Key Insights

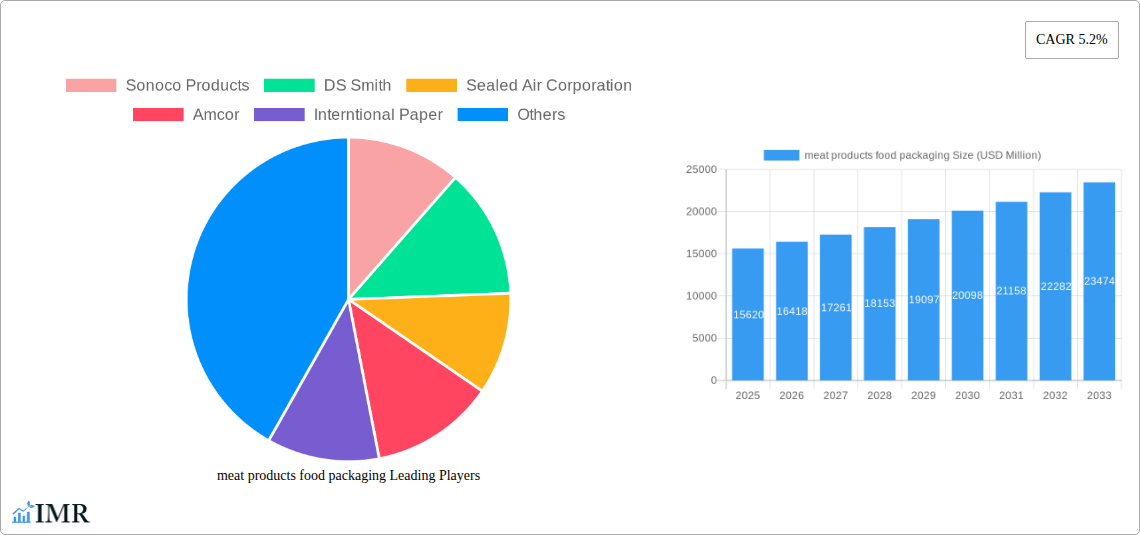

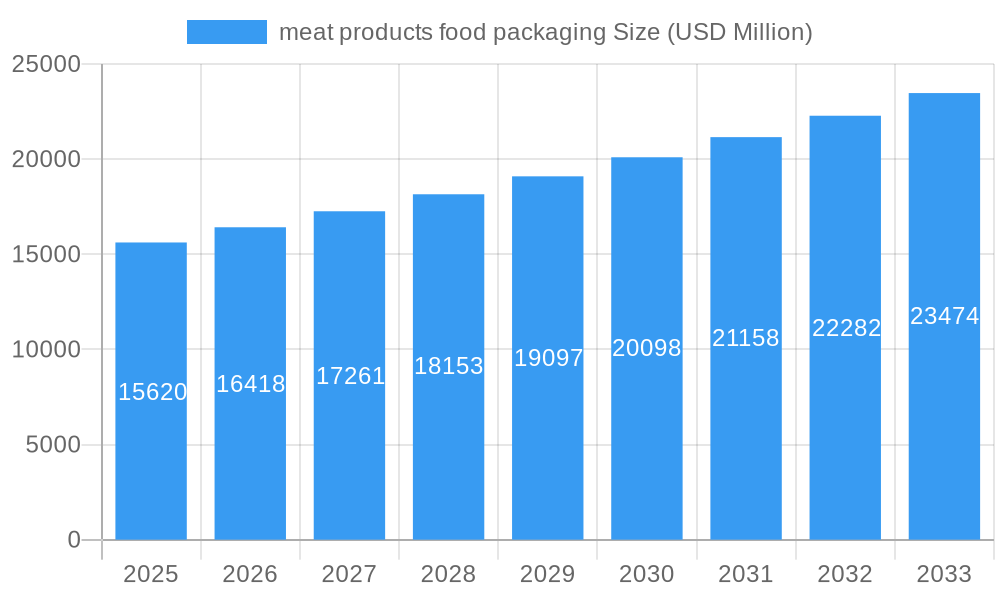

The global meat products food packaging market is poised for substantial growth, projected to reach USD 15.62 billion in 2025. This expansion is driven by an estimated Compound Annual Growth Rate (CAGR) of 5.2% over the forecast period of 2025-2033. The increasing global demand for convenient and safely packaged meat products, coupled with rising disposable incomes and evolving consumer lifestyles, are primary catalysts. Fresh meat products, in particular, are experiencing robust demand, necessitating advanced packaging solutions that ensure freshness, extend shelf life, and prevent contamination. This trend is being supported by innovations in materials science, with advancements in polymers like Polypropylene and Polyethylene, and barrier films such as BOPET, offering enhanced protection and sustainability features. Furthermore, the growing emphasis on food safety regulations and consumer awareness regarding food spoilage are compelling manufacturers to adopt high-performance packaging.

meat products food packaging Market Size (In Billion)

The market is segmented across various product types, including Polypropylene, Polyethylene, Paper, Aluminum, BOPET, Poly Vinyl Chloride, and others, catering to diverse packaging needs for fresh, frozen, and processed meat items. Key players like Amcor, Sealed Air Corporation, and DS Smith are actively investing in research and development to introduce sustainable and technologically advanced packaging solutions. This includes the development of recyclable and biodegradable materials, addressing growing environmental concerns and aligning with circular economy principles. However, the market also faces certain restraints, such as the fluctuating raw material costs and the complex regulatory landscape governing food packaging materials. Despite these challenges, the sustained demand for protein-rich diets globally, coupled with ongoing innovation in packaging technology and design, is expected to propel the meat products food packaging market to new heights, fostering a dynamic and competitive environment.

meat products food packaging Company Market Share

Unlocking the Future of Protein Preservation: A Comprehensive Report on the Meat Products Food Packaging Market

This in-depth report provides a strategic analysis of the global meat products food packaging market, a critical segment within the broader food packaging industry. Spanning from 2019 to 2033, with a base and estimated year of 2025 and a forecast period of 2025–2033, this study delves into the intricate dynamics, growth trajectories, and competitive landscape. We explore both parent and child market perspectives to offer unparalleled insights for industry professionals, investors, and decision-makers aiming to navigate and capitalize on this evolving sector. All quantitative data is presented in billions of units.

meat products food packaging Market Dynamics & Structure

The global meat products food packaging market is characterized by moderate concentration, with a few dominant players holding significant market share. Technological innovation remains a key driver, propelled by the continuous pursuit of extended shelf-life, enhanced food safety, and improved product presentation. Regulatory frameworks, particularly concerning food contact materials and sustainability mandates, exert substantial influence on product development and market entry. Competitive product substitutes, such as alternative protein sources and advanced preservation techniques, present a dynamic competitive front. End-user demographics, with a growing demand for convenience, traceability, and sustainable options, are increasingly shaping packaging design and material choices. Mergers and acquisitions (M&A) trends are active, as companies seek to expand their product portfolios, geographic reach, and technological capabilities.

- Market Concentration: Dominated by a mix of multinational corporations and specialized packaging providers.

- Technological Innovation Drivers: Focus on barrier properties, active and intelligent packaging, and sustainable material development.

- Regulatory Frameworks: Strict adherence to food safety standards (e.g., FDA, EFSA) and increasing pressure for recyclability and compostability.

- Competitive Product Substitutes: Growth in plant-based alternatives and innovations in food processing impacting traditional packaging needs.

- End-User Demographics: Rising demand for on-the-go options, smaller portion sizes, and packaging that clearly communicates origin and health benefits.

- M&A Trends: Strategic acquisitions aimed at securing advanced recycling technologies and expanding into high-growth emerging markets.

meat products food packaging Growth Trends & Insights

The meat products food packaging market is poised for substantial growth, driven by an escalating global demand for protein-rich foods and evolving consumer preferences. Market size is projected to expand significantly, fueled by increasing population, rising disposable incomes, and a growing appetite for processed and convenience meat products. Adoption rates for advanced packaging solutions, such as modified atmosphere packaging (MAP) and active packaging, are on an upward trajectory, contributing to extended shelf-life and reduced food waste. Technological disruptions, including the development of biodegradable and compostable packaging materials, alongside innovations in smart packaging that offer real-time spoilage detection, are reshaping the market landscape. Consumer behavior shifts, marked by a heightened awareness of health, sustainability, and ethical sourcing, are compelling manufacturers to prioritize eco-friendly and transparent packaging solutions. The projected CAGR for the forecast period indicates a robust expansion, reflecting the market's resilience and its vital role in the food supply chain. Market penetration of specialized packaging for fresh and frozen meats is expected to deepen, driven by increased urbanization and changing dietary habits in developing economies.

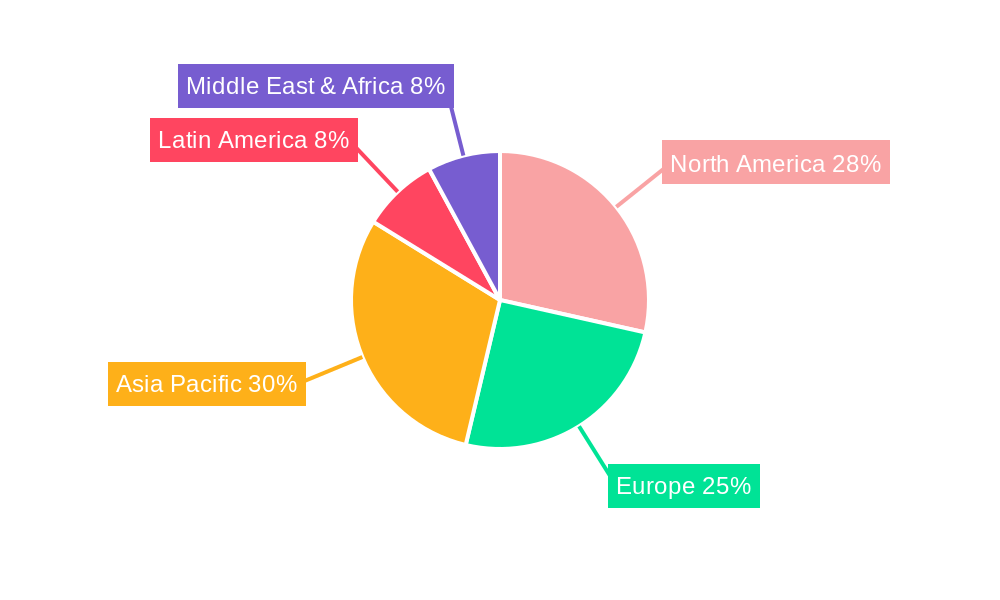

Dominant Regions, Countries, or Segments in meat products food packaging

The Fresh Meat Products application segment is currently the dominant force in the global meat products food packaging market, driven by its larger volume and widespread consumption. Within this segment, Polyethylene and Polypropylene emerge as leading material types, favored for their excellent barrier properties, flexibility, and cost-effectiveness in protecting fresh meat from spoilage and contamination.

North America and Europe currently represent the dominant regions, owing to established meat consumption patterns, advanced retail infrastructure, and stringent food safety regulations that necessitate high-quality packaging. However, the Asia Pacific region is emerging as the fastest-growing market, propelled by a burgeoning middle class, increasing urbanization, and a significant rise in meat consumption. Economic policies that support food processing and agricultural development, coupled with investments in modernizing cold chain logistics and retail supply chains, are key drivers in these rapidly developing regions.

- Key Drivers in Dominant Segments:

- Fresh Meat Products: Growing demand for convenient, ready-to-eat meat options and increasing adoption of MAP for extended freshness.

- Polyethylene & Polypropylene: Superior barrier properties against moisture and oxygen, cost-effectiveness, and high recyclability rates.

- North America & Europe: High per capita meat consumption, sophisticated retail networks, and strong regulatory enforcement.

- Asia Pacific (Growth Driver): Rapidly expanding middle class, increasing disposable income, and shifting dietary preferences towards protein-rich foods.

- Dominance Factors & Growth Potential: The dominance of fresh meat packaging is underpinned by its everyday necessity. The growth potential in the Asia Pacific region is immense, offering substantial market share expansion opportunities as it catches up to the consumption levels and packaging sophistication of developed economies. Continued innovation in sustainable packaging materials will also play a crucial role in maintaining dominance and unlocking new growth avenues across all regions.

meat products food packaging Product Landscape

The meat products food packaging landscape is defined by continuous innovation aimed at enhancing product safety, extending shelf-life, and improving consumer appeal. Advanced barrier films, incorporating materials like BOPET and specialized polyolefins, are crucial for preventing oxygen ingress and moisture loss, thereby preserving the freshness and quality of both fresh and frozen meats. Intelligent packaging solutions, such as time-temperature indicators and gas-sensing films, are gaining traction, providing consumers with greater confidence in product integrity. The trend towards mono-material packaging, particularly for improved recyclability, is driving the development of high-performance polypropylene and polyethylene-based structures. Sustainable alternatives, including paper-based solutions with enhanced barrier coatings and biodegradable polymers, are also emerging as significant product innovations.

Key Drivers, Barriers & Challenges in meat products food packaging

Key Drivers:

- Growing Global Protein Demand: An increasing world population and rising disposable incomes worldwide are fueling higher consumption of meat products, directly driving demand for their packaging.

- Food Safety and Shelf-Life Extension: Consumer and regulatory pressure for enhanced food safety and reduced spoilage necessitates advanced packaging technologies that extend product shelf-life, minimizing waste and ensuring consumer well-being.

- Convenience and Ready-to-Eat Trends: The shift towards more convenient food options, including pre-portioned and ready-to-cook meat products, requires specialized packaging that facilitates ease of use and preparation.

- Sustainability Initiatives: Growing environmental consciousness is a significant driver for the development and adoption of recyclable, compostable, and biodegradable packaging solutions.

Key Barriers & Challenges:

- Cost of Advanced Materials: The higher cost of some advanced and sustainable packaging materials can be a barrier for smaller manufacturers or in price-sensitive markets, impacting adoption rates.

- Recycling Infrastructure Limitations: Inadequate or inconsistent recycling infrastructure in many regions poses a significant challenge to the widespread adoption of fully recyclable packaging solutions.

- Complex Supply Chains: Managing complex and often temperature-sensitive meat supply chains requires robust and reliable packaging, making transitions to new materials or designs challenging.

- Regulatory Hurdles: Evolving and sometimes fragmented regulations across different countries concerning food contact materials and waste management can create compliance complexities and market access barriers.

- Consumer Perception of Alternatives: While demand for sustainable options is growing, consumer perception and acceptance of certain alternative materials can be a hurdle for widespread implementation.

Emerging Opportunities in meat products food packaging

Emerging opportunities in the meat products food packaging market lie in the burgeoning demand for sustainable and transparent packaging solutions. The rise of plant-based and alternative protein sources presents new packaging requirements, with opportunities for innovative materials that mimic the texture and appearance of traditional meat. The increasing focus on traceability and provenance offers a fertile ground for smart packaging technologies that can provide consumers with detailed information about the product's origin and journey. Furthermore, the expansion of e-commerce for food products necessitates robust and insulated packaging capable of maintaining product integrity during transit. Untapped markets in developing economies, with their rapidly growing middle classes and increasing meat consumption, represent significant growth potential for both standard and innovative packaging solutions.

Growth Accelerators in the meat products food packaging Industry

Several catalysts are accelerating growth within the meat products food packaging industry. Technological breakthroughs in material science, particularly in developing high-performance, sustainable barrier films and compostable polymers, are key accelerators. Strategic partnerships between packaging manufacturers and meat producers are fostering co-creation of solutions tailored to specific product needs and market demands. Furthermore, market expansion strategies focusing on emerging economies, where demand for processed and packaged meat is rapidly increasing, are significant growth drivers. The development of advanced recycling technologies and the establishment of circular economy models for packaging are also poised to accelerate adoption and market growth by addressing sustainability concerns.

Key Players Shaping the meat products food packaging Market

- Sonoco Products

- DS Smith

- Sealed Air Corporation

- Amcor

- International Paper

- Smurfit Kappa

- Silgan Holdings

- Schur Flexibles

Notable Milestones in meat products food packaging Sector

- 2021/03: Amcor launches a new line of recyclable mono-material barrier films for fresh meat packaging, addressing sustainability concerns.

- 2022/07: Sealed Air Corporation introduces a novel active packaging technology that extends the shelf-life of fresh meat by up to 50%.

- 2023/01: DS Smith announces significant investments in developing sustainable paper-based packaging solutions for the food industry.

- 2023/05: Schur Flexibles develops innovative, compostable packaging films designed for specific meat product applications.

- 2024/02: Smurfit Kappa expands its portfolio of sustainable packaging for the food sector with a focus on bio-based materials.

In-Depth meat products food packaging Market Outlook

The future of the meat products food packaging market is exceptionally promising, driven by a confluence of factors including sustained global demand for protein, increasing consumer consciousness around health and sustainability, and continuous technological advancements. Growth accelerators such as the development of advanced recyclable and compostable materials, strategic collaborations across the value chain, and significant market expansion in emerging economies will propel the industry forward. The market outlook points towards a dynamic landscape where innovation in smart packaging for enhanced traceability and safety will become increasingly prevalent. Investments in circular economy solutions and a focus on reducing food waste will further shape market strategies, creating ample opportunities for stakeholders who can adapt to these evolving demands.

meat products food packaging Segmentation

-

1. Application

- 1.1. Fresh Meat Products

- 1.2. Frozen Meat Products

-

2. Types

- 2.1. Polypropylene

- 2.2. Polyethylene

- 2.3. Paper

- 2.4. Aluminum

- 2.5. BOPET

- 2.6. Poly Vinyl Chloride

- 2.7. Others

meat products food packaging Segmentation By Geography

- 1. CA

meat products food packaging Regional Market Share

Geographic Coverage of meat products food packaging

meat products food packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. meat products food packaging Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Fresh Meat Products

- 5.1.2. Frozen Meat Products

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Polypropylene

- 5.2.2. Polyethylene

- 5.2.3. Paper

- 5.2.4. Aluminum

- 5.2.5. BOPET

- 5.2.6. Poly Vinyl Chloride

- 5.2.7. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. CA

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Sonoco Products

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 DS Smith

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Sealed Air Corporation

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Amcor

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Interntional Paper

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Smurfit Kappa

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Silgan Holdings

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Schur Flexibles

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.1 Sonoco Products

List of Figures

- Figure 1: meat products food packaging Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: meat products food packaging Share (%) by Company 2025

List of Tables

- Table 1: meat products food packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: meat products food packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: meat products food packaging Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: meat products food packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: meat products food packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: meat products food packaging Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the meat products food packaging?

The projected CAGR is approximately 9.9%.

2. Which companies are prominent players in the meat products food packaging?

Key companies in the market include Sonoco Products, DS Smith, Sealed Air Corporation, Amcor, Interntional Paper, Smurfit Kappa, Silgan Holdings, Schur Flexibles.

3. What are the main segments of the meat products food packaging?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3400.00, USD 5100.00, and USD 6800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "meat products food packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the meat products food packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the meat products food packaging?

To stay informed about further developments, trends, and reports in the meat products food packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence