Key Insights

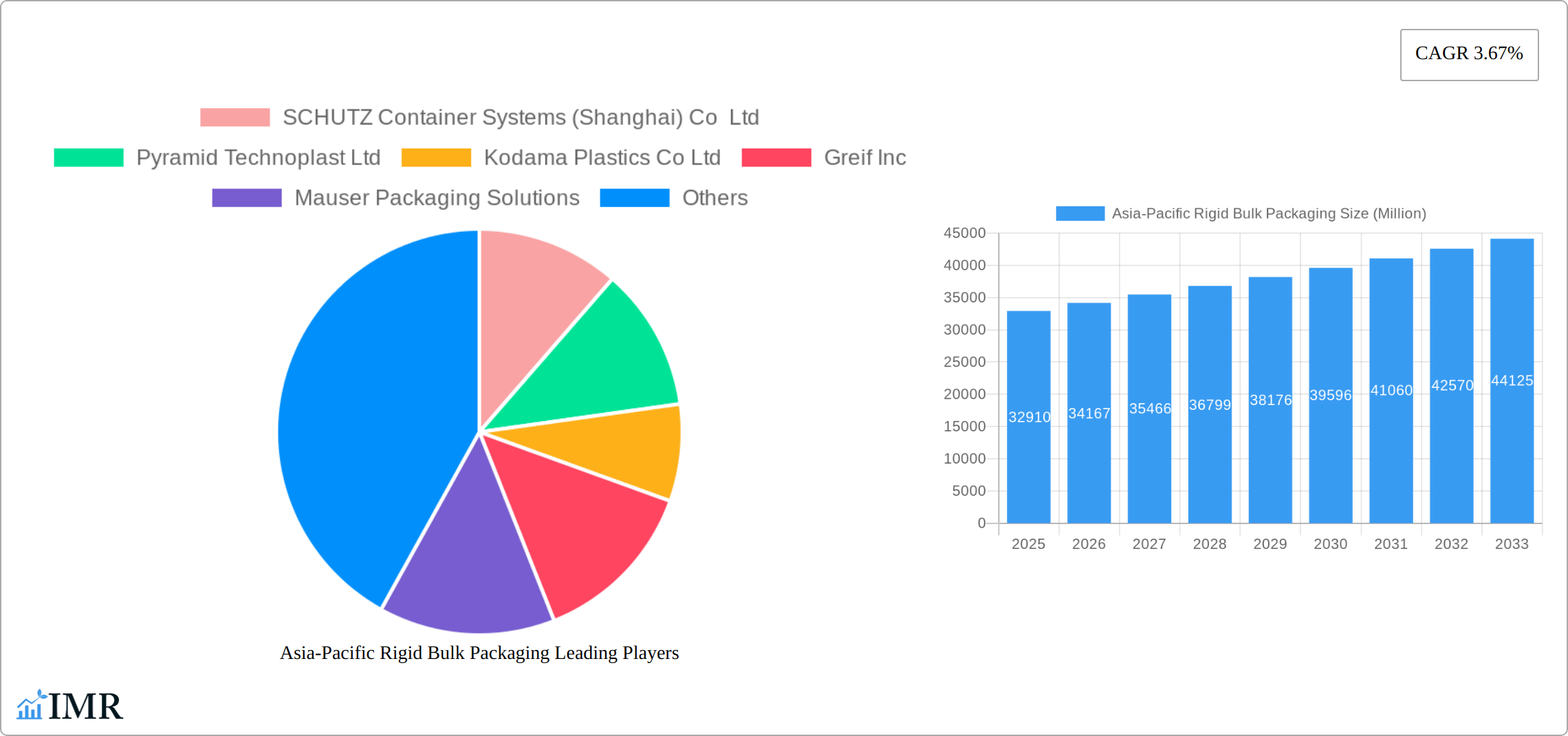

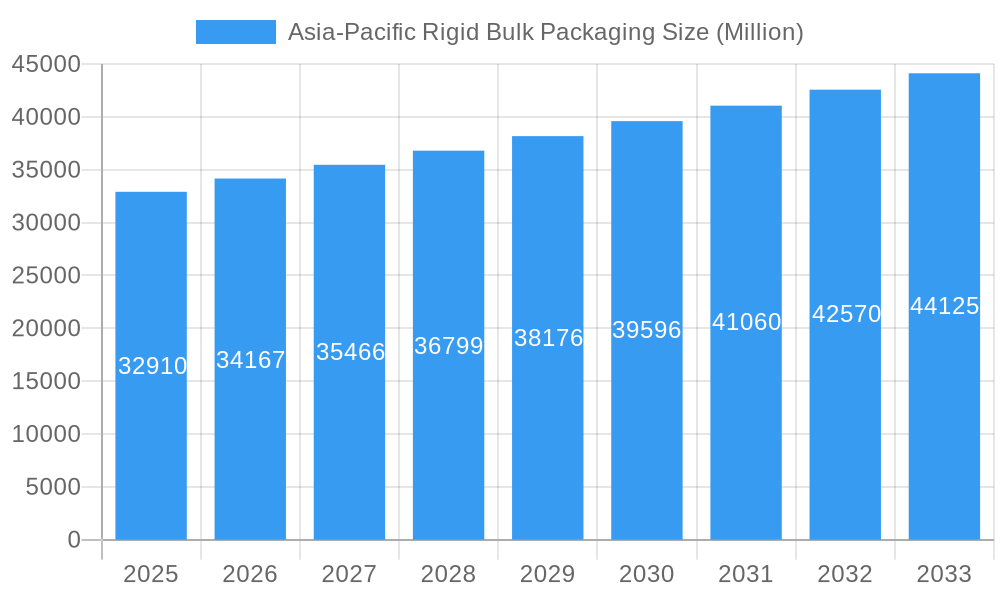

The Asia-Pacific rigid bulk packaging market, valued at $32.91 billion in 2025, is projected to experience steady growth, driven by the region's burgeoning manufacturing and industrial sectors. A Compound Annual Growth Rate (CAGR) of 3.67% from 2025 to 2033 indicates a substantial market expansion over the forecast period. Key drivers include the increasing demand for efficient and safe transportation of goods, particularly in the food and beverage, chemical, and pharmaceutical industries. The rising adoption of sustainable packaging solutions, such as recyclable and reusable containers, is a significant trend shaping the market. Furthermore, advancements in material science are leading to the development of lighter, stronger, and more durable packaging options, contributing to improved logistics and reduced transportation costs. While potential restraints include fluctuations in raw material prices and stringent environmental regulations, the overall growth outlook remains positive, fueled by robust economic growth and infrastructure development across the Asia-Pacific region.

Asia-Pacific Rigid Bulk Packaging Market Size (In Billion)

The market is segmented by material type (plastic, metal, fiberboard, etc.), packaging type (drums, barrels, IBCs, etc.), and end-use industry (chemicals, food & beverage, pharmaceuticals, etc.). Major players like Schutz Container Systems, Greif Inc., Mauser Packaging Solutions, and Time Technoplast Ltd. are shaping the competitive landscape through strategic partnerships, technological innovations, and geographic expansion. The competitive intensity is expected to remain high, necessitating continuous innovation and adaptation to meet evolving customer demands and environmental concerns. Further market segmentation data, while unavailable in the provided information, could reveal crucial insights into specific growth opportunities within various sub-sectors. Understanding these trends allows businesses to effectively tailor their strategies for sustained growth within the Asia-Pacific rigid bulk packaging market.

Asia-Pacific Rigid Bulk Packaging Company Market Share

Asia-Pacific Rigid Bulk Packaging Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Asia-Pacific rigid bulk packaging market, offering invaluable insights for industry professionals, investors, and strategic decision-makers. Covering the period from 2019 to 2033, with a focus on 2025, this report meticulously examines market dynamics, growth trends, key players, and emerging opportunities across diverse segments. The analysis encompasses various industries utilizing rigid bulk packaging, providing a granular understanding of the market landscape. This report is crucial for navigating the complexities of this dynamic sector and capitalizing on its future potential.

Asia-Pacific Rigid Bulk Packaging Market Dynamics & Structure

The Asia-Pacific rigid bulk packaging market is a dynamic and evolving landscape characterized by a moderately consolidated structure. While established key players maintain a significant market presence, the sector is witnessing heightened competition from nimble and innovative smaller enterprises. This section delves into the intricate interplay of competitive forces, technological breakthroughs, prevailing regulatory influences, and emerging market trends that are shaping the future of rigid bulk packaging across the region.

- Market Concentration: The top 5 players are estimated to command approximately 60-65% of the market share in 2025, a figure projected to reach 68-73% by 2033, indicating a trend towards further consolidation.

- Technological Innovation: A strong emphasis is being placed on the development of sustainable, recyclable, and lightweight packaging solutions. Innovations in advanced polymer science, bio-based materials, and enhanced manufacturing processes are crucial for addressing environmental concerns and meeting the evolving demands of environmentally conscious consumers and businesses.

- Regulatory Framework: Increasingly stringent environmental regulations, particularly concerning plastic waste management and the promotion of a circular economy, are a significant driver for the industry. Manufacturers are actively investing in eco-friendly materials, enhanced recycling technologies, and the adoption of reusable packaging models.

- Competitive Substitutes: While rigid bulk packaging holds its own, the market faces competitive pressure from alternative packaging formats, including advanced flexible packaging solutions and innovative paper-based materials, especially in price-sensitive segments and for specific product applications.

- End-User Demographics: The demand for rigid bulk packaging is intrinsically linked to the performance of key end-use sectors, including the chemical, food and beverage, pharmaceutical, agricultural, and construction materials industries. Robust growth and expansion within these sectors directly translate to increased demand for reliable and efficient bulk packaging solutions.

- M&A Trends: The Asia-Pacific rigid bulk packaging market has seen an average of 8-10 M&A deals annually during the historical period (2019-2024). This activity is projected to increase by 15-20% during the forecast period, driven by strategic expansions, technology acquisition, and market consolidation efforts.

Asia-Pacific Rigid Bulk Packaging Growth Trends & Insights

The Asia-Pacific rigid bulk packaging market has witnessed robust growth in recent years, fueled by factors such as industrial expansion, rising consumer spending, and increasing e-commerce activities. Market size, adoption rates, technological disruptions and consumer behaviour shifts are analyzed in detail, with quantitative data providing a clear picture of market evolution.

The market size reached xx Million units in 2024 and is projected to reach xx Million units by 2033, exhibiting a CAGR of xx% during the forecast period (2025-2033). Adoption of sustainable packaging solutions is steadily increasing, driven by governmental regulations and consumer demand. Technological advancements, such as the adoption of smart packaging and automation in manufacturing, are further accelerating market growth. Changing consumer behaviour towards eco-friendly and convenient packaging options are also influencing market trends.

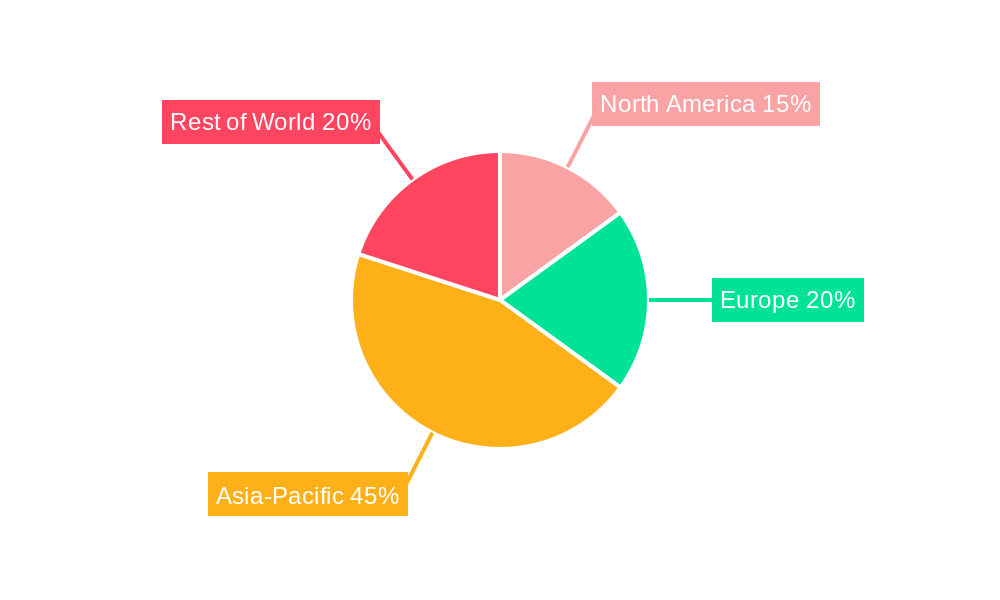

Dominant Regions, Countries, or Segments in Asia-Pacific Rigid Bulk Packaging

China and India are the leading markets for rigid bulk packaging in the Asia-Pacific region. This dominance is driven by the robust growth of their manufacturing sectors, expanding consumer base, and increasing demand for packaged goods across various industries.

- Key Drivers in China: Rapid industrialization, robust infrastructure development, and substantial investment in manufacturing capacities are key growth catalysts.

- Key Drivers in India: A burgeoning middle class with rising disposable incomes, coupled with the growth of organized retail and e-commerce, fuels the demand.

- Other Significant Markets: Southeast Asian nations like Vietnam, Indonesia, and Thailand also show considerable growth potential, driven by economic expansion and increasing industrial activity.

China holds the largest market share, accounting for approximately xx% in 2025 (estimated), followed by India at xx%. However, other countries are expected to experience higher growth rates during the forecast period, narrowing the gap.

Asia-Pacific Rigid Bulk Packaging Product Landscape

The Asia-Pacific rigid bulk packaging market offers a diverse range of products, including drums, pails, IBCs (Intermediate Bulk Containers), and other specialized containers. Recent innovations focus on lightweight designs, improved barrier properties, and enhanced sustainability features such as recyclability and compostability. Manufacturers are increasingly incorporating advanced materials and technologies to optimize performance and reduce environmental impact. Unique selling propositions frequently involve superior strength-to-weight ratios, enhanced chemical resistance, and customized solutions tailored to specific industry needs.

Key Drivers, Barriers & Challenges in Asia-Pacific Rigid Bulk Packaging

Key Drivers:

- Accelerated industrialization and a robust manufacturing base across the Asia-Pacific region continue to fuel demand.

- The growing middle class and evolving consumer lifestyles are driving increased consumption of packaged goods, necessitating bulk packaging solutions.

- A global and regional push towards sustainability, coupled with supportive government policies, encourages the adoption of eco-friendly and circular economy-aligned packaging.

- Technological advancements in material science and manufacturing are enabling the development of more efficient, cost-effective, and sustainable packaging options.

Challenges & Restraints:

- Volatility in the prices of key raw materials, particularly petrochemical-based resins, can significantly impact production costs and profit margins.

- Persistent supply chain disruptions, logistical complexities, and trade barriers in certain sub-regions can hinder timely delivery and market access, affecting operational efficiency.

- Intense competition from both established global players and rapidly growing local manufacturers necessitates continuous investment in innovation, operational efficiency, and competitive pricing strategies.

- The need for significant capital investment in advanced manufacturing technologies and sustainable solutions can pose a barrier for smaller players.

Emerging Opportunities in Asia-Pacific Rigid Bulk Packaging

- Growth in E-commerce: The booming e-commerce sector requires robust and secure packaging solutions, creating substantial demand.

- Sustainable Packaging: The increasing focus on sustainability opens opportunities for biodegradable and recyclable packaging options.

- Specialized Packaging: Growing demand from niche industries, such as pharmaceuticals and healthcare, necessitates the development of specialized packaging solutions.

Growth Accelerators in the Asia-Pacific Rigid Bulk Packaging Industry

Significant growth in the Asia-Pacific rigid bulk packaging industry is being driven by a confluence of factors. Continuous technological advancements, particularly in areas like lightweighting, enhanced barrier properties, and smart packaging, are creating new market opportunities. Strategic alliances and partnerships between raw material suppliers, packaging manufacturers, and end-users are fostering collaborative innovation, improving supply chain resilience, and ensuring the adoption of cutting-edge solutions. Furthermore, the expansion into rapidly developing economies within Southeast Asia and other emerging markets, where industrialization and consumerism are on the rise, presents substantial untapped potential for market penetration and sustained growth.

Key Players Shaping the Asia-Pacific Rigid Bulk Packaging Market

- SCHUTZ Container Systems (Shanghai) Co Ltd

- Pyramid Technoplast Ltd

- Kodama Plastics Co Ltd

- Greif Inc

- Mauser Packaging Solutions

- Manock Industry Co LTD

- Multipac Pty Ltd

- ABCD Drums & Barrels Industries

- Industrial Engineering Corporation

- Yangzhou United Packaging Co Ltd

- Exel Plastech Co Ltd

- Time Technoplast Ltd

- TPL Plastech Limited

- *List Not Exhaustive - This list represents prominent players, but the market includes a wider range of regional and specialized manufacturers.

Notable Milestones in Asia-Pacific Rigid Bulk Packaging Sector

- May 2023: Berry Global significantly enhances its commitment to sustainability and the circular economy by commencing the construction of a new state-of-the-art manufacturing facility and Global Centre of Excellence (COPE) in India, achieving ISCC Plus accreditation for its operations and products.

- May 2023: A landmark collaboration between Lyondell Basell and Shakti Plastic Industries results in the establishment of India's largest mechanical rigid plastic recycling plant, a pivotal development aimed at bolstering the circular economy, addressing plastic waste challenges, and promoting resource efficiency within the packaging sector.

In-Depth Asia-Pacific Rigid Bulk Packaging Market Outlook

The Asia-Pacific rigid bulk packaging market is poised for continued growth, driven by ongoing industrialization, rising consumer demand, and increasing adoption of sustainable packaging solutions. Strategic investments in innovation, sustainable practices, and expansion into high-growth markets will be crucial for success. Opportunities abound for companies that can offer customized solutions, leverage technological advancements, and adapt to evolving regulatory frameworks. The market presents significant potential for both established players and new entrants seeking to capitalize on this dynamic and expanding sector.

Asia-Pacific Rigid Bulk Packaging Segmentation

-

1. Material

- 1.1. Plastic

- 1.2. Metal

- 1.3. Wood

- 1.4. Other Materials

-

2. Product

- 2.1. Industrial Bulk Containers

- 2.2. Drums

- 2.3. Pails

- 2.4. Bulk Boxes

- 2.5. Other Bulk Containers

-

3. End-user Industry

- 3.1. Food

- 3.2. Beverage

- 3.3. Industrial

- 3.4. Pharmaceutical and Chemical

- 3.5. Other End-user Industries

Asia-Pacific Rigid Bulk Packaging Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia-Pacific Rigid Bulk Packaging Regional Market Share

Geographic Coverage of Asia-Pacific Rigid Bulk Packaging

Asia-Pacific Rigid Bulk Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.67% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Plastic

- 5.1.2. Metal

- 5.1.3. Wood

- 5.1.4. Other Materials

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. Industrial Bulk Containers

- 5.2.2. Drums

- 5.2.3. Pails

- 5.2.4. Bulk Boxes

- 5.2.5. Other Bulk Containers

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Food

- 5.3.2. Beverage

- 5.3.3. Industrial

- 5.3.4. Pharmaceutical and Chemical

- 5.3.5. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. Asia-Pacific Rigid Bulk Packaging Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. Plastic

- 6.1.2. Metal

- 6.1.3. Wood

- 6.1.4. Other Materials

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. Industrial Bulk Containers

- 6.2.2. Drums

- 6.2.3. Pails

- 6.2.4. Bulk Boxes

- 6.2.5. Other Bulk Containers

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Food

- 6.3.2. Beverage

- 6.3.3. Industrial

- 6.3.4. Pharmaceutical and Chemical

- 6.3.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 SCHUTZ Container Systems (Shanghai) Co Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Pyramid Technoplast Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Kodama Plastics Co Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Greif Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Mauser Packaging Solutions

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Manock Industry Co LTD

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Multipac Pty Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 ABCD Drums & Barrels Industries

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Industrial Engineering Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Yangzhou United Packaging Co Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Exel Plastech Co Ltd

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Time Technoplast Ltd

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 TPL Plastech Limited*List Not Exhaustive

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 SCHUTZ Container Systems (Shanghai) Co Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia-Pacific Rigid Bulk Packaging Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Rigid Bulk Packaging Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Rigid Bulk Packaging Revenue Million Forecast, by Material 2020 & 2033

- Table 2: Asia-Pacific Rigid Bulk Packaging Volume Billion Forecast, by Material 2020 & 2033

- Table 3: Asia-Pacific Rigid Bulk Packaging Revenue Million Forecast, by Product 2020 & 2033

- Table 4: Asia-Pacific Rigid Bulk Packaging Volume Billion Forecast, by Product 2020 & 2033

- Table 5: Asia-Pacific Rigid Bulk Packaging Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Asia-Pacific Rigid Bulk Packaging Volume Billion Forecast, by End-user Industry 2020 & 2033

- Table 7: Asia-Pacific Rigid Bulk Packaging Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Asia-Pacific Rigid Bulk Packaging Volume Billion Forecast, by Region 2020 & 2033

- Table 9: Asia-Pacific Rigid Bulk Packaging Revenue Million Forecast, by Material 2020 & 2033

- Table 10: Asia-Pacific Rigid Bulk Packaging Volume Billion Forecast, by Material 2020 & 2033

- Table 11: Asia-Pacific Rigid Bulk Packaging Revenue Million Forecast, by Product 2020 & 2033

- Table 12: Asia-Pacific Rigid Bulk Packaging Volume Billion Forecast, by Product 2020 & 2033

- Table 13: Asia-Pacific Rigid Bulk Packaging Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 14: Asia-Pacific Rigid Bulk Packaging Volume Billion Forecast, by End-user Industry 2020 & 2033

- Table 15: Asia-Pacific Rigid Bulk Packaging Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Asia-Pacific Rigid Bulk Packaging Volume Billion Forecast, by Country 2020 & 2033

- Table 17: China Asia-Pacific Rigid Bulk Packaging Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: China Asia-Pacific Rigid Bulk Packaging Volume (Billion) Forecast, by Application 2020 & 2033

- Table 19: Japan Asia-Pacific Rigid Bulk Packaging Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Japan Asia-Pacific Rigid Bulk Packaging Volume (Billion) Forecast, by Application 2020 & 2033

- Table 21: South Korea Asia-Pacific Rigid Bulk Packaging Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: South Korea Asia-Pacific Rigid Bulk Packaging Volume (Billion) Forecast, by Application 2020 & 2033

- Table 23: India Asia-Pacific Rigid Bulk Packaging Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: India Asia-Pacific Rigid Bulk Packaging Volume (Billion) Forecast, by Application 2020 & 2033

- Table 25: Australia Asia-Pacific Rigid Bulk Packaging Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Australia Asia-Pacific Rigid Bulk Packaging Volume (Billion) Forecast, by Application 2020 & 2033

- Table 27: New Zealand Asia-Pacific Rigid Bulk Packaging Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: New Zealand Asia-Pacific Rigid Bulk Packaging Volume (Billion) Forecast, by Application 2020 & 2033

- Table 29: Indonesia Asia-Pacific Rigid Bulk Packaging Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Indonesia Asia-Pacific Rigid Bulk Packaging Volume (Billion) Forecast, by Application 2020 & 2033

- Table 31: Malaysia Asia-Pacific Rigid Bulk Packaging Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Malaysia Asia-Pacific Rigid Bulk Packaging Volume (Billion) Forecast, by Application 2020 & 2033

- Table 33: Singapore Asia-Pacific Rigid Bulk Packaging Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Singapore Asia-Pacific Rigid Bulk Packaging Volume (Billion) Forecast, by Application 2020 & 2033

- Table 35: Thailand Asia-Pacific Rigid Bulk Packaging Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Thailand Asia-Pacific Rigid Bulk Packaging Volume (Billion) Forecast, by Application 2020 & 2033

- Table 37: Vietnam Asia-Pacific Rigid Bulk Packaging Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Vietnam Asia-Pacific Rigid Bulk Packaging Volume (Billion) Forecast, by Application 2020 & 2033

- Table 39: Philippines Asia-Pacific Rigid Bulk Packaging Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Philippines Asia-Pacific Rigid Bulk Packaging Volume (Billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Rigid Bulk Packaging?

The projected CAGR is approximately 3.67%.

2. Which companies are prominent players in the Asia-Pacific Rigid Bulk Packaging?

Key companies in the market include SCHUTZ Container Systems (Shanghai) Co Ltd, Pyramid Technoplast Ltd, Kodama Plastics Co Ltd, Greif Inc, Mauser Packaging Solutions, Manock Industry Co LTD, Multipac Pty Ltd, ABCD Drums & Barrels Industries, Industrial Engineering Corporation, Yangzhou United Packaging Co Ltd, Exel Plastech Co Ltd, Time Technoplast Ltd, TPL Plastech Limited*List Not Exhaustive.

3. What are the main segments of the Asia-Pacific Rigid Bulk Packaging?

The market segments include Material, Product, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 32.91 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Consisting Rise in the Construction Activities in the Asia Pacific Region4.; Robust Demand from the Pharmaceutical. Food and Beverage Sector.

6. What are the notable trends driving market growth?

Demand From the Pharmaceutical and Chemical Industry is Expected to Drive the Market.

7. Are there any restraints impacting market growth?

4.; Consisting Rise in the Construction Activities in the Asia Pacific Region4.; Robust Demand from the Pharmaceutical. Food and Beverage Sector.

8. Can you provide examples of recent developments in the market?

May 2023: Berry Global launched the construction of a new manufacturing facility and Global Centre of Excellence (COPE) in India. The new facility was to receive accreditation for the ISCC (International Sustainability & Carbon Certificate) Plus, which was expected to enable Berry Global to market healthcare clients’ approved packaging and rigid plastic components and to support a circular economy approach based on improved recycling and mass balancing.May 2023: Lyondell Basell and Shakti Plastic Industries entered a strategic partnership to create an automatic plastic recycling facility in India. The plant is expected to be able to handle rigid packaging waste from post-consumer use and will be able to produce around 55,000 tons/year of recycled polyester and polypropylene. This would make the facility India's biggest mechanical rigid plastic recycling plant when it starts up around the end of 2024.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Rigid Bulk Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Rigid Bulk Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Rigid Bulk Packaging?

To stay informed about further developments, trends, and reports in the Asia-Pacific Rigid Bulk Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence