Key Insights

The Canadian coal market is projected to witness moderate growth, with a Compound Annual Growth Rate (CAGR) of 5.2%. The market is currently valued at approximately $11 billion in 2024. Sustained demand from key sectors such as metallurgy and residual needs in power generation will drive market expansion. Metallurgy remains a critical application, with coal essential for specific processes despite the rise of alternatives. While the power sector is transitioning to renewables, a baseline demand for coal persists, especially in areas with limited clean energy infrastructure. The 'Others' segment, including cement production and industrial heating, also contributes to market volume. However, significant challenges persist. Stringent environmental regulations targeting carbon emission reductions are heavily influencing coal production and consumption. Increased compliance costs, coupled with the growing competitiveness of renewable energy and global decarbonization efforts, act as considerable restraints. This necessitates strategic adaptation within the Canadian coal industry, potentially through a focus on high-value products, operational efficiency, and the exploration of carbon capture and storage technologies.

Canada Coal Industry Market Size (In Billion)

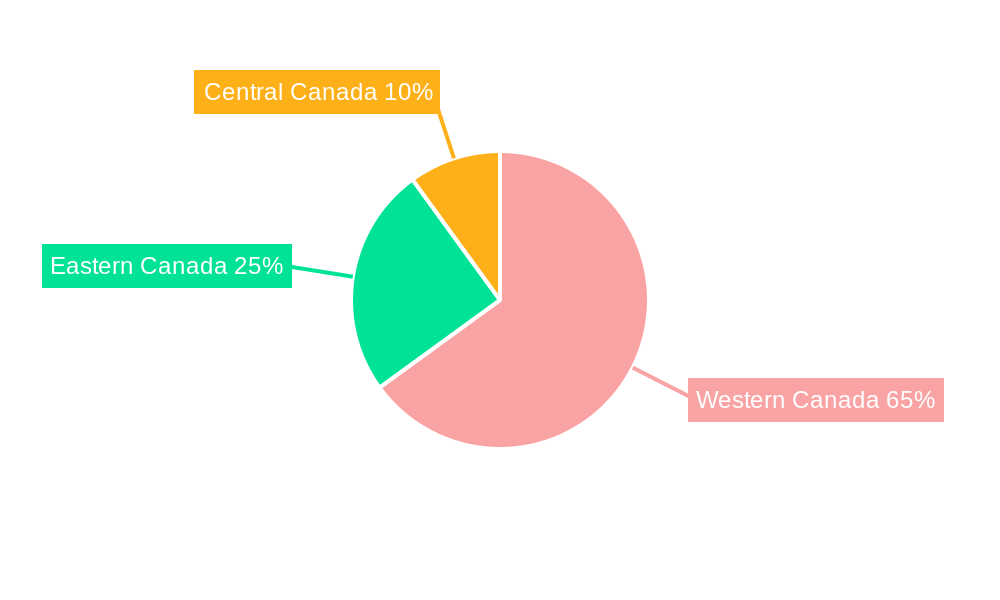

Geographical distribution highlights Western Canada's dominance due to substantial coal reserves, leading in market share over Eastern and Central regions. Key industry players, including Teck Resources Limited and Conuma Coal Resources Limited, primarily operate in Western Canada, shaping market dynamics. The competitive landscape is relatively concentrated, with a few major entities dominating. Future growth will be contingent on the industry's ability to adapt to evolving regulations, enhance operational efficiency, and develop new business models for long-term viability amidst a dynamic energy market. The forecast period will observe a continued emphasis on sustainability, impacting both coal production and consumption patterns.

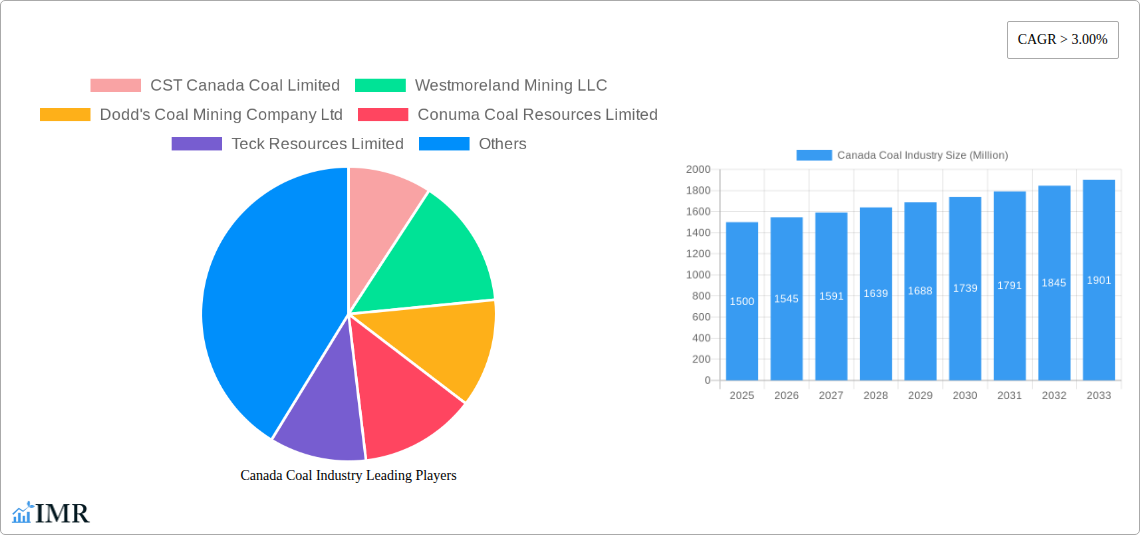

Canada Coal Industry Company Market Share

Canada Coal Industry Market Report: 2019-2033

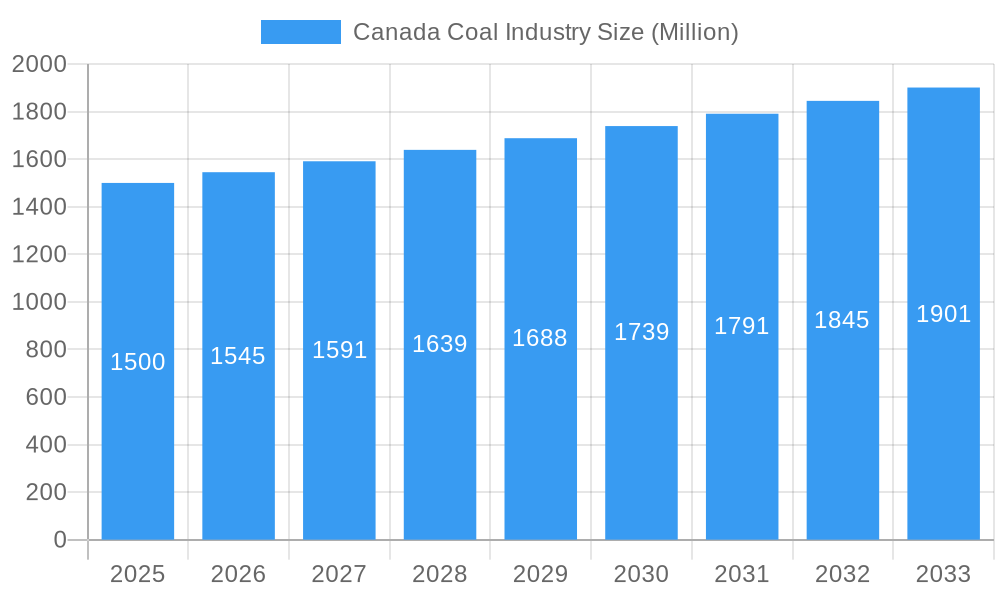

This comprehensive report provides a detailed analysis of the Canadian coal industry, encompassing market dynamics, growth trends, key players, and future outlook. The study period covers 2019-2033, with 2025 as the base and estimated year. The forecast period spans 2025-2033, and the historical period encompasses 2019-2024. This report is crucial for investors, industry professionals, and policymakers seeking a deep understanding of this evolving sector. Market values are presented in millions.

Canada Coal Industry Market Dynamics & Structure

The Canadian coal industry presents a complex interplay of factors influencing its structure and dynamics. Market concentration is moderate, with several key players holding significant shares, but a fragmented landscape comprising smaller independent mines. Technological innovation, while present, faces barriers including high capital investment needs and regulatory hurdles. Stringent environmental regulations form the core of the regulatory framework, impacting production and operational costs. Natural gas and renewable energy sources represent significant competitive product substitutes, constantly challenging coal's market share. End-user demographics primarily consist of power generation and metallurgical sectors, with varying sensitivity to coal price fluctuations. M&A activity has been relatively subdued in recent years, with a total deal volume of xx million in the last five years, reflecting consolidation and strategic adjustments within the industry.

- Market Concentration: Moderate, with Teck Resources Limited and Peabody Energy Corp holding the largest shares (xx% and xx%, respectively, in 2024).

- Technological Innovation: Slow adoption of advanced technologies due to high initial costs.

- Regulatory Framework: Stringent environmental regulations impacting operational costs and production.

- Competitive Substitutes: Natural gas and renewable energy sources pose significant competition.

- End-User Demographics: Primarily Power Generation (xx%) and Metallurgy (xx%), with 'Others' comprising xx%.

- M&A Trends: Limited activity in recent years, with a total deal volume of approximately xx million over the past five years.

Canada Coal Industry Growth Trends & Insights

The Canadian coal industry experienced a period of decline during the historical period (2019-2024), primarily driven by decreasing demand from the power generation sector and increased competition from cleaner energy sources. However, the forecast period (2025-2033) projects a more nuanced growth trajectory. While overall demand might remain subdued, specific segments, particularly metallurgical coal, may experience moderate growth fueled by increasing global steel production. Technological disruptions, focusing on improved mine efficiency and reduced environmental impact, will be a key determinant of growth. Consumer behavior shifts towards environmentally friendly energy options continue to pose a significant challenge. The projected CAGR for the forecast period is estimated at xx%, while market penetration is anticipated to remain relatively stable.

Dominant Regions, Countries, or Segments in Canada Coal Industry

British Columbia remains the dominant region for coal production in Canada, benefiting from established infrastructure and significant reserves. The metallurgical coal segment exhibits the strongest growth potential, driven by sustained demand from the global steel industry. While power generation continues to utilize coal, its share is gradually decreasing due to government policies promoting renewable energy.

- Key Drivers in British Columbia: Existing infrastructure, abundant coal reserves, and proximity to export terminals.

- Metallurgical Coal Segment Dominance: Strong global demand for steel and limited alternative materials.

- Power Generation Segment Challenges: Increasing competition from renewable energy and stricter environmental regulations.

Canada Coal Industry Product Landscape

The Canadian coal industry primarily produces metallurgical and thermal coal. Recent innovations focus on improving coal quality for specific applications, enhancing efficiency in mining operations and reducing environmental impact through improved emission control technologies. Key selling propositions include consistent quality, reliable supply, and competitive pricing.

Key Drivers, Barriers & Challenges in Canada Coal Industry

Key Drivers:

- Growing global demand for metallurgical coal, particularly from Asia.

- Continued reliance on coal for power generation in certain regions.

- Investments in mine optimization and emission control technologies.

Key Barriers & Challenges:

- Stringent environmental regulations increasing operational costs.

- Competition from renewable energy sources eroding market share.

- Fluctuations in global coal prices affecting profitability.

- Supply chain disruptions impacting transportation and logistics. This has led to an estimated xx% increase in transportation costs in the past year.

Emerging Opportunities in Canada Coal Industry

Opportunities exist in exploring untapped reserves, developing higher-value coal products, and investing in carbon capture technologies to reduce environmental impact. Additionally, strategic partnerships with steel manufacturers to secure long-term supply contracts present significant potential.

Growth Accelerators in the Canada Coal Industry Industry

Technological advancements in mining and processing will drive efficiency gains. Strategic collaborations with international steel producers can secure supply contracts, ensuring stable revenue streams. Expanding into new export markets, especially in Asia, can boost overall growth.

Key Players Shaping the Canada Coal Industry Market

- Teck Resources Limited

- Peabody Energy Corp

- CST Canada Coal Limited

- Westmoreland Mining LLC

- Dodd's Coal Mining Company Ltd

- Conuma Coal Resources Limited

Notable Milestones in Canada Coal Industry Sector

- 2020: Increased focus on environmental regulations and sustainability initiatives.

- 2021: Several smaller coal mines ceased operation due to economic pressure.

- 2022: Investment in carbon capture technologies announced by Teck Resources.

- 2023: New export agreements signed by major coal producers.

In-Depth Canada Coal Industry Market Outlook

The Canadian coal industry's future hinges on adapting to the evolving global energy landscape. Continued investment in efficiency improvements, strategic partnerships, and responsible environmental practices will determine long-term success. The industry’s ability to maintain its competitiveness within a shifting global energy market will be pivotal. Growth will depend on the balance between metallurgical coal's sustained demand and the ongoing decline in thermal coal usage. The projected market size in 2033 is estimated at xx million.

Canada Coal Industry Segmentation

-

1. Application

- 1.1. Metallurgy

- 1.2. Power Generation

- 1.3. Others

Canada Coal Industry Segmentation By Geography

- 1. Canada

Canada Coal Industry Regional Market Share

Geographic Coverage of Canada Coal Industry

Canada Coal Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Metallurgy

- 5.1.2. Power Generation

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Canada Coal Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Metallurgy

- 6.1.2. Power Generation

- 6.1.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 CST Canada Coal Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Westmoreland Mining LLC

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Dodd's Coal Mining Company Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Conuma Coal Resources Limited

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Teck Resources Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Peabody Energy Corp

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.1 CST Canada Coal Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Canada Coal Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Canada Coal Industry Share (%) by Company 2025

List of Tables

- Table 1: Canada Coal Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Canada Coal Industry Volume Tonnes Forecast, by Application 2020 & 2033

- Table 3: Canada Coal Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Canada Coal Industry Volume Tonnes Forecast, by Region 2020 & 2033

- Table 5: Canada Coal Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Canada Coal Industry Volume Tonnes Forecast, by Application 2020 & 2033

- Table 7: Canada Coal Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 8: Canada Coal Industry Volume Tonnes Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Coal Industry?

The projected CAGR is approximately 5.2%.

2. Which companies are prominent players in the Canada Coal Industry?

Key companies in the market include CST Canada Coal Limited, Westmoreland Mining LLC, Dodd's Coal Mining Company Ltd, Conuma Coal Resources Limited, Teck Resources Limited, Peabody Energy Corp.

3. What are the main segments of the Canada Coal Industry?

The market segments include Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 11 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Rising Industrialization across the Globe4.; Increasing Utilization of Natural Gas.

6. What are the notable trends driving market growth?

Metallurgy Sector to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; High Cost of Installation and Maintenance.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in Tonnes.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Coal Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Coal Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Coal Industry?

To stay informed about further developments, trends, and reports in the Canada Coal Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence