Key Insights

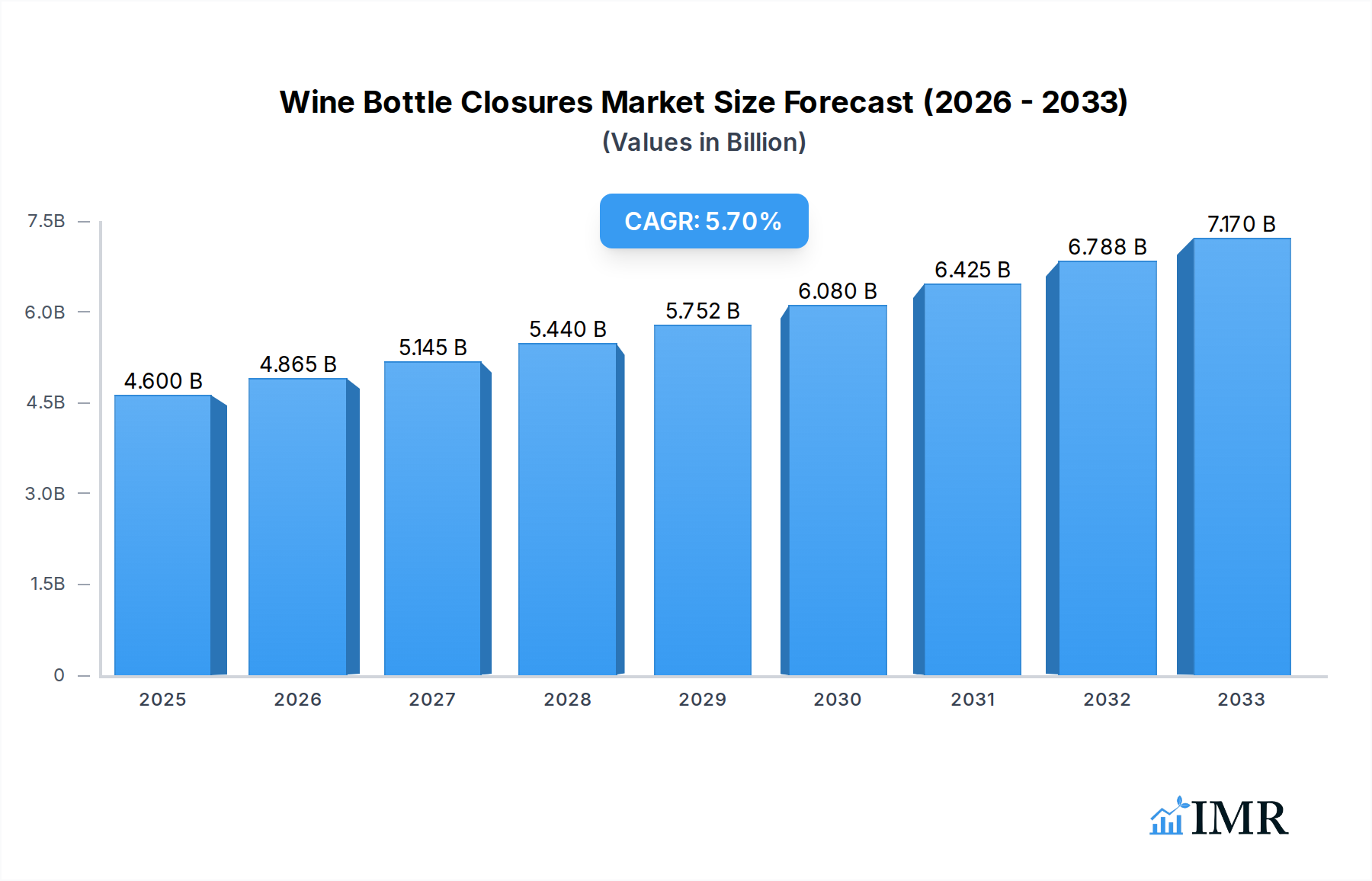

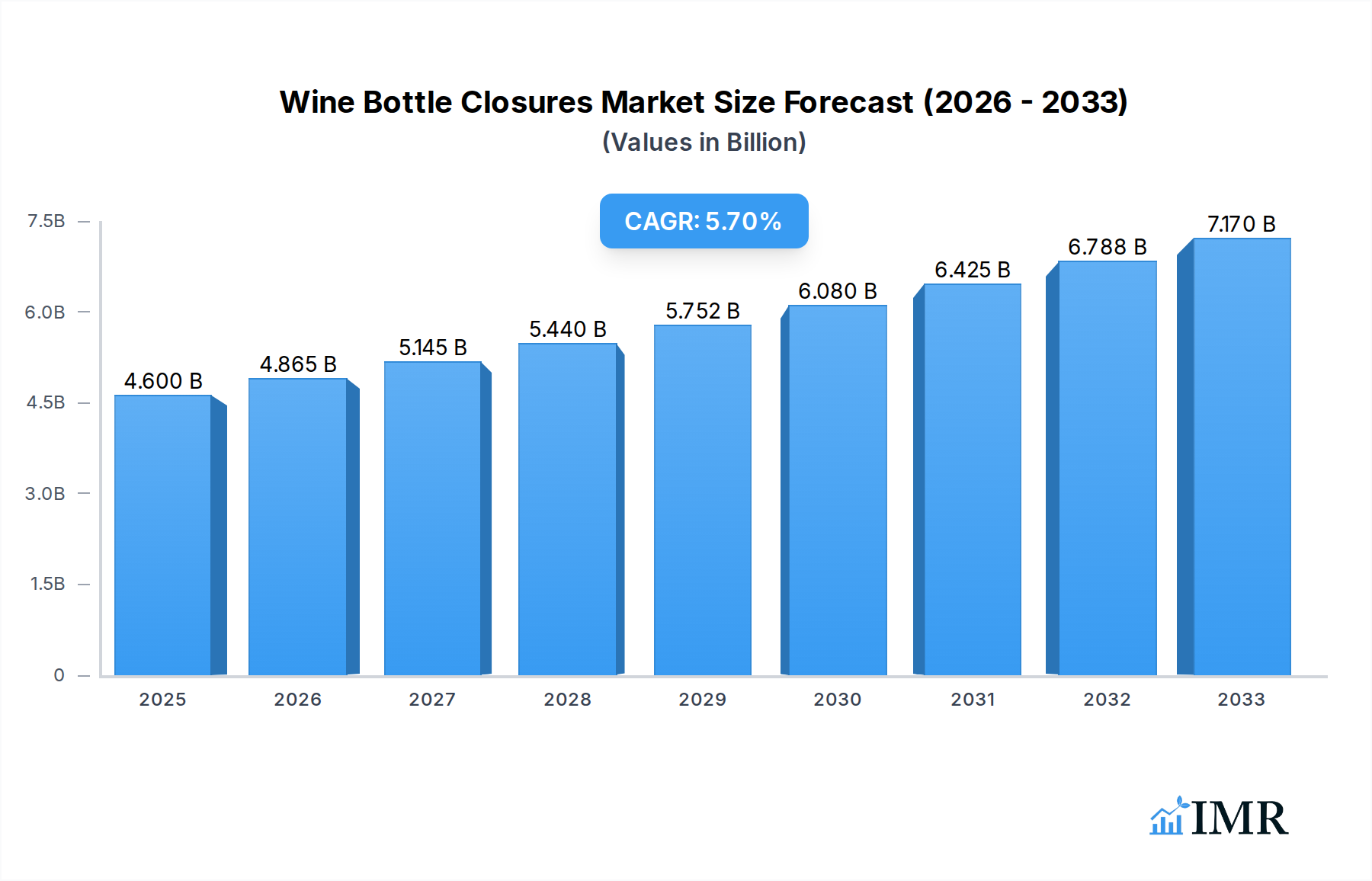

The global wine bottle closures market is poised for substantial growth, projected to reach an estimated $4.6 billion by 2025. This expansion is driven by a confluence of factors, including the burgeoning global demand for wine, particularly in emerging economies, and the increasing preference for premium wine experiences that necessitate reliable and aesthetically pleasing closures. Technological advancements are playing a crucial role, with innovations in materials and designs enhancing wine preservation and reducing spoilage rates, thus contributing to market value. The market is experiencing a Compound Annual Growth Rate (CAGR) of 5.83% during the forecast period of 2025-2033, indicating a robust and sustained upward trajectory. Key segments within the market, such as still wine closures, are benefiting from steady consumption, while sparkling wine closures are seeing increased demand driven by celebratory occasions and the growing popularity of sparkling wine varietals. The dominance of cork closures continues, but screwcaps are rapidly gaining traction due to their convenience and effectiveness in preserving wine freshness, especially for everyday wines.

Wine Bottle Closures Market Size (In Billion)

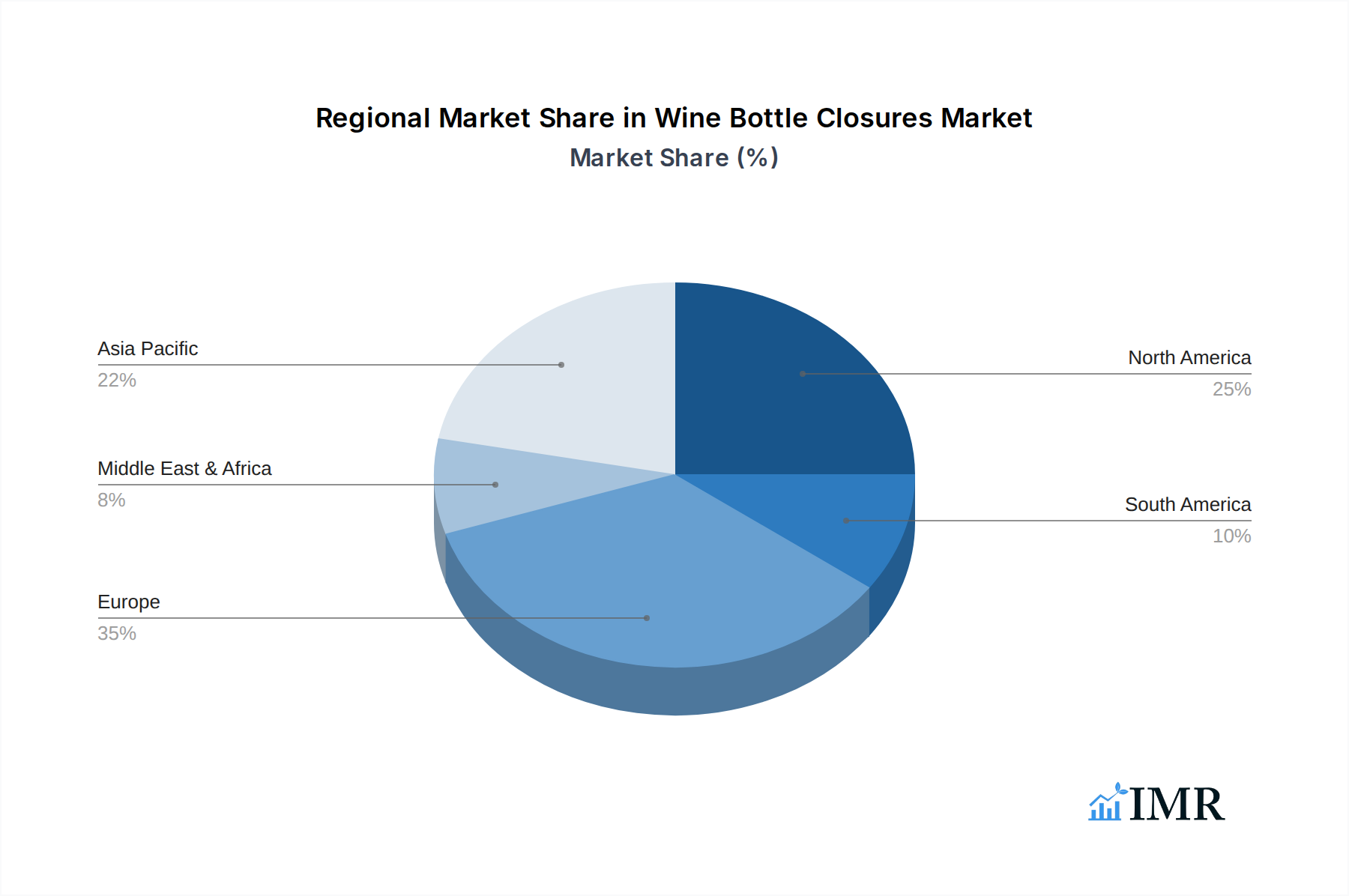

The market is characterized by dynamic trends and a competitive landscape featuring prominent players like Amorim, MASilva, and Guala Closures Group. These companies are actively investing in research and development to introduce sustainable and innovative closure solutions. Sustainability is a major trend, with a growing emphasis on environmentally friendly materials and manufacturing processes. This is reflected in the increasing adoption of natural cork, as well as advancements in synthetic and alternative closures designed to minimize environmental impact. However, the market faces certain restraints, including fluctuations in raw material costs and the potential for stricter environmental regulations on certain closure materials. Regional dynamics showcase North America and Europe as mature markets, while the Asia Pacific region presents significant growth opportunities driven by increasing wine consumption and a growing middle class. The ongoing evolution of consumer preferences, coupled with innovative product development, will continue to shape the trajectory of the wine bottle closures market.

Wine Bottle Closures Company Market Share

Comprehensive Wine Bottle Closures Market Report: Dynamics, Growth, and Future Outlook

This in-depth report offers an exhaustive analysis of the global wine bottle closures market, meticulously detailing its current landscape, historical evolution, and projected trajectory from 2019 to 2033. With a strong focus on SEO optimization and industry professional engagement, this report integrates high-traffic keywords, parent and child market segmentation, and critical market dynamics to provide unparalleled insights. All quantitative values are presented in billion units for clarity and actionable intelligence.

Wine Bottle Closures Market Dynamics & Structure

The global wine bottle closures market exhibits a dynamic and evolving structure, influenced by a complex interplay of technological innovation, regulatory frameworks, and shifting consumer preferences. Market concentration varies significantly across different closure types and geographic regions. Leading players like Amorim, MASilva, Cork Supply, Vinvention, Guala Closures Group, and Bericap hold substantial market shares, particularly in the natural cork and screwcap segments. However, the rise of innovative alternatives and specialized closures introduces pockets of intense competition.

- Technological Innovation Drivers: Advancements in materials science, sustainable manufacturing processes, and smart closure technologies are key innovation drivers. These include advancements in oxygen management for corks, improved sealing mechanisms for screwcaps, and the development of novel plastic and synthetic closures offering enhanced performance and aesthetic appeal.

- Regulatory Frameworks: Stringent regulations concerning food safety, material traceability, and environmental impact significantly shape the market. Compliance with international standards and regional legislation impacts product development, material sourcing, and market entry for closure manufacturers.

- Competitive Product Substitutes: The market is characterized by a robust ecosystem of product substitutes. Natural cork, while traditional, faces competition from agglomerated cork, technical corks, screwcaps (aluminum and plastic), synthetic stoppers, and increasingly, glass stoppers and innovative cap systems, each offering distinct advantages in terms of cost, performance, and sustainability.

- End-User Demographics: Evolving end-user demographics, particularly the growing millennial and Gen Z consumer base, influence demand for convenience, sustainability, and premiumization. This translates to a demand for closures that offer ease of opening, enhanced shelf life, and eco-friendly credentials.

- M&A Trends: Mergers and acquisitions are prevalent, driven by the pursuit of market consolidation, access to new technologies, and expansion into emerging markets. These strategic moves aim to bolster competitive positioning and drive synergistic growth within the parent market.

Wine Bottle Closures Growth Trends & Insights

The global wine bottle closures market is poised for robust growth, propelled by an escalating global wine consumption, coupled with continuous advancements in closure technologies and a growing emphasis on sustainability. The market size is projected to witness a significant CAGR of XX% over the forecast period, driven by increasing adoption rates of advanced closure solutions across both still and sparkling wine applications. Technological disruptions, such as the development of closures with integrated oxygen management systems and tamper-evident features, are not only enhancing wine preservation but also creating new avenues for market penetration.

Consumer behavior shifts are playing a pivotal role in shaping demand. The rising preference for convenience, reflected in the increasing popularity of screwcaps for everyday wines, is a key driver. Concurrently, a segment of consumers, particularly in premium and fine wine categories, continues to favor the traditional allure and perceived quality associated with natural cork. This dichotomy presents opportunities for manufacturers to innovate across the spectrum, offering tailored solutions for diverse wine types and consumer expectations.

The market penetration of innovative closures, including technical corks and advanced synthetic options, is steadily increasing as wineries seek to minimize spoilage and extend shelf life, thereby reducing wine waste. This trend is further amplified by the growing awareness of environmental concerns, leading to a stronger demand for closures made from recycled, recyclable, or biodegradable materials. The interplay of these factors is creating a dynamic growth trajectory for the wine bottle closures industry, with significant opportunities for players who can effectively adapt to these evolving trends.

Dominant Regions, Countries, or Segments in Wine Bottle Closures

The global wine bottle closures market is characterized by regional dominance driven by established wine-producing nations and burgeoning new markets. Within the application segment, Still Wine represents the dominant market, accounting for the lion's share of closure consumption due to its higher production volume compared to sparkling wine. This segment's growth is fueled by consistent global demand for still wines across all price points.

Among the closure types, Screwcaps are a significant growth engine, particularly in regions emphasizing convenience and value. Their ease of use, reliable seal, and prevention of cork taint have made them a preferred choice for a substantial portion of the still wine market. However, Cork, particularly natural and technical corks, retains a strong foothold, especially in premium and high-end wine segments where tradition, perceived quality, and long-term aging potential are paramount.

- Dominant Region: Europe remains the cornerstone of the global wine bottle closures market. This dominance stems from its long-standing viticulture history, established wine culture, and significant production and consumption of both still and sparkling wines. Countries like France, Italy, Spain, and Germany are major consumers and innovators in wine closure technologies.

- Key Drivers in Europe: High per capita wine consumption, presence of premium wine producers, strong emphasis on wine quality and heritage, and a growing consumer demand for sustainable packaging solutions.

- Market Share & Growth Potential: Europe holds a substantial market share, driven by both established players and niche innovators. Growth is expected to be steady, with an increasing adoption of technical corks and premium screwcaps.

- Dominant Country (Emerging Growth): United States is a critical market experiencing rapid expansion. Its significant wine production, particularly in California, and a large, diverse consumer base contribute to its growing importance.

- Key Drivers in the US: Increasing domestic wine production, growing demand for convenience (screwcaps), and a rising appreciation for premium and artisanal wines (technical corks).

- Market Share & Growth Potential: The US exhibits strong growth potential, with a rising demand for innovative and eco-friendly closure solutions across various wine segments.

- Dominant Segment: Still Wine Application: This segment consistently leads due to its sheer volume.

- Key Drivers: Global popularity of red, white, and rosé wines, diverse price points catering to a broad consumer base, and the need for reliable closures that maintain wine integrity.

- Market Share & Growth Potential: Still wine applications command the largest market share, with sustained growth driven by increasing global wine consumption and evolving packaging trends.

- Dominant Type (Growth Driver): Screwcap: While cork remains significant, screwcaps are a key growth accelerator.

- Key Drivers: Consumer preference for convenience, consistent performance, absence of cork taint, and suitability for wines intended for early to medium-term consumption.

- Market Share & Growth Potential: Screwcaps are witnessing considerable growth, capturing market share from traditional closures, particularly in mid-range and everyday wines.

Wine Bottle Closures Product Landscape

The wine bottle closures product landscape is characterized by continuous innovation aimed at enhancing wine quality, shelf life, and sustainability. Leading companies are focusing on developing closures with advanced oxygen management properties, ensuring optimal aging and preventing spoilage. Innovations include multi-layer barrier technologies in screwcaps, sophisticated micro-oxygenation control in technical corks, and the development of novel synthetic and plastic closures with improved inertness and sealing capabilities. Furthermore, the demand for aesthetic appeal and brand differentiation is driving the development of customizable closures with premium finishes and integrated security features, catering to the evolving needs of wineries seeking to enhance their product's visual impact and consumer trust.

Key Drivers, Barriers & Challenges in Wine Bottle Closures

The wine bottle closures market is propelled by several key drivers. Technological advancements in materials and manufacturing processes are enabling the creation of closures that offer superior performance, such as enhanced oxygen control and extended shelf life. The growing global demand for wine, particularly in emerging markets, directly translates to an increased need for closures. Furthermore, a significant driver is the increasing consumer preference for sustainable and eco-friendly packaging solutions, which is spurring innovation in biodegradable and recyclable closure materials. Economic growth in developing nations also plays a crucial role, boosting disposable incomes and wine consumption.

- Technological Drivers: Advanced barrier technologies, improved sealing mechanisms, sustainable material development.

- Economic Drivers: Rising global wine consumption, increasing disposable incomes in emerging markets.

- Policy Drivers: Growing emphasis on environmental regulations promoting sustainable packaging.

However, the market faces significant barriers and challenges. Fluctuations in raw material prices, particularly for natural cork and aluminum, can impact production costs and pricing strategies. Supply chain disruptions, as evidenced by recent global events, pose a persistent threat to consistent availability and timely delivery. Regulatory hurdles related to food contact materials and environmental standards can create complexities for new product development and market entry. Intense competition among closure manufacturers, leading to price pressures, is another considerable challenge.

- Supply Chain Issues: Volatility in raw material availability and pricing.

- Regulatory Hurdles: Compliance with evolving food safety and environmental standards.

- Competitive Pressures: Price sensitivity and market saturation in certain segments.

Emerging Opportunities in Wine Bottle Closures

Emerging opportunities in the wine bottle closures market are largely driven by evolving consumer preferences and technological advancements. The growing demand for convenience and ease of use is creating opportunities for innovative screwcap designs and easy-open synthetic closures, particularly for wines intended for immediate consumption. Furthermore, the increasing focus on sustainability is opening doors for closures made from recycled, biodegradable, and plant-based materials, appealing to environmentally conscious consumers. The "smart closure" concept, integrating features like tamper detection, authentication, and even limited IoT capabilities, presents a significant untapped market, offering enhanced product security and consumer engagement. Growth in the RTD (Ready-to-Drink) beverage segment also presents an ancillary opportunity for specialized closure solutions.

Growth Accelerators in the Wine Bottle Closures Industry

Several catalysts are accelerating long-term growth in the wine bottle closures industry. The continuous innovation in material science and manufacturing technology is a primary accelerator, leading to closures that offer superior wine preservation, reduced spoilage, and enhanced sustainability. Strategic partnerships between closure manufacturers and leading wineries are crucial for co-developing bespoke solutions tailored to specific wine profiles and market demands. Market expansion into high-growth regions, particularly in Asia and South America, where wine consumption is rapidly increasing, presents substantial growth opportunities. The increasing adoption of technical corks and advanced screwcaps in premium wine segments is also a significant growth accelerator, as wineries invest in quality and consumer confidence.

Key Players Shaping the Wine Bottle Closures Market

- Amorim

- MASilva

- Cork Supply

- Vinvention

- Guala Closures Group

- Labrenta

- DIAM

- Precision Elite

- Waterloo Container Company

- AMCOR

- Astro

- Inspiral

- Orora

- Federfin Tech

- Bericap

- Interpack

Notable Milestones in Wine Bottle Closures Sector

- 2019: Launch of new generation of technical corks with enhanced oxygen management by Amorim.

- 2020: Guala Closures Group acquires a significant stake in a key producer of aluminum screwcaps, expanding its market reach.

- 2021: Vinvention introduces a new range of biodegradable synthetic closures to meet growing sustainability demands.

- 2022: MASilva develops an innovative natural cork closure with advanced traceability features.

- 2023: Cork Supply expands its research and development into plant-based closure alternatives.

- 2024: Bericap launches a new tamper-evident closure solution for the sparkling wine segment.

In-Depth Wine Bottle Closures Market Outlook

The outlook for the wine bottle closures market remains exceptionally positive, with sustained growth driven by a confluence of factors. The ongoing pursuit of enhanced wine quality and extended shelf life will continue to fuel demand for advanced closure technologies, including technical corks and innovative screwcaps. The accelerating global adoption of sustainable packaging practices presents a significant opportunity for manufacturers offering eco-friendly and recyclable closure solutions. Strategic collaborations and market expansion into underserved regions will further bolster growth trajectories. The industry is poised for continued evolution, with a strong emphasis on innovation and responsiveness to shifting consumer preferences.

Wine Bottle Closures Segmentation

-

1. Application

- 1.1. Still Wine

- 1.2. Sparkling Wine

-

2. Types

- 2.1. Cork

- 2.2. Screwcap

- 2.3. Plastic

Wine Bottle Closures Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Wine Bottle Closures Regional Market Share

Geographic Coverage of Wine Bottle Closures

Wine Bottle Closures REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.83% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Wine Bottle Closures Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Still Wine

- 5.1.2. Sparkling Wine

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Cork

- 5.2.2. Screwcap

- 5.2.3. Plastic

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Wine Bottle Closures Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Still Wine

- 6.1.2. Sparkling Wine

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Cork

- 6.2.2. Screwcap

- 6.2.3. Plastic

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Wine Bottle Closures Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Still Wine

- 7.1.2. Sparkling Wine

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Cork

- 7.2.2. Screwcap

- 7.2.3. Plastic

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Wine Bottle Closures Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Still Wine

- 8.1.2. Sparkling Wine

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Cork

- 8.2.2. Screwcap

- 8.2.3. Plastic

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Wine Bottle Closures Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Still Wine

- 9.1.2. Sparkling Wine

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Cork

- 9.2.2. Screwcap

- 9.2.3. Plastic

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Wine Bottle Closures Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Still Wine

- 10.1.2. Sparkling Wine

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Cork

- 10.2.2. Screwcap

- 10.2.3. Plastic

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Amorim

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 MASilva

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Cork Supply

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Vinvention

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Guala Closures Group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Labrenta

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 DIAM

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Precision Elite

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Waterloo Container Company

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 AMCOR

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Astro

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Inspiral

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Orora

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Federfin Tech

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Bericap

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Interpack

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 Amorim

List of Figures

- Figure 1: Global Wine Bottle Closures Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Wine Bottle Closures Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Wine Bottle Closures Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Wine Bottle Closures Volume (K), by Application 2025 & 2033

- Figure 5: North America Wine Bottle Closures Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Wine Bottle Closures Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Wine Bottle Closures Revenue (undefined), by Types 2025 & 2033

- Figure 8: North America Wine Bottle Closures Volume (K), by Types 2025 & 2033

- Figure 9: North America Wine Bottle Closures Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Wine Bottle Closures Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Wine Bottle Closures Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Wine Bottle Closures Volume (K), by Country 2025 & 2033

- Figure 13: North America Wine Bottle Closures Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Wine Bottle Closures Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Wine Bottle Closures Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Wine Bottle Closures Volume (K), by Application 2025 & 2033

- Figure 17: South America Wine Bottle Closures Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Wine Bottle Closures Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Wine Bottle Closures Revenue (undefined), by Types 2025 & 2033

- Figure 20: South America Wine Bottle Closures Volume (K), by Types 2025 & 2033

- Figure 21: South America Wine Bottle Closures Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Wine Bottle Closures Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Wine Bottle Closures Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Wine Bottle Closures Volume (K), by Country 2025 & 2033

- Figure 25: South America Wine Bottle Closures Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Wine Bottle Closures Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Wine Bottle Closures Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Wine Bottle Closures Volume (K), by Application 2025 & 2033

- Figure 29: Europe Wine Bottle Closures Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Wine Bottle Closures Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Wine Bottle Closures Revenue (undefined), by Types 2025 & 2033

- Figure 32: Europe Wine Bottle Closures Volume (K), by Types 2025 & 2033

- Figure 33: Europe Wine Bottle Closures Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Wine Bottle Closures Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Wine Bottle Closures Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Wine Bottle Closures Volume (K), by Country 2025 & 2033

- Figure 37: Europe Wine Bottle Closures Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Wine Bottle Closures Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Wine Bottle Closures Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Wine Bottle Closures Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Wine Bottle Closures Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Wine Bottle Closures Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Wine Bottle Closures Revenue (undefined), by Types 2025 & 2033

- Figure 44: Middle East & Africa Wine Bottle Closures Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Wine Bottle Closures Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Wine Bottle Closures Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Wine Bottle Closures Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Wine Bottle Closures Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Wine Bottle Closures Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Wine Bottle Closures Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Wine Bottle Closures Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Wine Bottle Closures Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Wine Bottle Closures Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Wine Bottle Closures Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Wine Bottle Closures Revenue (undefined), by Types 2025 & 2033

- Figure 56: Asia Pacific Wine Bottle Closures Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Wine Bottle Closures Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Wine Bottle Closures Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Wine Bottle Closures Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Wine Bottle Closures Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Wine Bottle Closures Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Wine Bottle Closures Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Wine Bottle Closures Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Wine Bottle Closures Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Wine Bottle Closures Revenue undefined Forecast, by Types 2020 & 2033

- Table 4: Global Wine Bottle Closures Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Wine Bottle Closures Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Wine Bottle Closures Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Wine Bottle Closures Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Wine Bottle Closures Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Wine Bottle Closures Revenue undefined Forecast, by Types 2020 & 2033

- Table 10: Global Wine Bottle Closures Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Wine Bottle Closures Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Wine Bottle Closures Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Wine Bottle Closures Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Wine Bottle Closures Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Wine Bottle Closures Revenue undefined Forecast, by Types 2020 & 2033

- Table 22: Global Wine Bottle Closures Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Wine Bottle Closures Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Wine Bottle Closures Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Wine Bottle Closures Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Wine Bottle Closures Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Wine Bottle Closures Revenue undefined Forecast, by Types 2020 & 2033

- Table 34: Global Wine Bottle Closures Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Wine Bottle Closures Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Wine Bottle Closures Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Wine Bottle Closures Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Wine Bottle Closures Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Wine Bottle Closures Revenue undefined Forecast, by Types 2020 & 2033

- Table 58: Global Wine Bottle Closures Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Wine Bottle Closures Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Wine Bottle Closures Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Wine Bottle Closures Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Wine Bottle Closures Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Wine Bottle Closures Revenue undefined Forecast, by Types 2020 & 2033

- Table 76: Global Wine Bottle Closures Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Wine Bottle Closures Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Wine Bottle Closures Volume K Forecast, by Country 2020 & 2033

- Table 79: China Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Wine Bottle Closures Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Wine Bottle Closures Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Wine Bottle Closures?

The projected CAGR is approximately 5.83%.

2. Which companies are prominent players in the Wine Bottle Closures?

Key companies in the market include Amorim, MASilva, Cork Supply, Vinvention, Guala Closures Group, Labrenta, DIAM, Precision Elite, Waterloo Container Company, AMCOR, Astro, Inspiral, Orora, Federfin Tech, Bericap, Interpack.

3. What are the main segments of the Wine Bottle Closures?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Wine Bottle Closures," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Wine Bottle Closures report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Wine Bottle Closures?

To stay informed about further developments, trends, and reports in the Wine Bottle Closures, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence