Key Insights

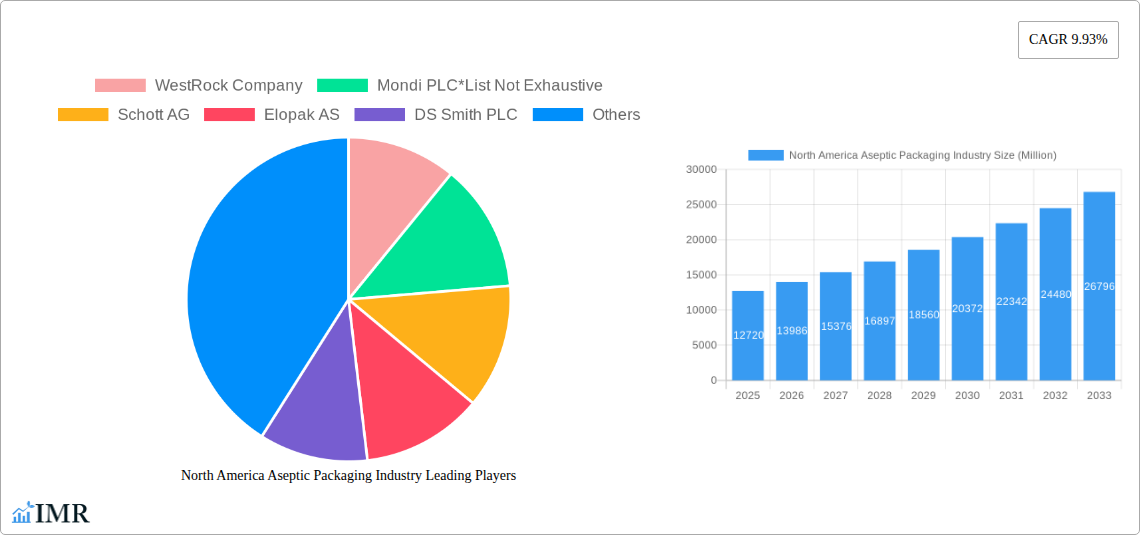

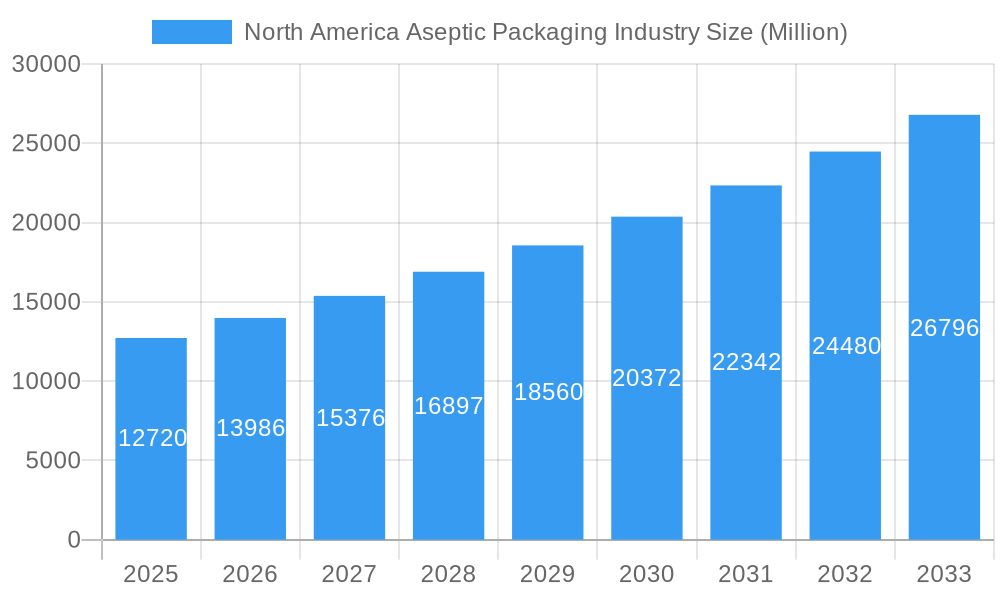

The North American aseptic packaging market, valued at $12.72 billion in 2025, is projected to experience robust growth, driven by the increasing demand for extended shelf-life products within the food and beverage sectors, and a rising focus on hygiene and food safety across the pharmaceutical industry. The market's Compound Annual Growth Rate (CAGR) of 9.93% from 2019 to 2024 indicates significant momentum, a trend expected to continue through 2033. Key drivers include the growing popularity of ready-to-drink beverages, the rising consumption of processed foods, and increasing investments in advanced packaging technologies. The pharmaceutical segment benefits from aseptic packaging's ability to ensure product sterility and integrity, extending shelf-life and preventing contamination. Specific product types like prefillable syringes, vials, and ampoules are experiencing heightened demand within this segment. Within the food industry, aseptic cartons and pouches are gaining traction due to their lightweight nature, cost-effectiveness, and suitability for various products. Geographic growth is concentrated primarily in the United States and Canada, reflecting high consumption levels and robust infrastructure. However, opportunities exist in Mexico and other North American regions as consumer preferences evolve. Competition among established players such as WestRock Company, Mondi PLC, Schott AG, and Amcor Limited is intense, leading to innovation and price competitiveness in the market.

North America Aseptic Packaging Industry Market Size (In Billion)

The North American aseptic packaging market is segmented by end-user type (pharmaceutical, beverage, food), product type (plastic bottles, prefillable syringes, vials, ampoules, bags, pouches, cartons, cups, glass bottles), and country (United States, Canada, Mexico). The prevalence of large multinational companies indicates a sophisticated and established market. The continuous expansion of e-commerce and online grocery shopping is further bolstering demand for convenient, shelf-stable products, indirectly fueling the aseptic packaging market’s growth. While challenges such as fluctuating raw material prices and stringent regulatory compliance requirements exist, the overall growth trajectory for the North American aseptic packaging market remains positive, supported by strong consumer demand, technological advancements, and the inherent benefits of aseptic packaging.

North America Aseptic Packaging Industry Company Market Share

North America Aseptic Packaging Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the North America aseptic packaging market, encompassing market dynamics, growth trends, key players, and future outlook. The study period covers 2019-2033, with 2025 as the base and estimated year. The report is essential for industry professionals, investors, and anyone seeking a deep understanding of this rapidly evolving sector.

Keywords: Aseptic Packaging, North America Aseptic Packaging Market, Aseptic Packaging Market Size, Aseptic Packaging Industry, Food Packaging, Beverage Packaging, Pharmaceutical Packaging, Tetra Pak, Amcor, WestRock, Mondi, Plastic Bottles, Cartons, Pouches, United States Aseptic Packaging, Canada Aseptic Packaging, Market Growth, Market Share, Market Analysis, Industry Trends, Competitive Landscape.

North America Aseptic Packaging Industry Market Dynamics & Structure

This section analyzes the competitive landscape, technological advancements, and regulatory influences shaping the North America aseptic packaging market. The market is characterized by a moderately concentrated structure with key players holding significant market share.

- Market Concentration: The market is moderately concentrated, with the top 5 players accounting for approximately xx% of the total market revenue in 2024.

- Technological Innovation: Continuous innovation in materials science and packaging technology drives market growth. This includes advancements in barrier films, sustainable materials (e.g., plant-based polymers), and intelligent packaging solutions.

- Regulatory Framework: Stringent regulations regarding food safety and environmental sustainability significantly impact packaging choices. Compliance costs and the need for sustainable solutions pose challenges and opportunities.

- Competitive Product Substitutes: Alternative packaging types, such as retort pouches and modified atmosphere packaging (MAP), present competitive pressure. However, aseptic packaging maintains a strong position due to its extended shelf life and hygiene benefits.

- End-User Demographics: The growing demand for convenient, safe, and shelf-stable food and beverages fuels growth across various end-user segments (food, beverage, pharmaceutical). The increasing aging population and evolving consumer preferences also influence market demand.

- M&A Trends: Consolidation is evident, with several mergers and acquisitions occurring in recent years. The number of M&A deals totaled xx in 2024, driving market consolidation and shaping the competitive landscape. For example, the acquisition of xx company by xx company in 2022 enhanced the market concentration.

North America Aseptic Packaging Industry Growth Trends & Insights

The North America aseptic packaging market has witnessed robust growth throughout the historical period (2019-2024) and is poised for continued expansion during the forecast period (2025-2033). The market size reached xx million units in 2024, exhibiting a CAGR of xx% during 2019-2024. This growth is attributed to several key factors:

- Rising Demand for Convenient and Shelf-Stable Products: Consumer preference for convenient and ready-to-eat products drives demand for aseptic packaging, ensuring product safety and extended shelf life.

- Technological Disruptions: Innovations in barrier materials, filling technologies, and sustainable packaging solutions enhance product quality and appeal. The adoption rate of new technologies is growing at xx% annually.

- Shifting Consumer Behavior: Increased health consciousness and a focus on hygiene impact packaging selection. Aseptic packaging aligns with these preferences, providing a safe and secure product.

- Market Penetration: Market penetration of aseptic packaging within the food and beverage sectors has steadily increased, with the highest penetration observed in the dairy segment, followed by beverages and ready meals. This penetration is expected to reach xx% by 2033.

- E-commerce Growth: The growth of online grocery shopping and e-commerce is driving demand for robust and durable packaging that can withstand the transit process.

Dominant Regions, Countries, or Segments in North America Aseptic Packaging Industry

The United States commands a significant share of the North America aseptic packaging market, bolstered by its expansive consumer base and a highly developed food and beverage sector. Canada follows as a key contributor, with its market influenced by evolving consumer preferences and the increasing adoption of advanced packaging solutions. Across end-user segments, the food and beverage industries remain the primary engines of market expansion, fueled by the demand for extended shelf-life and enhanced product safety.

- United States: The dominant position of the US is attributed to its substantial population, a thriving food and beverage industry, and a sophisticated infrastructure that supports widespread adoption of aseptic packaging. High disposable incomes and a growing preference for convenient, ready-to-consume food and beverage options are key market accelerators. The US aseptic packaging market was valued at approximately $XX billion in 2024 and is projected to continue its upward trajectory.

- Canada: While smaller in scale compared to the US, Canada's aseptic packaging market is demonstrating promising growth. This expansion is driven by rising per capita income, an increasing consumer focus on health and convenience, and a growing awareness of the benefits of aseptic packaging in preserving product quality and reducing food waste.

- Food Industry: The food industry represents the largest and most dynamic end-user segment. Aseptic packaging is crucial for preserving the quality and extending the shelf-life of a wide array of products, including dairy items (milk, yogurt, cheese), juices, sauces, soups, ready-to-eat meals, and plant-based alternatives.

- Beverage Industry: The beverage industry is another major market driver, with a substantial demand for aseptically packaged products such as fruit juices, dairy beverages, non-carbonated drinks, and plant-based milk alternatives. The ability to maintain product integrity without refrigeration is a key advantage for this segment.

- Pharmaceutical Industry: Aseptic packaging plays a critical role in the pharmaceutical sector, ensuring the sterility and efficacy of sensitive products like injectables, vaccines, ophthalmic solutions, and oral medications. The stringent regulatory requirements for drug safety and shelf-life further necessitate the use of advanced aseptic packaging solutions.

North America Aseptic Packaging Industry Product Landscape

The aseptic packaging product landscape is diverse, encompassing various formats such as cartons, bottles, pouches, and bags. Key innovations focus on improved barrier properties, sustainable materials, and convenience features. For example, the introduction of lightweight materials is gaining traction, reducing environmental impact and production costs.

Key Drivers, Barriers & Challenges in North America Aseptic Packaging Industry

Key Drivers:

- Enhanced Food Safety and Shelf-Life: The increasing consumer demand for safe, nutritious, and convenient food and beverage products with extended shelf-life is a primary market driver. Aseptic packaging significantly contributes to product safety by eliminating microorganisms without the need for preservatives or extensive refrigeration.

- Technological Innovations: Continuous advancements in material science (e.g., improved barrier properties, sustainable materials) and filling technologies are enhancing the efficiency, cost-effectiveness, and sustainability of aseptic packaging solutions.

- Growing Emphasis on Sustainability: The industry is witnessing a strong push towards sustainable packaging solutions, including the use of recycled materials, lighter-weight packaging, and designs that minimize environmental impact. Aseptic packaging, with its efficient material usage and reduced waste through extended shelf-life, aligns well with these sustainability goals.

- Stringent Food Safety Regulations: Government regulations and international standards prioritizing food safety and quality directly promote the adoption of aseptic packaging, as it inherently ensures product integrity and reduces the risk of spoilage and contamination.

- Demand for Convenience and Portability: Consumers increasingly seek portable and easy-to-use packaging formats for on-the-go consumption, a demand that aseptic packaging effectively addresses with its diverse product forms like pouches, cartons, and bottles.

Challenges & Restraints:

- High Initial Investment Costs: The upfront capital required for sophisticated aseptic processing and filling equipment can be a significant barrier, particularly for smaller manufacturers.

- Environmental Concerns and Waste Management: While offering sustainability benefits, the disposal and recycling of multi-layer aseptic packaging materials continue to be an area of concern and ongoing research, especially regarding plastic waste.

- Supply Chain Volatility and Material Costs: Global supply chain disruptions can impact the availability and cost of raw materials, leading to price fluctuations and potential production delays. These disruptions resulted in an approximate XX% increase in material costs in 2023, impacting profitability.

- Complexity in Material Sourcing: Sourcing specialized, high-performance materials required for aseptic packaging can sometimes be complex and dependent on a limited number of suppliers.

- Consumer Perception and Education: Although awareness is growing, some consumers may still have limited understanding of the benefits and safety of aseptic packaging compared to traditional methods, requiring ongoing educational efforts.

Emerging Opportunities in North America Aseptic Packaging Industry

- Growing demand for sustainable and eco-friendly packaging.

- Rise in demand for flexible packaging solutions.

- Increasing adoption of smart packaging technologies.

- Expansion into niche market segments.

Growth Accelerators in the North America Aseptic Packaging Industry

Long-term growth will be fueled by technological advancements, strategic partnerships, and market expansion into emerging segments. The development of biodegradable and compostable materials will also play a crucial role.

Key Players Shaping the North America Aseptic Packaging Industry Market

- WestRock Company

- Mondi PLC

- Schott AG

- Elopak AS

- DS Smith PLC

- Tetra Pak International S A

- Scholle IPN

- SIG Combibloc Group

- Amcor Limited

- Sealed Air Corporation

- Comar LLC

- Berry Global Inc.

- Greatview Aseptic Packaging Company

Notable Milestones in North America Aseptic Packaging Industry Sector

- 2020: The global COVID-19 pandemic significantly amplified the demand for aseptic packaging. Increased consumer focus on hygiene, long shelf-life, and reduced shopping frequency led to a surge in the purchase of aseptically packaged goods, particularly in essential food and beverage categories.

- 2021: The momentum towards sustainable packaging solutions intensified. Key players in the industry invested heavily in R&D to develop and implement more eco-friendly packaging materials, such as those with higher recycled content, improved recyclability, and reduced carbon footprints.

- 2022: The competitive landscape of the North American aseptic packaging industry underwent significant restructuring through strategic mergers and acquisitions. These consolidations aimed to expand market reach, enhance product portfolios, and achieve greater economies of scale.

- Ongoing: Tetra Pak International SA consistently leads in innovation, introducing advanced filling machinery and cutting-edge technologies. Their focus on enhancing production efficiency and reducing unit costs is exemplified by the introduction of the A1 aseptic filling machine in 20XX, which marked a significant advancement in high-speed, flexible aseptic filling capabilities and positively impacted market dynamics.

- Emergence of New Materials: Continued research and development have led to the introduction of innovative barrier materials and bio-based alternatives, further improving the sustainability profile and performance of aseptic packaging.

In-Depth North America Aseptic Packaging Industry Market Outlook

The North America aseptic packaging market is poised for sustained and robust growth in the foreseeable future. This expansion will be propelled by a confluence of factors, including an ever-increasing consumer appetite for convenient, safe, and shelf-stable food and beverage options, coupled with significant strides in technological innovation within packaging materials and filling processes. The growing imperative for sustainable packaging solutions also presents a substantial opportunity for market participants to align their offerings with evolving environmental consciousness. Key opportunities for industry players lie in forging strategic partnerships, diversifying product portfolios to cater to niche markets, and strategically expanding their presence into emerging geographical areas. The market is projected to reach an impressive valuation of $XX billion (or xx million units) by 2033, presenting substantial growth potential for companies that can adeptly navigate evolving consumer preferences, embrace technological advancements, and champion sustainable practices.

North America Aseptic Packaging Industry Segmentation

-

1. End- User Type

-

1.1. Pharmaceutical Industry

- 1.1.1. Prefillable Syringes

- 1.1.2. Bottles

- 1.1.3. Vials and Ampoules

- 1.1.4. Other Pharmaceutical Industry Types

-

1.2. Beverage Industry

- 1.2.1. Fruit-based

- 1.2.2. Milk and Other Dairy Beverages

- 1.2.3. Ready-to-Drink

- 1.2.4. Other Beverage Industry Types

-

1.3. Food Industry

- 1.3.1. Dairy Food

- 1.3.2. Processed Foods

- 1.3.3. Baby Foods

- 1.3.4. Soups and Broths

- 1.3.5. Other Food Industry Types

-

1.1. Pharmaceutical Industry

-

2. Product Type

- 2.1. Plastic Bottles

- 2.2. Prefillabe Syringes

- 2.3. Vials and Ampoules

- 2.4. Bags and Pouches

- 2.5. Cartons

- 2.6. Cups

- 2.7. Glass Bottles

North America Aseptic Packaging Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

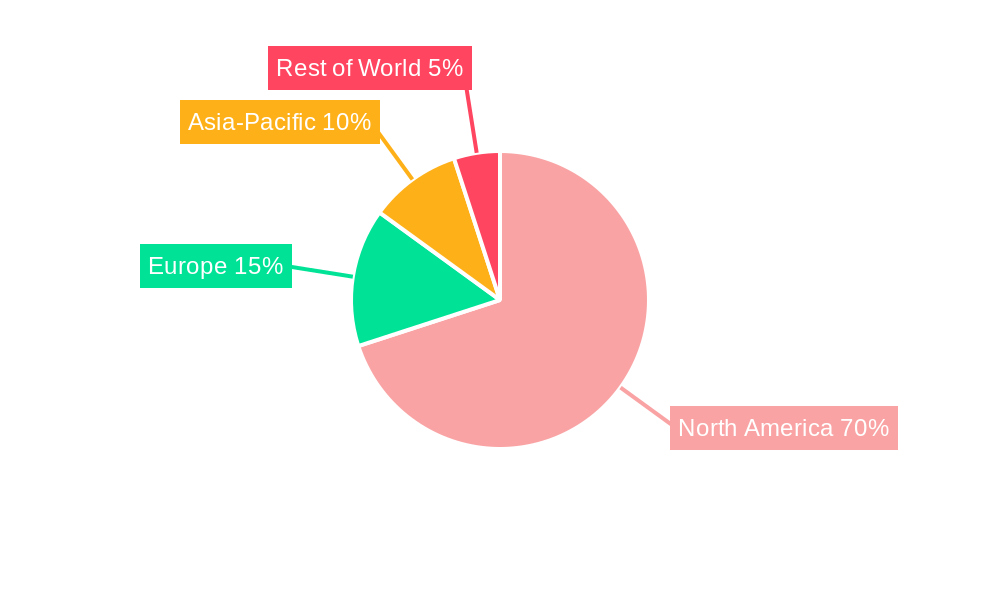

North America Aseptic Packaging Industry Regional Market Share

Geographic Coverage of North America Aseptic Packaging Industry

North America Aseptic Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.93% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End- User Type

- 5.1.1. Pharmaceutical Industry

- 5.1.1.1. Prefillable Syringes

- 5.1.1.2. Bottles

- 5.1.1.3. Vials and Ampoules

- 5.1.1.4. Other Pharmaceutical Industry Types

- 5.1.2. Beverage Industry

- 5.1.2.1. Fruit-based

- 5.1.2.2. Milk and Other Dairy Beverages

- 5.1.2.3. Ready-to-Drink

- 5.1.2.4. Other Beverage Industry Types

- 5.1.3. Food Industry

- 5.1.3.1. Dairy Food

- 5.1.3.2. Processed Foods

- 5.1.3.3. Baby Foods

- 5.1.3.4. Soups and Broths

- 5.1.3.5. Other Food Industry Types

- 5.1.1. Pharmaceutical Industry

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Plastic Bottles

- 5.2.2. Prefillabe Syringes

- 5.2.3. Vials and Ampoules

- 5.2.4. Bags and Pouches

- 5.2.5. Cartons

- 5.2.6. Cups

- 5.2.7. Glass Bottles

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by End- User Type

- 6. North America Aseptic Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End- User Type

- 6.1.1. Pharmaceutical Industry

- 6.1.1.1. Prefillable Syringes

- 6.1.1.2. Bottles

- 6.1.1.3. Vials and Ampoules

- 6.1.1.4. Other Pharmaceutical Industry Types

- 6.1.2. Beverage Industry

- 6.1.2.1. Fruit-based

- 6.1.2.2. Milk and Other Dairy Beverages

- 6.1.2.3. Ready-to-Drink

- 6.1.2.4. Other Beverage Industry Types

- 6.1.3. Food Industry

- 6.1.3.1. Dairy Food

- 6.1.3.2. Processed Foods

- 6.1.3.3. Baby Foods

- 6.1.3.4. Soups and Broths

- 6.1.3.5. Other Food Industry Types

- 6.1.1. Pharmaceutical Industry

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Plastic Bottles

- 6.2.2. Prefillabe Syringes

- 6.2.3. Vials and Ampoules

- 6.2.4. Bags and Pouches

- 6.2.5. Cartons

- 6.2.6. Cups

- 6.2.7. Glass Bottles

- 6.1. Market Analysis, Insights and Forecast - by End- User Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 WestRock Company

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Mondi PLC*List Not Exhaustive

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Schott AG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Elopak AS

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 DS Smith PLC

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Tetra Pak International S A

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Scholle IPN

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 SIG Combibloc Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Amcor Limited

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Sealed Air Corporation

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 WestRock Company

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Aseptic Packaging Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: North America Aseptic Packaging Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Aseptic Packaging Industry Revenue Million Forecast, by End- User Type 2020 & 2033

- Table 2: North America Aseptic Packaging Industry Volume K Tons Forecast, by End- User Type 2020 & 2033

- Table 3: North America Aseptic Packaging Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 4: North America Aseptic Packaging Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 5: North America Aseptic Packaging Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: North America Aseptic Packaging Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: North America Aseptic Packaging Industry Revenue Million Forecast, by End- User Type 2020 & 2033

- Table 8: North America Aseptic Packaging Industry Volume K Tons Forecast, by End- User Type 2020 & 2033

- Table 9: North America Aseptic Packaging Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 10: North America Aseptic Packaging Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 11: North America Aseptic Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: North America Aseptic Packaging Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 13: United States North America Aseptic Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United States North America Aseptic Packaging Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 15: Canada North America Aseptic Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Canada North America Aseptic Packaging Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 17: Mexico North America Aseptic Packaging Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Mexico North America Aseptic Packaging Industry Volume (K Tons) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Aseptic Packaging Industry?

The projected CAGR is approximately 9.93%.

2. Which companies are prominent players in the North America Aseptic Packaging Industry?

Key companies in the market include WestRock Company, Mondi PLC*List Not Exhaustive, Schott AG, Elopak AS, DS Smith PLC, Tetra Pak International S A, Scholle IPN, SIG Combibloc Group, Amcor Limited, Sealed Air Corporation.

3. What are the main segments of the North America Aseptic Packaging Industry?

The market segments include End- User Type, Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.72 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand to Reduce the Cost of Cold Chain Logistics; Increasing Demand for the Longer Shelf Life of Products.

6. What are the notable trends driving market growth?

Beverages Segment is Expected to Hold a Significant Market Share.

7. Are there any restraints impacting market growth?

Manufacturing Complications & Lower ROI.

8. Can you provide examples of recent developments in the market?

Owing to the spread of COVID-19, the market is expected to witness significant growth. Due to the pandemic, customers have shifted towards online retail and panic stocking, which led to an increased demand for essential food items such as milk, baby food, and vegetables. Moreover, the concerns regarding food hygiene due to Covid-19 have been increasing the demand for aseptic packaging. In the coming years, the customers are expected to prefer better packaging to prevent such diseases, which would compel the vendors to think on the lines of sustainable aseptic packaging.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Aseptic Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Aseptic Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Aseptic Packaging Industry?

To stay informed about further developments, trends, and reports in the North America Aseptic Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence