Key Insights

The Africa Data Center Networking Market is projected for significant growth, expected to reach $3.49 billion by 2033, with a Compound Annual Growth Rate (CAGR) of 11.79% from the base year 2024. This expansion is driven by increasing demand for digital services, widespread cloud adoption, and the deployment of 5G and IoT technologies across Africa. Government digital transformation initiatives and the e-commerce boom are accelerating investment in data center infrastructure. Key growth factors include the necessity for high-speed, scalable network connectivity to manage escalating data volumes and the adoption of advanced networking equipment like Ethernet switches, routers, and Application Delivery Controllers (ADCs) to optimize data center performance and ensure seamless data flow.

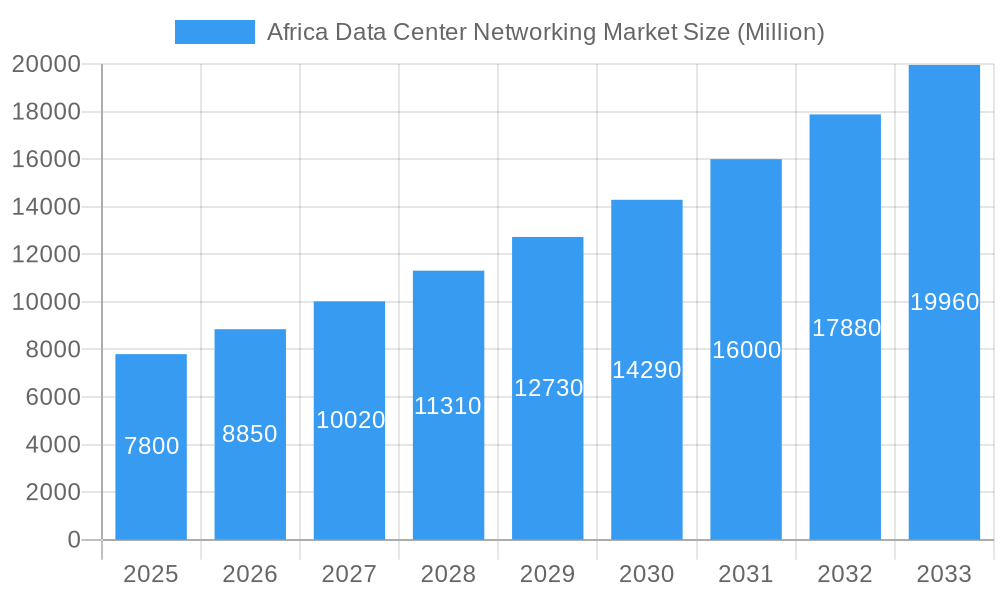

Africa Data Center Networking Market Market Size (In Billion)

Market segmentation highlights Ethernet Switches and Routers as dominant product categories due to their essential role in network infrastructure. Services, including installation, integration, training, consulting, and support, are also experiencing robust growth as organizations require expert management of complex networking environments. The IT & Telecommunication, BFSI, and Government sectors are leading in adopting advanced data center networking solutions to improve operational efficiency and data security. Challenges such as the high cost of advanced hardware and a shortage of skilled IT professionals are being addressed through investments in talent development and the availability of more cost-effective solutions, promising sustained and dynamic growth in the African data center networking market through 2033.

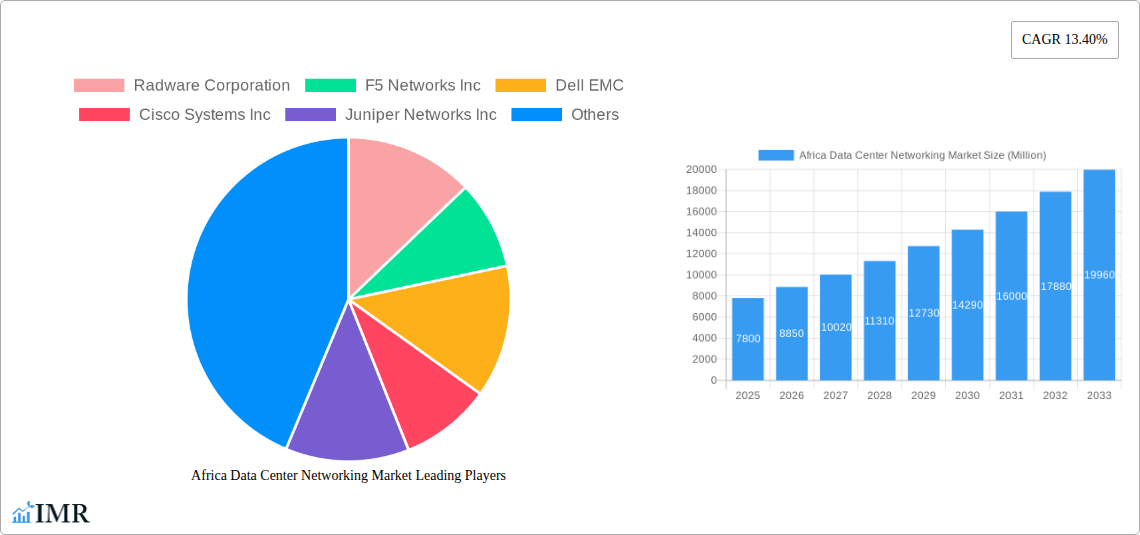

Africa Data Center Networking Market Company Market Share

Africa Data Center Networking Market Analysis: Growth, Trends, and Key Players (2019-2033)

This comprehensive report provides an in-depth analysis of the Africa Data Center Networking Market, offering critical insights into its growth trajectory, key drivers, segmentation, and competitive landscape. Delve into the evolving needs of African data centers, driven by digital transformation, cloud adoption, and the burgeoning demand for reliable and high-speed network infrastructure. We explore both parent and child markets to deliver a holistic view of this dynamic sector. This report leverages detailed market data and expert analysis to equip industry professionals with actionable intelligence for strategic decision-making.

Report Highlights:

- Market Size: Projected to reach USD 2,500 Million by 2033, with a CAGR of 12.5% during the forecast period (2025-2033).

- Study Period: 2019–2033

- Base Year: 2025

- Forecast Period: 2025–2033

- Key Segments: Ethernet Switches, Routers, SAN, ADCs, Installation & Integration, IT & Telecommunication, BFSI, Government.

- Leading Companies: Radware Corporation, F5 Networks Inc, Dell EMC, Cisco Systems Inc, Juniper Networks Inc, Extreme Networks Inc, NEC Corporation, A10 Networks Inc, Huawei Technologies Co Ltd, TP-Link Corporation Limited, Array Networks Inc, Moxa Inc, H3C Holding Limited, VMware Inc.

Africa Data Center Networking Market Market Dynamics & Structure

The Africa Data Center Networking Market is characterized by a moderate to high degree of market concentration, with established global players holding significant shares, alongside a growing number of regional providers. Technological innovation is a primary driver, fueled by the increasing demand for faster speeds, lower latency, and enhanced security in data center operations across the continent. Regulatory frameworks, while evolving, are becoming more conducive to data center development, particularly with the emphasis on data localization and cybersecurity. Competitive product substitutes exist, but the core functionality and performance requirements of data center networking create distinct market niches for specialized solutions. End-user demographics are shifting, with a pronounced rise in demand from the IT & Telecommunication and BFSI sectors, followed by government initiatives and the growing media and entertainment industry. Mergers and acquisitions (M&A) trends are emerging as companies seek to expand their geographical reach and product portfolios within Africa.

- Market Concentration: Dominated by a few key global vendors with substantial market presence, but opportunities exist for niche players.

- Technological Innovation: Driven by 5G deployment, AI/ML workloads, and the need for scalable and efficient network architectures.

- Regulatory Impact: Growing focus on data privacy, cybersecurity, and local content regulations influencing network design and vendor selection.

- Competitive Landscape: Intense competition among vendors offering a range of solutions from core networking to application delivery and security.

- M&A Activity: Expected to increase as companies aim to consolidate market share and gain access to emerging African markets.

Africa Data Center Networking Market Growth Trends & Insights

The Africa Data Center Networking Market is poised for robust growth, propelled by several intersecting trends that are transforming the continent's digital infrastructure. The market size is projected to expand significantly, driven by increasing investments in hyperscale data centers, colocation facilities, and edge computing deployments. The adoption rates of advanced networking technologies, such as Software-Defined Networking (SDN) and Network Function Virtualization (NFV), are on an upward trajectory, enabling greater agility, scalability, and cost-efficiency for data center operators. Technological disruptions, including the rapid evolution of Ethernet switch speeds and the integration of AI in network management, are key factors shaping market dynamics. Consumer behavior shifts, marked by an insatiable demand for digital services, online content, and mobile connectivity, are directly translating into increased data traffic and the subsequent need for more sophisticated data center networking solutions. The expanding internet penetration and the growth of mobile broadband across Africa are fundamental in fueling this demand. Furthermore, the increasing adoption of cloud computing services, both public and private, by African enterprises is a significant catalyst, necessitating robust and high-performance networking to support seamless data flow and application access. The ongoing digital transformation initiatives by governments and businesses across various sectors, including finance, healthcare, and education, are further accelerating the demand for data center networking infrastructure. The rise of the Internet of Things (IoT) is also contributing to the data deluge, requiring resilient and scalable network architectures to manage the influx of connected devices and their associated data streams. The focus on improving data center operational efficiency and reducing latency for real-time applications is also a key driver, pushing for the adoption of cutting-edge networking hardware and software. The market is also witnessing a growing interest in specialized networking solutions designed for high-performance computing (HPC) and artificial intelligence (AI) workloads, indicating a maturation of the African data center ecosystem. The interplay of these factors creates a fertile ground for innovation and sustained growth within the Africa Data Center Networking Market, with an anticipated Compound Annual Growth Rate (CAGR) of 12.5% during the forecast period. This signifies a substantial expansion from its current market value, indicating a strong investor confidence and market opportunity. The penetration of advanced networking solutions is expected to deepen across various industries as businesses recognize the critical role of robust data center infrastructure in their digital strategies. The evolving landscape of data consumption and production across Africa underscores the critical importance of the underlying networking technologies that power these data centers, making this market a significant area of focus for stakeholders. The growing number of interconnected devices and the increasing reliance on cloud-based services are creating a persistent demand for bandwidth, low latency, and high reliability, all of which are directly addressed by advancements in data center networking. The market's evolution is further shaped by a growing awareness of energy efficiency and sustainability in data center operations, leading to the adoption of networking solutions that can optimize power consumption while maintaining high performance.

Dominant Regions, Countries, or Segments in Africa Data Center Networking Market

The Africa Data Center Networking Market's dominance is multifaceted, with certain regions, countries, and specific segments exhibiting exceptional growth and influencing the overall market trajectory. Within the Component: By Product segmentation, Ethernet Switches are currently leading the market due to their foundational role in connecting servers, storage, and other network devices within a data center. Their ubiquity and continuous evolution in terms of speed and port density make them indispensable. Following closely are Routers, crucial for directing traffic within and between data centers and to external networks. Storage Area Networks (SAN) are also vital, especially for high-performance data storage and retrieval needs, particularly in enterprise environments. Application Delivery Controllers (ADCs) are gaining significant traction as businesses increasingly focus on optimizing application performance, availability, and security.

Geographically, South Africa has historically been a dominant player due to its relatively mature digital infrastructure, significant foreign investment, and a well-established ecosystem of data centers. However, Nigeria and Egypt are rapidly emerging as powerhouses, driven by their large populations, growing economies, and ambitious digital transformation agendas. These countries are witnessing substantial investments in hyperscale and enterprise data centers, creating a surge in demand for networking solutions. The IT & Telecommunication end-user segment is the undisputed leader, as these industries are the primary consumers and providers of data center services, necessitating extensive and high-performance networking capabilities. The BFSI (Banking, Financial Services, and Insurance) sector is a close second, driven by the need for secure, reliable, and high-availability networks to support financial transactions, digital banking services, and regulatory compliance. The Government sector is also a significant contributor, with increasing initiatives in e-governance, smart cities, and digital public services requiring robust data center infrastructure. The Media & Entertainment sector's growth, fueled by streaming services and digital content creation, further amplifies the demand for efficient data center networking.

Key drivers for this regional and segmental dominance include:

- Economic Policies: Governments in leading African nations are implementing favorable policies to attract data center investments, including tax incentives and streamlined regulatory processes. For instance, South Africa's National Broadband Policy and Nigeria's Digital Economy Policy are fostering an environment conducive to data center growth.

- Infrastructure Development: Significant investments are being made in subsea cables and terrestrial fiber optic networks, enhancing connectivity and reducing latency across the continent. This improved connectivity is critical for the performance of data center networks.

- Digital Transformation Initiatives: Countries are actively pursuing digital transformation across public and private sectors, leading to increased adoption of cloud computing, big data analytics, and IoT, all of which rely heavily on advanced data center networking.

- Growing Demand for Cloud Services: The rapid expansion of cloud service providers and the increasing adoption of cloud solutions by African enterprises are directly driving the need for scalable and high-performance data center networks.

- Urbanization and Population Growth: Concentrated populations in major economic hubs are creating localized demand for data services, spurring the development of distributed data centers and edge computing facilities.

The market share within these dominant segments is continually shifting as new investments are made and technological advancements are adopted. For example, the increasing adoption of 400GbE and beyond in Ethernet switches for hyperscale data centers signifies a technological leap and a shift in demand towards higher-performance products. Similarly, the growing focus on cybersecurity is elevating the importance of ADCs and advanced routing solutions within the BFSI and Government sectors. The continuous expansion of internet access and mobile data usage across the continent ensures sustained demand for upgraded networking infrastructure within data centers to cater to this ever-increasing data flow.

Africa Data Center Networking Market Product Landscape

The product landscape within the Africa Data Center Networking Market is characterized by a steady stream of innovations aimed at enhancing performance, scalability, and efficiency. Ethernet switches are witnessing advancements in port speeds, reaching up to 400GbE and beyond, enabling massive data throughput essential for hyperscale data centers and demanding workloads. Routers are evolving to handle increased traffic volumes with lower latency and improved routing protocols, supporting the dynamic nature of modern networks. Storage Area Networks (SANs) are becoming more intelligent, offering faster access speeds and enhanced data protection features, critical for data-intensive applications. Application Delivery Controllers (ADCs) are integrating advanced security features, intelligent traffic management, and multi-cloud capabilities to ensure seamless and secure application delivery. Beyond these core products, the market sees growth in specialized networking equipment for areas like edge computing and IoT, requiring compact, ruggedized, and power-efficient solutions.

Key Drivers, Barriers & Challenges in Africa Data Center Networking Market

Key Drivers:

The Africa Data Center Networking Market is propelled by a confluence of powerful forces. The escalating demand for digital services, fueled by rapid internet penetration and smartphone adoption across the continent, necessitates robust data center infrastructure. Digital transformation initiatives by governments and businesses across sectors like finance, healthcare, and telecommunications are creating a significant need for enhanced networking capabilities. The burgeoning growth of cloud computing adoption, both public and private, is a primary accelerator, requiring scalable and high-performance networks to support seamless data transfer and application access. Furthermore, the proliferation of IoT devices and the increasing data generated by them are driving the demand for more connected and intelligent networking solutions within data centers.

Barriers & Challenges:

Despite the strong growth potential, the market faces several significant challenges. Inadequate and inconsistent power supply in many regions remains a major hurdle, often requiring substantial investment in backup power solutions. The high cost of importing advanced networking equipment and the associated duties can impact affordability, particularly for smaller enterprises. A shortage of skilled IT professionals with expertise in advanced networking technologies poses a significant challenge for deployment and maintenance. Regulatory inconsistencies and bureaucratic hurdles in certain countries can slow down infrastructure development and investment. Finally, cybersecurity threats are a constant concern, demanding continuous investment in advanced security features and protocols within networking solutions, which can increase operational costs. Supply chain disruptions, though improving, can still impact the timely availability of critical networking components.

Emerging Opportunities in Africa Data Center Networking Market

Emerging opportunities in the Africa Data Center Networking Market lie in the growing demand for edge computing solutions, driven by the need for lower latency in applications like autonomous vehicles, smart cities, and real-time analytics. The expansion of 5G networks across the continent creates a massive opportunity for data centers to support the increased data traffic and new use cases enabled by this technology. Furthermore, there's a growing need for specialized networking for AI and Machine Learning workloads, requiring high-bandwidth, low-latency interconnects. The increasing focus on sustainability presents an opportunity for energy-efficient networking solutions and smart data center management systems. The underserved markets in various African countries represent a significant untapped potential for data center networking vendors and service providers.

Growth Accelerators in the Africa Data Center Networking Market Industry

Long-term growth in the Africa Data Center Networking Market will be significantly accelerated by continued advancements in fiber optic infrastructure, which forms the backbone for high-speed data transmission. The increasing adoption of hyper-converged infrastructure (HCI) and composable infrastructure within data centers will drive demand for integrated and intelligent networking solutions. Strategic partnerships between global technology providers and local African businesses are crucial for knowledge transfer, market penetration, and the development of tailored solutions. Furthermore, government support for digital innovation and the establishment of innovation hubs will foster a more dynamic ecosystem, encouraging the adoption of cutting-edge networking technologies. The ongoing development of specialized data centers for specific industries, such as healthcare and manufacturing, will also fuel targeted growth in networking solutions.

Key Players Shaping the Africa Data Center Networking Market Market

- Radware Corporation

- F5 Networks Inc

- Dell EMC

- Cisco Systems Inc

- Juniper Networks Inc

- Extreme Networks Inc

- NEC Corporation

- A10 Networks Inc

- Huawei Technologies Co Ltd

- TP-Link Corporation Limited

- Array Networks Inc

- Moxa Inc

- H3C Holding Limited

- VMware Inc

Notable Milestones in Africa Data Center Networking Market Sector

- July 2023: Moxa introduced its MDS-G4020-L3-4XGS series of Ethernet switches, a highly versatile line of Layer 3 full Gigabit modular managed switches. This series offers support for four 10GbE ports and sixteen Gigabit ports, including four embedded ports. Furthermore, it includes four interface module expansion slots and two power module slots, ensuring the utmost flexibility for a wide range of applications. This launch enhances the availability of advanced modular networking solutions for demanding African data center environments.

- March 2023: F5 Networks Inc. unveiled its multi-cloud networking (MCN) capabilities, enabling effortless extension of application and security services across one or more public clouds, hybrid deployments, native Kubernetes environments, and edge sites. F5's Distributed Cloud Services stand out for their ability to provide connectivity and security at both the network and application layers. This development signifies a crucial step towards simplifying complex cloud networking architectures for African enterprises.

In-Depth Africa Data Center Networking Market Market Outlook

The Africa Data Center Networking Market outlook is exceptionally positive, driven by accelerating digital transformation and increasing investments in connectivity. Growth accelerators such as advancements in optical networking, the widespread deployment of 5G, and the adoption of AI-driven network management will significantly enhance performance and efficiency. Strategic collaborations between international technology firms and local African entities are vital for market penetration and the localized development of solutions. The expansion of cloud services and the growing demand for edge computing applications will further fuel the need for scalable and resilient data center networks. The market is poised to witness sustained growth, presenting lucrative opportunities for stakeholders to capitalize on the continent's burgeoning digital economy.

Africa Data Center Networking Market Segmentation

-

1. Component

-

1.1. By Product

- 1.1.1. Ethernet Switches

- 1.1.2. Router

- 1.1.3. Storage Area Network (SAN)

- 1.1.4. Application Delivery Controller (ADC)

- 1.1.5. Other Networking Equipment

-

1.2. By Services

- 1.2.1. Installation & Integration

- 1.2.2. Training & Consulting

- 1.2.3. Support & Maintenance

-

1.1. By Product

-

2. End-User

- 2.1. IT & Telecommunication

- 2.2. BFSI

- 2.3. Government

- 2.4. Media & Entertainment

- 2.5. Other End-Users

Africa Data Center Networking Market Segmentation By Geography

-

1. Africa

- 1.1. Nigeria

- 1.2. South Africa

- 1.3. Egypt

- 1.4. Kenya

- 1.5. Ethiopia

- 1.6. Morocco

- 1.7. Ghana

- 1.8. Algeria

- 1.9. Tanzania

- 1.10. Ivory Coast

Africa Data Center Networking Market Regional Market Share

Geographic Coverage of Africa Data Center Networking Market

Africa Data Center Networking Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.79% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Need of Cloud Storage; Increasing Cyberattacks Among Enterprises

- 3.3. Market Restrains

- 3.3.1. Increasing Network Complexity

- 3.4. Market Trends

- 3.4.1. IT and Telecom to Hold Significant Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Africa Data Center Networking Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. By Product

- 5.1.1.1. Ethernet Switches

- 5.1.1.2. Router

- 5.1.1.3. Storage Area Network (SAN)

- 5.1.1.4. Application Delivery Controller (ADC)

- 5.1.1.5. Other Networking Equipment

- 5.1.2. By Services

- 5.1.2.1. Installation & Integration

- 5.1.2.2. Training & Consulting

- 5.1.2.3. Support & Maintenance

- 5.1.1. By Product

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. IT & Telecommunication

- 5.2.2. BFSI

- 5.2.3. Government

- 5.2.4. Media & Entertainment

- 5.2.5. Other End-Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Africa

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Radware Corporation

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 F5 Networks Inc

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Dell EMC

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Cisco Systems Inc

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Juniper Networks Inc

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Extreme Networks Inc

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 NEC Corporation

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 A10 Networks Inc

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Huawei Technologies Co Ltd

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 TP-Link Corporation Limited

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Array Networks Inc

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Moxa Inc *List Not Exhaustive

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 H3C Holding Limited

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.14 VMware Inc

- 6.2.14.1. Overview

- 6.2.14.2. Products

- 6.2.14.3. SWOT Analysis

- 6.2.14.4. Recent Developments

- 6.2.14.5. Financials (Based on Availability)

- 6.2.1 Radware Corporation

List of Figures

- Figure 1: Africa Data Center Networking Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Africa Data Center Networking Market Share (%) by Company 2025

List of Tables

- Table 1: Africa Data Center Networking Market Revenue billion Forecast, by Component 2020 & 2033

- Table 2: Africa Data Center Networking Market Revenue billion Forecast, by End-User 2020 & 2033

- Table 3: Africa Data Center Networking Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Africa Data Center Networking Market Revenue billion Forecast, by Component 2020 & 2033

- Table 5: Africa Data Center Networking Market Revenue billion Forecast, by End-User 2020 & 2033

- Table 6: Africa Data Center Networking Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Nigeria Africa Data Center Networking Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: South Africa Africa Data Center Networking Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Egypt Africa Data Center Networking Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Kenya Africa Data Center Networking Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Ethiopia Africa Data Center Networking Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Morocco Africa Data Center Networking Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Ghana Africa Data Center Networking Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Algeria Africa Data Center Networking Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Tanzania Africa Data Center Networking Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Ivory Coast Africa Data Center Networking Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Africa Data Center Networking Market?

The projected CAGR is approximately 11.79%.

2. Which companies are prominent players in the Africa Data Center Networking Market?

Key companies in the market include Radware Corporation, F5 Networks Inc, Dell EMC, Cisco Systems Inc, Juniper Networks Inc, Extreme Networks Inc, NEC Corporation, A10 Networks Inc, Huawei Technologies Co Ltd, TP-Link Corporation Limited, Array Networks Inc, Moxa Inc *List Not Exhaustive, H3C Holding Limited, VMware Inc.

3. What are the main segments of the Africa Data Center Networking Market?

The market segments include Component, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.49 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Need of Cloud Storage; Increasing Cyberattacks Among Enterprises.

6. What are the notable trends driving market growth?

IT and Telecom to Hold Significant Share.

7. Are there any restraints impacting market growth?

Increasing Network Complexity.

8. Can you provide examples of recent developments in the market?

July 2023: Moxa introduced its MDS-G4020-L3-4XGS series of Ethernet switches, a highly versatile line of Layer 3 full Gigabit modular managed switches. This series offers support for four 10GbE ports and sixteen Gigabit ports, including four embedded ports. Furthermore, it includes four interface module expansion slots and two power module slots, ensuring the utmost flexibility for a wide range of applications.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Africa Data Center Networking Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Africa Data Center Networking Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Africa Data Center Networking Market?

To stay informed about further developments, trends, and reports in the Africa Data Center Networking Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence