Key Insights

The global sterile medical packaging market is poised for significant expansion, projected to reach an estimated $55,000 million by 2025, driven by an anticipated Compound Annual Growth Rate (CAGR) of 7.2% from 2025 to 2033. This robust growth is fueled by the escalating demand for advanced healthcare solutions, particularly in pharmaceuticals and in vitro diagnostic products, which are increasingly relying on sterile packaging to maintain product integrity and patient safety. The rising prevalence of chronic diseases and the growing global healthcare expenditure are further propelling the adoption of sterile medical packaging. Technological advancements in material science, leading to the development of more resilient and sustainable packaging options such as specialized plastics and advanced composites, are also key contributors to market expansion. The increasing stringency of regulatory standards worldwide for medical device and pharmaceutical packaging further necessitates the use of high-quality sterile solutions, thereby bolstering market demand.

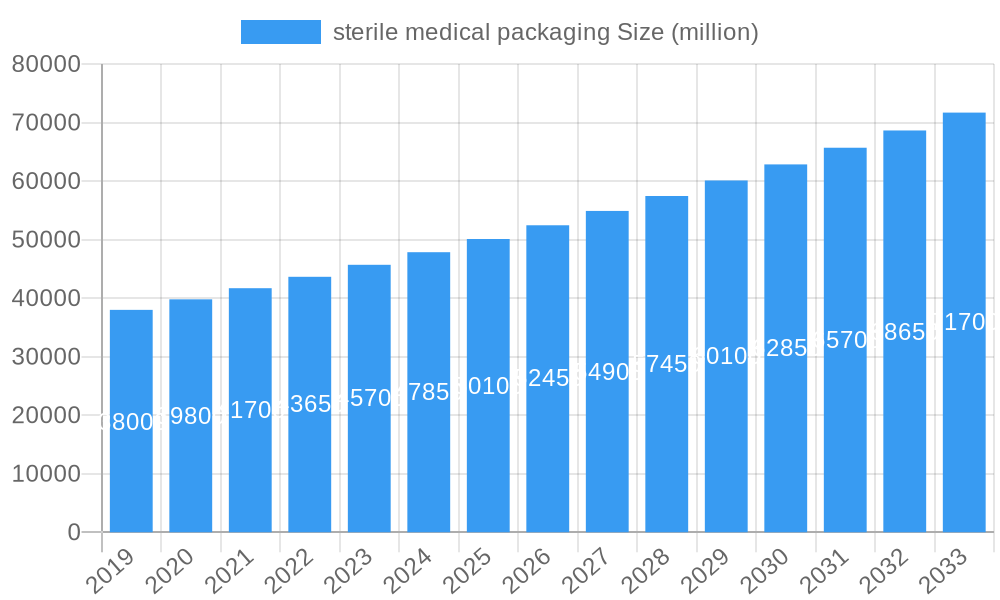

sterile medical packaging Market Size (In Billion)

The market is segmented into various applications including pharmaceuticals, surgical instruments, in vitro diagnostic products, medical implants, and others, with pharmaceuticals and in vitro diagnostics expected to lead the growth trajectory due to their critical need for sterile environments. In terms of materials, plastic dominates the market due to its versatility, cost-effectiveness, and barrier properties, though glass, metal, and paperboard also hold significant shares for specific applications. Key players like West, Amcor, and Gerresheimer are actively investing in research and development to innovate packaging solutions that offer enhanced sterility, extended shelf life, and improved user experience. Geographically, North America and Europe are anticipated to retain substantial market share, attributed to their advanced healthcare infrastructure and high adoption rates of sophisticated medical technologies. Emerging economies are also presenting considerable growth opportunities as healthcare access expands. However, challenges such as the high cost of advanced packaging materials and the complexity of sterilization processes could pose moderate restraints to the market's otherwise promising outlook.

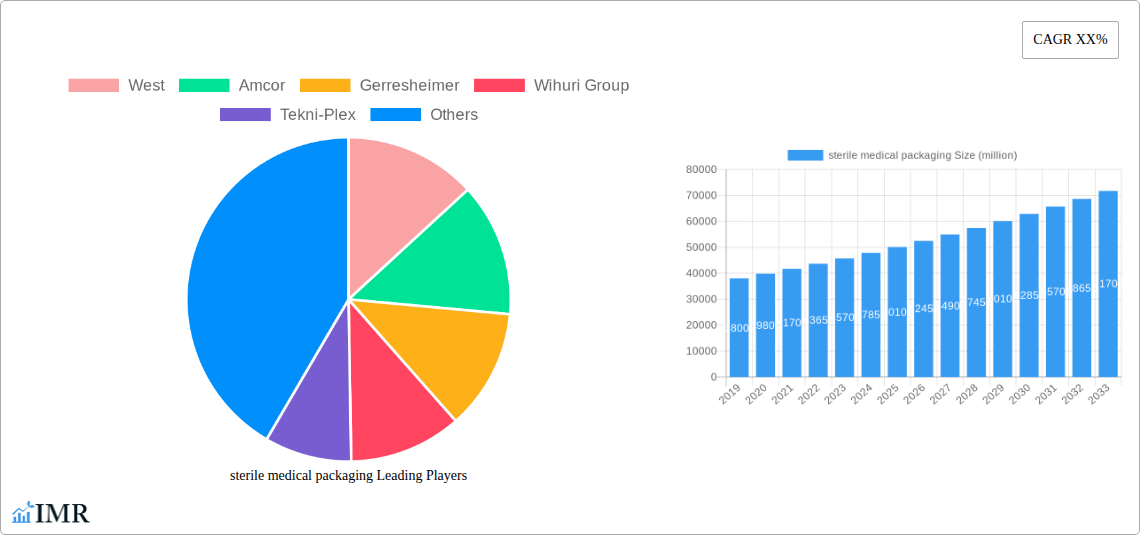

sterile medical packaging Company Market Share

Comprehensive Report on Sterile Medical Packaging: Market Dynamics, Growth Trends, and Future Outlook (2019-2033)

This in-depth report offers a panoramic view of the global sterile medical packaging market, delving into its intricate dynamics, robust growth trajectories, and promising future. Covering the historical period from 2019 to 2024, with a base year of 2025 and a forecast period extending to 2033, this analysis provides actionable insights for stakeholders navigating this critical industry. The report examines market size evolution, key drivers, emerging opportunities, and the competitive landscape, with all quantitative data presented in million units.

sterile medical packaging Market Dynamics & Structure

The sterile medical packaging market exhibits a moderately concentrated structure, with a mix of large multinational corporations and specialized niche players. Key drivers of technological innovation include advancements in material science, such as the development of high-barrier films and antimicrobial coatings, and the integration of smart packaging solutions for enhanced traceability and patient safety. Regulatory frameworks, including stringent FDA and EMA guidelines for device and drug packaging, play a pivotal role in shaping market entry and product development. Competitive product substitutes, primarily from conventional packaging materials not meeting sterile requirements, present a constant challenge, necessitating continuous innovation in performance and cost-effectiveness. End-user demographics are increasingly influenced by an aging global population, rising chronic disease prevalence, and the growing demand for minimally invasive procedures, all of which necessitate sophisticated sterile packaging solutions. Merger and acquisition (M&A) activity has been observed, particularly among companies seeking to expand their product portfolios, geographical reach, or technological capabilities, reflecting a strategic consolidation trend.

- Market Concentration: Moderately concentrated, dominated by key players but with significant contributions from specialized manufacturers.

- Technological Innovation: Driven by material science (barrier films, antimicrobial coatings) and smart packaging integration.

- Regulatory Frameworks: Strict adherence to FDA, EMA, and other global health authority regulations is paramount.

- Competitive Substitutes: Conventional non-sterile packaging and materials that do not meet regulatory sterilization requirements.

- End-User Demographics: Aging population, increased chronic disease rates, and growth in surgical procedures.

- M&A Trends: Strategic acquisitions aimed at portfolio expansion, market access, and technology acquisition.

sterile medical packaging Growth Trends & Insights

The global sterile medical packaging market is poised for significant expansion, driven by an escalating global demand for safe and reliable healthcare solutions. The market size has witnessed a steady evolution, with a projected Compound Annual Growth Rate (CAGR) of approximately 6.5% from the base year 2025 through 2033. This growth is underpinned by increasing healthcare expenditure worldwide, a growing emphasis on infection prevention and control, and the continuous development of new pharmaceuticals and advanced medical devices that require specialized sterile containment. Adoption rates for advanced sterile packaging solutions, such as those incorporating tamper-evident features, sterilization indicators, and advanced barrier properties, are on the rise. Technological disruptions, including the advent of sustainable and bio-based sterile packaging materials, are also influencing market dynamics, appealing to a growing environmentally conscious consumer base and regulatory push for greener alternatives. Shifts in consumer behavior, particularly patient demand for assurance of product sterility and safety, further fuel the adoption of high-quality sterile packaging.

The market penetration of advanced sterile medical packaging continues to deepen across diverse healthcare applications. For instance, the pharmaceutical segment, a cornerstone of the market, benefits from stringent requirements for drug integrity and shelf-life extension, driving demand for sophisticated blister packs, vials, and pre-filled syringe packaging. Similarly, the surgical instruments sector relies heavily on sterile packaging to maintain aseptic conditions during sterilization and transport, with advancements in rigid trays and pouch systems enabling enhanced protection. The in vitro diagnostic (IVD) products segment is experiencing rapid growth due to the proliferation of diagnostic testing, necessitating sterile packaging for reagents, sample collection devices, and assay kits to ensure accurate and reliable results. The medical implants sector, characterized by high-value, implantable devices, demands the highest levels of sterility assurance, driving the use of advanced materials and designs.

Key Growth Metrics:

- Projected CAGR (2025-2033): ~6.5%

- Market Size Evolution: Steadily increasing year-over-year, driven by healthcare demand.

- Adoption Rates: Rising for advanced features like tamper-evidence and sterilization indicators.

- Technological Disruptions: Emergence of sustainable and bio-based materials.

- Consumer Behavior Shifts: Increased patient emphasis on sterility assurance and safety.

- Market Penetration: Deepening across pharmaceuticals, surgical instruments, IVD, and medical implants.

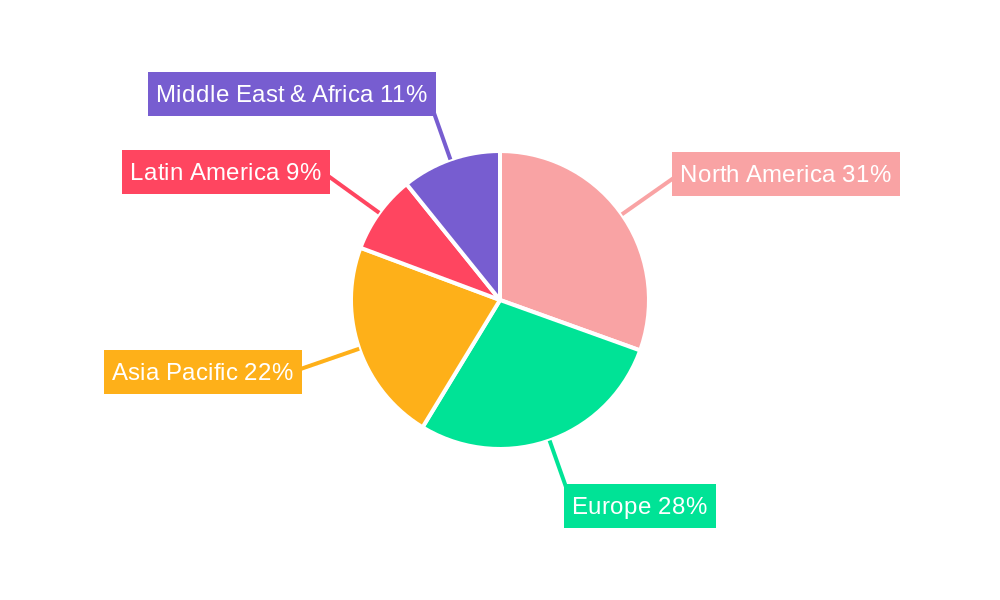

Dominant Regions, Countries, or Segments in sterile medical packaging

North America currently stands as a dominant region in the sterile medical packaging market, primarily driven by the United States. This dominance is attributed to a robust healthcare infrastructure, high per capita healthcare spending, a well-established pharmaceutical and medical device manufacturing base, and stringent regulatory enforcement that mandates high standards for sterile packaging. The region's advanced research and development capabilities foster continuous innovation in packaging technologies, further solidifying its leading position. Countries like Germany, the United Kingdom, and France are significant contributors within Europe, bolstered by advanced healthcare systems, strong biopharmaceutical sectors, and an increasing focus on patient safety and infection control. Asia-Pacific is emerging as a rapidly growing market, propelled by expanding healthcare access, a burgeoning middle class, increasing investments in domestic medical device manufacturing, and supportive government initiatives in countries like China and India.

Within the Application segment, Pharmaceuticals represent the largest and most influential segment in the sterile medical packaging market. The sheer volume of pharmaceutical products, coupled with the critical need for drug stability, sterility, and regulatory compliance, makes this segment a consistent driver of demand. Pharmaceutical packaging encompasses a wide array of formats, including blister packs, vials, ampoules, syringes, and sachets, all requiring specific sterile properties. The Surgical Instruments segment also holds significant market share, as the sterilization and aseptic presentation of surgical tools are paramount to preventing surgical site infections. The increasing number of surgical procedures globally directly correlates with the demand for sterile packaging solutions for these instruments.

The In Vitro Diagnostic Products segment is exhibiting a particularly high growth rate, fueled by advancements in diagnostic technologies, the increasing prevalence of chronic diseases requiring regular testing, and the expansion of point-of-care diagnostics. Sterile packaging for IVD kits, reagents, and sample collection devices is crucial for ensuring the accuracy and reliability of diagnostic results. The Medical Implants segment, while smaller in volume compared to pharmaceuticals, commands a high value due to the critical nature of implantable devices. These products necessitate the utmost sterility assurance and often employ advanced packaging solutions with features like nitrogen purging and advanced sealing technologies.

In terms of Types, Plastic packaging dominates the sterile medical packaging market. This is due to its versatility, cost-effectiveness, durability, and ability to be molded into various shapes and sizes, catering to a wide range of medical products. High-performance polymers offer excellent barrier properties against moisture, oxygen, and light, crucial for maintaining product sterility and extending shelf-life. Glass packaging remains important for certain sterile applications, particularly for pharmaceuticals and some IVD reagents, offering excellent chemical inertness and barrier properties. However, its fragility and higher cost limit its widespread adoption compared to plastics.

- Dominant Region: North America (primarily the United States), followed by Europe and a rapidly growing Asia-Pacific.

- Dominant Application Segment: Pharmaceuticals, followed closely by Surgical Instruments and a high-growth IVD segment.

- Dominant Packaging Type: Plastic, due to its versatility, cost-effectiveness, and barrier properties.

- Key Drivers (Regional): Healthcare expenditure, manufacturing capabilities, regulatory landscape, R&D.

- Key Drivers (Segmental): Drug integrity, infection prevention, diagnostic accuracy, implant safety.

- Growth Potential: Asia-Pacific region and IVD segment showing significant expansion.

sterile medical packaging Product Landscape

The sterile medical packaging product landscape is characterized by continuous innovation aimed at enhancing product safety, functionality, and sustainability. Key product developments include advanced polymer films with superior barrier properties against oxygen, moisture, and microbial ingress, ensuring extended shelf-life and maintaining drug efficacy. Innovations in sterilization-compatible materials, such as advanced polyolefins and co-polyesters, are crucial for products undergoing terminal sterilization methods like gamma irradiation or ethylene oxide (EtO). Smart packaging solutions are gaining traction, incorporating features like temperature indicators, humidity sensors, and tamper-evident seals that provide real-time product integrity information to healthcare professionals and patients. Unique selling propositions often revolve around a combination of superior barrier performance, compatibility with various sterilization methods, enhanced usability, and a commitment to sustainability through the use of recyclable materials or bio-based alternatives. Technological advancements are also focused on creating lighter-weight yet equally protective packaging, reducing material usage and transportation costs.

Key Drivers, Barriers & Challenges in sterile medical packaging

Key Drivers:

- Rising Global Healthcare Expenditure: Increased funding for healthcare services and infrastructure globally drives demand for medical supplies and devices, consequently boosting the need for sterile packaging.

- Growing Prevalence of Chronic Diseases: The increasing burden of chronic conditions necessitates ongoing medical treatments and device usage, leading to sustained demand for sterile packaging solutions.

- Stringent Regulatory Requirements: Mandates from regulatory bodies like the FDA and EMA for patient safety and product integrity necessitate the use of high-quality, compliant sterile packaging.

- Advancements in Medical Technology: The development of new and complex medical devices and pharmaceuticals often requires innovative and specialized sterile packaging solutions.

- Focus on Infection Prevention and Control: Heightened awareness and initiatives aimed at reducing healthcare-associated infections (HAIs) amplify the importance of maintaining product sterility throughout the supply chain.

Barriers & Challenges:

- High Cost of Advanced Materials and Technologies: Premium sterile packaging solutions often involve sophisticated materials and manufacturing processes, leading to higher costs that can impact affordability, especially for emerging markets.

- Complex Regulatory Compliance: Navigating the intricate and evolving regulatory landscape across different geographical regions can be challenging and time-consuming for manufacturers.

- Supply Chain Disruptions and Raw Material Volatility: Global supply chain vulnerabilities, geopolitical events, and fluctuations in raw material prices can impact production schedules and increase operational costs.

- Environmental Sustainability Concerns: Increasing pressure to adopt eco-friendly packaging solutions while maintaining sterilization integrity poses a significant challenge, requiring investment in R&D for sustainable alternatives.

- Counterfeit Product Risk: The persistent threat of counterfeit medical products necessitates robust anti-counterfeiting features within sterile packaging, adding complexity and cost.

Emerging Opportunities in sterile medical packaging

Emerging opportunities in the sterile medical packaging market lie in the development of smart and connected packaging solutions that offer enhanced traceability, real-time monitoring, and improved patient engagement. The growing demand for sustainable and eco-friendly packaging presents a significant avenue for innovation, with opportunities in bio-based polymers, compostable materials, and optimized designs that reduce material usage and waste. The expansion of personalized medicine and biologics also creates a need for highly specialized, custom-engineered sterile packaging solutions tailored to specific product requirements. Furthermore, the increasing adoption of telemedicine and home healthcare models will drive the demand for sterile packaging that facilitates safe and convenient self-administration of medications and devices outside traditional clinical settings.

Growth Accelerators in the sterile medical packaging Industry

Several key factors are accelerating growth within the sterile medical packaging industry. Technological breakthroughs in material science, such as the development of novel polymers with improved barrier properties and antimicrobial capabilities, are enhancing product performance and safety. Strategic partnerships and collaborations between packaging manufacturers, medical device companies, and pharmaceutical firms are fostering innovation and market penetration. The increasing globalization of healthcare, with emerging economies investing heavily in their healthcare infrastructure, is opening up new markets for sterile medical packaging. Moreover, a growing emphasis on end-to-end supply chain solutions, including sterile packaging integrated with logistics and track-and-trace systems, is driving efficiency and reliability, further propelling market expansion.

Key Players Shaping the sterile medical packaging Market

- West

- Amcor

- Gerresheimer

- Wihuri Group

- Tekni-Plex

- Sealed Air

- OLIVER

- ProAmpac

- Printpack

- ALPLA

- Nelipak Healthcare

- VP Group

- OKADA SHIGYO

Notable Milestones in sterile medical packaging Sector

- 2020: Introduction of enhanced EtO sterilization compatible pouches with improved seal integrity by a leading manufacturer, addressing increased demand for flexible sterile packaging.

- 2021: Major acquisition of a specialized medical device packaging company by a global packaging conglomerate, consolidating market share and expanding capabilities.

- 2022: Launch of a new line of sustainable, recyclable sterile packaging films derived from post-consumer recycled (PCR) content, responding to growing environmental pressures.

- 2023: Development and regulatory approval of a novel smart packaging solution incorporating real-time temperature monitoring for temperature-sensitive biologics.

- 2024 (early): Increased investment in advanced manufacturing technologies for sterile barrier systems to meet growing demand for medical implants and complex surgical instruments.

In-Depth sterile medical packaging Market Outlook

The future outlook for the sterile medical packaging market is exceptionally robust, fueled by an unyielding demand for safe, effective, and compliant healthcare solutions. Growth accelerators, including continuous material innovation, the integration of digital technologies for enhanced traceability, and a global push towards sustainability, will shape the market's trajectory. Strategic market expansion into underdeveloped regions and a focus on developing specialized packaging for biologics, cell therapies, and advanced medical devices will be crucial for capturing future potential. The industry is well-positioned to capitalize on evolving healthcare needs, driven by an aging global population and advancements in medical science, ensuring sustained growth and significant opportunities for innovation and investment.

sterile medical packaging Segmentation

-

1. Application

- 1.1. Pharmaceuticals

- 1.2. Surgical Instruments

- 1.3. In Vitro Diagnostic Products

- 1.4. Medical Implants

- 1.5. Others

-

2. Types

- 2.1. Plastic

- 2.2. Glass

- 2.3. Metal

- 2.4. Paper and Paperboard

- 2.5. Other

sterile medical packaging Segmentation By Geography

- 1. CA

sterile medical packaging Regional Market Share

Geographic Coverage of sterile medical packaging

sterile medical packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. sterile medical packaging Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Pharmaceuticals

- 5.1.2. Surgical Instruments

- 5.1.3. In Vitro Diagnostic Products

- 5.1.4. Medical Implants

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Plastic

- 5.2.2. Glass

- 5.2.3. Metal

- 5.2.4. Paper and Paperboard

- 5.2.5. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. CA

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 West

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Amcor

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Gerresheimer

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Wihuri Group

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Tekni-Plex

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Sealed Air

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 OLIVER

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 ProAmpac

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Printpack

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 ALPLA

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Nelipak Healthcare

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 VP Group

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 OKADA SHIGYO

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.1 West

List of Figures

- Figure 1: sterile medical packaging Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: sterile medical packaging Share (%) by Company 2025

List of Tables

- Table 1: sterile medical packaging Revenue million Forecast, by Application 2020 & 2033

- Table 2: sterile medical packaging Revenue million Forecast, by Types 2020 & 2033

- Table 3: sterile medical packaging Revenue million Forecast, by Region 2020 & 2033

- Table 4: sterile medical packaging Revenue million Forecast, by Application 2020 & 2033

- Table 5: sterile medical packaging Revenue million Forecast, by Types 2020 & 2033

- Table 6: sterile medical packaging Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the sterile medical packaging?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the sterile medical packaging?

Key companies in the market include West, Amcor, Gerresheimer, Wihuri Group, Tekni-Plex, Sealed Air, OLIVER, ProAmpac, Printpack, ALPLA, Nelipak Healthcare, VP Group, OKADA SHIGYO.

3. What are the main segments of the sterile medical packaging?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3400.00, USD 5100.00, and USD 6800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "sterile medical packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the sterile medical packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the sterile medical packaging?

To stay informed about further developments, trends, and reports in the sterile medical packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence