Key Insights

The Asia-Pacific (APAC) food packaging market is poised for significant expansion, fueled by escalating disposable incomes, a growing populace, and evolving consumer demand for convenient, ready-to-eat food options. The region's rich culinary diversity and thriving food processing sector further underpin this demand. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.4%. Key market segments include product type (bottles & containers, cartons & pouches, cans, films & wraps, caps & closures, others), end-user (fruits & vegetables, meat & poultry, dairy, bakery & confectionery, others), and material type (plastic, paper & paperboard, metal, glass). Major contributors to market share are China, India, and Japan, owing to their substantial populations and strong economies. Emerging economies within APAC, such as Indonesia and Thailand, also present considerable growth opportunities.

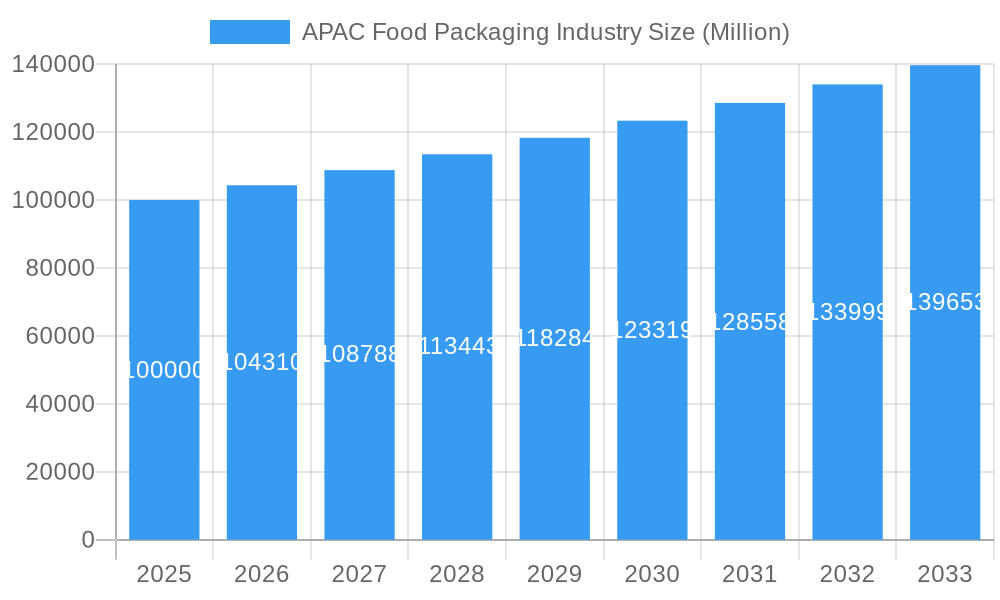

APAC Food Packaging Industry Market Size (In Billion)

Market challenges include volatile raw material costs, stringent regulations on packaging materials (especially plastics), and growing environmental sustainability concerns. Nevertheless, the development of innovative solutions like biodegradable and compostable packaging is expected to address these issues. The rapid adoption of e-commerce and online food delivery services is a significant growth driver, demanding efficient and reliable packaging for transit and product integrity. This dynamic market offers substantial growth potential, necessitating agile strategies to navigate evolving regulatory frameworks and consumer expectations. The market is valued at 421.38 billion in 2025, with continued robust expansion anticipated.

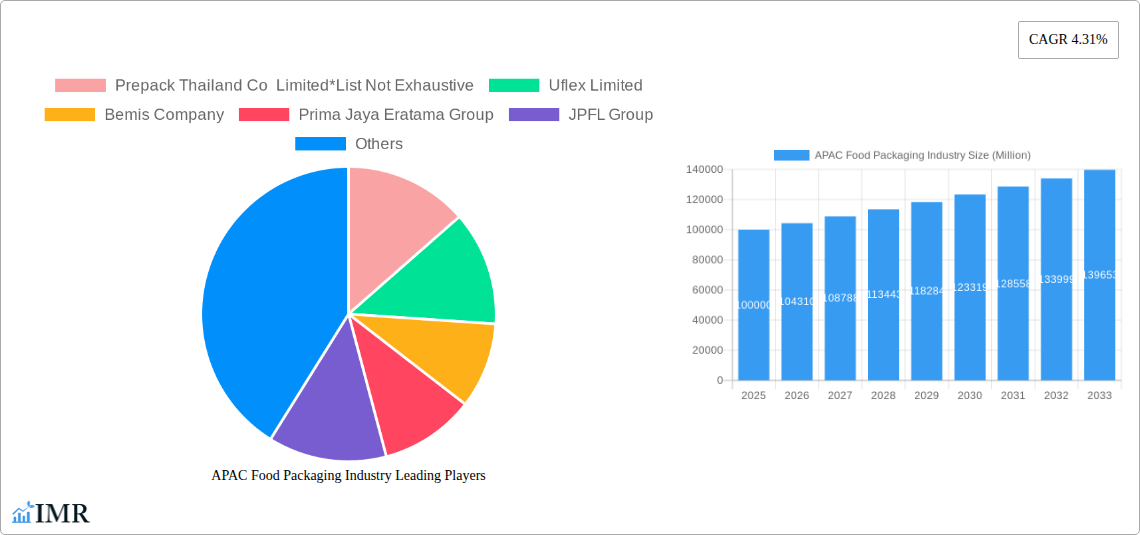

APAC Food Packaging Industry Company Market Share

APAC Food Packaging Industry Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Asia-Pacific (APAC) food packaging market, covering the period 2019-2033. It offers invaluable insights into market dynamics, growth trends, dominant segments, and key players, equipping businesses with the knowledge to navigate this dynamic landscape and capitalize on emerging opportunities. The report utilizes a robust methodology, incorporating both quantitative and qualitative data to deliver actionable intelligence.

APAC Food Packaging Industry Market Dynamics & Structure

The APAC food packaging market is characterized by a moderately concentrated landscape, with a few major players holding significant market share. However, the presence of numerous smaller, regional players also contributes to the market's complexity. Technological innovation, driven by increasing demand for sustainable and functional packaging, is a significant driver of market growth. Stringent regulatory frameworks concerning food safety and environmental sustainability influence packaging material choices and manufacturing processes. Competitive product substitutes, such as biodegradable and compostable packaging materials, are gaining traction, impacting the market share of traditional materials. The evolving demographics of APAC, with a growing middle class and increasing urbanization, are fuelling demand for convenient and attractive food packaging. Mergers and acquisitions (M&A) activity is relatively frequent, indicating consolidation and expansion among key players. The overall market value in 2025 is estimated at xx Million units, with a projected CAGR of xx% during 2025-2033.

- Market Concentration: Moderately concentrated, with top 5 players holding approximately xx% market share in 2025.

- Technological Innovation: Focus on sustainable materials (e.g., biodegradable plastics, paper-based alternatives), smart packaging, and improved barrier properties.

- Regulatory Framework: Stringent regulations on food safety and waste management, driving demand for eco-friendly packaging solutions.

- M&A Activity: xx deals recorded between 2019 and 2024, indicating a trend towards consolidation.

- Innovation Barriers: High R&D costs for new materials, difficulty in scaling up production of sustainable alternatives, and regulatory complexities.

APAC Food Packaging Industry Growth Trends & Insights

The APAC food packaging market experienced significant growth during the historical period (2019-2024), driven by factors such as rising disposable incomes, changing consumer preferences, and the expansion of the food processing industry. The market size is expected to reach xx Million units by 2025 and continue its upward trajectory, registering a CAGR of xx% during the forecast period (2025-2033). Technological disruptions, including the adoption of automation and advanced packaging technologies, are enhancing efficiency and creating new opportunities. Consumer behavior shifts towards healthier and more convenient food options are influencing packaging choices, with increased demand for eco-friendly and sustainable options. The increasing adoption of e-commerce is further fueling demand for specialized packaging solutions that ensure product safety and quality during transportation. Market penetration of sustainable packaging materials is gradually increasing, although challenges remain in terms of cost and scalability.

Dominant Regions, Countries, or Segments in APAC Food Packaging Industry

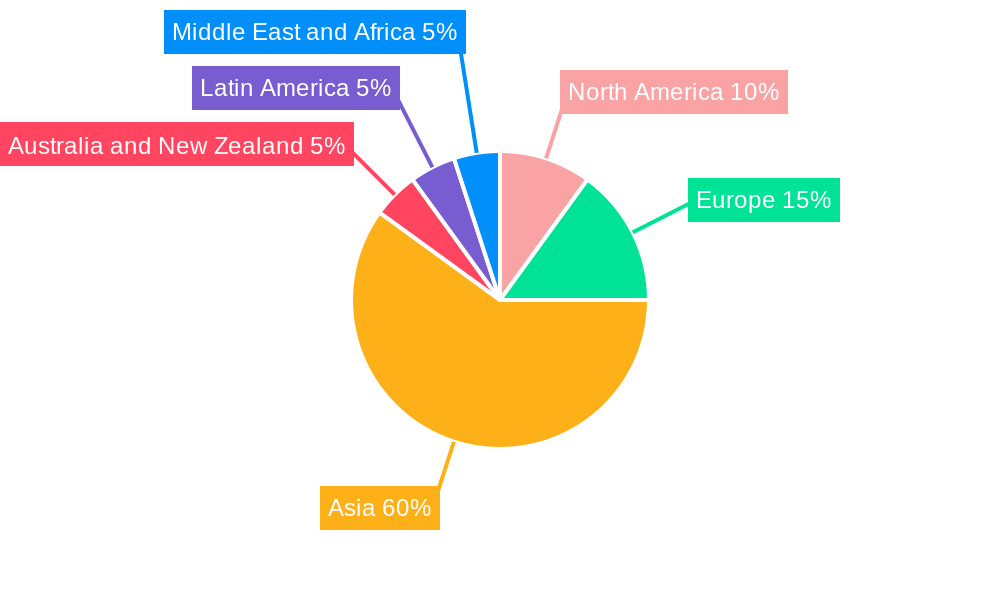

China and India are the leading markets for food packaging in APAC, owing to their large and rapidly growing populations, expanding middle classes, and booming food processing industries. Within product types, bottles and containers, cartons and pouches, and films and wraps represent the largest segments, collectively accounting for approximately xx% of the total market in 2025. The Fruits and Vegetables end-user segment drives significant demand, followed by the Dairy Products and Meat and Poultry segments. Plastic remains the dominant material type, although paper and paperboard are experiencing growing adoption due to environmental concerns.

- Key Drivers in China: Robust economic growth, rising consumer spending, and stringent food safety regulations.

- Key Drivers in India: Large population, increasing urbanization, and government initiatives promoting food processing and packaging industries.

- Bottles and Containers: High demand driven by the beverage and liquid food industries.

- Cartons and Pouches: Growing popularity for their versatility and cost-effectiveness.

- Plastic: Dominant material due to its versatility and cost-effectiveness, however, facing increasing scrutiny due to environmental concerns.

APAP Food Packaging Industry Product Landscape

Significant advancements are being made in food packaging materials and technologies, focusing on enhanced barrier properties, improved shelf life, and sustainable options. Innovations include active and intelligent packaging that extends product shelf life and provides information about product freshness. Biodegradable and compostable materials are gaining traction, driven by growing environmental awareness. The key selling propositions often emphasize sustainability, improved product protection, and enhanced convenience for consumers. The market is witnessing the adoption of advanced printing technologies for enhanced aesthetics and brand differentiation.

Key Drivers, Barriers & Challenges in APAC Food Packaging Industry

Key Drivers: Rising disposable incomes, increasing urbanization, growth of the food processing and retail industries, evolving consumer preferences (health, convenience, sustainability), and government initiatives promoting food safety and waste management.

Key Challenges: Fluctuating raw material prices, stringent environmental regulations, increasing competition, ensuring supply chain reliability amid geopolitical uncertainties, and consumer resistance to price increases for sustainable alternatives. The estimated impact of supply chain disruptions on market growth in 2024 was approximately xx%.

Emerging Opportunities in APAP Food Packaging Industry

Untapped markets exist in less developed regions of APAC, offering significant growth potential. The increasing popularity of e-commerce is creating opportunities for specialized packaging solutions that meet the demands of online grocery delivery. Innovative applications, such as active and intelligent packaging, are gaining traction. Evolving consumer preferences towards sustainability and health are driving demand for eco-friendly and functional food packaging.

Growth Accelerators in the APAC Food Packaging Industry

Long-term growth will be driven by technological breakthroughs in sustainable materials and packaging technologies, strategic partnerships between packaging companies and food manufacturers, and expansion into new and emerging markets within APAC. Further consolidation through M&A activity will reshape the industry landscape.

Key Players Shaping the APAC Food Packaging Industry Market

- Prepack Thailand Co Limited

- Uflex Limited

- Bemis Company

- Prima Jaya Eratama Group

- JPFL Group

- Huhtamaki Group

- Amcor PLC

- Berry Plastics

- Crown Holdings

- Sealed Air Corporation

Notable Milestones in APAC Food Packaging Industry Sector

- March 2022: The Food Safety and Standards Authority of India (FSSAI) introduced stricter standards for recycled plastic in food packaging.

- January 2022: The SIG Group launched the combibloc ECOPLUS carton packaging in China, a sustainable alternative with a reduced carbon footprint.

In-Depth APAC Food Packaging Industry Market Outlook

The APAC food packaging market is poised for sustained growth in the coming years. Technological advancements, coupled with a focus on sustainability and convenience, will drive innovation. Strategic partnerships and market expansion into underserved regions will be critical for success. The market offers significant opportunities for both established players and new entrants, with those able to adapt to changing consumer preferences and regulatory frameworks best positioned for success. The potential for market expansion is substantial, particularly in e-commerce and food delivery segments.

APAC Food Packaging Industry Segmentation

-

1. Material Type

-

1.1. Plastic

- 1.1.1. Rigid

- 1.1.2. Flexible

- 1.2. Paper and Paperboard

- 1.3. Metal

- 1.4. Glass

-

1.1. Plastic

-

2. Product Type

- 2.1. Bottles and Containers

- 2.2. Cartons and Pouches

- 2.3. Cans

- 2.4. Films and Wraps

- 2.5. Caps and Closures

- 2.6. Other Product Types

-

3. End-user Type

- 3.1. Fruits and Vegetables

- 3.2. Meat and Poultry

- 3.3. Dairy Products

- 3.4. Bakery and Confectionery

- 3.5. Other end-users

APAC Food Packaging Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

APAC Food Packaging Industry Regional Market Share

Geographic Coverage of APAC Food Packaging Industry

APAC Food Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Plastic

- 5.1.1.1. Rigid

- 5.1.1.2. Flexible

- 5.1.2. Paper and Paperboard

- 5.1.3. Metal

- 5.1.4. Glass

- 5.1.1. Plastic

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Bottles and Containers

- 5.2.2. Cartons and Pouches

- 5.2.3. Cans

- 5.2.4. Films and Wraps

- 5.2.5. Caps and Closures

- 5.2.6. Other Product Types

- 5.3. Market Analysis, Insights and Forecast - by End-user Type

- 5.3.1. Fruits and Vegetables

- 5.3.2. Meat and Poultry

- 5.3.3. Dairy Products

- 5.3.4. Bakery and Confectionery

- 5.3.5. Other end-users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. South America

- 5.4.3. Europe

- 5.4.4. Middle East & Africa

- 5.4.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. Global APAC Food Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Plastic

- 6.1.1.1. Rigid

- 6.1.1.2. Flexible

- 6.1.2. Paper and Paperboard

- 6.1.3. Metal

- 6.1.4. Glass

- 6.1.1. Plastic

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Bottles and Containers

- 6.2.2. Cartons and Pouches

- 6.2.3. Cans

- 6.2.4. Films and Wraps

- 6.2.5. Caps and Closures

- 6.2.6. Other Product Types

- 6.3. Market Analysis, Insights and Forecast - by End-user Type

- 6.3.1. Fruits and Vegetables

- 6.3.2. Meat and Poultry

- 6.3.3. Dairy Products

- 6.3.4. Bakery and Confectionery

- 6.3.5. Other end-users

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. North America APAC Food Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 7.1.1. Plastic

- 7.1.1.1. Rigid

- 7.1.1.2. Flexible

- 7.1.2. Paper and Paperboard

- 7.1.3. Metal

- 7.1.4. Glass

- 7.1.1. Plastic

- 7.2. Market Analysis, Insights and Forecast - by Product Type

- 7.2.1. Bottles and Containers

- 7.2.2. Cartons and Pouches

- 7.2.3. Cans

- 7.2.4. Films and Wraps

- 7.2.5. Caps and Closures

- 7.2.6. Other Product Types

- 7.3. Market Analysis, Insights and Forecast - by End-user Type

- 7.3.1. Fruits and Vegetables

- 7.3.2. Meat and Poultry

- 7.3.3. Dairy Products

- 7.3.4. Bakery and Confectionery

- 7.3.5. Other end-users

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 8. South America APAC Food Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 8.1.1. Plastic

- 8.1.1.1. Rigid

- 8.1.1.2. Flexible

- 8.1.2. Paper and Paperboard

- 8.1.3. Metal

- 8.1.4. Glass

- 8.1.1. Plastic

- 8.2. Market Analysis, Insights and Forecast - by Product Type

- 8.2.1. Bottles and Containers

- 8.2.2. Cartons and Pouches

- 8.2.3. Cans

- 8.2.4. Films and Wraps

- 8.2.5. Caps and Closures

- 8.2.6. Other Product Types

- 8.3. Market Analysis, Insights and Forecast - by End-user Type

- 8.3.1. Fruits and Vegetables

- 8.3.2. Meat and Poultry

- 8.3.3. Dairy Products

- 8.3.4. Bakery and Confectionery

- 8.3.5. Other end-users

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 9. Europe APAC Food Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 9.1.1. Plastic

- 9.1.1.1. Rigid

- 9.1.1.2. Flexible

- 9.1.2. Paper and Paperboard

- 9.1.3. Metal

- 9.1.4. Glass

- 9.1.1. Plastic

- 9.2. Market Analysis, Insights and Forecast - by Product Type

- 9.2.1. Bottles and Containers

- 9.2.2. Cartons and Pouches

- 9.2.3. Cans

- 9.2.4. Films and Wraps

- 9.2.5. Caps and Closures

- 9.2.6. Other Product Types

- 9.3. Market Analysis, Insights and Forecast - by End-user Type

- 9.3.1. Fruits and Vegetables

- 9.3.2. Meat and Poultry

- 9.3.3. Dairy Products

- 9.3.4. Bakery and Confectionery

- 9.3.5. Other end-users

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 10. Middle East & Africa APAC Food Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 10.1.1. Plastic

- 10.1.1.1. Rigid

- 10.1.1.2. Flexible

- 10.1.2. Paper and Paperboard

- 10.1.3. Metal

- 10.1.4. Glass

- 10.1.1. Plastic

- 10.2. Market Analysis, Insights and Forecast - by Product Type

- 10.2.1. Bottles and Containers

- 10.2.2. Cartons and Pouches

- 10.2.3. Cans

- 10.2.4. Films and Wraps

- 10.2.5. Caps and Closures

- 10.2.6. Other Product Types

- 10.3. Market Analysis, Insights and Forecast - by End-user Type

- 10.3.1. Fruits and Vegetables

- 10.3.2. Meat and Poultry

- 10.3.3. Dairy Products

- 10.3.4. Bakery and Confectionery

- 10.3.5. Other end-users

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 11. Asia Pacific APAC Food Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Material Type

- 11.1.1. Plastic

- 11.1.1.1. Rigid

- 11.1.1.2. Flexible

- 11.1.2. Paper and Paperboard

- 11.1.3. Metal

- 11.1.4. Glass

- 11.1.1. Plastic

- 11.2. Market Analysis, Insights and Forecast - by Product Type

- 11.2.1. Bottles and Containers

- 11.2.2. Cartons and Pouches

- 11.2.3. Cans

- 11.2.4. Films and Wraps

- 11.2.5. Caps and Closures

- 11.2.6. Other Product Types

- 11.3. Market Analysis, Insights and Forecast - by End-user Type

- 11.3.1. Fruits and Vegetables

- 11.3.2. Meat and Poultry

- 11.3.3. Dairy Products

- 11.3.4. Bakery and Confectionery

- 11.3.5. Other end-users

- 11.1. Market Analysis, Insights and Forecast - by Material Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Prepack Thailand Co Limited*List Not Exhaustive

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Uflex Limited

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Bemis Company

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Prima Jaya Eratama Group

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 JPFL Group

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Huhtamaki Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Amcor PLC

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Berry Plastics

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Crown Holdings

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Sealed Air Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Prepack Thailand Co Limited*List Not Exhaustive

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global APAC Food Packaging Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America APAC Food Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 3: North America APAC Food Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 4: North America APAC Food Packaging Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 5: North America APAC Food Packaging Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America APAC Food Packaging Industry Revenue (billion), by End-user Type 2025 & 2033

- Figure 7: North America APAC Food Packaging Industry Revenue Share (%), by End-user Type 2025 & 2033

- Figure 8: North America APAC Food Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: North America APAC Food Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: South America APAC Food Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 11: South America APAC Food Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 12: South America APAC Food Packaging Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 13: South America APAC Food Packaging Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 14: South America APAC Food Packaging Industry Revenue (billion), by End-user Type 2025 & 2033

- Figure 15: South America APAC Food Packaging Industry Revenue Share (%), by End-user Type 2025 & 2033

- Figure 16: South America APAC Food Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: South America APAC Food Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe APAC Food Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 19: Europe APAC Food Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 20: Europe APAC Food Packaging Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 21: Europe APAC Food Packaging Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 22: Europe APAC Food Packaging Industry Revenue (billion), by End-user Type 2025 & 2033

- Figure 23: Europe APAC Food Packaging Industry Revenue Share (%), by End-user Type 2025 & 2033

- Figure 24: Europe APAC Food Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Europe APAC Food Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East & Africa APAC Food Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 27: Middle East & Africa APAC Food Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 28: Middle East & Africa APAC Food Packaging Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 29: Middle East & Africa APAC Food Packaging Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 30: Middle East & Africa APAC Food Packaging Industry Revenue (billion), by End-user Type 2025 & 2033

- Figure 31: Middle East & Africa APAC Food Packaging Industry Revenue Share (%), by End-user Type 2025 & 2033

- Figure 32: Middle East & Africa APAC Food Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: Middle East & Africa APAC Food Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Asia Pacific APAC Food Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 35: Asia Pacific APAC Food Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 36: Asia Pacific APAC Food Packaging Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 37: Asia Pacific APAC Food Packaging Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 38: Asia Pacific APAC Food Packaging Industry Revenue (billion), by End-user Type 2025 & 2033

- Figure 39: Asia Pacific APAC Food Packaging Industry Revenue Share (%), by End-user Type 2025 & 2033

- Figure 40: Asia Pacific APAC Food Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: Asia Pacific APAC Food Packaging Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global APAC Food Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 2: Global APAC Food Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 3: Global APAC Food Packaging Industry Revenue billion Forecast, by End-user Type 2020 & 2033

- Table 4: Global APAC Food Packaging Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global APAC Food Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 6: Global APAC Food Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 7: Global APAC Food Packaging Industry Revenue billion Forecast, by End-user Type 2020 & 2033

- Table 8: Global APAC Food Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Mexico APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global APAC Food Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 13: Global APAC Food Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 14: Global APAC Food Packaging Industry Revenue billion Forecast, by End-user Type 2020 & 2033

- Table 15: Global APAC Food Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Brazil APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Argentina APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Rest of South America APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Global APAC Food Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 20: Global APAC Food Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 21: Global APAC Food Packaging Industry Revenue billion Forecast, by End-user Type 2020 & 2033

- Table 22: Global APAC Food Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 23: United Kingdom APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Germany APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: France APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Italy APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Spain APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Russia APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Benelux APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Nordics APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of Europe APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global APAC Food Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 33: Global APAC Food Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 34: Global APAC Food Packaging Industry Revenue billion Forecast, by End-user Type 2020 & 2033

- Table 35: Global APAC Food Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Turkey APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Israel APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: GCC APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: North Africa APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: South Africa APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: Rest of Middle East & Africa APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Global APAC Food Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 43: Global APAC Food Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 44: Global APAC Food Packaging Industry Revenue billion Forecast, by End-user Type 2020 & 2033

- Table 45: Global APAC Food Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 46: China APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 47: India APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Japan APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 49: South Korea APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: ASEAN APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 51: Oceania APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Rest of Asia Pacific APAC Food Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the APAC Food Packaging Industry?

The projected CAGR is approximately 5.4%.

2. Which companies are prominent players in the APAC Food Packaging Industry?

Key companies in the market include Prepack Thailand Co Limited*List Not Exhaustive, Uflex Limited, Bemis Company, Prima Jaya Eratama Group, JPFL Group, Huhtamaki Group, Amcor PLC, Berry Plastics, Crown Holdings, Sealed Air Corporation.

3. What are the main segments of the APAC Food Packaging Industry?

The market segments include Material Type, Product Type, End-user Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 421.38 billion as of 2022.

5. What are some drivers contributing to market growth?

Reduction in pack sizes coupled with move towards convenience; Recent advancements in food packaging technology has led to extension of shelf life.

6. What are the notable trends driving market growth?

Flexible Packaging is Expected to Drive the Market Growth..

7. Are there any restraints impacting market growth?

Dynamic nature of regulatory changes. specifically in the case of plastic packaging; Price competition has been a major concern impacting the packaging manufacturers.

8. Can you provide examples of recent developments in the market?

March 2022 - The Food Safety and Standards Authority India (FSSAI) has issued new, stricter standards to govern the use of recycled plastic for food packaging after facing pushback from a group of concerned scientific experts, which was designed as a positive move toward more efficient management of the country's massive plastic waste.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "APAC Food Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the APAC Food Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the APAC Food Packaging Industry?

To stay informed about further developments, trends, and reports in the APAC Food Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence