven insights, including compound annual growth rate (CAGR), provide a clear picture of market dynamics.

The MEA private equity market witnessed significant growth during 2019-2024, with the market size expanding from xx million in 2019 to xx million in 2024. This growth is expected to continue, driven by factors such as increasing institutional investor participation, a growing number of investable companies, and supportive government policies in key markets. The projected CAGR for the 2025-2033 period is estimated at xx%, indicating robust future growth. This expansion reflects a rising preference for private equity as an asset class among both regional and international investors. Technological disruptions, such as the rise of fintech platforms, are streamlining operations, while shifts in consumer behavior are influencing investment strategies towards sectors such as sustainable energy and technology. Market penetration is gradually increasing, but significant untapped potential remains across various sectors and geographies in the MEA region.

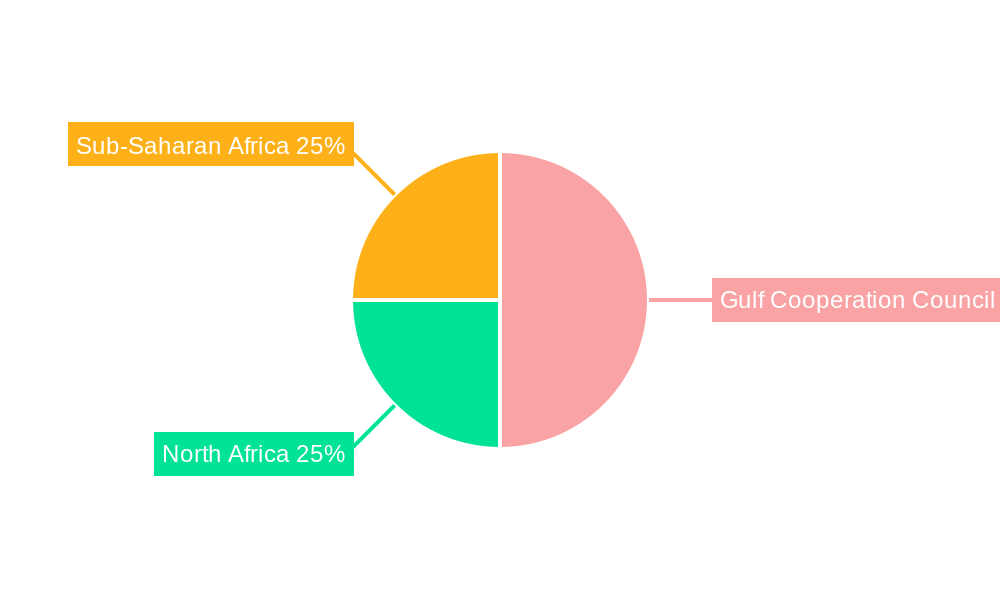

Dominant Regions, Countries, or Segments in Middle East and Africa Private Equity Fund Industry

This section meticulously identifies the leading regions, countries, and industry segments that are currently spearheading the growth and development of the MEA private equity fund industry. A detailed analysis of the pivotal factors contributing to their pronounced dominance is thoroughly explored.

- UAE and South Africa: As of 2024, the United Arab Emirates (UAE) and South Africa stand out as the most dominant markets within the MEA private equity landscape. Collectively, these nations account for approximately xx% of the total market value, a position bolstered by their robust economic foundations, forward-thinking regulatory frameworks, and relatively advanced financial infrastructures.

- Key Drivers: The overarching growth of the MEA private equity industry is propelled by a confluence of factors. These include sustained strong economic expansion across several key MEA nations, proactive government policies designed to foster private sector investment, a steadily increasing availability of viable investment-ready companies, and a growing pool of sophisticated institutional investors actively seeking compelling opportunities.

- Market Share and Growth Potential: While the UAE and South Africa currently hold a commanding market share, the horizon reveals substantial growth potential in emerging markets. Regions such as East Africa (with key players like Kenya and Ethiopia) and North Africa (including Egypt and Morocco) are experiencing rapid economic development and a surge in entrepreneurial activity. The anticipated expansion of private equity operations into these promising regions is set to significantly diversify the overall market, offering new avenues for investment and returns.

Middle East and Africa Private Equity Fund Industry Product Landscape

This section provides a concise overview of the product innovations, applications, and performance metrics within the MEA private equity fund industry. The discussion highlights unique selling propositions and technological advancements.

Private equity funds in the MEA region offer a range of investment strategies, from growth capital to leveraged buyouts and distressed debt investments. Recent innovations include the incorporation of ESG (Environmental, Social, and Governance) factors into investment decisions, as well as a focus on developing specialized funds targeting specific sectors. The industry is rapidly adopting technology to improve efficiency and transparency in fund management and portfolio tracking, resulting in enhanced returns and reduced operational costs.

Key Drivers, Barriers & Challenges in Middle East and Africa Private Equity Fund Industry

This section systematically outlines both the propelling forces that are driving the MEA private equity fund industry forward and the significant restraining factors that present hurdles to its expansion.

Key Drivers: The market's expansion is significantly fueled by a substantial increase in Foreign Direct Investment (FDI) into the region. This is complemented by the burgeoning growth of domestic capital markets and a rising number of high-growth companies seeking private equity backing. Furthermore, supportive government initiatives aimed at nurturing and developing the private sector are critically enhancing the region's attractiveness for private equity investments.

Key Challenges: A primary challenge arises from the inherent complexities and inconsistencies within the regulatory frameworks across the diverse MEA countries, creating significant operational hurdles for private equity firms. The scarcity of experienced management talent and a persistent lack of readily accessible and reliable information on potential investment targets are other key obstacles that need to be effectively addressed. Geopolitical risks, a perpetual concern in the region, continue to significantly impact investor confidence and shape investment decisions. Moreover, for some smaller private equity firms, access to adequate and appropriate financing remains a persistent challenge. The ripple effects of supply chain disruptions, particularly in the wake of global events, have also presented challenges to achieving optimal investment returns.

Emerging Opportunities in Middle East and Africa Private Equity Fund Industry

This section highlights emerging trends and untapped opportunities within the MEA private equity fund industry.

The growing adoption of technology and the rise of the gig economy present promising investment opportunities. The focus on sustainable investments, aligned with ESG principles, is also gaining traction. Untapped markets in underserved sectors, such as renewable energy and agribusiness, offer significant growth potential. Furthermore, the expansion of private equity into less-developed regions within the MEA region creates considerable opportunity.

Growth Accelerators in the Middle East and Africa Private Equity Fund Industry Industry

This section details the catalysts that will drive long-term growth within the MEA private equity fund industry.

Strategic partnerships between regional and international private equity firms are expected to accelerate market expansion. Technological advancements in fund management and portfolio monitoring enhance operational efficiency. The increased focus on ESG investing and the development of specialized sector funds also promise to boost industry growth. Furthermore, a more supportive regulatory environment across the region will enable a more favorable investment climate.

Key Players Shaping the Middle East and Africa Private Equity Fund Industry Market

- Investcorp

- Mubadala

- Hyatt Group

- Olive Rock Partners

- Colliers International Middle East

- Ascension Capital Partners

- Saint Capital Fund

- BluePeak Private Capital

- Sigma Capital Holding

- Vantage Capital

Notable Milestones in Middle East and Africa Private Equity Fund Industry Sector

- January 2022: Colliers International significantly expanded its presence in the Middle East and North Africa (MENA) region through the strategic acquisition of Falcon Investments LLC by Eltizam Asset Management Group, signaling consolidation and growth within the real estate services sector.

- January 2022: BluePeak Private Capital made a strategic investment in Grit Real Estate Income Group Limited, a move that is set to bolster industrial and healthcare infrastructure development across key East African markets, highlighting a focus on essential sectors.

In-Depth Middle East and Africa Private Equity Fund Industry Market Outlook

The private equity fund industry in the Middle East and Africa is confidently positioned for sustained and robust growth throughout the foreseeable forecast period. This optimistic outlook is underpinned by strategic and targeted investments in key growth sectors, further amplified by supportive government policies and an increasing influx of institutional investor participation, all of which will collectively drive significant market expansion. The progressive integration of cutting-edge technology and a heightened, more pronounced focus on Environmental, Social, and Governance (ESG) considerations are set to profoundly shape the industry's future trajectory, thereby creating compelling opportunities for both established, seasoned players and agile new entrants. Furthermore, the continuously expanding middle class across the region, coupled with an escalating demand for consumer goods and services, will continue to act as a powerful magnet, attracting substantial investment into various sectors of the economy.

Middle East and Africa Private Equity Fund Industry Segmentation

-

1. Industry / Sector

- 1.1. Utilities

- 1.2. Oil & Gas

- 1.3. Financials

- 1.4. Technology

- 1.5. Healthcare

- 1.6. Consumer Goods & Services

- 1.7. Others

-

2. Investment Type

- 2.1. Venture Capital

- 2.2. Growth

- 2.3. Buyout

- 2.4. Others

Middle East and Africa Private Equity Fund Industry Segmentation By Geography

-

1. Middle East

- 1.1. Saudi Arabia

- 1.2. United Arab Emirates

- 1.3. Israel

- 1.4. Qatar

- 1.5. Kuwait

- 1.6. Oman

- 1.7. Bahrain

- 1.8. Jordan

- 1.9. Lebanon

Middle East and Africa Private Equity Fund Industry Regional Market Share

Geographic Coverage of Middle East and Africa Private Equity Fund Industry

Middle East and Africa Private Equity Fund Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.41% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Industry / Sector

- 5.1.1. Utilities

- 5.1.2. Oil & Gas

- 5.1.3. Financials

- 5.1.4. Technology

- 5.1.5. Healthcare

- 5.1.6. Consumer Goods & Services

- 5.1.7. Others

- 5.2. Market Analysis, Insights and Forecast - by Investment Type

- 5.2.1. Venture Capital

- 5.2.2. Growth

- 5.2.3. Buyout

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Industry / Sector

- 6. Middle East and Africa Private Equity Fund Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Industry / Sector

- 6.1.1. Utilities

- 6.1.2. Oil & Gas

- 6.1.3. Financials

- 6.1.4. Technology

- 6.1.5. Healthcare

- 6.1.6. Consumer Goods & Services

- 6.1.7. Others

- 6.2. Market Analysis, Insights and Forecast - by Investment Type

- 6.2.1. Venture Capital

- 6.2.2. Growth

- 6.2.3. Buyout

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Industry / Sector

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Investcorp

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Mubadala

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Hyaat Group

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Olive Rock Partners

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Colliers International Middle East

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Ascension Capital Partners

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Saint Capital Fund

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 BluePeak Private Capital

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Sigma Capital Holding

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Vantage Capital**List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Investcorp

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Middle East and Africa Private Equity Fund Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Middle East and Africa Private Equity Fund Industry Share (%) by Company 2025

List of Tables

- Table 1: Middle East and Africa Private Equity Fund Industry Revenue million Forecast, by Industry / Sector 2020 & 2033

- Table 2: Middle East and Africa Private Equity Fund Industry Revenue million Forecast, by Investment Type 2020 & 2033

- Table 3: Middle East and Africa Private Equity Fund Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: Middle East and Africa Private Equity Fund Industry Revenue million Forecast, by Industry / Sector 2020 & 2033

- Table 5: Middle East and Africa Private Equity Fund Industry Revenue million Forecast, by Investment Type 2020 & 2033

- Table 6: Middle East and Africa Private Equity Fund Industry Revenue million Forecast, by Country 2020 & 2033

- Table 7: Saudi Arabia Middle East and Africa Private Equity Fund Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: United Arab Emirates Middle East and Africa Private Equity Fund Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Israel Middle East and Africa Private Equity Fund Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Qatar Middle East and Africa Private Equity Fund Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 11: Kuwait Middle East and Africa Private Equity Fund Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 12: Oman Middle East and Africa Private Equity Fund Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 13: Bahrain Middle East and Africa Private Equity Fund Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Jordan Middle East and Africa Private Equity Fund Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Lebanon Middle East and Africa Private Equity Fund Industry Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East and Africa Private Equity Fund Industry?

The projected CAGR is approximately 6.41%.

2. Which companies are prominent players in the Middle East and Africa Private Equity Fund Industry?

Key companies in the market include Investcorp, Mubadala, Hyaat Group, Olive Rock Partners, Colliers International Middle East, Ascension Capital Partners, Saint Capital Fund, BluePeak Private Capital, Sigma Capital Holding, Vantage Capital**List Not Exhaustive.

3. What are the main segments of the Middle East and Africa Private Equity Fund Industry?

The market segments include Industry / Sector, Investment Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 21063.4 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Increase in Capital Deployment in Africa.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

In Jan 2022, Colliers, a services and investment management firm, improved its footprint in the Middle East and North Africa (MENA) with Eltizam Asset Management Group's (Eltizam) acquisition of Falcon Investments LLC, an associate partner that has been doing business in the region as Colliers since 1995. Colliers benefits from the competence in core real estate transactions and advisory services offered by Eltizam and the asset management services.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East and Africa Private Equity Fund Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East and Africa Private Equity Fund Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East and Africa Private Equity Fund Industry?

To stay informed about further developments, trends, and reports in the Middle East and Africa Private Equity Fund Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence