Key Insights

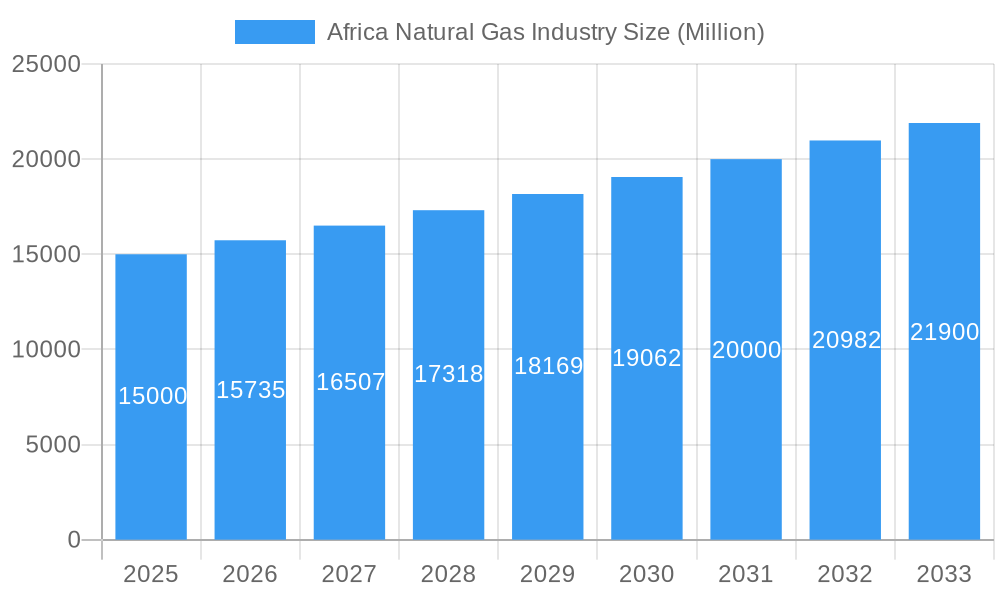

The African natural gas market, currently valued at approximately $XX million (estimated based on industry reports and market trends for similar regions with available data), is experiencing robust growth, projected to maintain a CAGR exceeding 4.50% from 2025 to 2033. This expansion is fueled by several key drivers. Increasing energy demands across diverse sectors—power generation, industrial processes, and residential consumption—are significantly boosting natural gas consumption. Furthermore, government initiatives promoting energy diversification and infrastructure development, coupled with discoveries of new gas reserves, are creating favorable conditions for investment and market expansion. The South African, Sudanese, Ugandan, Tanzanian, and Kenyan markets are leading the charge, representing substantial regional market shares. However, challenges such as infrastructure limitations in certain regions and fluctuating global energy prices pose potential restraints on growth. The market is segmented geographically across North, West, Central, East, and Southern Africa and by end-user (power generation, industrial, residential) and company size (large, medium, small). Major players like Shell PLC, TotalEnergies SE, Sonatrach, and Nigerian National Petroleum Corporation are actively shaping the market landscape through exploration, production, and distribution.

Africa Natural Gas Industry Market Size (In Billion)

The diverse nature of the African landscape creates both opportunities and hurdles for natural gas development. While substantial reserves exist, their exploitation requires significant investment in pipeline infrastructure and distribution networks. Moreover, political stability and regulatory frameworks play a vital role in attracting foreign investment and ensuring sustainable growth. The market's future hinges on successfully addressing these challenges and fostering collaboration between governments, private sector entities, and international organizations to unlock the full potential of Africa's natural gas resources. This will involve continued exploration for new reserves, strategic infrastructure development, and policy frameworks that encourage both domestic consumption and export opportunities. The long-term outlook remains positive, with substantial potential for growth and a significant role to play in meeting Africa's rising energy needs and fostering economic development.

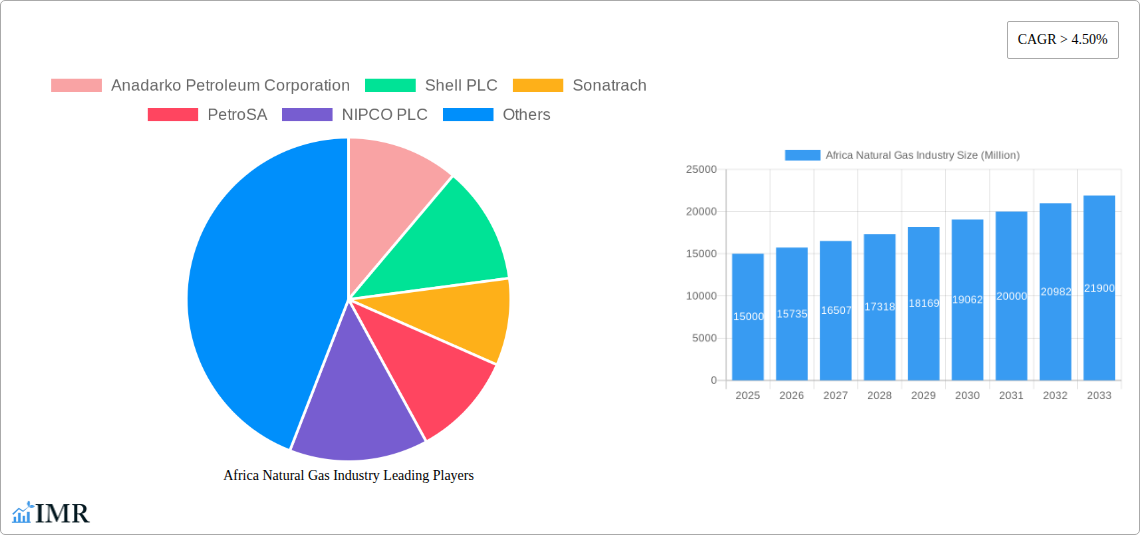

Africa Natural Gas Industry Company Market Share

Africa Natural Gas Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the African natural gas industry, covering market dynamics, growth trends, dominant players, and future outlook. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. This report is essential for industry professionals, investors, and policymakers seeking to understand and capitalize on opportunities within this dynamic sector.

Keywords: Africa natural gas market, natural gas industry Africa, African gas market analysis, natural gas consumption Africa, natural gas exploration Africa, gas pipeline Africa, Nigeria-Morocco gas pipeline, Sonatrach, Eni, TotalEnergies, Shell, North Africa gas, West Africa gas, East Africa gas, Southern Africa gas, power generation, industrial gas, residential gas, African energy market, LNG Africa, natural gas production Africa, gas market size Africa, African gas infrastructure.

Africa Natural Gas Industry Market Dynamics & Structure

The African natural gas market is characterized by a complex interplay of factors influencing its structure and growth. Market concentration varies significantly across regions, with some dominated by national oil companies (NOCs) while others see greater participation from international players. Technological innovation, though present, faces hurdles such as limited infrastructure and funding. Regulatory frameworks differ across nations, impacting investment and production. The market also contends with competitive substitutes like renewable energy sources. End-user demographics, primarily driven by increasing urbanization and industrialization, are a key growth driver. Finally, mergers and acquisitions (M&A) activity, while not extensive, plays a role in shaping market dynamics.

- Market Concentration: Highly variable across regions; NOCs hold significant shares in several nations, while international players like Shell and TotalEnergies have substantial influence in others. xx% of the market is controlled by the top 5 players in 2025.

- Technological Innovation: Driven by exploration and production techniques, including improved seismic imaging and drilling technologies. Barriers include funding constraints and a shortage of skilled labor.

- Regulatory Frameworks: Vary considerably across countries, influencing investment decisions and exploration activities. Inconsistencies hinder regional integration and standardization.

- Competitive Substitutes: Renewable energy sources like solar and wind power pose a growing competitive threat, especially in areas with abundant sunlight and wind resources.

- End-User Demographics: Increasing urbanization and industrialization fuel demand, particularly in power generation and industrial sectors. Residential consumption is also growing, albeit more slowly.

- M&A Trends: Moderate activity observed in recent years, mainly focused on exploration and production assets, and strategic partnerships. xx M&A deals were recorded between 2019 and 2024.

Africa Natural Gas Industry Growth Trends & Insights

The African natural gas market is experiencing substantial growth, driven by a combination of factors. Market size has exhibited a significant expansion over the past five years, primarily due to rising energy demand, increasing exploration and production activities, and supportive government policies in several nations. The Compound Annual Growth Rate (CAGR) from 2019-2024 stood at xx%, and is projected to remain strong at xx% during 2025-2033. This expansion is visible in higher adoption rates across different end-use sectors. Technological disruptions, mainly in upstream activities, have boosted extraction efficiency, while downstream developments focus on improving pipeline infrastructure and gas processing capabilities. Shifts in consumer behavior, particularly toward more efficient gas utilization technologies, are also contributing to growth.

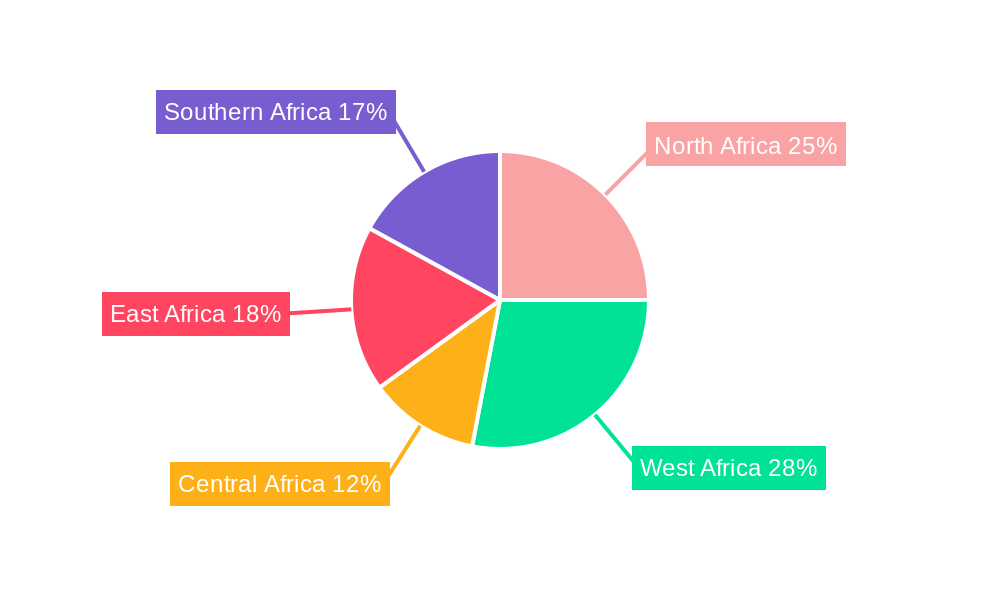

Dominant Regions, Countries, or Segments in Africa Natural Gas Industry

North Africa (primarily Algeria and Egypt) currently dominates the African natural gas market, fueled by substantial reserves and established production infrastructure. However, West Africa is showing significant growth potential, driven by major gas discoveries and ongoing infrastructural developments. The power generation sector is the largest end-user, followed by the industrial sector. Large companies dominate the market, given the capital-intensive nature of the industry.

- Leading Region: North Africa (market share xx% in 2025) benefits from established infrastructure and large reserves.

- Leading Country: Algeria (market share xx% of North Africa in 2025) leads due to its substantial gas reserves and export capabilities.

- Leading Segment (End-User): Power generation (market share xx% in 2025) remains the dominant consumer, driven by increasing electricity demand.

- Leading Segment (Company Size): Large companies (market share xx% in 2025) continue to dominate due to access to capital and technology.

- Key Drivers (North Africa): Established infrastructure, substantial gas reserves, and existing export pipelines.

- Key Drivers (West Africa): Recent large gas discoveries, government support for infrastructure development, and rising domestic demand.

- Key Drivers (Power Generation): Growing electricity demand in urban areas and industrial centers.

Africa Natural Gas Industry Product Landscape

The African natural gas industry's product landscape encompasses natural gas in various forms, including pipeline gas, liquefied natural gas (LNG), and compressed natural gas (CNG). Recent innovations focus on improving the efficiency of gas extraction, processing, and transportation, along with developing cleaner burning technologies and minimizing methane emissions. Unique selling propositions often center around the reliability and affordability of natural gas compared to other energy sources. Technological advancements, such as the adoption of advanced drilling techniques and improved pipeline infrastructure, are driving efficiency and reducing operational costs.

Key Drivers, Barriers & Challenges in Africa Natural Gas Industry

Key Drivers:

- Rising energy demand fueled by population growth and industrialization.

- Government initiatives promoting gas development and infrastructure investment.

- Significant gas discoveries in several African countries.

- Growing demand for cleaner energy sources relative to coal.

Key Challenges:

- Inadequate infrastructure limiting efficient gas transportation and distribution (estimated infrastructure deficit of xx Million USD in 2025).

- Regulatory inconsistencies and uncertainties across different countries hindering investment.

- Security concerns in certain regions impacting exploration and production activities.

- Competition from renewable energy sources and increasing energy efficiency improvements.

Emerging Opportunities in Africa Natural Gas Industry

- Development of regional gas pipelines to facilitate cross-border trade and enhance energy security.

- Growth in the LNG sector for export and domestic consumption.

- Expansion of gas-to-power projects to meet rising electricity demand.

- Increased investment in gas processing and distribution infrastructure.

- Growing potential for CNG in the transportation sector.

Growth Accelerators in the Africa Natural Gas Industry

Long-term growth in the African natural gas industry will be fueled by sustained investment in exploration and production, strategic partnerships between international and national players, and a concerted effort to improve infrastructure. Technological advancements in gas processing and transportation, as well as the development of new gas-based industries, will play a significant role in unlocking further market potential. Government policies promoting energy diversification and energy security will further incentivize growth.

Key Players Shaping the Africa Natural Gas Industry Market

- Anadarko Petroleum Corporation

- Shell PLC

- Sonatrach

- PetroSA

- NIPCO PLC

- TotalEnergies SE

- Egyptian Natural Gas Holding Company

- Eni SpA

- Nigerian National Petroleum Corporation

- Chevron Corporation

Notable Milestones in Africa Natural Gas Industry Sector

- September 2022: Nigerian National Petroleum Company Limited (NNPCL) announces MoU for the 7,000-kilometer Nigeria-Morocco gas pipeline project, aiming to increase gas supply to Europe.

- May 2022: Sonatrach and Eni sign MoU to accelerate gas field development in Algeria, targeting an additional 3 billion cubic meters of annual gas export through the Transmed pipeline.

In-Depth Africa Natural Gas Industry Market Outlook

The future of the African natural gas industry is promising, with significant growth potential driven by rising energy demand, ongoing exploration activities, and investments in infrastructure development. Strategic partnerships and technological advancements will further accelerate market expansion. The focus on gas-to-power projects and the growing interest in LNG export will shape the market's future trajectory. However, addressing infrastructure gaps and promoting regional energy cooperation will be crucial for sustainable and inclusive growth.

Africa Natural Gas Industry Segmentation

-

1. Geography

- 1.1. Nigeria

- 1.2. Algeria

- 1.3. Egypt

- 1.4. South Africa

- 1.5. Rest of Africa

Africa Natural Gas Industry Segmentation By Geography

- 1. Nigeria

- 2. Algeria

- 3. Egypt

- 4. South Africa

- 5. Rest of Africa

Africa Natural Gas Industry Regional Market Share

Geographic Coverage of Africa Natural Gas Industry

Africa Natural Gas Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 4.50% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Geography

- 5.1.1. Nigeria

- 5.1.2. Algeria

- 5.1.3. Egypt

- 5.1.4. South Africa

- 5.1.5. Rest of Africa

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Nigeria

- 5.2.2. Algeria

- 5.2.3. Egypt

- 5.2.4. South Africa

- 5.2.5. Rest of Africa

- 5.1. Market Analysis, Insights and Forecast - by Geography

- 6. Africa Natural Gas Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Geography

- 6.1.1. Nigeria

- 6.1.2. Algeria

- 6.1.3. Egypt

- 6.1.4. South Africa

- 6.1.5. Rest of Africa

- 6.1. Market Analysis, Insights and Forecast - by Geography

- 7. Nigeria Africa Natural Gas Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Geography

- 7.1.1. Nigeria

- 7.1.2. Algeria

- 7.1.3. Egypt

- 7.1.4. South Africa

- 7.1.5. Rest of Africa

- 7.1. Market Analysis, Insights and Forecast - by Geography

- 8. Algeria Africa Natural Gas Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Geography

- 8.1.1. Nigeria

- 8.1.2. Algeria

- 8.1.3. Egypt

- 8.1.4. South Africa

- 8.1.5. Rest of Africa

- 8.1. Market Analysis, Insights and Forecast - by Geography

- 9. Egypt Africa Natural Gas Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Geography

- 9.1.1. Nigeria

- 9.1.2. Algeria

- 9.1.3. Egypt

- 9.1.4. South Africa

- 9.1.5. Rest of Africa

- 9.1. Market Analysis, Insights and Forecast - by Geography

- 10. South Africa Africa Natural Gas Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Geography

- 10.1.1. Nigeria

- 10.1.2. Algeria

- 10.1.3. Egypt

- 10.1.4. South Africa

- 10.1.5. Rest of Africa

- 10.1. Market Analysis, Insights and Forecast - by Geography

- 11. Rest of Africa Africa Natural Gas Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Geography

- 11.1.1. Nigeria

- 11.1.2. Algeria

- 11.1.3. Egypt

- 11.1.4. South Africa

- 11.1.5. Rest of Africa

- 11.1. Market Analysis, Insights and Forecast - by Geography

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Anadarko Petroleum Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Shell PLC

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Sonatrach

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 PetroSA

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 NIPCO PLC

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 TotalEnergies SE

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Egyptian Natural Gas Holding Company

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Eni SpA

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Nigerian National Petroleum Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Chevron Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Anadarko Petroleum Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Africa Natural Gas Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Africa Natural Gas Industry Share (%) by Company 2025

List of Tables

- Table 1: Africa Natural Gas Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 2: Africa Natural Gas Industry Volume Tonnes Forecast, by Geography 2020 & 2033

- Table 3: Africa Natural Gas Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Africa Natural Gas Industry Volume Tonnes Forecast, by Region 2020 & 2033

- Table 5: Africa Natural Gas Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 6: Africa Natural Gas Industry Volume Tonnes Forecast, by Geography 2020 & 2033

- Table 7: Africa Natural Gas Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 8: Africa Natural Gas Industry Volume Tonnes Forecast, by Country 2020 & 2033

- Table 9: Africa Natural Gas Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 10: Africa Natural Gas Industry Volume Tonnes Forecast, by Geography 2020 & 2033

- Table 11: Africa Natural Gas Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Africa Natural Gas Industry Volume Tonnes Forecast, by Country 2020 & 2033

- Table 13: Africa Natural Gas Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 14: Africa Natural Gas Industry Volume Tonnes Forecast, by Geography 2020 & 2033

- Table 15: Africa Natural Gas Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Africa Natural Gas Industry Volume Tonnes Forecast, by Country 2020 & 2033

- Table 17: Africa Natural Gas Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 18: Africa Natural Gas Industry Volume Tonnes Forecast, by Geography 2020 & 2033

- Table 19: Africa Natural Gas Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 20: Africa Natural Gas Industry Volume Tonnes Forecast, by Country 2020 & 2033

- Table 21: Africa Natural Gas Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 22: Africa Natural Gas Industry Volume Tonnes Forecast, by Geography 2020 & 2033

- Table 23: Africa Natural Gas Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Africa Natural Gas Industry Volume Tonnes Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Africa Natural Gas Industry?

The projected CAGR is approximately > 4.50%.

2. Which companies are prominent players in the Africa Natural Gas Industry?

Key companies in the market include Anadarko Petroleum Corporation, Shell PLC, Sonatrach, PetroSA, NIPCO PLC, TotalEnergies SE, Egyptian Natural Gas Holding Company, Eni SpA, Nigerian National Petroleum Corporation, Chevron Corporation.

3. What are the main segments of the Africa Natural Gas Industry?

The market segments include Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Amount of Waste Generation. Growing Concern for Waste Management to Meet the Needs for Sustainable Urban Living4.; Increasing Focus on Non-fossil Fuel Sources of Energy.

6. What are the notable trends driving market growth?

Governments Moving Towards the Cleaner Energy Sources is Driving the Market.

7. Are there any restraints impacting market growth?

4.; Expensive Nature of Incinerators.

8. Can you provide examples of recent developments in the market?

In September 2022, The Nigerian National Petroleum Company Limited (NNPCL) announced its intention to sign a Memorandum of Understanding (MoU) on developing a gas pipeline with Morocco's National Office of Hydrocarbons and Mines and the commission of the Economic Community of West African States (ECOWAS). As a result of the MoU, the 7,000-kilometre Nigeria-Morocco gas pipeline project is expected to ramp up gas supply to Europe. Upon the project completion, 3 billion standard cubic feet of gas is expected to be supplied along the coast of West Africa from Nigeria, Benin, Togo, Ghana, Cote d'Ivoire, Liberia, Sierra Leone, Guinea, Guinea Bissau, Gambia, Senegal, Mauritania to Morocco.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Tonnes.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Africa Natural Gas Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Africa Natural Gas Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Africa Natural Gas Industry?

To stay informed about further developments, trends, and reports in the Africa Natural Gas Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence