Key Insights

The Asia Pacific flexible packaging market, currently experiencing robust growth, is projected to expand significantly between 2025 and 2033. Driven by factors such as the rising demand for convenient and portable food products, increasing consumption of packaged beverages, and the burgeoning pharmaceutical and medical sectors across the region, the market is poised for considerable expansion. The preference for lightweight, flexible packaging materials, owing to their cost-effectiveness and reduced environmental impact compared to rigid packaging, further fuels market growth. Specific growth drivers include the booming e-commerce sector, necessitating efficient and secure packaging solutions, and the rising disposable incomes within key Asian markets, leading to increased consumer spending on packaged goods. While challenges such as fluctuating raw material prices and stringent environmental regulations exist, ongoing innovation in sustainable packaging materials like biodegradable plastics and eco-friendly paper-based alternatives is mitigating these concerns. Key players are focusing on strategic partnerships, product diversification, and technological advancements to maintain their competitive edge within this rapidly evolving landscape. The segmentation by material (plastic, paper, aluminum/composites), end-user vertical (food, beverages, pharmaceuticals, personal care), and country (China, India, Japan, Australia, etc.) reveals diverse growth opportunities across the Asia Pacific region, with China and India expected to remain the dominant markets due to their large populations and expanding consumer bases.

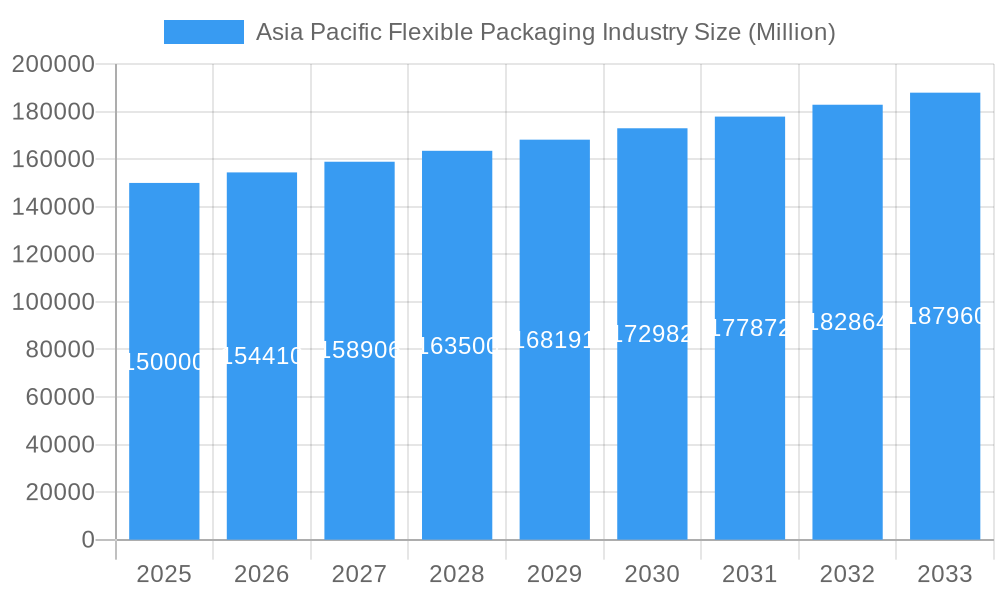

Asia Pacific Flexible Packaging Industry Market Size (In Billion)

The segment analysis indicates a strong preference for plastic-based flexible packaging due to its versatility and cost-effectiveness, although this is being challenged by growing environmental concerns and a shift towards more sustainable alternatives. The food and beverage industry remains the largest end-user, fueled by rising consumption and evolving consumer preferences. However, the pharmaceutical and medical sector is witnessing impressive growth due to increasing healthcare expenditure and demand for sterile and tamper-evident packaging. Competitive dynamics are intensifying, with both established multinational corporations and regional players vying for market share. The forecast period (2025-2033) suggests a continuous expansion of the Asia Pacific flexible packaging market, albeit with a fluctuating growth rate influenced by macroeconomic factors and evolving consumer trends. The market's future trajectory is closely linked to the adoption of sustainable packaging solutions, regulatory changes, and technological advancements within the packaging industry.

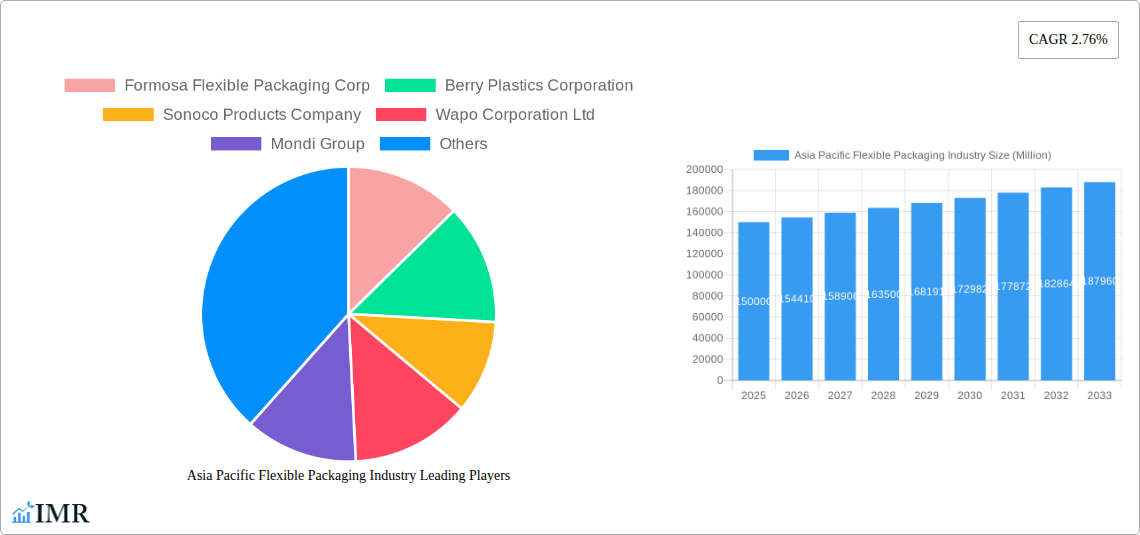

Asia Pacific Flexible Packaging Industry Company Market Share

Asia Pacific Flexible Packaging Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report delivers an in-depth analysis of the Asia Pacific flexible packaging industry, offering invaluable insights for industry professionals, investors, and strategic decision-makers. The report covers the period from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033. The market is segmented by material (plastic, paper, aluminum/composites), end-user vertical (food, beverages, pharmaceutical and medical, household and personal care, other), country (China, India, Japan, Australia, Rest of Asia Pacific), and type (pouches, bags, wraps, other). Key players such as Amcor Ltd, Formosa Flexible Packaging Corp, Berry Plastics Corporation, Sonoco Products Company, Wapo Corporation Ltd, Mondi Group, Rengo Co Ltd, Ester Industries Ltd (Wilemina Finance Corporation), TCPL Packaging Ltd, Sealed Air Corporation, and Chuan Peng Enterprise Co Ltd are analyzed, providing a holistic view of this dynamic market. The report's value is expressed in million units.

Asia Pacific Flexible Packaging Industry Market Dynamics & Structure

This section analyzes the competitive landscape of the Asia Pacific flexible packaging market, exploring market concentration, technological advancements, regulatory impacts, and evolving consumer preferences. We delve into the intricacies of mergers and acquisitions (M&A) activities, assessing their influence on market share distribution and competitive dynamics.

- Market Concentration: The Asia Pacific flexible packaging market exhibits a moderately concentrated structure, with a few dominant players and numerous smaller regional participants. Market share data for 2024 indicates that the top five players hold approximately xx% of the market share.

- Technological Innovation: Technological advancements, including the adoption of sustainable materials and digital printing techniques, are significant drivers of market growth. The integration of smart packaging and improved barrier properties is shaping product innovation.

- Regulatory Frameworks: Stringent environmental regulations, particularly regarding plastic waste reduction, are influencing material choices and packaging designs. Compliance costs and the need for sustainable solutions are key considerations for industry players.

- Competitive Product Substitutes: The market faces competition from rigid packaging alternatives. However, flexible packaging’s advantages in terms of cost-effectiveness, versatility, and lightweight nature continue to drive its preference.

- End-User Demographics: Growing urbanization and changing consumer preferences towards convenience and sustainability are boosting demand for flexible packaging across various end-user verticals. Shifting consumer demographics in emerging Asian economies are influencing packaging design and material selection.

- M&A Trends: The Asia Pacific region has witnessed a moderate level of M&A activity in recent years, with xx major deals recorded between 2019 and 2024. These activities primarily focused on expanding market reach and enhancing product portfolios.

Asia Pacific Flexible Packaging Industry Growth Trends & Insights

This section presents a comprehensive analysis of the Asia Pacific flexible packaging market's growth trajectory, leveraging extensive market data and research to provide key insights into market size, adoption rates, and influential consumer behaviors.

(This section would contain approximately 600 words detailing market size evolution (including historical and projected figures in million units), CAGR, market penetration rates across different segments, the impact of technological disruptions such as the rise of e-commerce and digital printing, and shifts in consumer behavior towards sustainability and convenience. Specific data points and illustrative examples would be included to support the analysis.)

Dominant Regions, Countries, or Segments in Asia Pacific Flexible Packaging Industry

This section provides an in-depth analysis of the leading regions, countries, and key segments that are shaping the Asia Pacific flexible packaging market. We delve into the market share dynamics, analyze the underlying growth drivers, and assess the future potential of each segment, offering a comprehensive understanding of the current landscape and its trajectory.

- By Material: Plastic packaging continues its stronghold, expected to represent approximately 65-70% of the market share in 2024, owing to its exceptional versatility, cost-effectiveness, and functional properties. However, the burgeoning demand for environmentally responsible solutions is significantly boosting the growth of paper-based and aluminum/composite packaging segments, which are projected to see a CAGR of over 6%. Innovations in bioplastics and recycled content are also gaining traction.

- By End-User Vertical: The food and beverage sector remains the undisputed leader, accounting for an estimated 55-60% of the market demand in 2024. This dominance is fueled by the critical role flexible packaging plays in extending shelf life, ensuring product integrity, and facilitating efficient distribution of a vast array of food and beverage products. The pharmaceutical and medical segments are experiencing particularly robust growth, projected at a CAGR of 7-8%, driven by the increasing healthcare expenditure and the need for sterile and safe packaging solutions.

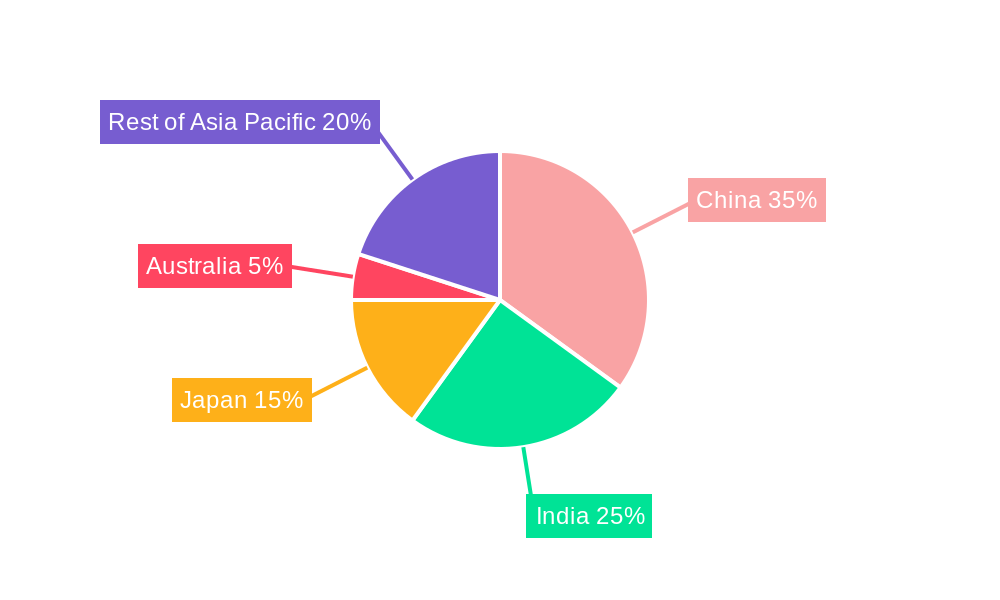

- By Country: China unequivocally leads the Asia Pacific flexible packaging market, driven by its massive manufacturing capabilities, robust domestic consumption, and significant export activities. India follows closely, propelled by its burgeoning middle class, rapid urbanization, and expanding food processing industry. Japan, with its advanced technological infrastructure and high standards for product quality and safety, maintains a strong and influential presence. Other key markets showing considerable growth include South Korea, Indonesia, and Vietnam, each with unique drivers.

- By Type: Pouches and bags collectively command over 50-55% of the market share in 2024. This segment's prevalence stems from their adaptability across a wide spectrum of applications, from single-serve snacks and personal care items to larger industrial goods. Stand-up pouches, spouted pouches, and various bag formats are increasingly favored for their convenience and shelf appeal. Other significant types include flow wrap films and laminates.

The dominance factors for each segment are further elaborated upon, including detailed market share data for 2024 and strategic projections extending to 2033. The analysis delves into the specific economic, demographic, and technological drivers, as well as consumer trends, that underpin the growth and market penetration of these dominant regions, countries, and segments. For instance, China's dominance is attributed to its extensive industrial ecosystem and government support for manufacturing, while India's rise is linked to its vast untapped consumer base and the growth of its organized retail sector. The food and beverage sector's lead is reinforced by increasing disposable incomes and evolving dietary habits across the region. The market is expected to witness a CAGR of approximately 5.5-6.5% over the next decade, reflecting a dynamic and evolving industry landscape.

Asia Pacific Flexible Packaging Industry Product Landscape

The Asia Pacific flexible packaging market is characterized by ongoing product innovation, with a focus on enhanced functionality, sustainability, and convenience. New product development concentrates on improved barrier properties, extended shelf life, and reduced environmental impact. Technological advancements like digital printing enable customized packaging designs and reduced waste. Unique selling propositions revolve around lightweight designs, improved material strength, and ease of use for consumers.

Key Drivers, Barriers & Challenges in Asia Pacific Flexible Packaging Industry

Key Drivers: The Asia Pacific flexible packaging market is experiencing dynamic growth, propelled by several compelling factors. The continuously expanding food and beverage sector, driven by population growth and evolving consumer preferences for convenience and healthier options, remains a primary engine. The meteoric rise of e-commerce across the region is creating unprecedented demand for protective, lightweight, and adaptable packaging solutions. Furthermore, the increasing consumer preference for convenient, on-the-go consumption and single-serve packaging formats significantly boosts the adoption of flexible packaging. Supportive government policies and initiatives aimed at promoting sustainable packaging practices, coupled with significant technological innovations in material science, high-barrier films, and advanced printing technologies, are further accelerating market expansion.

Challenges & Restraints: Despite the positive outlook, the industry navigates several critical challenges and restraints. Escalating raw material costs, particularly for polymers, and volatile oil prices directly impact the production costs of plastic-based flexible packaging. Growing global concerns and stringent regulations surrounding plastic waste and its environmental impact necessitate a shift towards more sustainable alternatives, which can incur higher initial investment and processing complexities. Intense competition among a multitude of established global players and emerging regional manufacturers creates significant pricing pressures and demands continuous innovation. Disruptions in global supply chains, geopolitical uncertainties, and trade tensions can lead to material shortages, increased lead times, and production setbacks, posing considerable operational risks.

Emerging Opportunities in Asia Pacific Flexible Packaging Industry

The Asia Pacific flexible packaging industry is ripe with emerging opportunities for strategic growth. Expanding into currently underserved or emerging markets within Southeast Asia, such as Vietnam, Thailand, and the Philippines, presents a significant untapped potential. There is a surging demand for genuinely sustainable and eco-friendly packaging solutions, including compostable, biodegradable, and recyclable materials, offering a clear avenue for innovation and market differentiation. The continued exponential growth of e-commerce across the region necessitates specialized packaging that ensures product protection during transit while enhancing unboxing experiences. The rising popularity of customized and personalized packaging, driven by branding and consumer engagement strategies, also presents a lucrative opportunity. Furthermore, the development and adoption of advanced packaging concepts, such as active packaging that extends shelf life and intelligent packaging that monitors product conditions, represent significant long-term growth potential.

Growth Accelerators in the Asia Pacific Flexible Packaging Industry Industry

Several key factors are poised to accelerate the growth trajectory of the Asia Pacific flexible packaging industry. The sustained adoption of advanced and high-performance materials, including bio-based polymers and improved barrier films, will be instrumental. Continuous technological advancements in printing, lamination, and converting technologies, leading to enhanced efficiency, improved aesthetics, and new functionalities, will act as significant growth catalysts. Strategic partnerships and collaborations, aimed at accessing new markets, sharing technological expertise, and developing innovative solutions, will be crucial for expansion. Substantial and focused investments in research and development (R&D) for pioneering sustainable packaging alternatives, smart packaging solutions, and cost-effective production processes will further fuel industry growth and competitiveness.

Key Players Shaping the Asia Pacific Flexible Packaging Industry Market

- Formosa Flexible Packaging Corp

- Berry Plastics Corporation

- Sonoco Products Company

- Wapo Corporation Ltd

- Mondi Group

- Rengo Co Ltd

- Ester Industries Ltd (Wilemina Finance Corporation)

- TCPL Packaging Ltd

- Sealed Air Corporation

- Chuan Peng Enterprise Co Ltd

- Amcor Ltd

Notable Milestones in Asia Pacific Flexible Packaging Industry Sector

- August 2022: Amcor opens an innovation center in Jiangyin, China, focusing on sustainable packaging solutions.

- September 2022: Amcor invests up to USD 45 million in ePac Flexible Packaging, enhancing its digital printing capabilities.

In-Depth Asia Pacific Flexible Packaging Industry Market Outlook

The Asia Pacific flexible packaging market is on a trajectory for substantial and sustained growth over the forecast period. This robust expansion will be primarily driven by the confluence of the previously discussed key drivers, opportunities, and accelerators. Strategic and significant investments in the development and adoption of sustainable packaging materials, coupled with the embrace of cutting-edge technological innovations across the value chain, will be paramount in shaping the industry's future landscape. The market is anticipated to witness a pronounced increase in demand for highly specialized and customized packaging solutions that precisely cater to evolving consumer needs and address growing environmental concerns. Companies that proactively champion sustainable practices, embrace digital transformation, and prioritize innovation in their product development and operational strategies will be best positioned to capitalize on the abundant and substantial growth opportunities present in this dynamic and rapidly evolving regional market.

Asia Pacific Flexible Packaging Industry Segmentation

-

1. Type

- 1.1. Pouches

- 1.2. Bags

- 1.3. Wraps

- 1.4. Other Types

-

2. Material

- 2.1. Plastic

- 2.2. Paper

- 2.3. Aluminum/Composites

-

3. End-user Industry

- 3.1. Food

- 3.2. Beverages

- 3.3. Pharmaceutical and Medical

- 3.4. Household and Personal Care

- 3.5. Other End-user Industries

Asia Pacific Flexible Packaging Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia Pacific Flexible Packaging Industry Regional Market Share

Geographic Coverage of Asia Pacific Flexible Packaging Industry

Asia Pacific Flexible Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Pouches

- 5.1.2. Bags

- 5.1.3. Wraps

- 5.1.4. Other Types

- 5.2. Market Analysis, Insights and Forecast - by Material

- 5.2.1. Plastic

- 5.2.2. Paper

- 5.2.3. Aluminum/Composites

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Food

- 5.3.2. Beverages

- 5.3.3. Pharmaceutical and Medical

- 5.3.4. Household and Personal Care

- 5.3.5. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Asia Pacific Flexible Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Pouches

- 6.1.2. Bags

- 6.1.3. Wraps

- 6.1.4. Other Types

- 6.2. Market Analysis, Insights and Forecast - by Material

- 6.2.1. Plastic

- 6.2.2. Paper

- 6.2.3. Aluminum/Composites

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Food

- 6.3.2. Beverages

- 6.3.3. Pharmaceutical and Medical

- 6.3.4. Household and Personal Care

- 6.3.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Formosa Flexible Packaging Corp

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Berry Plastics Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Sonoco Products Company

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Wapo Corporation Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Mondi Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Rengo Co Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Ester Industries Ltd (Wilemina Finance Corporation)*List Not Exhaustive

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 TCPL Packaging Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Sealed Air Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Chuan Peng Enterprise Co Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Amcor Ltd

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Formosa Flexible Packaging Corp

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia Pacific Flexible Packaging Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Asia Pacific Flexible Packaging Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia Pacific Flexible Packaging Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Asia Pacific Flexible Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 3: Asia Pacific Flexible Packaging Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 4: Asia Pacific Flexible Packaging Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Asia Pacific Flexible Packaging Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Asia Pacific Flexible Packaging Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 7: Asia Pacific Flexible Packaging Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 8: Asia Pacific Flexible Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: China Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Japan Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: South Korea Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: India Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Australia Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: New Zealand Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Indonesia Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Malaysia Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Singapore Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Thailand Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Vietnam Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Philippines Asia Pacific Flexible Packaging Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia Pacific Flexible Packaging Industry?

The projected CAGR is approximately 4.2%.

2. Which companies are prominent players in the Asia Pacific Flexible Packaging Industry?

Key companies in the market include Formosa Flexible Packaging Corp, Berry Plastics Corporation, Sonoco Products Company, Wapo Corporation Ltd, Mondi Group, Rengo Co Ltd, Ester Industries Ltd (Wilemina Finance Corporation)*List Not Exhaustive, TCPL Packaging Ltd, Sealed Air Corporation, Chuan Peng Enterprise Co Ltd, Amcor Ltd.

3. What are the main segments of the Asia Pacific Flexible Packaging Industry?

The market segments include Type, Material, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 301.2 billion as of 2022.

5. What are some drivers contributing to market growth?

Increased Demand for Convenient Packaging; Demand for Longer Shelf Life and Innovative Packaging.

6. What are the notable trends driving market growth?

Food-Packaging Industry to Drive the Market Growth.

7. Are there any restraints impacting market growth?

Concerns about the Environment and Recycling of Packaging Material.

8. Can you provide examples of recent developments in the market?

September 2022: Amcor, a key player in responsible packaging solutions development and production, announced a new strategic investment in ePac Flexible Packaging ("ePac"), a pioneer in high-quality, brief run length digitally-based flexible packaging of up to USD 45 million. Amcor will own more minority shares of ePac Holdings LLC due to the investment.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia Pacific Flexible Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia Pacific Flexible Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia Pacific Flexible Packaging Industry?

To stay informed about further developments, trends, and reports in the Asia Pacific Flexible Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence