Key Insights

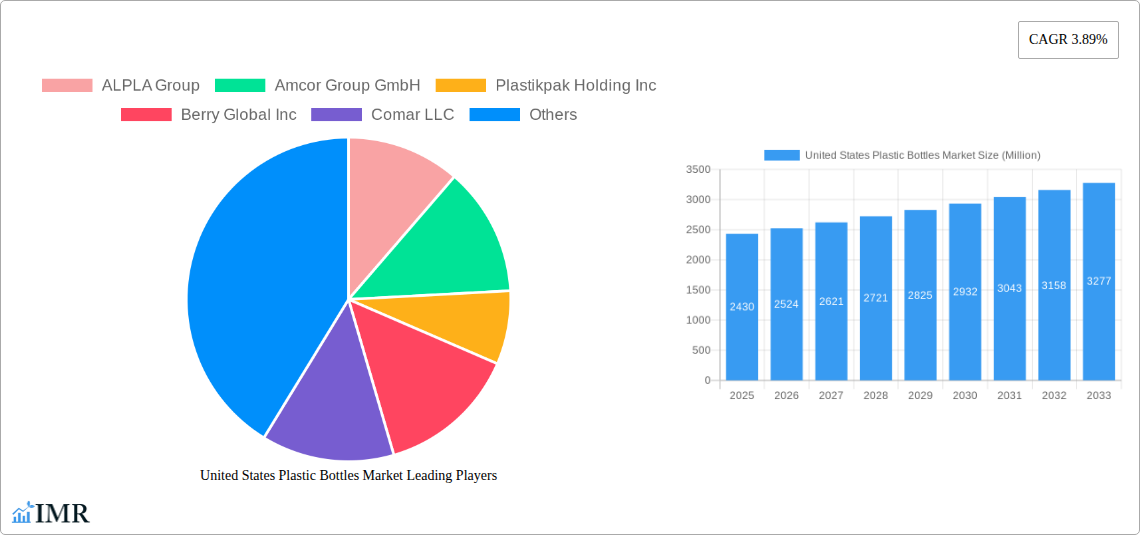

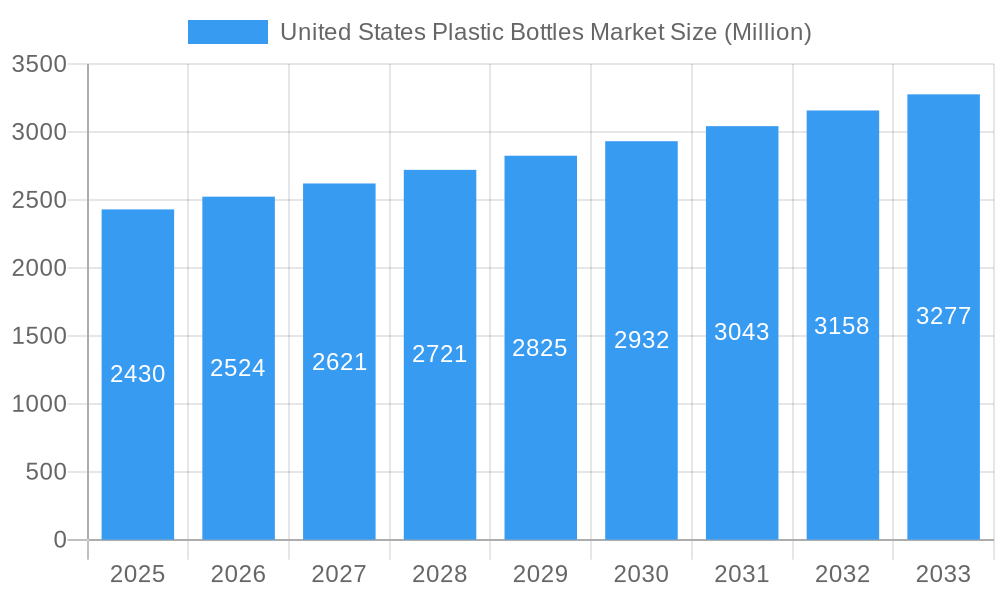

The United States plastic bottles market is poised for steady growth, projected to reach approximately $2.43 billion by 2025. This expansion is underpinned by a Compound Annual Growth Rate (CAGR) of 3.89% over the forecast period (2025-2033), indicating a robust and sustained demand for plastic packaging solutions. A primary driver for this market is the ever-increasing consumption across key end-use industries, particularly food and beverages. The convenience, durability, and cost-effectiveness of plastic bottles make them the preferred choice for a vast array of products, from bottled water and carbonated soft drinks to juices and energy drinks. Furthermore, the pharmaceutical and personal care & toiletries sectors continue to rely heavily on plastic bottles for product safety, hygiene, and consumer appeal. While concerns regarding environmental sustainability are influencing market dynamics, innovation in recyclable and biodegradable plastic materials is helping to mitigate these restraints and foster continued adoption.

United States Plastic Bottles Market Market Size (In Billion)

The market's trajectory is further shaped by evolving consumer preferences and industry trends. A significant trend is the rising demand for sustainable packaging options, prompting manufacturers to invest in advanced recycling technologies and the development of bio-based plastics. This focus on recyclability is a crucial factor in addressing environmental concerns and ensuring the long-term viability of the plastic bottle market. Within the resin segment, Polyethylene Terephthalate (PET) is expected to maintain its dominance due to its excellent clarity, strength, and barrier properties, making it ideal for beverage packaging. Polyethylene (PE) and Polypropylene (PP) will also continue to hold significant market share, catering to a diverse range of applications. The competitive landscape features a mix of established global players like ALPLA Group and Amcor Group, alongside emerging companies, all vying for market share through product innovation, strategic partnerships, and a focus on meeting the evolving needs of diverse end-use industries.

United States Plastic Bottles Market Company Market Share

United States Plastic Bottles Market Report: Comprehensive Analysis & Future Outlook (2019-2033)

Gain unparalleled insights into the dynamic United States plastic bottles market with this in-depth report. Covering the study period of 2019–2033, with a base and estimated year of 2025, this analysis delves into market size, growth trends, competitive landscapes, and emerging opportunities. Essential for stakeholders including manufacturers, suppliers, investors, and regulatory bodies, this report provides a granular view of parent and child market segments, crucial for strategic decision-making in the ever-evolving packaging industry. All values are presented in Million units for clarity.

United States Plastic Bottles Market Market Dynamics & Structure

The United States plastic bottles market exhibits a moderately consolidated structure, with key players like ALPLA Group, Amcor Group GmbH, and Berry Global Inc. dominating a significant portion of the market share. Technological innovation is a primary driver, with continuous advancements in lighter-weight designs, barrier properties, and sustainable materials like rPET. Regulatory frameworks, particularly concerning single-use plastics and recycled content mandates, are shaping market dynamics and pushing for increased sustainability. Competitive product substitutes, such as glass, metal cans, and paper-based packaging, present a constant challenge, albeit plastic's inherent advantages in cost, durability, and flexibility often prevail. End-user demographics, driven by convenience-seeking consumers and a growing demand for single-serve packaging in beverages and personal care, are influencing product development. Mergers and acquisitions (M&A) are active, with companies seeking to expand their geographic reach, product portfolios, and sustainable packaging capabilities. For instance, the acquisition of smaller specialized bottle manufacturers by larger conglomerates can bolster market share and technological expertise. Innovation barriers, such as the high cost of developing and implementing new sustainable technologies and the need for significant capital investment in new production lines, are also notable.

- Market Concentration: Moderately consolidated with leading players holding substantial market share.

- Technological Innovation: Driven by advancements in lightweighting, barrier technologies, and sustainable materials (e.g., rPET).

- Regulatory Influence: Growing impact of regulations on recycled content and single-use plastic reduction.

- Competitive Landscape: Ongoing competition from alternative packaging materials like glass, metal, and paper.

- End-User Demand: Influenced by convenience, portability, and increasing consumer preference for sustainable packaging options.

- M&A Activity: Strategic acquisitions to enhance market presence, product offerings, and sustainability initiatives.

United States Plastic Bottles Market Growth Trends & Insights

The United States plastic bottles market is projected for robust growth driven by evolving consumer preferences, technological advancements in sustainable packaging, and the expansion of key end-use industries. The market size evolution is characterized by a steady upward trajectory, propelled by the sheer volume of consumption across food, beverage, pharmaceutical, and personal care sectors. Adoption rates for innovative bottle designs and sustainable materials are accelerating, influenced by both consumer demand and regulatory pressures. Technological disruptions, such as improved recycling processes and the development of advanced barrier coatings for extended shelf life, are further stimulating market expansion.

Consumer behavior shifts are playing a pivotal role. There's a growing awareness and demand for eco-friendly packaging, leading to increased preference for bottles made from recycled content (rPET) and a surge in demand for smaller, more convenient packaging formats. The convenience offered by plastic bottles, their lightweight nature, and their cost-effectiveness continue to be significant adoption drivers. For instance, the bottled water segment, a major consumer of plastic bottles, is expected to see sustained growth due to increased health consciousness and on-the-go consumption patterns. Similarly, the personal care and toiletries sector relies heavily on plastic bottles for product safety and ease of use, contributing to consistent market demand. The increasing focus on a circular economy is pushing manufacturers to invest in technologies that enable higher percentages of recycled content, thereby influencing the overall growth trajectory and market penetration of sustainable plastic bottle solutions. The forecast period of 2025–2033 anticipates a Compound Annual Growth Rate (CAGR) of approximately 3.5% to 4.2%, underscoring the sustained momentum of the United States plastic bottles market. The market penetration of PET bottles, especially in the beverage sector, remains exceptionally high, expected to reach over 85% of the total beverage packaging by 2030. The increasing investment in recycling infrastructure and government incentives for using recycled materials are crucial factors supporting this growth.

Dominant Regions, Countries, or Segments in United States Plastic Bottles Market

The United States plastic bottles market is largely dominated by the Beverage end-use industry, specifically within the Bottled Water and Carbonated Soft Drinks sub-segments. This dominance is propelled by several key factors, including vast consumer demand, established distribution networks, and the inherent suitability of plastic for packaging these high-volume products. The convenience, durability, and cost-effectiveness of plastic bottles, particularly PET, make them the preferred choice for beverage manufacturers aiming for widespread market reach and affordability for consumers.

Beverage Sector Dominance: This segment accounts for the largest share of the United States plastic bottles market, estimated to be over 50% of the total market value.

- Bottled Water: Driven by increasing health consciousness, hydration awareness, and the demand for portable, convenient hydration solutions. Market share within beverages is approximately 25-30 million units.

- Carbonated Soft Drinks (CSDs): A mature but consistently large market, benefiting from established brands and widespread availability. Market share within beverages is approximately 20-25 million units.

- Other Beverages (Juices & Energy Drinks, Alcoholic Beverages, Other Beverages): These sub-segments also contribute significantly, with growing demand for specialized packaging solutions.

Resin Dominance: Polyethylene Terephthalate (PET) is the overwhelmingly dominant resin type, accounting for an estimated 75-80% of all plastic bottles produced in the U.S. Its excellent clarity, barrier properties, and recyclability make it ideal for beverage packaging.

- PET: Its widespread adoption is a direct result of its suitability for food and beverage applications, offering a good balance of performance and cost. Market share is in excess of 300 million units.

- Polyethylene (PE) and Polypropylene (PP): These resins hold significant shares in other end-use industries like Personal Care & Toiletries and Household Chemicals due to their flexibility and chemical resistance, but they are secondary to PET in overall market volume for bottles. PE holds approximately 15-20% market share and PP approximately 5-10% market share.

Regional Influence: While the entire United States constitutes the market, states with higher population density and significant manufacturing hubs, such as California, Texas, and the Northeast corridor, exhibit the highest consumption and production of plastic bottles. These regions benefit from robust economic activity, extensive distribution networks, and a large consumer base, further solidifying their dominance.

United States Plastic Bottles Market Product Landscape

The product landscape of the United States plastic bottles market is characterized by a relentless pursuit of innovation aimed at enhancing functionality, sustainability, and consumer appeal. Innovations span across material science, design, and manufacturing processes. The increasing demand for lightweight bottles, reducing material usage without compromising structural integrity, is a significant trend. Furthermore, advancements in barrier technologies for PET bottles are extending the shelf life of sensitive products, particularly in the food and beverage sectors. The integration of high percentages of recycled content, especially post-consumer recycled PET (rPET), is a paramount innovation, driven by both consumer demand and stringent environmental regulations. Unique selling propositions are increasingly tied to the sustainability credentials of the bottles, with brands highlighting their commitment to circularity and reduced environmental impact. Technological advancements also include the development of specialized closures and dispensing systems that enhance user experience and product safety.

Key Drivers, Barriers & Challenges in United States Plastic Bottles Market

Key Drivers:

- Growing Beverage Consumption: The sustained demand for bottled water, soft drinks, and other beverages fuels the need for plastic bottles.

- Convenience and Portability: Plastic bottles offer unmatched convenience for on-the-go consumption across various demographics.

- Cost-Effectiveness: Plastic remains a highly economical packaging material compared to alternatives.

- Technological Advancements: Innovations in lightweighting, barrier properties, and sustainable materials like rPET are driving adoption.

- Regulatory Support for Recycling: Government initiatives and mandates promoting recycled content are encouraging the use of rPET.

Key Barriers & Challenges:

- Environmental Concerns and Plastic Waste: Negative public perception and growing pressure to reduce plastic waste and pollution.

- Fluctuating Resin Prices: Volatility in the cost of raw materials like PET and PE can impact profit margins.

- Competition from Alternative Materials: Increasing adoption of glass, metal, and paper-based packaging in certain applications.

- Infrastructure for Recycling: Inconsistent and insufficient collection and recycling infrastructure across different regions.

- Regulatory Hurdles: Evolving and sometimes stringent regulations regarding plastic usage, recyclability, and post-consumer recycled content can pose compliance challenges. For example, evolving Extended Producer Responsibility (EPR) schemes are a significant factor to monitor.

Emerging Opportunities in United States Plastic Bottles Market

Emerging opportunities in the United States plastic bottles market lie in the expanded use of advanced recycling technologies, such as chemical recycling, which can process a wider range of plastic waste and create higher-quality recycled materials. The development of bio-based and biodegradable plastic alternatives, while still in their nascent stages, presents a long-term growth avenue. Furthermore, the increasing demand for personalized and functional packaging, including smart bottles with integrated sensors or unique dispensing mechanisms, offers niche market potential. The growth of e-commerce also presents opportunities for optimized, durable, and lightweight plastic bottle designs that can withstand the rigors of shipping.

Growth Accelerators in the United States Plastic Bottles Market Industry

Several catalysts are accelerating the long-term growth of the United States plastic bottles market. Technological breakthroughs in material science, leading to the development of stronger, lighter, and more easily recyclable plastics, are critical. Strategic partnerships between resin manufacturers, bottle producers, and brand owners are essential for driving innovation and scaling sustainable solutions. Market expansion strategies, particularly in emerging consumer segments and through the development of specialized packaging for niche beverages and personal care products, will also contribute significantly. The increasing investment in advanced recycling infrastructure and the development of circular economy models are fundamental growth accelerators, promising a more sustainable future for plastic packaging.

Key Players Shaping the United States Plastic Bottles Market Market

- ALPLA Group

- Amcor Group GmbH

- Plastikpak Holding Inc

- Berry Global Inc

- Comar LLC

- Cole-Parmer Instrument Company LLC

- Sailor Plastics Inc

- Plastic Bottle Corporation

- Thornton Plastics

Notable Milestones in United States Plastic Bottles Market Sector

- February 2024: Califia Farms transitioned all its U.S. bottles to 100% recycled plastic (rPET), projected to reduce greenhouse gas emissions by at least 19% and halve energy consumption, demonstrating a commitment to a cleaner planet.

- January 2024: Coca-Cola UNITED unveiled its initiative to transition select top-selling 20-ounce plastic products to bottles made entirely from 100% recycled plastic (rPET), reinforcing its commitment to reducing virgin plastic and achieving a World Without Waste. This move included integrating 100% recycled plastic bottles into offerings like 12-ounce, 20-ounce, and 1-liter DASANI bottles.

In-Depth United States Plastic Bottles Market Market Outlook

The United States plastic bottles market is poised for continued expansion, driven by an increasing demand for convenient and sustainable packaging solutions. The ongoing integration of recycled content, particularly rPET, will be a major growth propeller, supported by both consumer preference and regulatory mandates. Innovations in lightweighting and advanced barrier technologies will enhance product performance and reduce material usage, contributing to greater efficiency. The market's future outlook is characterized by a strong focus on circular economy principles, with significant investments expected in recycling infrastructure and advanced recycling technologies. Strategic collaborations among industry players will be crucial for navigating evolving environmental regulations and consumer expectations, ensuring a dynamic and resilient market for plastic bottles.

United States Plastic Bottles Market Segmentation

-

1. Resin

- 1.1. Polyethylene (PE)

- 1.2. Polyethylene Terephthalate (PET)

- 1.3. Polypropylene (PP)

- 1.4. Other Re

-

2. End-use Industries

- 2.1. Food

-

2.2. Beverage

- 2.2.1. Bottled Water

- 2.2.2. Carbonated Soft Drinks

- 2.2.3. Alcoholic Beverages

- 2.2.4. Juices & Energy Drinks

- 2.2.5. Other Beverages

- 2.3. Pharmaceuticals

- 2.4. Personal Care & Toiletries

- 2.5. Industrial

- 2.6. Household Chemicals

- 2.7. Paints & Coatings

- 2.8. Other End-use Industries

United States Plastic Bottles Market Segmentation By Geography

- 1. United States

United States Plastic Bottles Market Regional Market Share

Geographic Coverage of United States Plastic Bottles Market

United States Plastic Bottles Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.89% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Resin

- 5.1.1. Polyethylene (PE)

- 5.1.2. Polyethylene Terephthalate (PET)

- 5.1.3. Polypropylene (PP)

- 5.1.4. Other Re

- 5.2. Market Analysis, Insights and Forecast - by End-use Industries

- 5.2.1. Food

- 5.2.2. Beverage

- 5.2.2.1. Bottled Water

- 5.2.2.2. Carbonated Soft Drinks

- 5.2.2.3. Alcoholic Beverages

- 5.2.2.4. Juices & Energy Drinks

- 5.2.2.5. Other Beverages

- 5.2.3. Pharmaceuticals

- 5.2.4. Personal Care & Toiletries

- 5.2.5. Industrial

- 5.2.6. Household Chemicals

- 5.2.7. Paints & Coatings

- 5.2.8. Other End-use Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.1. Market Analysis, Insights and Forecast - by Resin

- 6. United States Plastic Bottles Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Resin

- 6.1.1. Polyethylene (PE)

- 6.1.2. Polyethylene Terephthalate (PET)

- 6.1.3. Polypropylene (PP)

- 6.1.4. Other Re

- 6.2. Market Analysis, Insights and Forecast - by End-use Industries

- 6.2.1. Food

- 6.2.2. Beverage

- 6.2.2.1. Bottled Water

- 6.2.2.2. Carbonated Soft Drinks

- 6.2.2.3. Alcoholic Beverages

- 6.2.2.4. Juices & Energy Drinks

- 6.2.2.5. Other Beverages

- 6.2.3. Pharmaceuticals

- 6.2.4. Personal Care & Toiletries

- 6.2.5. Industrial

- 6.2.6. Household Chemicals

- 6.2.7. Paints & Coatings

- 6.2.8. Other End-use Industries

- 6.1. Market Analysis, Insights and Forecast - by Resin

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 ALPLA Group

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Amcor Group GmbH

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Plastikpak Holding Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Berry Global Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Comar LLC

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Cole-Parmer Instrument Company LLC

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Sailor Plastics Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Plastic Bottle Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Thornton Plastics7 2 Competitor Analysis - Emerging vs Established Player

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 ALPLA Group

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United States Plastic Bottles Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: United States Plastic Bottles Market Share (%) by Company 2025

List of Tables

- Table 1: United States Plastic Bottles Market Revenue Million Forecast, by Resin 2020 & 2033

- Table 2: United States Plastic Bottles Market Volume Billion Forecast, by Resin 2020 & 2033

- Table 3: United States Plastic Bottles Market Revenue Million Forecast, by End-use Industries 2020 & 2033

- Table 4: United States Plastic Bottles Market Volume Billion Forecast, by End-use Industries 2020 & 2033

- Table 5: United States Plastic Bottles Market Revenue Million Forecast, by Region 2020 & 2033

- Table 6: United States Plastic Bottles Market Volume Billion Forecast, by Region 2020 & 2033

- Table 7: United States Plastic Bottles Market Revenue Million Forecast, by Resin 2020 & 2033

- Table 8: United States Plastic Bottles Market Volume Billion Forecast, by Resin 2020 & 2033

- Table 9: United States Plastic Bottles Market Revenue Million Forecast, by End-use Industries 2020 & 2033

- Table 10: United States Plastic Bottles Market Volume Billion Forecast, by End-use Industries 2020 & 2033

- Table 11: United States Plastic Bottles Market Revenue Million Forecast, by Country 2020 & 2033

- Table 12: United States Plastic Bottles Market Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States Plastic Bottles Market?

The projected CAGR is approximately 3.89%.

2. Which companies are prominent players in the United States Plastic Bottles Market?

Key companies in the market include ALPLA Group, Amcor Group GmbH, Plastikpak Holding Inc, Berry Global Inc, Comar LLC, Cole-Parmer Instrument Company LLC, Sailor Plastics Inc, Plastic Bottle Corporation, Thornton Plastics7 2 Competitor Analysis - Emerging vs Established Player.

3. What are the main segments of the United States Plastic Bottles Market?

The market segments include Resin, End-use Industries.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.43 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Recycling and Other Cost-Effective Initiatives are Bolstering the Demand; Increasing Demand From Bottled-Water and Beverage Industry Aids the Market.

6. What are the notable trends driving market growth?

Demand for Polyethylene Terephthalate (PET) Bottles.

7. Are there any restraints impacting market growth?

Growing Recycling and Other Cost-Effective Initiatives are Bolstering the Demand; Increasing Demand From Bottled-Water and Beverage Industry Aids the Market.

8. Can you provide examples of recent developments in the market?

February 2024 - Califia Farms, a prominent brand in the premium plant-based beverage sector, has announced a significant packaging update. The brand has transitioned all its bottles in the U.S. to 100% recycled plastic (rPET). This initiative is projected to reduce the company's greenhouse gas emissions by a minimum of 19% and halve its energy consumption. This move underscores Califia's steadfast commitment to promoting a cleaner, healthier planet and its endeavors to diminish the demand for new plastic.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States Plastic Bottles Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States Plastic Bottles Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States Plastic Bottles Market?

To stay informed about further developments, trends, and reports in the United States Plastic Bottles Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence