Key Insights

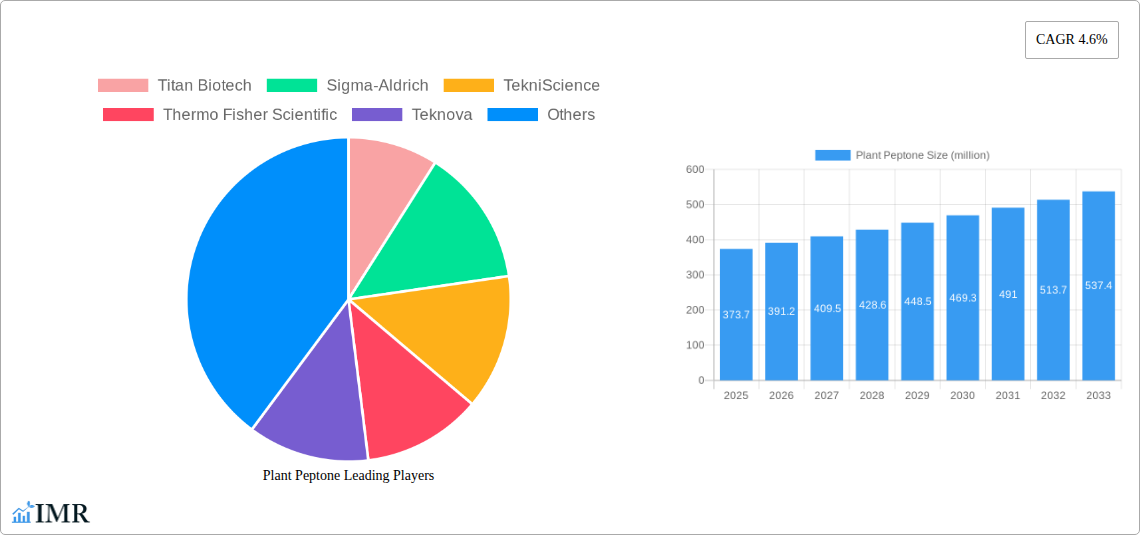

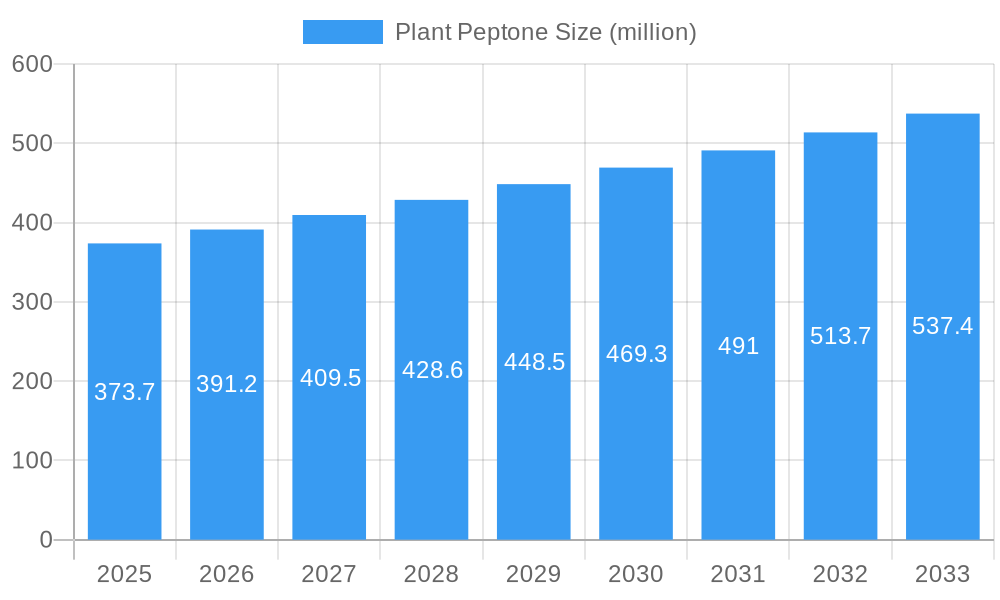

The global Plant Peptone market is poised for substantial growth, projected to reach an estimated $373.7 million in 2025, with a robust Compound Annual Growth Rate (CAGR) of 4.6% anticipated over the forecast period extending to 2033. This expansion is primarily fueled by the increasing demand for sustainable and plant-based ingredients across various industries. The pharmaceutical sector stands out as a significant driver, leveraging plant peptones for cell culture media, fermentation processes, and vaccine production due to their allergen-free and consistent properties. Similarly, the food industry is witnessing a surge in demand for plant peptones as functional ingredients, flavor enhancers, and nutrient supplements, aligning with the growing consumer preference for clean-label products and plant-based diets. The "Others" application segment, encompassing cosmetics and animal feed, also contributes to this upward trajectory, reflecting the versatility of plant peptone derivatives.

Plant Peptone Market Size (In Million)

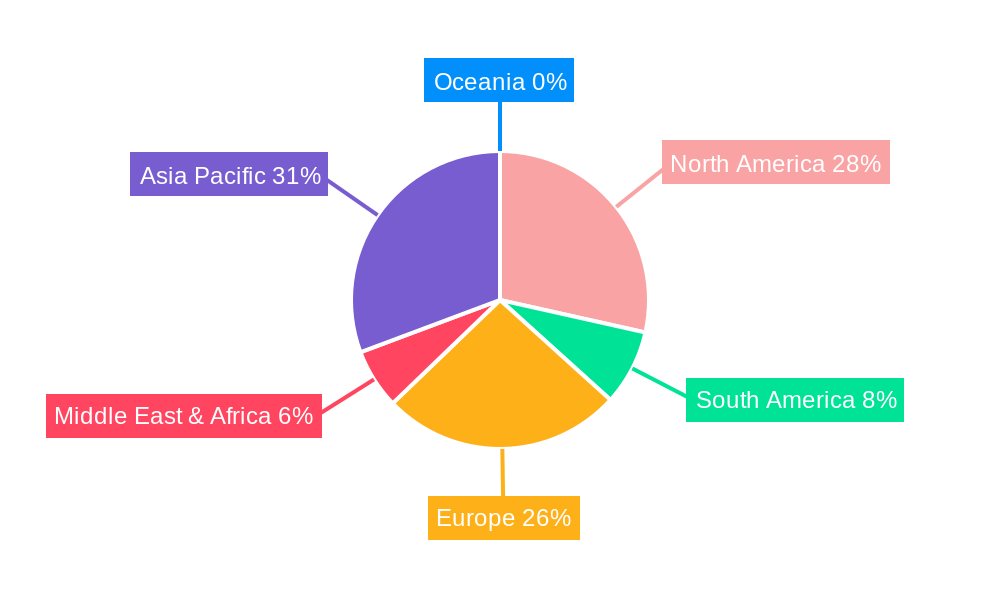

Emerging trends such as advancements in extraction and purification technologies are enhancing the quality and bioavailability of plant peptones, further propelling market adoption. These innovations are making plant peptones a more attractive alternative to animal-derived components. The market's growth, however, faces certain restraints including the cost-effectiveness of production compared to established animal-derived counterparts and the need for standardized regulatory frameworks to ensure product safety and efficacy across different regions. Nonetheless, the ongoing research and development efforts aimed at optimizing production processes and exploring novel applications are expected to mitigate these challenges. Geographically, the Asia Pacific region is anticipated to exhibit significant growth, driven by the expanding biopharmaceutical industry in China and India, coupled with a rising awareness of sustainable food production. North America and Europe, with their established pharmaceutical and food industries, will continue to hold substantial market shares.

Plant Peptone Company Market Share

Plant Peptone Market: Comprehensive Growth Analysis, Opportunities, and Key Player Insights (2019–2033)

This in-depth market research report provides a holistic view of the global Plant Peptone market, meticulously analyzing its dynamics, growth trajectory, and future potential. Covering the period from 2019 to 2033, with a base and estimated year of 2025, the report offers actionable insights for stakeholders across the pharmaceutical industry, food industry, and other diverse applications. We delve into the market's structure, examine emerging trends, identify dominant segments and regions, and profile key players shaping the industry. This report is your definitive guide to understanding the plant-based protein hydrolysates market, including bean peptone, wheat peptone, and other critical plant peptone types.

Plant Peptone Market Dynamics & Structure

The Plant Peptone market is characterized by a moderately concentrated structure, with key players investing heavily in research and development to drive technological innovation. Drivers of growth include the increasing demand for sustainable and plant-based ingredients, the rising awareness of protein's health benefits, and advancements in enzymatic hydrolysis and fermentation technologies for improved peptone quality. Regulatory frameworks, particularly concerning food safety and ingredient sourcing, play a crucial role in shaping market access and product development. Competitive product substitutes, such as animal-derived peptones and other protein sources, present a continuous challenge, necessitating ongoing innovation and cost-effectiveness. End-user demographics increasingly favor natural, ethically sourced ingredients, pushing manufacturers towards plant-based alternatives. Mergers and acquisitions (M&A) are active, consolidating market share and expanding product portfolios, as companies seek to leverage synergies and gain access to new technologies and markets.

- Market Concentration: Moderate, with a few leading players holding significant market share.

- Technological Innovation Drivers: Enzymatic hydrolysis, fermentation, protein engineering for enhanced bioavailability and functionality.

- Regulatory Frameworks: Focus on GRAS status, food safety standards (e.g., HACCP, ISO), and country-specific ingredient approvals.

- Competitive Product Substitutes: Animal-derived peptones (e.g., bovine, porcine), soy protein isolates, whey protein concentrates.

- End-User Demographics: Growing demand from health-conscious consumers, vegans, vegetarians, and individuals with dietary restrictions.

- M&A Trends: Strategic acquisitions to enhance product portfolios, expand geographical reach, and secure supply chains.

Plant Peptone Growth Trends & Insights

The global Plant Peptone market is poised for substantial expansion, driven by a confluence of evolving consumer preferences, technological advancements, and a growing emphasis on sustainable sourcing. The market size is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 8.5% from 2025 to 2033, reaching an estimated value of $1,250 million in 2033 from $720 million in 2025. This growth trajectory is fueled by increasing adoption rates across the pharmaceutical industry, where plant peptones are utilized in cell culture media, vaccine production, and diagnostics due to their purity and lack of zoonotic risk. In the food industry, plant peptones are gaining traction as functional ingredients, flavor enhancers, and protein supplements in plant-based meat alternatives, dairy substitutes, and sports nutrition products. Technological disruptions, including the development of novel extraction and purification techniques, are enhancing the bioavailability and functional properties of plant peptones, further stimulating demand. Consumer behavior shifts towards plant-centric diets and a demand for transparent ingredient sourcing are key accelerators. The market penetration of plant peptones is expected to deepen as manufacturers innovate to overcome taste and texture challenges in food applications and demonstrate superior performance in biotechnological processes.

- Market Size Evolution: Projected to grow from $720 million in 2025 to $1,250 million by 2033.

- Adoption Rates: Increasing across the pharmaceutical sector for cell culture and diagnostics, and in the food industry for plant-based product development.

- Technological Disruptions: Advances in enzymatic hydrolysis, membrane filtration, and spray-drying for improved quality and functionality.

- Consumer Behavior Shifts: Growing preference for vegan, vegetarian, and flexitarian diets, and increased demand for sustainable and traceable ingredients.

- Market Penetration: Deepening in both established and emerging markets as product development and awareness increase.

Dominant Regions, Countries, or Segments in Plant Peptone

The Pharmaceutical Industry segment is a significant driver of the global Plant Peptone market, projected to hold a market share of approximately 45% by 2025. This dominance is attributed to the critical role of peptones in providing essential amino acids and growth factors for microbial fermentation, cell culture, and the production of biopharmaceuticals, vaccines, and diagnostic kits. The inherent advantage of plant peptones in eliminating the risk of prion or viral contamination associated with animal-derived counterparts further solidifies their position in this highly regulated sector.

Within the Types segment, Beans are anticipated to lead, accounting for a substantial portion of the market. Bean-derived peptones, particularly from sources like soy and pea, offer excellent nutritional profiles and are widely available, contributing to their popularity. Their high protein content and favorable amino acid composition make them suitable for a broad range of applications.

Geographically, North America is expected to emerge as the dominant region, driven by a strong presence of leading pharmaceutical and food manufacturers, robust R&D investments, and high consumer awareness regarding health and sustainability. The region’s advanced regulatory landscape also supports the adoption of novel ingredients like plant peptones. Favorable government initiatives promoting biotechnology and plant-based food innovation further bolster growth in North America.

- Dominant Application Segment: Pharmaceutical Industry (estimated 45% market share by 2025)

- Key Drivers: Biopharmaceutical production, cell culture media, vaccine development, diagnostics.

- Growth Potential: Continuous innovation in bioprocessing and increasing demand for novel therapeutics.

- Dominant Type Segment: Beans (projected to lead in market share)

- Key Drivers: High protein content, favorable amino acid profile, wide availability, and cost-effectiveness.

- Growth Potential: Expansion into new food and pharmaceutical applications.

- Dominant Region: North America

- Key Drivers: Presence of major biopharmaceutical and food companies, strong R&D infrastructure, high consumer demand for plant-based and sustainable products, supportive regulatory environment.

- Market Share: Estimated to hold over 30% of the global market by 2025.

Plant Peptone Product Landscape

The Plant Peptone product landscape is characterized by continuous innovation aimed at enhancing nutritional profiles, functional properties, and application versatility. Manufacturers are developing highly purified and specific peptone fractions to meet the stringent requirements of the pharmaceutical sector, particularly for sensitive cell culture applications. In the food industry, advancements focus on improving taste, texture, and solubility to better integrate plant peptones into a wider array of products, including plant-based meats, dairy alternatives, and nutritional supplements. Novel enzymatic hydrolysis techniques are yielding peptones with specific peptide chains, offering targeted health benefits and improved digestibility. These advancements ensure that plant peptones are not just protein sources but also functional ingredients that contribute to product efficacy and consumer appeal.

Key Drivers, Barriers & Challenges in Plant Peptone

The Plant Peptone market is propelled by the escalating demand for sustainable and plant-based ingredients, driven by growing environmental consciousness and ethical consumerism. Technological advancements in enzymatic hydrolysis and fermentation processes enhance the quality and functionality of plant peptones, making them more competitive. The rising prevalence of chronic diseases and a growing focus on health and wellness further fuel demand for protein-rich ingredients.

However, the market faces several challenges. High production costs associated with specialized extraction and purification processes can limit widespread adoption. Competition from well-established animal-derived peptones and other protein sources remains a significant barrier. Regulatory hurdles in certain regions for novel food ingredients and the need for extensive validation in pharmaceutical applications can slow down market entry. Supply chain complexities and the availability of consistent, high-quality raw materials also pose challenges.

Emerging Opportunities in Plant Peptone

Emerging opportunities lie in the expansion of plant peptone applications into niche markets, such as animal nutrition and cosmetics, where their bioavailability and natural origin are highly valued. The development of specialized peptones for specific therapeutic targets, such as immune support or gut health, presents a significant avenue for growth. Furthermore, untapped markets in developing economies, with their growing middle class and increasing awareness of health and nutrition, offer substantial potential. Innovative marketing strategies highlighting the sustainability and ethical sourcing of plant peptones can also attract a broader consumer base.

Growth Accelerators in the Plant Peptone Industry

Key growth accelerators for the Plant Peptone industry include breakthroughs in cost-effective and sustainable production technologies, enabling wider market penetration. Strategic partnerships between raw material suppliers, peptone manufacturers, and end-users (pharmaceutical and food companies) are crucial for co-development and market access. The increasing focus on circular economy principles and waste valorization in agriculture offers opportunities for utilizing by-products to produce plant peptones, further enhancing sustainability and reducing costs. Government support for bio-based industries and the growing trend of ingredient transparency and clean labeling will also drive long-term growth.

Key Players Shaping the Plant Peptone Market

- Titan Biotech

- Sigma-Aldrich

- TekniScience

- Thermo Fisher Scientific

- Teknova

- Kerry

- Solabia

- Angel Yeast

- Friesland Campina Domo

- Lesaffre

- Organotechnie

- Zhongshi Duqing

- Xinhua Biochemical Tech Development

- HiMedia Laboratories

- Neogen

- Qingzhou Qidi

- Rongcheng Hongde Marine

- Zhejiang Huzhou Confluence Biology

- Liangshan Ketai Biological

Notable Milestones in Plant Peptone Sector

- 2019: Increased investment in R&D for novel enzymatic hydrolysis techniques for improved plant peptone yields and functionalities.

- 2020: Emergence of new plant-based food formulations incorporating plant peptones, driving demand in the food industry.

- 2021: Several key players expanded their product portfolios with specialized plant peptones for cell culture applications.

- 2022: Growing focus on sustainable sourcing and traceability of raw materials for plant peptone production.

- 2023: Significant advancements in purification technologies leading to higher purity plant peptones for pharmaceutical use.

- 2024: Growing regulatory approvals for plant peptones in various food and pharmaceutical applications globally.

In-Depth Plant Peptone Market Outlook

The future of the Plant Peptone market is exceptionally promising, driven by sustained demand for plant-based and sustainable solutions across vital industries. Growth accelerators such as technological innovations in bioprocessing, the continued expansion of the plant-based food sector, and the increasing reliance on cell-based manufacturing in pharmaceuticals will shape its trajectory. Strategic collaborations and a focus on product differentiation will be key for players to capture market share. The market is expected to see increased investment in research to unlock novel applications and overcome existing limitations, solidifying its position as a critical ingredient in both health and nutrition sectors.

Plant Peptone Segmentation

-

1. Application

- 1.1. Pharmaceutical Industry

- 1.2. Food Industry

- 1.3. Others

-

2. Types

- 2.1. Beans

- 2.2. Wheat

- 2.3. Others

Plant Peptone Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Plant Peptone Regional Market Share

Geographic Coverage of Plant Peptone

Plant Peptone REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Plant Peptone Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Pharmaceutical Industry

- 5.1.2. Food Industry

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Beans

- 5.2.2. Wheat

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Plant Peptone Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Pharmaceutical Industry

- 6.1.2. Food Industry

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Beans

- 6.2.2. Wheat

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Plant Peptone Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Pharmaceutical Industry

- 7.1.2. Food Industry

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Beans

- 7.2.2. Wheat

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Plant Peptone Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Pharmaceutical Industry

- 8.1.2. Food Industry

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Beans

- 8.2.2. Wheat

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Plant Peptone Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Pharmaceutical Industry

- 9.1.2. Food Industry

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Beans

- 9.2.2. Wheat

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Plant Peptone Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Pharmaceutical Industry

- 10.1.2. Food Industry

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Beans

- 10.2.2. Wheat

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Titan Biotech

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Sigma-Aldrich

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 TekniScience

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Thermo Fisher Scientific

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Teknova

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Kerry

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Solabia

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Angel Yeast

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Friesland Campina Domo

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Lesaffre

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Organotechnie

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Zhongshi Duqing

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Xinhua Biochemical Tech Development

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 HiMedia Laboratories

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Neogen

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Qingzhou Qidi

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Rongcheng Hongde Marine

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Zhejiang Huzhou Confluence Biology

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Liangshan Ketai Biological

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.1 Titan Biotech

List of Figures

- Figure 1: Global Plant Peptone Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Plant Peptone Revenue (million), by Application 2025 & 2033

- Figure 3: North America Plant Peptone Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Plant Peptone Revenue (million), by Types 2025 & 2033

- Figure 5: North America Plant Peptone Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Plant Peptone Revenue (million), by Country 2025 & 2033

- Figure 7: North America Plant Peptone Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Plant Peptone Revenue (million), by Application 2025 & 2033

- Figure 9: South America Plant Peptone Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Plant Peptone Revenue (million), by Types 2025 & 2033

- Figure 11: South America Plant Peptone Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Plant Peptone Revenue (million), by Country 2025 & 2033

- Figure 13: South America Plant Peptone Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Plant Peptone Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Plant Peptone Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Plant Peptone Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Plant Peptone Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Plant Peptone Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Plant Peptone Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Plant Peptone Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Plant Peptone Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Plant Peptone Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Plant Peptone Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Plant Peptone Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Plant Peptone Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Plant Peptone Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Plant Peptone Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Plant Peptone Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Plant Peptone Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Plant Peptone Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Plant Peptone Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Plant Peptone Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Plant Peptone Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Plant Peptone Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Plant Peptone Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Plant Peptone Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Plant Peptone Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Plant Peptone Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Plant Peptone Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Plant Peptone Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Plant Peptone Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Plant Peptone Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Plant Peptone Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Plant Peptone Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Plant Peptone Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Plant Peptone Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Plant Peptone Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Plant Peptone Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Plant Peptone Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Plant Peptone Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Plant Peptone?

The projected CAGR is approximately 4.6%.

2. Which companies are prominent players in the Plant Peptone?

Key companies in the market include Titan Biotech, Sigma-Aldrich, TekniScience, Thermo Fisher Scientific, Teknova, Kerry, Solabia, Angel Yeast, Friesland Campina Domo, Lesaffre, Organotechnie, Zhongshi Duqing, Xinhua Biochemical Tech Development, HiMedia Laboratories, Neogen, Qingzhou Qidi, Rongcheng Hongde Marine, Zhejiang Huzhou Confluence Biology, Liangshan Ketai Biological.

3. What are the main segments of the Plant Peptone?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 373.7 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Plant Peptone," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Plant Peptone report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Plant Peptone?

To stay informed about further developments, trends, and reports in the Plant Peptone, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence